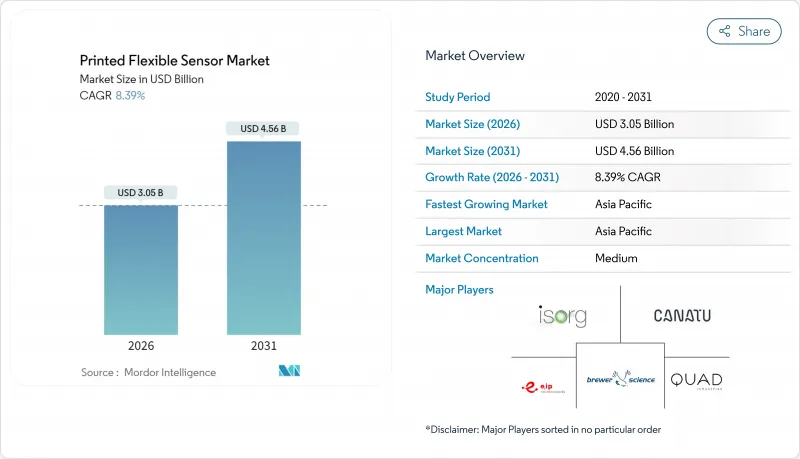

프린티드 플렉서블 센서 시장은 2025년 28억 1,000만 달러에서 2026년에는 30억 5,000만 달러로 성장해 2026년부터 2031년에 걸쳐 CAGR 8.39%를 나타낼 전망입니다. 2031년까지 45억 6,000만 달러에 이를 것으로 예측됩니다.

이 꾸준한 확대는 롤-투-롤 방식의 적층 조형 기술의 진보, 국내 반도체 생산 능력을 지원하는 정책 인센티브, 그리고 소비자용 전자기기, 의료용 웨어러블 기기, 자동차 시스템, 방위 플랫폼에 있어서 적합성이 있는 센싱 솔루션에 대한 수요 증가가 함께 발생하고 있습니다. 새로운 인쇄 프로세스로 인해 설비 투자액이 40% 이상 줄어들어 기존 기업과 신흥 기업 모두에게 진입 장벽이 저하되고 비용 최적화가 성장의 중요한 추진력이 되고 있습니다. 바이덴 해리스 정권에 의한 선진 포장을 위한 16억 달러의 예산 배분 등 정부 프로그램은 플렉서블 일렉트로닉스 인프라의 전략적 중요성을 뒷받침하고 있습니다. 아시아태평양은 특히 유연한 OLED 생산 능력 확충에 있어서 규모의 우위성에 의해 2030년까지 인쇄 센서 전체의 거의 절반을 공급하는 입장에 있습니다. 한편, 유럽의 규제 동향은 재활용 가능한 센서 구조에 대한 수요를 촉진하고 있습니다.

스마트폰 및 웨어러블 기기의 OEM 제조업체는 기존의 단단한 부품으로는 실현할 수 없는 폴더블 디스플레이와 압력 감지 하우징을 구현하기 위해 프린티드 플렉서블 센서를 통합합니다. 초저전력 아키텍처는 디바이스의 배터리 수명을 연장하여 사용자의 에너지 절약 기대에 부응하면서 슬림한 폼 팩터를 실현합니다. 펜실베니아 주립대학의 조사에서는 2차 활성화 공정을 필요로 하지 않는 자기조립 도전 네트워크가 개발되어 제조시 에너지 소비를 줄였습니다. 게이밍 주변기기에서는 압력 매핑 표면의 채용이 증가하고 있으며, 모바일 기기 이외의 분야에도 프린티드 플렉서블 센서 시장이 확대되고 있습니다. 같은 박형·굽힘 가능한 필름은 산업용 모니터링 분야에도 진출하고 있어, 센서는 곡면 기기에 적합하면서 두께를 늘리지 않는 것이 요구되고 있습니다.

의료 제공업체는 실시간 바이탈 사인 추적에 인쇄 바이오 센서를 도입하여 예방 및 원격 의료로의 전환을 가속화하고 있습니다. 코베스트로사와 엑센소아사의 제휴에 의해 베이메딕스사의 접착제와 플라티론 TPU 필름을 활용한 통기성 및 촉감이 뛰어난 패치형 센서가 탄생했습니다. 한국재료과학연구원은 1ppm 감도의 암모니아가스 검출기를 시연하고 신장질환 모니터링에서 비침습적 진단의 가능성을 개척하고 있습니다. 플렉서블 디바이스가 임상적 증거를 축적함에 따라 규제 경로가 간소화되고, 바이오센서는 프린티드 플렉서블 센서 시장에서 가장 빠르게 성장하는 궤도를 포착하는 태세를 갖추고 있습니다.

인쇄 게이지는 특히 온도 변동이나 기계적 피로에 노출되면 장기 안정성에서 미세 가공 실리콘으로 여전히 열등합니다. 미결정 실리콘 디바이스는 드리프트를 최소화하면서 게이지 계수(31)를 달성하는 반면, 인쇄 필름은 정밀도가 요구되는 용도에서 허용 범위를 초과하는 편차를 생성할 수 있습니다. 임상 평가에서 유연한 압력 센서의 정확도 범위는 88-94%로 보고되었으며, 지표적 모니터링에는 충분하지만 침습적 검사 수준의 기준값에 도달하지 못했습니다. 봉지층이나 나노복합 잉크에 관한 조사가 진행중이며, 성능차이의 축소를 도모하고 있습니다.

2025년 인쇄 압력 센서는 플렉서블 센서 시장 전체의 27.95%를 차지하며 스마트폰, 게임 컨트롤러, 자동차용 터치 패널용 촉각 인터페이스를 공급했습니다. 바이오센서 분야에서도 병행하여 기세를 늘리고 있으며, CAGR9.03%로 확대 중. 이는 의료 분야에서의 비침습적, 상시 가동형 환자 모니터링에 대한 수요 증가를 반영하고 있습니다. 바이오센서의 급성장은 진단이 의료기관에서 소비자 영역으로 이동하는 가운데 프린티드 플렉서블 센서 시장의 확대를 촉진하고 있습니다. 견고한 수요는 AI 대응 분석 기술과 어울리며 고해상도 스트레인 게이지가 재활 피드백 루프를 위해 생체역학을 매핑합니다. 게다가 1ppm의 암모니아를 검지하는 가스센서는 농업·환경위생 분야에서의 이용 사례를 개척해, 프린티드 플렉서블 센서 산업에 있어서 제품 포트폴리오의 다양화를 나타내고 있습니다.

인접 시장이 차별화를 촉진 : 스마트 포장용 광검출기는 신선도 인증을 실현하고, 전자 섬유에 짜여진 변형 센서는 산업 안전 프로그램을 위한 인체공학적 지표를 포착합니다. 바이오센서를 위한 프린티드 플렉서블 센서 시장 규모는 고분자 기판과 나노 엔지니어링 잉크의 조합이 착용자의 편안함을 손상시키지 않고 임상적으로 유용한 감도를 제공하기 때문에 기존 부문을 능가하는 성장이 예상됩니다. 효소기능화 전극이나 자기수복 도체에 있어서 연구개발의 강화에 의해 기존의 압력·온도 센서와 비교한 본 부문의 우위성은 지속될 것으로 전망됩니다.

후막 형성 능력과 낮은 단가를 강요하는 스크린 인쇄는 2025년 시점에서 35.55%의 수익 점유율을 유지했지만, 잉크젯 인쇄의 예측 CAGR 8.78%는 업계가 고해상도 패턴과 다재료 대응성으로 전환하고 있음을 보여주고 있습니다. 선폭이 20µm 미만인 한계에 가까워짐에 따라 잉크젯 플랫폼은 제한된 면적에서 고밀도 배선을 가능하게 하여 프린티드 플렉서블 센서 시장에서 소형화 로드맵을 추진합니다. 신기술인 에어로졸 제트 인쇄 및 3D 인쇄 기술은 비평면 형상으로 전도성 페이스트를 도포할 수 있어 아비오닉스 및 의료용 임플란트에 요구되는 적합성을 실현함으로써 설계의 자유도를 더욱 확대합니다.

그라비아 프린팅 및 플렉소 프린팅 라인은 소비자용 전자기기 생산의 백만 단위에 여전히 주력하고 있지만, 잉크젯의 디지털 특성은 공정 전환 시간을 단축하고 센서 레이아웃의 대량 사용자 정의를 가능하게 합니다. 학술그룹이 입증한 서브미크론 CNT 트랜지스터의 모세관 흐름 인쇄 기술은 포토리소그래피와 동등한 미세화를 실현하여 결정적인 경쟁 전환점을 나타내고 있습니다. 잉크젯 시스템과 관련된 프린티드 플렉서블 센서 시장 규모는 귀금속 가격의 영향을 받지 않고 벌크은과 동등한 전도성을 실현하는 광플래시에 의한 소결이 가능한 무산화구리 나노유체를 잉크 공급자가 상용화함에 따라 가속될 것으로 예측됩니다.

아시아태평양은 2025년 프린티드 플렉서블 센서 시장 점유율의 46.35%를 차지했으며 2031년까지 연평균 복합 성장률(CAGR) 8.71%를 나타낼 것으로 전망됩니다. 중국이 생산능력 증강을 주도하고 BOE는 2028년까지 플렉서블 OLED 생산량으로 삼성디스플레이를 능가할 것으로 예측되고 있습니다. 이 발전은 업스트림 재료 수요를 보장하고 인쇄 센서공급망을 현지화합니다. 일본의 정밀 제조의 전통과 한국의 재료 과학의 깊이가 지역의 강인성을 높이고, 동남아시아 국가는 대량 생산형 민생 전자 기기에 대한 비용 효율적인 조립 거점을 제공합니다.

북미는 매출에서 2위입니다. 16억 달러의 선진 포장 프로그램과 1억 7,900만 달러의 DOE 마이크로 일렉트로닉스 센터 등 연방 정부의 지원책이 국내 프린티드 플렉서블 센서 산업의 능력 향상을 촉진하고 있습니다. 방위 예산은 컨포멀 항공 전자 센서의 조기 도입을 뒷받침하고, 견고한 의료기기 생태계는 바이오 센서의 상업화를 가속화하고 있습니다.

유럽은 자동차 분야의 주도적 입장과 엄격한 에코 디자인 규제를 활용하여 재활용 가능한 센서의 세계 사양 형성을 추진하고 있습니다. 지역기능성 일렉트로닉스 공급망 구축을 목표로 하는 「개혁 프로젝트」는 아시아로부터의 수입 의존도를 저감해, 지속 가능한 기판 기술에 대한 연구 개발 자금을 유도합니다. 라틴아메리카 및 중동 및 아프리카은 현재 점유율이 작고, 산업 근대화와 통신 인프라의 고도화에 의해 잠재 수요가 시사되고 있으며, 특히 스마트 그리드나 빌딩 오토메이션용 센싱 분야에서 두드러집니다.

The printed flexible sensor market is expected to grow from USD 2.81 billion in 2025 to USD 3.05 billion in 2026 and is forecast to reach USD 4.56 billion by 2031 at 8.39% CAGR over 2026-2031.

This steady expansion results from converging advances in roll-to-roll additive manufacturing, policy incentives supporting domestic semiconductor capacity, and rising demand for conformable sensing solutions across consumer electronics, medical wearables, automotive systems, and defense platforms. Cost optimization remains a pivotal growth lever as new printing processes shave more than 40% from capital expenditure outlays, thereby lowering entry barriers for both incumbents and start-ups. Government programs such as the Biden-Harris Administration's USD 1.6 billion allocation for advanced packaging underscore the strategic relevance of flexible electronics infrastructure.Asia-Pacific's scale advantage, particularly in flexible OLED capacity build-out, positions the region to supply nearly half of all printed sensors by 2030, while regulatory moves in Europe foster demand for recyclable sensor architectures.

Smartphone and wearable OEMs embed printed flexible sensors to deliver foldable displays and pressure-sensitive housings that conventional rigid components cannot support. Ultra-low-power architectures extend device battery life, meeting user expectations for energy efficiency while enabling slim form factors. Research at Penn State produced self-assembling conductive networks that remove secondary activation steps, trimming manufacturing energy budgets. Gaming peripherals increasingly rely on pressure-mapped surfaces, widening the printed flexible sensor market beyond mobile hardware. The same thin, bendable films are migrating into industrial monitoring where sensors must conform to curved equipment without adding bulk.

Healthcare providers deploy printed biosensors for real-time vital-sign tracking, accelerating the shift toward preventive, remote care. Covestro's partnership with accensors yielded breathable, skin-friendly patch sensors that leverage Baymedix adhesives and Platilon TPU films. The Korea Institute of Materials Science demonstrated ammonia-gas detectors with 1 ppm sensitivity, opening non-invasive diagnostics for renal disease monitoring. Regulatory pathways are streamlining as flexible devices build clinical evidence, positioning biosensors to capture the fastest growth trajectory within the printed flexible sensor market.

Printed gauges still trail micro-machined silicon alternatives on long-term stability, especially when exposed to temperature swings or mechanical fatigue. Microcrystalline silicon devices achieve gauge factors of 31 with minimal drift, whereas printed films can deviate beyond acceptable thresholds in precision-critical deployments. Clinical evaluations report accuracy spreads of 88-94% for flexible pressure sensors, sufficient for indicative monitoring yet below invasive-grade benchmarks. Ongoing research into encapsulation layers and nanocomposite inks seeks to narrow the performance delta.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Printed pressure sensors controlled 27.95% of the overall printed flexible sensor market share in 2025, supplying haptic interfaces to smartphones, gaming controllers, and automotive touch-surfaces. Parallel momentum in biosensors, expanding at a 9.03% CAGR, reflects healthcare's drive toward non-invasive, always-on patient monitoring. The biosensor surge widens the printed flexible sensor market as diagnostics migrate from clinic to consumer spheres. Robust demand intersects with AI-enabled analytics, where high-resolution strain gauges map biomechanics for rehabilitation feedback loops. Furthermore, gas sensors detecting 1 ppm ammonia open agricultural and environmental-health use-cases, illustrating portfolio diversification within the printed flexible sensor industry.

Market adjacencies amplify differentiation: photodetectors for smart packaging authenticate freshness, while strain sensors woven into e-textiles capture ergonomic metrics for industrial safety programs. The printed flexible sensor market size for biosensors is forecast to outgrow legacy segments as polymer substrates coupled with nano-engineered inks deliver clinically relevant sensitivity without sacrificing wearer comfort. Intensifying R&D in enzyme-functionalized electrodes and self-healing conductors will likely sustain the segment's outperformance against conventional pressure and temperature counterparts.

Screen printing retained 35.55% revenue in 2025 thanks to its thick-film capability and low-unit cost, but inkjet printing's anticipated 8.78% CAGR underscores industry migration toward higher pattern resolution and multi-material flexibility. As line widths approach the sub-20 µm threshold, inkjet platforms enable dense routing on limited real-estate, thereby advancing miniaturization roadmaps within the printed flexible sensor market. Emergent aerosol-jet and 3D printing modalities further extend the design envelope by depositing conductive pastes on non-planar geometries, a requirement for conformal avionics and medical implants.

Gravure and flexographic lines remain staples for million-unit consumer-electronics volumes, yet inkjet's digital nature curtails changeover time, permitting mass-customization of sensor layouts. Capillary-flow printing of submicron CNT transistors demonstrated by academic groups showcases feature parity with photolithography, marking a decisive competitive inflection. The printed flexible sensor market size tied to inkjet systems is projected to accelerate as ink suppliers commercialize oxide-free copper nanofluids that sinter via photonic flashes, achieving bulk-silver conductivities without the precious-metal price drag.

The Printed Flexible Sensor Market Report is Segmented by Sensor Type (Biosensors, Touch Sensors, Photodetectors, and More), Printing Technology (Screen Printing, Inkjet Printing, Gravure Printing, Fand More), Substrate Material (Polyimide, PET, PEN, Paper and More), End-User Industry (Consumer Electronics, Medical and Healthcare, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 46.35% printed flexible sensor market share in 2025 and is anticipated to grow at 8.71% CAGR to 2031. China leads capacity additions, with BOE projected to surpass Samsung Display in flexible OLED throughput by 2028, a development that secures upstream material demand and localizes printed sensor supply chains. Japan's precision-manufacturing heritage and South Korea's material-science depth add regional resilience, while Southeast Asian economies provide cost-efficient assembly for high-volume consumer electronics.

North America ranks second by revenue. Federal incentives such as the USD 1.6 billion advanced packaging program and the USD 179 million DOE microelectronics centers stimulate domestic printed flexible sensor industry capability. Defense budgets catalyze early adoption of conformal avionics sensors, and the robust medical-device ecosystem accelerates biosensor commercialization.

Europe leverages automotive leadership and stringent eco-design mandates to shape global specifications for recyclable sensors. The Reform Project's initiative to forge a regional functional electronics supply chain reduces reliance on Asian imports and channels R&D funding toward sustainable substrate technologies. Latin America and the Middle East & Africa currently command small shares, yet industrial modernization and telecom infrastructure upgrades signal latent demand, particularly in smart-grid and building-automation sensing.