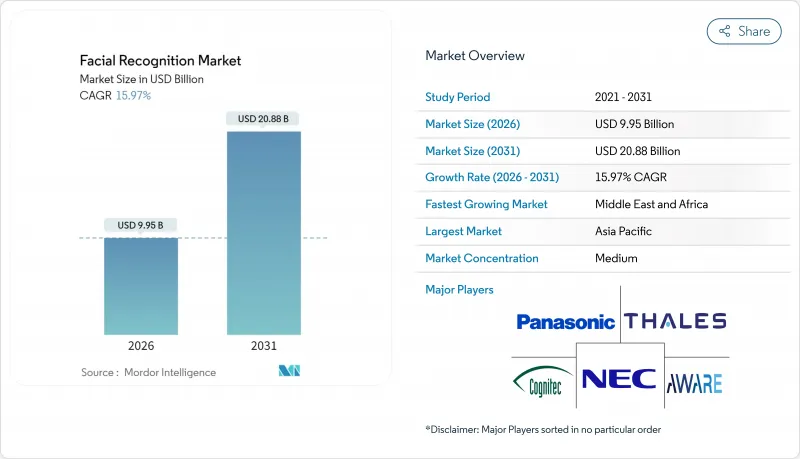

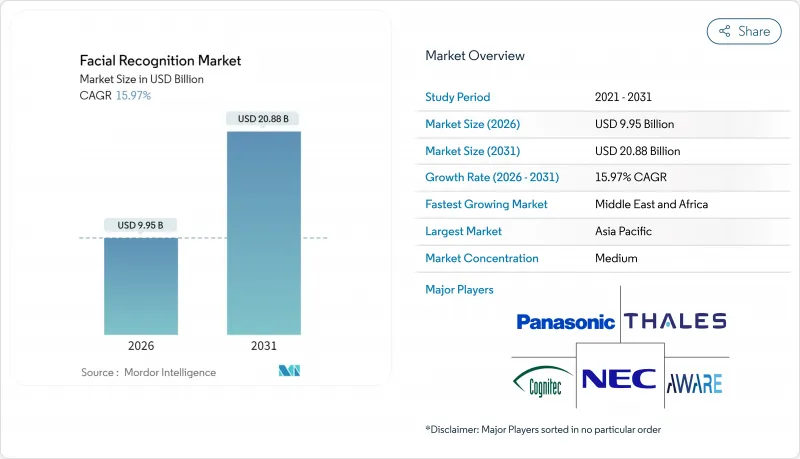

얼굴 인식 시장은 2025년 85억 8,000만 달러로 평가되었고, 2026년에는 99억 5,000만 달러, 2031년까지 208억 8,000만 달러로 성장할 것으로 예상됩니다. 2026년부터 2031년에 걸쳐 CAGR은 15.97%를 나타낼 전망입니다.

현재의 성장은 생체 인증 데이터를 단말기에 유지하면서 1초 미만의 추론을 실현하는 에지 기반 아키텍처에 의존하고 있습니다. 이는 중국 '얼굴인식기술 보안관리조치' 등 신법에 내장된 요건입니다. EU AI 법에 따른 엄격한 동의 규칙은 유럽 구매자를 프라이버시 보호 설계로 이끌어 벤더에게 차등 프라이버시, 동형 암호 및 페더레이티드 학습의 기본 통합을 촉구하고 있습니다. 하드웨어 소형화와 저소비전력 AI 가속기로 스마트폰, 바디카메라, 키오스크가 등록 포인트로 활용되고, 대상 기반은 고정식 CCTV를 훨씬 넘어 확대하고 있습니다. 마지막으로 결제, 여객 대응, 소매 분석이 기존의 보안이용 사례를 보완하여 수익원의 다양화와 지역 간 수요주기의 평준화를 도모하고 있습니다.

2025년까지 베트남은 전 국경에서 생체인증을 의무화?습니다. 싱가포르는 창이 공항 여권 불필요 레인에서 대기 시간을 40% 단축하고 2026년까지 95%의 자동화 이용을 목표로 하고 있습니다. 말레이시아와 파푸아 뉴기니도 전국 전개를 계획하고 있으며, 이로써 아시아태평양의 등록자 수는 누계 8억명을 넘어 디바이스 내 얼굴 인식 시스템의 세계 최대의 시험장이 형성됩니다. 각 공급업체는 라이선스 소득 외에도 아프리카에서 라틴아메리카에 이르는 공공 부문 입찰에 영향을 미치는 참조 아키텍처를 획득합니다. 이러한 프로젝트에서 개발된 상호 운용성 기준은 금융 서비스 사업자가 나중에 동일한 ID 지갑을 재사용할 때 통합 위험을 줄입니다. 결과적으로 얼굴 인식 시장 전반에 걸쳐 소프트웨어, 에지 하드웨어 및 관리형 컴플라이언스 서비스에 대한 구조적인 수요 증가가 이어집니다.

2024년 미국의 조직적 소매범죄 피해액은 1,000억 달러를 넘어 클라우드 서버로 스트리밍하지 않고 얼굴과 행동을 분석하는 엣지 AI 카메라의 도입이 가속화되고 있습니다. 아즈다의 FaiceTech사와의 파일럿 사업에서는 99.992%의 정확도를 달성하고, GDPR(EU 개인정보보호규정) 요건을 충족하기 위해 비일치 데이터를 즉시 삭제하고 있습니다. 미국 상위 50곳의 식료품점 중 15곳이 상습범의 식별이나 직원과 고객의 공모에 의한 부정(스위트 하트 사기)의 검지에 얼굴 인식 기술을 도입하고 있습니다. Nvidia Jetson 또는 EdgeCortix SAKURA-II 보드에서 제공되는 실시간 분석은 상품 분실을 줄이고 마케팅 시스템에 활용되는 방문객 분석 데이터를 생성하여 소매업체에게 수개월 내에 명확한 투자 이익률(ROI)을 제공합니다. 손실 방지와 고객 경험의 개인화라는 이중 이점으로 인해 소매 업계는 얼굴 인식 시장에서 민간 부문에서 가장 빠르게 도입이 진행되는 분야로 계속되고 있습니다.

EU AI법은 원격 생체인증을 '고위험'으로 분류하고, 한정적인 예외를 제외하고 법집행기관에 의한 실시간 이용을 금지합니다. 직장에서의 감정 인식도 금지되어 있습니다. 도입 기업은 데이터 보호 영향 평가를 실시하고 정당한 이익을 입증하고 권력 격차가 존재하는 경우에는 명시적인 동의를 취득해야 합니다. 통합 사업자가 마스킹 기능, 단말 내 처리, 감사 로그를 추가하기 때문에 컴플라이언스 비용은 20-30% 상승합니다. EU 지원 버전을 개발하는 공급업체는 다른 시장에서 프라이버시 바이 디자인 설계 스택을 활용하는 경향이 있지만, 중소기업은 유럽 시장에서 철수 또는 진입 연기를 선택하기 때문에 얼굴 인식 시장의 단기 보급은 둔화되고 있습니다.

2025년에는 알고리즘 개선으로 오인식률이 0.1% 미만으로 떨어졌으며, 표준 CPU에 도입할 수 있게 되었기 때문에 소프트웨어가 세계 수익의 57.20%를 차지했습니다. 엣지 하드웨어는 금융 및 의료 분야의 컴플라이언스 팀이 '생체 인증 템플릿을 시설 밖으로 꺼내지 않는다'를 요구하기 때문에 18.76%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 분야입니다. SAKURA-II 칩은 10W의 전력 예산 내에서 복잡한 모델을 실행할 수 있어 편의점이나 교통 거점 내에서 자율적인 키오스크 실현을 가능하게 합니다.

API 기반 라이선싱을 통해 개발자는 몇 시간 안에 모바일 앱에 얼굴 인식 기능을 통합할 수 있어 전통적인 턴키 프로젝트에서 몇년단위의 일반적인 사이클이 제거되었습니다. 동시에 공급업체는 보안 요소 스토리지 및 전용 가속기와 컴퓨터 비전 SDK를 번들로 제공하여 모든 새로운 분석 모듈이 펌웨어 다운로드로 지속적인 수익원을 확보하고 있습니다. 이 양면 모델은 소프트웨어의 정착률을 높이는 동시에 얼굴 인식 시장 전체의 전환 비용을 끌어올리고 있습니다.

2차원 알고리즘은 기존 CCTV 인프라를 기반으로 하기 때문에 2025년 수익의 43.10%를 차지했습니다. 그러나, 미표정, 주의 지속시간 및 졸음을 해석하는 「감정 AI」엔진은 CAGR18.11%로 확대되어 고객 경험이나 교통 안전 용도를 재구축합니다. 소매업체, 보험사, 자동차업체가 행동분석의 지식을 수익화함에 따라 분석주도모듈의 얼굴인식 시장 규모는 2031년까지 3.40배로 확대될 것으로 예측됩니다.

하이브리드 스택은 3D 심도 정보와 2D RGB 프레임을 융합시켜, 위장을 저지하는 것과 동시에 ISO/IEC 30107-3 준거의 생체 인증 체크를 실현합니다. Suprema의 Q-Vision Pro는 1대당 최대 50,000명의 사용자를 인증할 수 있으며 모든 거래를 엔드 투 엔드로 암호화하므로 ATM 사업자는 PIN 패드를 폐지할 수 있습니다. 이러한 보안과 분석 기술의 융합은 R&D 파이프라인을 지속적으로 강화하고 라이선스, 하드웨어, 서비스의 각 계층에 걸친 수익의 다양화를 도모하고 있습니다.

아시아 지역은 2025년 수익의 38.25%를 차지하고 있습니다. 이는 디지털 공공 인프라에 얼굴 인식을 통합하는 각국 정부의 이니셔티브 때문입니다. 중국의 '보안관리조치'에서는 10만명 이상의 템플릿을 보관하는 사업자는 모두 절전 수준의 사이버 당국에 등록이 의무화되어 있어 안전한 공급망을 가진 기존 벤더에게 유리한 심사 허들이 설치되어 있습니다. 일본의 2025년 오사카·간사이 만박에서는 NEC의 얼굴 인식 결제 시스템이 120만명의 방문자용으로 도입되어 동남아시아 전역으로의 수출 확대의 계기가 되는 실증의 장이 됩니다.

중동에서는 UAE의 생체 인식 ID가 은행, 의료 및 공공 포털에서 플라스틱 카드를 대체하는 동안 CAGR 16.88%로 확대될 것으로 예측됩니다. 두바이 공항은 승객의 얼굴 정보를 탑승 수속과 소매 지갑에 연동시키는 여권이 필요없는 이동 시스템을 계획하고 있으며, 이 지역을 마찰이 없는 이동성 실험실로 자리잡고 있습니다. 걸프 국가 정부는 실증 실험에 자금을 제공하고 신속하게 전국 정책으로 전환함으로써 도입 사이클을 단축하고 얼굴 인식 시장에서 공급업체의 수익 획득을 가속화하고 있습니다.

북미는 항공사 도입과 법 집행기관의 예산에 의해 여전히 중요하지만, 가장 강한 소송 위험에 직면하고 있습니다. 여객 처리 능력의 향상은 부정할 수 없는 것, TSA(운수 보안청)의 확대에 대한 의회의 감시는 시민의 자유에 대한 우려를 부각하고 있습니다. 연방정부의 분단에 의해 일리노이주의 BIPA(바이오메트릭 정보 프라이버시법)나 캘리포니아주의 CPRA(캘리포니아 소비자 프라이버시법) 등 주법이 패치워크 형태로 존재해, 주를 넘는 도입을 복잡화시키고 있습니다. 유럽의 엄격한 규제는 도시의 실시간 감시를 늦추지만, 단말기에서 편집 처리 및 동의 관리를 수행하는 에지 디바이스 수요를 증가시키고, 프라이버시 기술 벤더에게 얼굴 인식 업계 입지를 확보할 수 있도록 합니다.

The Facial Recognition market is expected to grow from USD 8.58 billion in 2025 to USD 9.95 billion in 2026 and is forecast to reach USD 20.88 billion by 2031 at 15.97% CAGR over 2026-2031.

Growth now relies on edge-based architectures that deliver sub-second inference while allowing biometric data to remain on-device, a requirement embedded in new laws such as China's Security Management Measures for Facial Recognition Technology. Stricter consent rules under the EU AI Act steer European buyers toward privacy-preserving designs, pushing vendors to integrate differential privacy, homomorphic encryption, and federated learning by default. Hardware miniaturization and low-power AI accelerators have turned smartphones, body cameras, and kiosks into enrolment points, broadening the addressable base well beyond fixed CCTV. Finally, payments, passenger facilitation, and retail analytics now complement traditional security use cases, diversifying revenue streams and smoothing demand cycles across regions.

By 2025 Vietnam requires biometric authentication at every border, while Singapore's passport-free lanes at Changi have cut wait times by 40% and target 95% automated use by 2026. Malaysia and Papua New Guinea have scheduled nationwide deployments that push cumulative APAC enrolments above 800 million citizens, creating the world's largest testing ground for on-device facial verification systems. Vendors gain not only licence revenue but also reference architectures that influence public-sector bids from Africa to Latin America. Interoperability standards drafted in these projects reduce integration risk for financial-service players that later reuse the same ID wallets. The result is a structural pull-through for software, edge hardware, and managed compliance services across the facial recognition market.

Organized retail crime exceeded USD 100 billion in the United States in 2024, accelerating deployment of edge AI cameras that analyse faces and behaviours without streaming to cloud servers. Asda's pilot with FaiceTech achieves 99.992% accuracy and deletes non-matches instantly to satisfy GDPR mandates. Fifteen of the top 50 US grocers now use facial recognition to flag repeat offenders and detect employee-customer "sweethearting" fraud. Real-time analytics delivered on Nvidia Jetson or EdgeCortix SAKURA-II boards reduce shrinkage and generate footfall intelligence that feeds marketing systems, giving retailers a hard ROI within months. This twin benefit of loss prevention and experience personalisation keeps retail the fastest-growing private-sector adopter in the facial recognition market.

The EU AI Act classifies remote biometric identification as "high-risk," banning real-time use for law enforcement except under narrow exemptions and prohibiting emotion recognition at work. Deployers must run Data Protection Impact Assessments, justify legitimate interest, and obtain explicit consent where power imbalances exist. Compliance costs rise 20-30% as integrators add masking, on-device processing, and audit logs. Vendors building EU-ready versions often re-use the privacy-by-design stack for other markets, but smaller firms exit or defer Europe, slowing short-term diffusion of the facial recognition market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software accounted for 57.20% of global revenue in 2025 as algorithmic improvements lowered false accept rates to below 0.1% and enabled deployment on standard CPUs. Edge hardware remains the fastest-growing slice at 18.76% CAGR because compliance teams in finance and healthcare insist that biometric templates never leave the premises. SAKURA-II chips run complex models within 10 W power budgets, making autonomous kiosks viable inside convenience stores and transit hubs.

API-based licensing lets developers embed facial verification into mobile apps in hours, eliminating the multi-year cycles typical of earlier turnkey projects. At the same time, hardware vendors bundle computer-vision SDKs with secure-element storage and dedicated accelerators, locking in annuity streams as every new analytics module becomes a firmware download. This two-sided model keeps software sticky while raising switching costs for the entire facial recognition market.

2-D algorithms still ride on existing CCTV infrastructure and therefore generated 43.10% of 2025 revenue. Yet "emotion AI" engines that map micro-expressions, attention span, or drowsiness will grow at 18.11% CAGR, reshaping customer-experience and road-safety applications. The facial recognition market size for analytics-driven modules is forecast to rise 3.40 X by 2031 as retailers, insurers, and automakers monetise behavioural insights.

Hybrid stacks blend 3-D depth cues with 2-D RGB frames to thwart spoofing and deliver liveness checks that comply with ISO/IEC 30107-3. Suprema's Q-Vision Pro validates up to 50,000 users per device and encrypts every transaction end-to-end, allowing ATM operators to eliminate PIN pads. Such crossover of security and analytics keeps R&D pipelines full and diversifies revenue across licence, hardware, and service layers.

Facial Recognition Market Report is Segmented by Component (Hardware, Software, Services), Technology (2-D, 3-D, Thermal, Facial Analytics, Hybrid), Deployment (On-Premise, Cloud, Edge), Device (Fixed Cameras, Mobile, Smartphones, Kiosks), Application (Security, Identity Verification, Payments), End-User (Government, BFSI, Retail, Healthcare and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD)

Asia held 38.25% of 2025 revenue thanks to states that embed facial recognition into digital public infrastructure. China's Security Management Measures force any entity that stores templates for more than 100,000 persons to register with provincial cyber authorities, establishing a vetting hurdle that favours established vendors with secure supply chains. Japan's 2025 Osaka-Kansai Expo will run NEC face-payments for an anticipated 1.2 million visitors, a live showcase that can seed exports across Southeast Asia.

The Middle East will expand at a 16.88% CAGR as UAE's biometric ID replaces plastic cards across banking, healthcare, and public portals. Dubai Airport plans passport-free travel that links passengers' faces to boarding and retail wallets in one corridor, positioning the region as a laboratory for frictionless mobility. Gulf governments bankroll proof-of-concepts and rapidly convert them to nationwide policies, compressing adoption cycles and accelerating revenue capture for suppliers within the facial recognition market.

North America remains pivotal through airline rollouts and law-enforcement budgets but faces the strongest litigation risk. Congressional scrutiny over TSA's expansion highlights civil-liberty concerns even as passenger throughput gains are undeniable. Federal fragmentation spawns a patchwork of state laws Illinois' BIPA, California's CPRA making cross-border deployments complex. Europe's strict regime slows real-time city surveillance but ramps demand for edge devices running on-device redaction and consent management, giving privacy-tech vendors a foothold in the facial recognition industry.