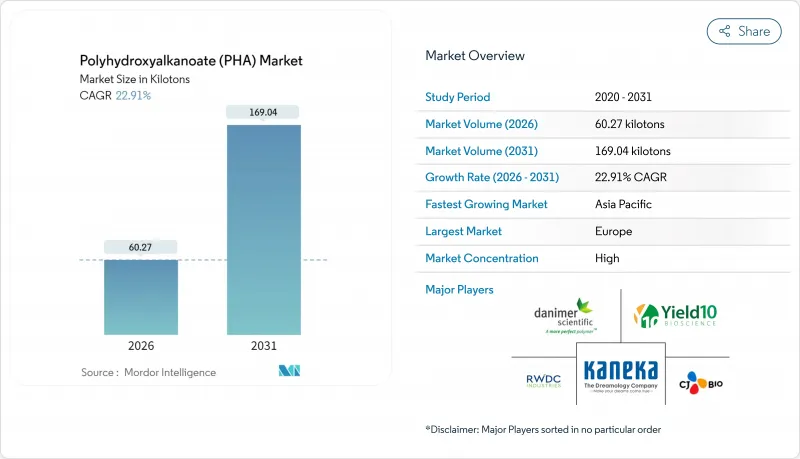

폴리하이드록시알카노에이트 시장은 2025년 49.04킬로톤에서 2026년에는 60.27킬로톤으로 성장하고 2026년부터 2031년에 걸쳐 CAGR 22.91%로 성장을 지속하여 2031년까지 169.04킬로톤에 이를 것으로 예측되고 있습니다.

일회용 플라스틱에 대한 규제 강화, 생산 능력에 대한 대규모 투자, 지속적인 재료 과학의 진보가 포장, 의료 및 농업 분야에서의 급속한 대체 동향을 뒷받침하고 있습니다. 유럽은 엄격한 폐기물 저감 지침에 의해 선행 우위성을 확립하고 있는 한편, 아시아태평양의 공급 기반은 산업 성장과 풍부한 원료 공급을 배경으로 급속히 확대하고 있습니다. 혼합 미생물 배양 공정은 멸균 요건을 줄이고 단위 비용을 낮춰 원료 선택을 확대하는 가능성으로 신뢰성을 높입니다. 경쟁의 치열성은 여전히 중간 정도이며, BASF 등의 확립된 화학그룹이 원료의 혁신과 용도 특화형 수지 설계에 의해 차별화를 도모하는 전문 제조업체나 벤처 지원 스타트업 기업과 시장을 공유하고 있습니다.

각국 및 지자체에 의한 규제 강화가 퇴비화 가능 소재의 조달 목표에 직접 반영되고 있습니다. 캘리포니아주 상원법안 54호는 생산자 책임 재활용 제도를 확립하고, 대상 소재 모두가 2032년까지 재활용 가능 또는 퇴비화 가능할 것을 의무화하여 재활용 및 저감 목표 대상 플라스틱의 정의에 PHA를 명시적으로 포함했습니다. 분류에 관한 논의는 있지만, EU의 일회용 플라스틱 지침도 같은 압력을 가하여 푸드서비스 용품에 대한 브랜드의 신속한 재설계를 촉진하고 있습니다. 하와이주에서의 비생분해성 용기의 단계적 금지도 이러한 동향을 뒷받침하고 있습니다. 주요 소비재 제조업체는 현재 페널티 회피를 위해 PHA 기반의 빨대, 식기, 뚜껑 프로그램을 시험적으로 도입하고 있으며, 이를 통해 수지 공급자의 초기 물량 계약이 확보되고 있습니다.

기업의 탈탄소화 목표와 개정된 에코디자인 기준에 따라 가공업자는 토양과 물 환경에서 분해 가능한 소재로의 이행을 요구받고 있습니다. PHA는 특수한 산업용 퇴비 처리를 필요로 하지 않고 광물화하기 때문에 이 요건을 충족하며 전분계 배합이나 폴리유산과의 차별화를 도모하고 있습니다. 수명 주기 연구에 의하면, 폐기물 유래 탄소원을 이용한 PHA는 환경 부하를 최대 50% 줄이는 것으로 나타났습니다. 포장재, 농업용 필름, 가전 인클로저, 의료용 일회용 제품은 특히 최근의 상용화제 기술로 인장 강도와 장벽 성능이 향상됨에 따라 현저히 성장하는 시장 규모를 형성하고 있습니다.

범용 플라스틱의 거래가격은 1kg당 약 1.00-1.30달러인 반면, 시판 PHA는 1파운드당 2.25-2.75달러로 고가이며 이는 이익률이 낮은 포장 분야에서의 보급을 제약하고 있습니다. 공정 최적화 연구에 따르면 식품 폐기물을 원료로 전환함으로써 30-40%의 비용 절감이 가능할 것으로 예측되고 있지만, 가까운 미래의 가격 경쟁력 확보는 여전히 어렵습니다. 이 때문에 최종 사용자는 생산량이 증가하고 규모의 경제가 실현될 때까지 고부가가치 분야나 규제 주도의 틈새 시장을 우선시하고 있습니다.

폴리하이드록시알카노에이트(PHA) 시장에서 공중합체 시장의 규모는 2025년 25.21킬로톤에 이르면서 51.40%의 점유율을 차지했습니다. PHBV와 같은 공중합체 등급은 냉장 식품의 포장 기준을 충족하는 유연성과 산소 차단 기능을 제공합니다. 최근에는 PHBV를 50% 배합한 폴리부틸렌 아디페이트 테레프탈레이트와의 배합에 의해 파단신률이 향상되고 수증기 투과성이 저감되어, 고기나 치즈 포장용 열성형 트레이에 대한 응용이 기대되고 있습니다. 제품 개발자는 기존의 압출 라인에 대한 다운스트림 공정 변환의 용이성도 높이 평가하고 있으며 이는 설비 투자를 억제할 수 있습니다.

삼원 공중합체는 현재 생산량이 비교적 적지만, 23.70%의 연평균 복합 성장률(CAGR)로 다른 수지군을 상회하고 있으며 이는 전문적인 의료기기나 전자기기 케이스에서의 중요성이 뒷받침하고 있습니다. 4HB 함유율을 50% 이상 높이는 생산 기술의 혁신으로 탄성과 서방 특성이 향상되어 흡수성 약물 전달 필름에 유용합니다. 생산 규모가 확대됨에 따라, 삼원 공중합체의 제조는 석유화학계 엘라스토머가 우세했던 기계적 요건을 충족하는 차별화된 틈새 시장을 개척하여 폴리하이드록시알카노에이트 시장 전체를 견인할 것입니다.

2025년 시점에서는 당류와 당밀이 폴리하이드록시알카노에이트 시장에서 점유율 56.60%를 차지하였습니다. 이는 예측 가능한 수율과 확립된 물류 네트워크에 의해 뒷받침된 결과입니다. 브라질과 태국에서는 사탕수수와 사탕무 공급과 연동한 발효 플랫폼을 통해 원료를 자사에서 확보할 수 있는 통합형 아그로 산업 허브를 형성하고 있습니다. 그러나 원료 비용은 상업 플랜트에서 가장 큰 비용 항목으로 계속되고 있습니다. 에탄올 시장과 식품 시장에서 자당에 대한 경쟁 격화로 인해 폐유와 글리세롤을 원료로 하는 전략적 전환이 진행되고 있습니다. 이 원료 공급원은 CAGR 23.95%로 규모가 확대될 것으로 전망되고 있습니다.

폐유 경로는 탄소 강도를 줄이고 최대 40%의 비용 절감을 실현합니다. 시험에서 비정제 글리세롤로부터 Priestia megaterium을 이용하여 세포 내 PHA 함량 42%를 달성하였습니다. 농업잔사도 주목을 받고 있으며, 한국에서는 김치 제조 시 양배추 조각이 개념 증명용 바이오리액터의 원료로 활용되면서 지역적인 순환형 경제의 시너지 효과를 나타내고 있습니다. 메탄 및 COa의 직접적인 이용은 아직 개발 단계이지만, 광합성 혼합 배양 시스템이 성숙하면 완전한 탄소 네거티브 특성을 부여할 수 있습니다.

유럽은 2025년 시점에서 43.80%의 점유율을 유지했으며, 에코디자인 규제, 매립세, 소비자 기호가 함께 도입을 가속화하면서 주도적 입장을 유지했습니다. 일회용 플라스틱 지침에 의해 석유 유래의 나이프나 접시의 폐지가 의무화되고 독일, 프랑스, 북유럽 국가의 소매 체인에서는 레토르트 식품의 뚜껑이나 과일용 망에 PHA(폴리하이드록시알카노에이트)의 사용이 진행되고 있습니다. COM4PHA 컨소시엄 등의 연구개발 이니셔티브에서는 공공 보조금과 민간의 노하우를 조합하여 PHBV(폴리히드록시비닐알코올) 화합물의 상용화를 추진해 화장품 용기나 농업용 끈에 대한 응용을 목표로 하면서 지역의 전문성을 더욱 강화하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 24.10%로 가장 빠른 성장을 나타낼 것으로 예상되는 시장입니다. 중국은 기존의 설탕 및 팜유 가공 시설에 PHA 생산 능력을 통합하고 공급 리스크를 헤지함으로써 전환을 주도하고 있습니다. Total Energies와 Bluefa의 협업은 다국적 기업과 국내 그룹이 자본과 다운스트림 채널을 통합하는 좋은 예입니다. 일본은 성능 한계를 높이고 있으며, 카네카사의 플랜트 확장에 의해 연간 생산량은 2만 톤을 돌파할 전망입니다. 동시에 생분해성 어구용 등급의 개발도 선도하고 있습니다. 한국에서는 세계김치연구소의 폐기물에서 PHA로의 실증 프로젝트가 원료 혁신을 통해 폐기물 처리의 과제를 해결하고 폴리머 생산량을 확대하는 방법을 제시하고 있습니다.

북미에서는 규제 추진과 벤처 자금에 의해 견조한 성장을 볼 수 있습니다. 캘리포니아주, 뉴욕주 및 연안부 지자체에서는 EPR(생산자 재활용 책임) 제도에 근거한 수수료가 부과되어 퇴비화 가능 소재에 대한 실질적인 뒷받침이 되고 있습니다. Danimer Scientific의 조지아 확장은 지역 생산량을 증가시키고 브랜드 소유자의 공급 라인을 단축합니다. 캐나다에서 예정된 일회용품 규제와 멕시코에서의 도시 내 발포 스티렌 금지 조치가 추가적인 견인 요인이 됩니다. 또한 지역의 학술기관에 의한 인재 육성이 지속적인 프로세스 최적화를 지원하고 있습니다.

The Polyhydroxyalkanoate market is expected to grow from 49.04 kilotons in 2025 to 60.27 kilotons in 2026 and is forecast to reach 169.04 kilotons by 2031 at 22.91% CAGR over 2026-2031.

Regulatory restrictions on single-use plastics, sizeable investments in production capacity and continuing material-science advances are reinforcing a rapid substitution dynamic in packaging, biomedical and agricultural uses. Europe commands early-mover advantage on account of strict waste-reduction directives, while the Asia-Pacific supply base is scaling fast in response to industrial growth and abundant feedstock. Mixed microbial culture processing is gaining credibility by cutting sterilisation demands, potentially lowering unit costs and broadening the feedstock slate. Competitive intensity remains moderate; established chemical groups such as BASF share the stage with specialist producers and venture-backed start-ups that differentiate through feedstock innovation and application-specific resin design.

Mounting national and municipal restrictions are translating directly into procurement targets for compostable materials. California's Senate Bill 54 established an Extended Producer Responsibility program mandating that all covered materials be recyclable or compostable by 2032, explicitly including PHA in its definition of plastics subject to recycling and reduction targets . Despite classification debates, the EU Single-Use Plastics Directive exerts similar pressure, spurring rapid brand reformulations in food service articles. Hawaii's phased bans on non-biodegradable containers reinforce the trend. Major consumer-goods companies now pilot PHA-based straw, cutlery, and lid programmes to pre-empt penalties, thereby anchoring early-volume contracts for resin suppliers.

Corporate decarbonisation targets and updated eco-design metrics push converters toward materials that can degrade in soil and aquatic environments. PHAs fulfil this requirement because they mineralise without specialised industrial composting, differentiating them from starch blends and polylactic acid. Life-cycle studies record up to 50% lower environmental footprints when PHAs derive their carbon from waste substrates. Packaging, agricultural films, consumer electronics casings and medical disposables therefore constitute growing addressable volume, especially as recent compatibiliser chemistries boost tensile strength and barrier performance.

Commodity plastics trade at roughly USD 1.00-1.30 per kg, whereas commercial PHA grades range from USD 2.25-2.75 per lb, constraining uptake in thin-margined packaging. Process optimisation studies project a possible 30-40% cost reduction when switching to food-waste feedstocks, yet parity remains elusive in the near term. Consequently, end-users prioritise high-value or regulation-driven niches until volumes rise and economies of scale materialise.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The polyhydroxyalkanoate market size for co-polymers reached a leading 25.21 kilotons in 2025, translating into 51.40% share. Co-polymer grades such as PHBV deliver flexibility and oxygen barrier performance that meet chilled-food packaging standards. Recent work blending 50% PHBV with polybutylene adipate terephthalate improved elongation at break and cut water-vapour transmission, paving the way for thermoformed trays in meat and cheese packs. Product formulators also value the ease of downstream conversion on conventional extrusion lines, which curtails capital expenditure.

Terpolymers command only a modest volume base today yet outpace all other resin families at a 23.70% CAGR, underscoring their role in specialised biomedical and electronics housings. Production breakthroughs that boost 4HB content above 50% have enhanced elasticity and slow-release characteristics, useful for absorbable drug-delivery films. As scale grows, terpolymer production will lift the overall polyhydroxyalkanoate market by opening differentiated niches where mechanical demands previously favoured petrochemical elastomers.

Sugar and molasses contributed 56.60% of polyhydroxyalkanoate market share in 2025 on the back of predictable yields and established logistics. Fermentation platforms tethered to sugar-cane or beet supply in Brazil and Thailand create integrated agro-industrial hubs with captive raw materials. Nonetheless, feedstock cost remains the single largest expense at commercial plants. Rising competition for sucrose among ethanol and food markets has sparked a strategic pivot toward waste oils and glycerol, a stream forecast to expand volume at 23.95% CAGR.

Waste-oil pathways lower carbon intensity and deliver up to 40% cost relief, according to trials where Priestia megaterium achieved 42% intracellular PHA content from crude glycerol. Agricultural residues are also gaining traction; cabbage trimmings from kimchi production now feed proof-of-concept bioreactors in South Korea, pointing to regional circular-economy synergies. Methane and direct COa utilisation remain embryonic yet could confer true carbon-negative credentials once phototrophic mixed-culture systems mature.

The Polyhydroxyalkanoate Market Report Segments the Industry by Product Type (Monomers, Copolymers, and Terpolymers), Feedstock (Sugar/Molasses, Plant Oils and Fatty Acids, and More), Production Method (Bacterial Fermentation and More), End-User Industry (Packaging, Agriculture, and More) and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (tons).

Europe retained leadership with 43.80% share in 2025 as eco-design rules, landfill taxes and consumer preference converged to accelerate deployment. The Single-Use Plastics Directive mandates steep reduction of petroleum-based cutlery and plates, prompting retail chains across Germany, France and the Nordics to use PHA for ready-meal lids and fruit nets. R&D initiatives such as the COM4PHA consortium bundle public grants with private know-how to scale PHBV compounds targeting cosmetic jars and agricultural twines, further anchoring regional expertise.

Asia-Pacific is the fastest-growing arena, expanding at 24.10% CAGR to 2031. China champions the transition by integrating PHA capacity into existing sugar and palm-oil processing complexes, thereby hedging against supply risk. TotalEnergies and Bluepha's collaboration exemplifies how multinational and domestic groups pool capital and downstream channels. Japan continues to edge performance thresholds; Kaneka's plant upgrade pushes annual output past 20 kt while pioneering grades tailored for biodegradable fishing gear. South Korea's waste-to-PHA demonstration at the World Institute of Kimchi showcases how feedstock innovation solves disposal headaches and fuels polymer volume.

North America exhibits robust growth supported by regulatory momentum and venture funding. California, New York and several coastal municipalities impose EPR fees that effectively subsidise compostable materials. Danimer Scientific's Georgia expansion will lift local output and offer brand owners shorter supply lines. Canada's forthcoming single-use regulation and Mexico's city-level bans on styrene foams present additional traction points. Regional academics widen the talent pipeline, ensuring sustained process optimisation.