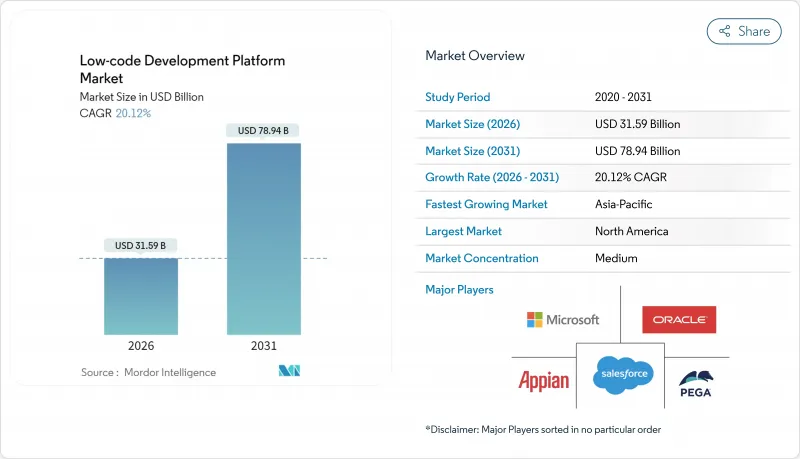

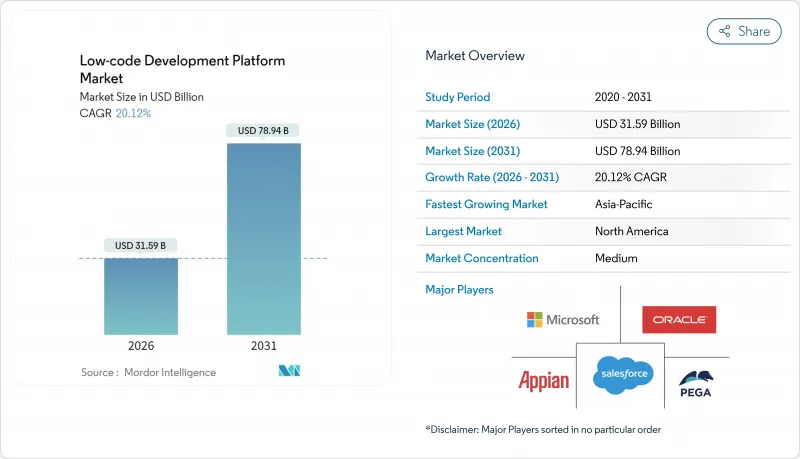

로우코드 개발 플랫폼 시장 규모는 2026년에는 315억 9,000만 달러에 달할 것으로 예측되고 있습니다. 2025년의 263억 달러에서 성장해 2031년에는 789억 4,000만 달러에 이를 전망으로, 2026년부터 2031년에 걸쳐 CAGR 20.12%를 나타낼 것으로 예상됩니다.

이 성장은 레거시 시스템의 현대화가 시급하다는 사실, 개발자의 심각한 부족, 신속한 용도 제공을 평가하는 엄격한 규제 기한에 의해 지원됩니다. 연방 정부 기관은 로우코드 솔루션을 위한 다년간 포괄 구매 계약을 체결했으며, EU 은행은 2027년 시행될 컴포저블 뱅킹 및 데이터 액세스 규칙에 대한 대응을 서두르고 있습니다. 클라우드 퍼스트 아키텍처, AI 구동 개발 코파일럿, 확장되는 소블린 클라우드 프레임워크가 업계와 지역에 관계없이 도입을 더욱 촉진하고 있습니다. 플랫폼 공급업체가 빌드 사이클의 단축, 데이터 통합, 시장 포지션 방어를 목적으로 생성형 AI와 데이터 패브릭 기능을 쌓아 가면 경쟁 압력이 격화되고 있습니다.

연방 정부 기관은 수십 년에 걸쳐 COBOL 플랫폼을 폐지하고 있으며, 여러 기업과의 포괄 구매 계약(계약 관리 비용을 23% 삭감)을 통해 로우코드 시스템으로의 이행을 추진하고 있습니다. 국방계약관리국(DCMA)은 2025년 근대화 RFI에서 통합계약관리의 우선수단으로서 로우코드를 명기했습니다. 각 주정부도 연방정부의 템플릿을 모방하고, 대상이 되는 지출규모를 확대함과 동시에, 공공 부문에서의 신속한 근대화의 표준 수단으로서 로우코드 플랫폼의 지위를 확고하게 하고 있습니다. FedRAMP 및 국방부 IL5 준수를 검증할 수 있는 공급업체는 이러한 확장된 조달 동향에 대한 우선 액세스를 획득하고 로우코드 개발 플랫폼 시장의 추가 성장을 지원합니다.

금융 데이터 액세스 규정을 통해 유럽 은행은 2027년까지 고객 데이터를 API를 통해 공개할 의무가 있습니다. 보완적인 디지털 업무 탄력성 법(Digital Operational Resilience Act)의 규정은 ICT 위험 모니터링을 강화하고 주간 업데이트되는 규제를 수용할 수 있는 민첩한 아키텍처로의 전환을 금융기관에 촉구합니다. 로우코드 플랫폼은 준수 API 생성 및 관리 증거 자동화를 통해 이 두 가지 요구를 모두 충족합니다. 유럽 중앙 은행의 감독 당국은 모듈식 서비스 배포를 평가하는 클라우드 아웃소싱의 기대치를 공식적으로 결정했습니다. 따라서 전통적인 은행은 로우코드 개발 플랫폼 시장 전체에서 핀테크 과제들의 출시 속도를 따라잡기 위해 로우코드 툴에 의존하고 있습니다.

2024년의 검토된 연구에서는 클라우드 공급업체 락인 예측 프레임워크를 도입하여 마이그레이션 리스크를 정량화하면서 자체 런타임에 묶인 용도의 고비용 리스크를 밝혔습니다. 많은 로우코드 시스템은 워크플로우를 폐쇄 실행 엔진으로 컴파일하므로 이식성이 제한됩니다. CIO는 소스 코드 내보내기 및 컨테이너화된 배포 옵션을 요구하므로 구매주기가 지연되고 로우코드 개발 플랫폼 시장의 일부가 억제됩니다.

플랫폼 부문은 2025년에 수익의 71.35%를 차지하며 로우코드 개발 플랫폼 시장의 기반이 되었습니다. 기업은 비주얼 모델링, 프로세스 오케스트레이션 및 통합 데이터베이스를 결합한 통합 환경을 선호하며, 이로써 도구의 난립을 억제하고 있습니다. Salesforce를 통한 Informatica의 80억 달러 인수와 같은 통합 전략은 데이터 관리와 AI를 단일 런타임으로 통합하여 기업에 대한 잠금을 강화합니다. 서비스 라인의 확장은 플랫폼 구축을 계속합니다. 단일 공급업체를 표준화하는 정부 기관은 통합 컨설팅, 거버넌스 프레임워크, AI 프롬프트 설계에 대한 지속적인 수요를 창출합니다.

서비스 분야는 규모가 작은 것, 조직이 COBOL 워크로드의 이행, ESG 분석의 임베디드, 생성형 AI 코파일럿의 트레이닝을 파트너에게 요구하는 움직임으로부터, 23.45%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 이 권고 수요가 증가함에 따라 프리미엄 지원 및 관리 서비스의 부대율을 높이고 업계에 지속적인 수익 계층을 추가합니다. 예측 기간 동안 라이선스와 함께 교육, 데이터 패브릭 조정 및 AI 모델 거버넌스를 패키징하는 공급업체는 평생 가치를 두 배로 늘리고 시장을 확대할 수 있을 것입니다.

2025년에도 웹 용도 지출의 54.40%를 차지했지만, 현장 기술자나 원격 직원에 의한 오프라인 우선 기능 수요 증가에 따라 모바일 워크로드는 22.63%의 연평균 복합 성장률(CAGR)로 확대 중입니다. 카메라, 생체인증 및 증강현실(AR)을 위한 네이티브 플러그인은 모바일 경험을 더욱 풍부하고 컨텍스트에 맞게 만듭니다. 특히 보험검사 및 유틸리티 유지보수 분야에서 모바일 이용 사례를 위한 로우코드 개발 플랫폼 시장 규모는 급속한 성장이 예상되고 있습니다.

API 중심 디자인은 웹과 모바일 앱을 모두 확장하며 컴포저블 뱅킹 및 오픈 데이터 지침을 준수합니다. Microsoft가 계획하는 모놀리식 Dynamics 365 화면에서 작업 지향 AI 에이전트로의 마이그레이션은 인터페이스가 컨텍스트에 맞는 마이크로 인터랙션으로 녹아 가는 것을 보여줍니다. 반응형 디자인, 원 클릭 PWA 생성, 안전한 오프라인 동기화를 제공하는 공급업체는 다중 채널 균일성을 추구하는 조직 간 시장 점유율을 확대할 것입니다.

북미는 2025년에 30.60%의 수익 점유율을 차지하고 연방 정부의 근대화와 성숙한 벤처 생태계가 견인했습니다. 미국 정부에 의한 COBOL 폐지 추진과 FedRAMP 준거의 철저는 주 기관의 모델 케이스가 되어 사법·운수·의료 분야에서 재현 가능한 전개를 촉진하고 있습니다. 캐나다에서는 로우코드를 활용하여 핀테크 라이선싱과 디지털 ID 프로젝트를 가속화함으로써 지역 전체의 기세를 확대하고 있습니다. 벤처캐피탈은 AI를 통합한 로우코드 스타트업에 대한 지원을 계속하고 로우코드 개발 플랫폼 시장을 지원하는 제품 혁신을 촉진하고 있습니다.

아시아태평양은 21.13%라는 가장 빠른 CAGR을 나타낼 전망입니다. 일본의 보험사는 IFRS17 대응을 위해 감사 대응 빌더를 채용하고 싱가포르 금융관리국은 신속한 핀테크 샌드박스 운영을 추진하고 있습니다. 중국은 걸프 국가에 하이퍼스케일 데이터센터를 자금 제공하고 서양 호환 런타임을 호스팅하는 소블린 클라우드를 제공합니다. 인도의 IT서비스 대기업은 세계의 변혁 계약에 로우코드 가속기를 통합, 수출 수익을 확대하는 동시에 국내 공공 부문의 도입을 촉진합니다. 이러한 이니셔티브가 함께 이 지역이 미래의 로우코드 개발 플랫폼 시장 성장에 크게 기여하는 기반을 형성하고 있습니다.

유럽은 규제 측면에서 영향력을 발휘하고 세계 제품 로드맵을 형성하고 있습니다. 유럽 중앙 은행(ECB)의 클라우드 기준, 오픈 뱅킹 API의 기한, ESG 공개 의무로 기업은 컴플라이언스 대응의 신속한 자동화를 촉구하고 있습니다. 북유럽 국가 정부는 로우코드 포털에서 시민 서비스를 제공하고 독일 자동차 제조업체는 성능 측면에서 우려가 있는 것 현장용 앱의 프로토타입 개발을 진행하고 프랑스의 유틸리티 회사는 ESG 보고 파이프라인을 통합하고 있습니다. 정책의 기세가 시너지 효과를 낳는 가운데, 유럽은 확대되는 로우코드 개발 플랫폼 시장의 기반이 되고 있습니다.

Low-code Development Platform Market size in 2026 is estimated at USD 31.59 billion, growing from 2025 value of USD 26.30 billion with 2031 projections showing USD 78.94 billion, growing at 20.12% CAGR over 2026-2031.

This growth rests on urgent legacy-system modernization, acute developer shortages, and strict regulatory deadlines that reward rapid application delivery. Federal agencies are issuing multi-year blanket purchase agreements for low-code solutions, while EU banks race to meet 2027 composable-banking and data-access rules. Cloud-first architectures, AI-driven development copilots, and expanding sovereign-cloud frameworks are further lifting adoption across industries and regions. Competitive pressure is intensifying as platform vendors layer generative AI and data-fabric capabilities to shorten build cycles, consolidate data, and defend market position.

Federal departments are retiring decades-old COBOL platforms and replacing them with low-code systems through multi-award blanket purchase agreements that lower contract overhead by 23% . The Defense Contract Management Agency highlighted low-code in its 2025 modernization RFI as the preferred path for integrated contract management. States now replicate these federal templates, expanding addressable spend and cementing low-code platforms as the public-sector default for rapid modernization. Vendors able to verify FedRAMP and DoD IL5 compliance gain privileged access to this growing procurement wave, supporting further growth for the low-code development platform market.

The Financial Data Access regulation obliges European banks to expose customer data via APIs by 2027. Complementary Digital Operational Resilience Act rules tighten ICT risk oversight and push institutions toward agile architectures that can adapt to weekly rule updates. Low-code platforms answer both needs by generating compliant APIs and automating control evidence. Supervisors at the European Central Bank have formalized cloud-outsourcing expectations that reward modular service deployment. Traditional banks therefore rely on low-code tooling to match the release velocity of fintech challengers across the low-code development platform market.

A 2024 peer-reviewed study introduced a cloud vendor lock-in prediction framework that quantifies switching risk and reveals high cost exposures for applications bound to proprietary runtimes. Many low-code systems compile workflows into closed execution engines that limit portability. CIOs now require source-code export and containerized deployment options, slowing purchase cycles and suppressing a portion of the low-code development platform market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The platform segment represented 71.35% revenue in 2025 and anchors the low-code development platform market. Enterprises favor unified environments that combine visual modelling, process orchestration, and integrated databases, thereby reducing tool sprawl. Consolidation plays such as Salesforce's USD 8 billion acquisition of Informatica fold data management and AI into a single runtime to deepen enterprise lock-in. Service-line expansion follows platform rollout: federal agencies that standardize on one vendor generate continuous demand for integration consulting, governance frameworks, and AI-prompt design.

Services, while smaller, are growing at 23.45% CAGR as organizations look for partners to migrate COBOL workloads, embed ESG analytics, and train GenAI copilots. This advisory wave lifts attach rates for premium support and managed services, adding recurring revenue layers to the industry. Over the forecast, vendors that package training, data-fabric tuning, and AI-model governance alongside licences can double lifetime value and widen the market.

Web apps still controlled 54.40% spending in 2025, yet mobile workloads are rising at 22.63% CAGR as field technicians and remote employees demand offline-first capabilities. Native plug-ins for camera, biometrics, and augmented reality make mobile experiences richer and more contextual. The low-code development platform market size for mobile use cases is projected to grow rapidly, especially in insurance inspections and utility maintenance.

API-centric designs extend both web and mobile apps, aligning with composable-banking and open-data directives. Microsoft's planned shift from monolithic Dynamics 365 screens to task-oriented AI agents underlines how interfaces will dissolve into contextual micro-interactions. Vendors that ship responsive design, one-click PWA generation, and secure offline sync will capture incremental market share among organizations pursuing multi-channel parity.

Low Code Development Platform Market Report is Segmented by Component (Platform and More), Application Type (Web-Based, Mobile-Based, and More), Deployment Type (On-Premises, Cloud), Organization Size (Small and Medium Enterprises, Large Enterprises), Industry Vertical (BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America held 30.60% revenue in 2025, driven by federal modernization and a mature venture ecosystem. The U.S. government's push to sunset COBOL and enforce FedRAMP compliance sets a template for state agencies, seeding repeatable rollouts across justice, transport, and health. Canada leverages low-code to expedite fintech licensing and digital-identity projects, broadening regional momentum. Venture capital continues to back AI-infused low-code startups, fuelling product innovation that sustains the low-code development platform market.

Asia-Pacific posts the fastest 21.13% CAGR. Japan's insurers adopted audit-ready builders for IFRS 17, while Singapore's Monetary Authority encourages rapid fintech sandboxing. China finances hyperscale data centers in Gulf states, offering sovereign clouds that host Western-compatible runtimes. India's IT-services leaders embed low-code accelerators within global transformation deals, amplifying export revenue while catalyzing local public-sector uptake. These initiatives collectively underpin the region's outsized contribution to future low-code development platform market growth.

Europe wields regulatory influence that shapes global product roadmaps. ECB cloud standards, open-banking API deadlines, and ESG disclosure mandates force enterprises to automate compliance fast. Nordic governments deliver citizen services via low-code Portals, Germany's auto OEMs prototype shop-floor apps despite performance caveats, and French utilities integrate ESG reporting pipelines. With policy momentum compounding, Europe remains a cornerstone of the expanding low-code development platform market.