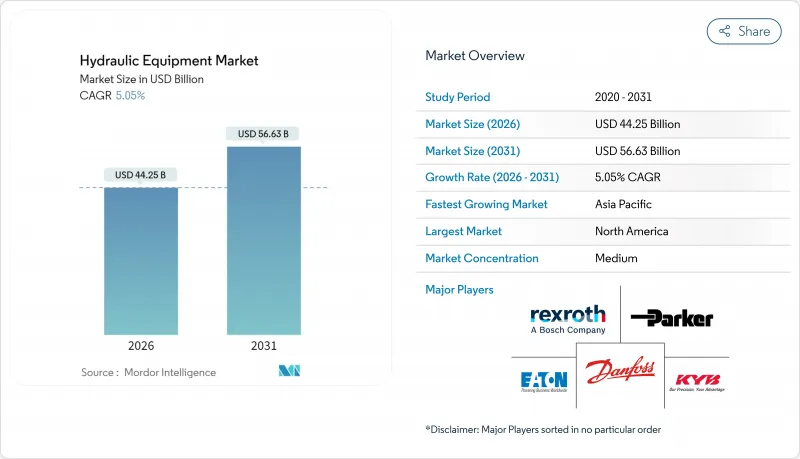

유압 장비 시장은 2025년 421억 1,000만 달러로 평가되었으며, 2026년 442억 5,000만 달러에서 2031년까지 566억 3,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 5.05%를 나타낼 것으로 예상됩니다.

이 꾸준한 성장은 경기 순환에 의한 감속, 원재료 가격의 변동, 전동화에 의한 압력의 상승과 같은 과제에 직면해도, 이 섹터가 가지는 회복력을 뒷받침하고 있습니다. 미국과 중국의 견조한 공공 인프라 투자, 세계의 전자상거래에서의 창고 자동화의 진전, 정밀 농업의 확대가 수요를 지지하고 있습니다. 한편, 기기 제조업체는 에너지 효율이 뛰어난 전기 유압 하이브리드 기술로의 이행을 가속시키고 있습니다. 어플라이드 인더스트리얼 테크놀로지스의 하이드라다인 인수로 대표되는 업계 재편의 가속화는 공급업체가 이익률 압축 및 디지털화 및 고출력 밀도 솔루션의 필요성에 대응하고 있음을 보여줍니다. 북미는 전례 없는 물 인프라 예산에 힘입어 최대의 지역 시장으로 계속되고 있는 한편, 중국과 인도가 수조 달러 규모의 교통·도시 서비스용 경기 자극책을 투입하는 아시아태평양이 가장 급속한 성장을 기록하고 있습니다.

폭발적으로 증가하는 EC 주문량에 대응하기 위해 유통 센터에서는 자율 주행 지게차, 셔틀 시스템, 상품 반송 로봇의 도입이 진행되고 있습니다. 이 장비는 mm 단위의 정확도를 실현하는 소형 서보 유압 실린더에 의존합니다. 아마존의 모바일 로봇 네트워크는 24시간 365일 가동 시 누출이 없는 센서 장착 유압 시스템이 필수적이며, 예지 보전 기능으로 인한 고장 예측으로 다운타임을 최소화할 필요성을 보여줍니다. 창고 운영 회사는 일반적으로 40%의 생산성 향상을 보고하며, 이를 통해 부품 공급업체는 초고신뢰성 및 오염 관리 어셈블리에 프리미엄 가격을 설정할 수 있습니다.

1조 2,000억 달러 규모의 미국 인프라 투자·고용 창출법에서 1조 4,000억 달러 규모의 중국 지방정부 채무계획에 이르는 다년간 유틸리티은 굴삭기, 콘크리트 펌프, 대구경 실린더에 대한 수요 전망을 창출합니다. 장기간의 프로젝트 계획을 통해 OEM 제조업체는 장기 계약 확보, 지역 서비스 거점 확대, 교량, 항만, 재생에너지 건설을 위한 용도 특화형 유압 시스템의 공동 개발이 가능해집니다.

2024년에는 철강 가격이 40% 변동하고 중국이 희토류 가공을 지배했기 때문에 자석·모터공급 체인은 지정학적 리스크에 노출되었습니다. 중국제 유압부품에 대한 44-54%의 관세는 이익률을 더욱 압박하고, 공급자는 상품 헤지의 실시, 재료 사용량의 삭감을 목적으로 한 설계 변경, 혹은 합병에 의한 규모 확대를 촉구하고 있습니다.

2025년 펌프는 건설·농업·산업기계에 있어서 필수적인 동력원으로서 유압 장비 시장의 27.85%를 차지했습니다. 가변 용량식 및 부하 감지식 모델은 연료 소비를 줄이고 OEM의 효율 목표 달성과 애프터마켓 개조 판매 확대에 기여하고 있습니다. 펌프 유압 장비 시장 규모는 2031년까지 인프라 투자주기에 따라 확대될 것으로 전망됩니다. 필터와 어큐뮬레이터는 ISO 4406 청정도 규격의 엄격화로 보증 교섭의 오염 관리가 결정적인 요인이 되기 때문에 6.18%의 연평균 복합 성장률(CAGR)로 가장 급속한 성장을 기록하고 있습니다. 고유량·저차압 필터 매체 수요는 이익률을 향상시키고, 질소 충전식 블래더는 하이브리드 회로로 재생 에너지를 축적해, 이 하위 부문의 유압 장비 시장 점유율을 이동식 용도 전체로 확대하고 있습니다.

밸브 공급업체는 원격 조작 및 자율 작업에 필요한 정밀 유량 제어에 대한 수요를 포착합니다. 실린더는 재현성 있는 고사이클 직선운동을 필요로 하는 전자상거래 창고 로봇의 보급에 의해 혜택을 받습니다. 모터와 변속기는 토크 밀도와 과부하 용량이 여전히 중요한 특수 이동 장비에 공급됩니다. 보조 부품(저장소, 매니폴드, 쿨러)은 OEM 조립 라인을 간소화하고 시장 출시 기간을 단축하는 통합 파워팩의 보급으로 수요를 확대합니다.

건설 분야는 2025년 유압 장비 시장 수익의 31.05%를 차지했습니다. 이것은 세계의 유틸리티 파이프라인과 상업용 부동산 착공이 뒷받침한 것입니다. 플릿 오퍼레이터는 현장 배출 규제 강화에 대응하기 위해 전기 유압 하이브리드를 채용하여 높은 가동률과 부품 소비를 유지하고 있습니다. 건설 분야의 유압 장비 시장 규모는 교량, 항만, 철도 프로젝트가 여러 해 동안 롱 스트로크 액추에이터와 중부하 펌프를 소비하기 때문에 안정된 1자리대 중반의 성장이 전망됩니다. 한편 항공우주 및 방위분야는 민간 내로우 바디기의 생산 확대와 방위기관의 기체 근대화로 6.35%의 연평균 복합 성장률(CAGR)로 가장 급격한 성장 궤도를 나타냅니다. 비행 제어 및 착륙 장치를 위한 중량 최적화 고압 액추에이터는 고가격 대역이며 항공우주 공급업체가 유압 장비 시장에서 차지하는 점유율을 확대하고 있습니다.

농업 분야에서는 정밀 농업에 있어서 GPS 유도 유압 시스템에 의한 센티미터 단위의 종마기 기술의 도입에 의해 꾸준한 성장을 유지하고 있습니다. 자재관리 분야는 옴니채널 소매 물류의 확대로 활황을 나타내고, 석유 및 가스 분야 수요는 해양 구조물 건설이나 파이프라인 보수를 중심으로 안정되고 있습니다. 공작기계, 플라스틱, 자동차 분야는 세계의 제조 사이클에 연동한 동향을 볼 수 있지만, 씰, 밸브, 소구경 실린더 수요에 있어서 필수적인 양산 기반으로서의 지위는 흔들리지 않습니다.

북미는 2025년 세계 수익의 37.65%를 차지했으며, 688억 달러의 물 인프라 정비 자금과 8억 5,000만 달러의 토지 재생 프로젝트 자금에 지원되었습니다. 견조한 창고 자동화 투자와 노후화된 설비의 갱신 수요가 실린더, 비례 밸브, 여과 키트의 판매를 지원하고 있습니다. 그러나 운송 장비 분야 수요 감소는 역풍이 되고 있으며, 공급업체는 애프터마켓 서비스 계약 및 디지털화된 유지보수 서비스 제공에 주력하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 8.07%로 가장 높은 성장률을 나타낼 예정이며, 중국의 1조 4,000억 달러 규모의 신용공여 패키지와 인도의 도시철도·수도 공급계획이 국내 경기순환을 넘은 수요의 피크를 지속시키고 있습니다. 현지 OEM 제조업체는 Tier 4f 기준 대응을 위해 부품 전문 기업과 제휴하는 한편, 관세 분쟁에 의해 다국적 공급업체는 동남아시아에의 조립 거점 분산을 진행하고 있습니다. 고압 마이크로펌프와 내오염 밸브는 한국과 일본의 정밀 제조 클러스터에서 채용이 확대되고 있습니다.

유럽의 전망은 복잡합니다. 독일의 유체동력기기 수주는 2024년 8% 감소했지만 프랑스의 그란 파리 익스프레스와 이탈리아의 풍력발전소 건설 프로젝트가 틈새 고압 수요를 견인하고 있습니다. PFAS 규제 강화로 바이오 베이스 씰로의 전환이 가속화되고 유압 장비 시장 전체에서 대규모 R&D 투자가 진행되고 있습니다. REPowerEU 계획에서 신재생에너지 인프라를 위한 3,000억 유로(3,390억 달러)의 예산 배분은 해상 풍력 발전 설비선을 위한 신축 실린더 수요를 확대하고 거시 경제의 연조를 완화할 전망입니다.

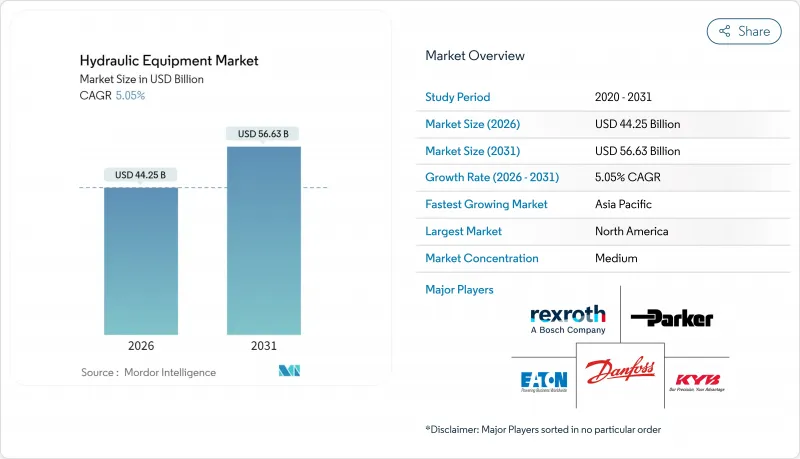

The hydraulic equipment market was valued at USD 42.11 billion in 2025 and estimated to grow from USD 44.25 billion in 2026 to reach USD 56.63 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031).

This steady momentum underscores the sector's resilience in the face of cyclical slowdowns, raw material volatility, and intensifying pressures from electrification. Robust public infrastructure spending in the United States and China, rising warehouse automation in global e-commerce, and expanding precision agriculture underpin demand, even as equipment makers accelerate the shift toward energy-efficient electro-hydraulic hybrids. Heightened consolidation, exemplified by Applied Industrial Technologies' acquisition of Hydradyne, signals how suppliers are responding to margin compression and the need for digital, power-dense solutions. North America remains the largest regional base, supported by unprecedented water infrastructure appropriations, while the Asia-Pacific records the fastest gains as China and India commit multi-trillion-dollar stimulus to transport and urban services.

Explosive e-commerce order volumes compel distribution centers to deploy autonomous forklifts, shuttle systems, and goods-to-person robots that rely on compact servo-hydraulic cylinders for milli-meter accuracy. Amazon's network of mobile robots illustrates how 24/7 operation requires leak-free, sensor-equipped hydraulics offering predictive failure alerts to minimize downtime. Warehouse operators typically report 40% productivity gains, enabling component suppliers to charge premium prices for ultra-reliable, contamination-controlled assemblies.

Multi-year public works-from the USD 1.2 trillion U.S. Infrastructure Investment and Jobs Act to China's USD 1.4 trillion local-government debt plan-create demand visibility for excavators, concrete pumps, and large-bore cylinders. Extended project pipelines allow OEMs to lock-in long-term contracts, expand regional service hubs, and co-develop application-specific hydraulics for bridge, port, and renewable-energy construction.

Steel prices swung 40% in 2024, while China's dominance of rare-earth processing exposes magnet-motor supply chains to geopolitical risk. Tariffs of 44-54% on Chinese hydraulic components further compress margins, forcing suppliers to hedge commodities, redesign to reduce material intensity, or pursue scale through mergers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Pumps anchored 27.85% of the hydraulic equipment market in 2025 as the indispensable power-source across construction, agriculture, and industrial machinery. Variable-displacement and load-sensing models cut fuel draw, satisfying OEM efficiency targets and boosting aftermarket retrofit sales. The hydraulic equipment market size for pumps is positioned to advance with infrastructure investment cycles through 2031. Filters and accumulators log the quickest gains at a 6.18% CAGR as stricter ISO 4406 cleanliness codes make contamination control decisive during warranty negotiations. Demand for high-flow, low-delta-pressure filter media elevates margins, while nitrogen-charged bladders store regenerative energy in hybrid circuits, extending the hydraulic equipment market share of this sub-segment across mobile applications.

Valve suppliers capitalize on precision flow control required by tele-operation and autonomous tasks. Cylinders benefit from e-commerce warehouse robotics that necessitate repeatable, high-cycle linear motion. Motors and transmissions cater to specialty mobile equipment where torque density and overload capacity remain critical. Ancillary components-reservoirs, manifolds, coolers-gain from integrated power-packs that simplify OEM assembly lines and shorten time-to-market.

Construction contributed 31.05% of hydraulic equipment market revenue in 2025, buoyed by global public-works pipelines and commercial real-estate starts. Fleet operators adopt electro-hydraulic hybrids to meet stricter job-site emissions caps, sustaining high utilization and parts consumption. The hydraulic equipment market size for construction is poised for stable mid-single-digit growth as bridge, port, and rail projects consume long-stroke actuators and heavy-duty pumps over multi-year timelines. Aerospace and defense, however, posts the sharpest trajectory at 6.35% CAGR as commercial narrow-body production ramps and defense agencies modernize airframes. High-pressure, weight-optimized actuation for flight-control and landing-gear commands premium pricing, increasing the hydraulic equipment market share captured by aerospace suppliers.

Agriculture maintains steady gains as precision farming embeds GPS-guided hydraulics for centimeter-level seed placement. Material-handling thrives on omnichannel retail logistics, while oil and gas demand stabilizes around offshore construction and pipeline maintenance. Machine-tool, plastics, and automotive segments experience mixed trends tied to global manufacturing cycles yet remain indispensable volume anchors for seal, valve, and small-bore cylinder demand.

The Hydraulic Equipment Market Report is Segmented by Equipment Type (Pumps, Valves, Cylinders, Motors, Filters and Accumulators, Transmissions, and Others), End-User Industry (Construction, Agriculture, Material Handling, and More), Application (Mobile Hydraulics and Industrial Stationary Hydraulics), Operating-Pressure Range (Low, Medium, and High), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 37.65% of global revenue in 2025, supported by USD 68.8 billion in obligated water-infrastructure funds and USD 850 million dedicated to reclamation projects. Robust warehouse-automation investments and aging fleet replacements underpin sales of cylinders, proportional valves, and filtration kits. Nevertheless, the softness of transport equipment presents a headwind, prompting suppliers to emphasize aftermarket service contracts and digitalized maintenance offers.

The Asia-Pacific region registers the fastest growth, with an 8.07% CAGR through 2031, as China's USD 1.4 trillion credit package and India's urban-rail and water-supply programs sustain demand peaks beyond domestic cycles. Local OEMs partner with component specialists to meet Tier 4f standards, while tariff disputes prompt multinational suppliers to diversify assembly footprints into Southeast Asia. High-pressure micro-pumps and contamination-resistant valves are seeing a rising take-up in Korean and Japanese precision-manufacturing clusters.

Europe presents a mixed outlook: German fluid-power orders fell 8% in 2024, yet projects such as France's Grand Paris Express and Italy's wind-farm builds drive niche high-pressure requirements. PFAS restrictions are accelerating the shift to bio-based seals, prompting significant R&D investment across the hydraulic equipment market. The REPowerEU plan's EUR 300 billion (USD 339 billion) allocation for renewable energy infrastructure multiplies demand for telescopic cylinders in offshore wind installation vessels, cushioning macroeconomic softness.