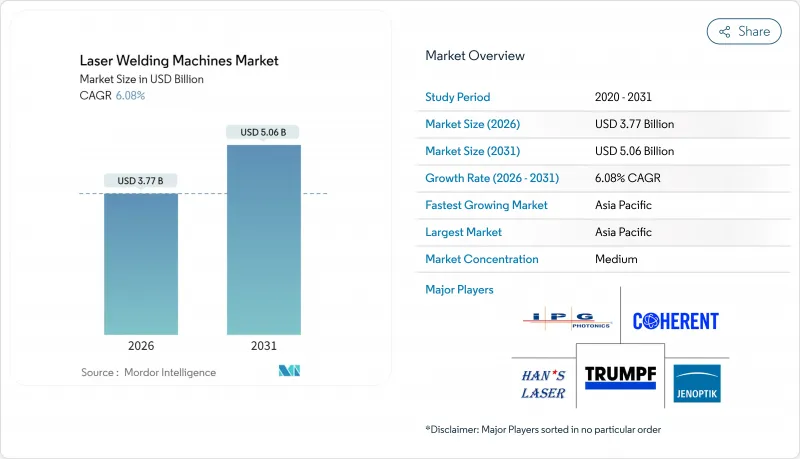

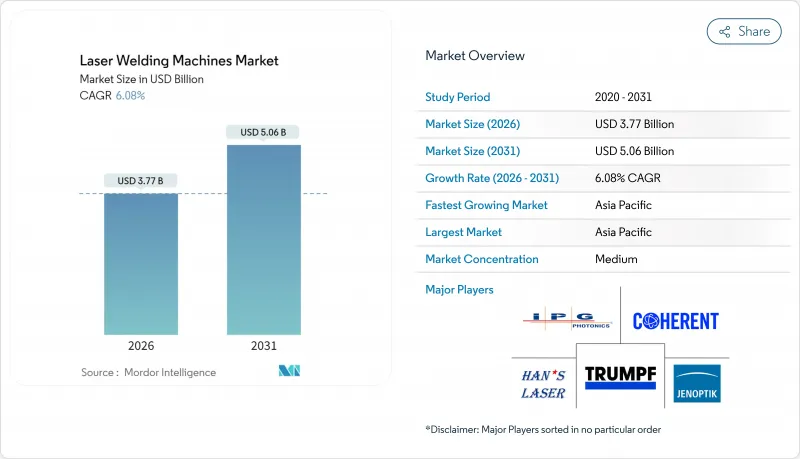

레이저 용접기 시장은 2025년 35억 5,000만 달러에서 2026년에는 37억 7,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 6.08%로 성장을 지속하여 2031년까지 50억 6,000만 달러에 이를 것으로 예측됩니다.

이러한 성장 궤도의 주요 원동력은 배터리 팩 조립 라인에 대한 견고한 설비 투자, Industry 4.0 대응 로봇 셀의 도입 확대 및 핸드헬드형 4-in-1 파이버 시스템의 보급 확대입니다. 또한, 제조업체가 보다 엄격한 공차, 저열 입력, 원활한 자동화를 요구하는 가운데, 종래의 용접 방법으로부터의 단계적인 이행도 레이저 용접기 시장을 진전시키고 있습니다. 게르마늄과 갈륨의 공급 제약에 따른 재료 비용의 인플레이션은 진입 장벽을 높이고 있지만 동시에 주요 기업은 자사 내에서 레이저 광원 생산을 가속화하고 있습니다. 고반사성 구리의 용접이 가능한 녹색 파장 플랫폼에 대한 수요 축적은 프리미엄 벤더에게 잠재적인 기회를 더욱 확대하고 있습니다.

전기자동차의 보급 확대에 따라 구리에 대한 깊은 용해와 최소의 기공률을 실현하는 레이저 광원의 수요가 높아지고 있습니다. 테슬라의 4,680 원통형 셀은 구리 기재의 95% 이상의 전기 전도도를 유지하면서 2mm 이상의 용접이 필요합니다. 적외선 레이저는 구리 입사 에너지의 5%만을 흡수하지만, 녹색 파장 장치는 흡수율을 35-50%로 높여 스퍼터링 및 재작업을 줄입니다. 녹색 광원의 고가격화는 공급업체의 이익률 확대에 기여하며, 자동차 제조업체는 향후 기가비트 팩토리 전체에서 이러한 시스템을 표준화할 전망입니다. 이러한 촉진요인은 2020년대 중반까지의 전체 성장률에 1.2포인트의 상승을 불러왔습니다.

IPG사의 LightWELD 2000 XR과 같은 휴대용 유닛은 용접, 절단, 세척, 브레이징 기능을 2kW 장치에 집약하면서 가격은 5만 달러 미만입니다. 핸드헬드 설계를 통해 작업장에서 여러 개의 기존 스테이션을 대체하여 현장 수리를 위한 기동성을 유지할 수 있습니다. ASEAN과 라틴아메리카의 중소기업은 50만 달러 규모의 로봇 설비 도입을 피하기 위해 본 시스템을 도입하여 투자 회수 기간을 18개월 미만으로 단축하고 있습니다. 또한 현지 은행이 저금리 렌탈 패키지를 제공함으로써 수요가 가속화되고 단기 기여도가 1.1% 포인트로 상승하고 있습니다.

레이저 용접 셀 세트는 20만-200만 달러이며 이는 MIG 또는 TIG 용접 장치의 가격인 1만 5천-5만 달러를 크게 웃돌고 있습니다. 인건비가 시간당 15달러 미만인 저비용 지역의 제조업체는 ROI가 3년을 초과하는 경우 도입이 지연됩니다. 갈륨 및 게르마늄에 대한 규제로 인한 부품 가격 상승은 광학 부품 및 칩 비용을 최대 25%까지 끌어올려 도입 장벽을 더욱 높입니다. 자금 조달 이니셔티브는 존재하지만 신용 접근은 여전히 불균일하며 이는 단기적으로 CAGR의 0.9포인트 하락을 초래하고 있습니다.

파이버 플랫폼은 2025년 수익의 43.68%를 차지하였으며 뛰어난 비용 효율성과 확립된 통합업체 생태계를 배경으로 성장을 유지했습니다. 파이버 시스템의 레이저 용접기 시장 내 규모는 원료 파이버의 비용 저하에 의한 혜택을 받고 있지만, 빔 파라미터 제품은 통상 4-8 mm-mrad의 범위에서 추이하며 초미세 가공에는 제한이 있습니다. 고체 레이저 구성은 가격이 높지만 2mm-mrad 미만의 출력을 실현하여 마이크로일렉트로닉스나 혈관 스텐트 조립을 견인하고 있습니다. 이러한 정밀도가 2031년까지 CAGR 6.43%로 예상되는 고체 레이저 부문을 뒷받침하며 기술 구성 중에서 가장 빠른 성장률을 나타내고 있습니다. 각 공급업체는 나노초 펄스와 연속파 사이를 전환할 수 있는 빔 모듈을 번들하여 제품 간의 경쟁 위험을 피합니다. 반면에 CO2 레이저는 틈새 플라스틱 용접 응용 분야에 머무르고 있으며 다이렉트 다이오드 장치는 중간 정도의 정확도가 필요한 자동차 시트 백 프레임 용도로 유지됩니다.

녹색 파장 유닛은 구리 흡수율 35% 이상을 달성하기 때문에 '기타' 범주 내에서 상승하고 있습니다. TRUMPF사의 TruDisk Pulse는 부스바 용접에 새로운 기준을 확립하였으며 평균 출력 500W로 안정된 키홀 상태를 실현하고 있습니다. 통합자는 기존의 파이버 용접 스테이션에 주파수 증폭 모듈을 추가하여 전체 셀을 폐기하는 대신 광학 시스템을 업그레이드합니다. 레이저 용접기 시장은 이러한 개조와 관련된 교정 서비스 및 예비 광학 시스템의 출하와 같은 지속적인 수익을 통해 벤더의 이익률을 향상시킵니다.

2025년에는 로봇 통합 셀이 시장 가치의 41.85%를 차지했습니다. 이는 자동차 및 항공우주 분야에서의 확고한 도입 실적에 의한 것입니다. 이 셀은 6축 운동 메커니즘과 비전 가이드 동작을 통해 50µm 미만의 재현성 있는 용접 위치 결정을 실현합니다. 그러나 핸드헬드 장치가 가장 주목을 받고 있으며 CAGR 8.39%로 확대 중입니다. 핸드헬드형의 레이저 용접기 시장 내 점유율 확대에는 유지보수를 용이하게 하는 드롭인 파워 모듈과 올인원 소모품 카트리지가 기여하고 있습니다. 실드 가스 설비가 없는 오퍼레이터는 아르곤과 질소를 전환할 수 있는 내장 듀얼 가스 노즐을 도입하고 있습니다. 벤치탑 스테이션과 하이브리드 기계는 각각 연구 개발 실험실과 웨이퍼 레벨 패키징을 목표로 하고 있지만, 보급 속도는 완만합니다.

선박의 선체 수리 및 풍력 타워 리모델링과 같은 현장 서비스는 휴대용 시스템의 미개척 분야입니다. LightWELD 2000 XR은 TIG 용접보다 70% 빠르게 현장에서 스테인리스에 대한 수리를 완료하여 선박의 조기 가동을 가능하게 합니다. 보험 회사가 중요 해양 자산에 레이저 수리를 의무화하기 시작하면서, 핸드헬드 기계의 도입에 규제면에서의 뒷받침이 일어나고 있습니다. 서비스 계약은 교육, 광학 교환 및 소프트웨어 업데이트를 구독 형식으로 제공하여 초기 장비 판매를 보완합니다.

아시아태평양은 2025년 레이저 용접기 시장에서 49.35%의 점유율을 차지했으며, 2031년까지 연평균 복합 성장률(CAGR) 7.62%로 가장 빠르게 성장할 것으로 예상되는 지역입니다. 중국의 설비 용량은 2024년에 2만 5,000대를 넘어섰으며, 지방 정부는 신규 플랜트 건설을 보조하여 지역공급망 강화를 도모하고 있습니다. 일본의 시스템 통합자는 숙련 노동자의 부족을 보완하기 위해 정밀 로봇과 국내 파이버 광원을 결합합니다. 한편, 한국은 다층 동판 용접을 필요로 하는 배터리 팩 제조 거점에 보조금을 투입하고 있습니다. 인도의 생산 연동형 인센티브는 현지에서의 장비 조립을 촉진하고 수입 관세를 줄여 서유럽 벤더가 인도의 시스템 하우스와 제휴하도록 뒷받침하고 있습니다.

북미는 항공우주산업과 클래스 III 의료기기산업의 기반을 살려 고가격 전략을 유지하고 있습니다. 미국 중서부의 전기자동차 확대는 녹색 파장 셀의 설치를 가속화하고 있지만, 게르마늄 공급 리스크에 의해 광학 비용이 최대 75% 상승할 우려가 있습니다. 캐나다 규제 당국은 희토류 채굴 승인을 가속화하고 있지만, 정제 공정의 병목 현상으로 인해 수입 의존도가 계속되고 있습니다. 인플레이션 억제법에 근거한 연방 세액 공제는 청정 제조 설비에 대한 자본 지출의 최대 30%를 환급하여 설비 투자의 가격 감응도를 완화합니다.

유럽에서는 독일의 중견 기계 제조업체가 중국의 신규 진출기업과의 비용 경쟁에 직면하여 성장은 중간 정도로 유지되고 있습니다. 2026년 시행된 EU 탄소국경조정메커니즘은 특히 철강 집약형 산업에서 레이저 용접과 같은 저열 입력 공정을 촉진합니다. 스칸디나비아의 조선소는 암모니아 대응 추진 라인의 개조를 위한 핸드헬드 시스템을 시험적으로 도입하고, 동유럽의 자동차 공장에서는 TRUMPF사와 제휴한 현지 인테그레이터가 공급하는 턴키 셀을 도입하고 있습니다. 공급안전법에 의해 컨소시엄은 EU 역내에서 질화갈륨 에피웨이퍼 제조 능력의 개발을 추진하고, 업스트림 원료에 대한 중국의 지배적 지위를 완화하는 것을 목표로 하고 있습니다.

The Laser Welding Machines market is expected to grow from USD 3.55 billion in 2025 to USD 3.77 billion in 2026 and is forecast to reach USD 5.06 billion by 2031 at 6.08% CAGR over 2026-2031.

Robust capital spending on battery-pack assembly lines, growing deployment of Industry 4.0 robotic cells, and wider availability of handheld four-in-one fiber systems are the primary engines behind this growth trajectory. The laser welding machines market also benefits from a gradual pivot away from conventional fusion methods as manufacturers seek tighter tolerances, lower heat input, and seamless automation. Material cost inflation linked to germanium and gallium restrictions has raised entry barriers, yet it simultaneously accelerates in-house laser source production among leading players. Pent-up demand for green-wavelength platforms capable of welding highly reflective copper further widens the addressable opportunity for premium vendors.

Escalating electric-vehicle penetration lifts demand for laser sources that achieve deeper copper penetration with minimal porosity. Tesla's 4680 cylindrical cells rely on welds surpassing 2 mm while maintaining electrical conductivity above 95% of base copper. Infrared lasers absorb only 5% of incident energy on copper, yet green-wavelength devices raise absorption to 35-50%, trimming spatter and rework. Premium pricing on green sources widens vendor margins, and automakers standardize these systems across future Gigafactories. The driver adds 1.2 percentage points to overall growth through mid-decade.

Portable units, such as IPG's LightWELD 2000 XR, consolidate welding, cutting, cleaning, and brazing in a 2 kW device priced below USD 50,000. The handheld form factor lets workshops replace multiple conventional stations while preserving mobility for field repairs. SMEs in ASEAN and Latin America acquire these systems to bypass USD 500,000 robotic installations, shrinking payback periods to under 18 months. Demand accelerates further as local banks bundle low-interest leasing packages, lifting the driver's short-term contribution to 1.1 percentage points.

Complete laser welding cells range from USD 200,000 to USD 2 million, dwarfing the USD 15,000-50,000 outlay for MIG or TIG setups. Manufacturers in lower-cost geographies where labor sits below USD 15 per hour delay adoption when ROI stretches beyond three years. Component price spikes arising from gallium and germanium restrictions inflate optics and chip costs by up to 25%, aggravating the hurdle. Financing initiatives exist, but credit access remains uneven, pulling down CAGR by 0.9 percentage points in the near term.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fiber platforms retained 43.68% of 2025 revenue on the back of favorable cost-performance ratios and established integrator ecosystems. The laser welding machines market size for fiber systems benefits from raw-fiber cost deflation, but beam parameter products typically hover between 4 and 8 mm-mrad, limiting ultra-fine work. Solid-state configurations, while pricier, deliver sub-2 mm-mrad outputs that drive micro-electronics and vascular stent assembly. This precision underpins a 6.43% CAGR for solid-state through 2031, the fastest inside the technology mix. Vendors hedge against cannibalization by bundling switchable beam modules that toggle between nanosecond pulsing and continuous wave. Meanwhile, CO2 lasers cling to niche plastic welding duties, and direct-diode devices secure automotive seat-back frame contracts where moderate precision suffices.

Green-wavelength units rise within the "Others" bucket because they reach copper absorption rates above 35%. TRUMPF's TruDisk Pulse sets new benchmarks in busbar welding, achieving stable keyhole regimes at 500 W average power. Integrators retrofit legacy fiber stations with frequency-doubled modules, upgrading optics rather than scrapping entire cells. The laser welding machines market captures annuity revenues from these retrofits, including calibration services and spare optics shipments, thereby thickening vendor margin profiles.

Robotic-integrated cells controlled 41.85% of the market value in 2025, owing to entrenched automotive and aerospace pipelines. These cells deliver repeatable sub-50 µm weld positioning through six-axis kinematics and vision-guided motion. However, handheld devices spark the most enthusiasm, expanding at 8.39% CAGR. The laser welding machines market share of handheld units benefits from drop-in power modules and all-in-one consumable cartridges, easing maintenance. Operators without shielding-gas infrastructure now employ built-in dual-gas nozzles that alternate between argon and nitrogen. Bench-top stations and hybrid machines target R&D labs and wafer-level packaging, respectively, but encounter slower uptake.

Field services such as ship-hull repair or wind-tower refurbishment form an untapped vein for portable systems. LightWELD 2000 XR completes on-site stainless repairs 70% faster than TIG, freeing vessels sooner. Insurance firms begin mandating laser repair in critical maritime assets, adding a regulatory tailwind to handheld adoption. Service contracts bundle training, optics swaps, and software updates under subscription, complementing initial equipment sales.

The Laser Welding Machines Market Report is Segmented by Technology (Fiber, CO2, Solid-State, and More), by System Type (Hand-held/Portable, Stationary Bench-Top, and More), by Application (Automotive, Electronics, Mining, Oil & Gas and More), by Material Type (Steel, Aluminum, Titanium, Copper, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific dominated the laser welding machines market with 49.35% value in 2025 and remains the fastest-growing territory at a 7.62% CAGR to 2031. China's capacity surpassed 25,000 laser systems in 2024, with provincial governments subsidizing new plant builds to reinforce local supply chains. Japanese integrators combine precision robots with domestic fiber sources to absorb skilled-labor shortages, while South Korea channels subsidies toward battery-pack fabrication centers that demand multilayer copper welding. India's production-linked incentives nurture localized equipment assembly, reducing import duties and encouraging Western vendors to partner with Indian system houses.

North America leverages its entrenched aerospace and Class-III medical device clusters to maintain premium pricing. EV expansion across the United States Midwest accelerates green-wavelength cell installation, although germanium supply risks lift optics costs by as much as 75%. Canadian regulators fast-track rare-earth mining approvals, yet refining bottlenecks force continued import dependence. Federal tax credits under the Inflation Reduction Act reimburse up to 30% of capital expenditures on clean manufacturing assets, buffering capex sensitivity.

Europe experiences middling growth as German mid-sized machine builders contend with cost competition from Chinese entrants. The European Union's Carbon Border Adjustment Mechanism, effective 2026, incentivizes low-heat-input processes like laser welding, especially in steel-intensive sectors. Scandinavian shipyards trial handheld systems to retrofit ammonia-ready propulsion lines, while Eastern European auto plants adopt turnkey cells supplied by local integrators partnered with TRUMPF. Supply security legislation spurs consortiums to develop gallium-nitride epi-wafer capabilities inside the bloc, aiming to loosen China's stranglehold on upstream raw materials.