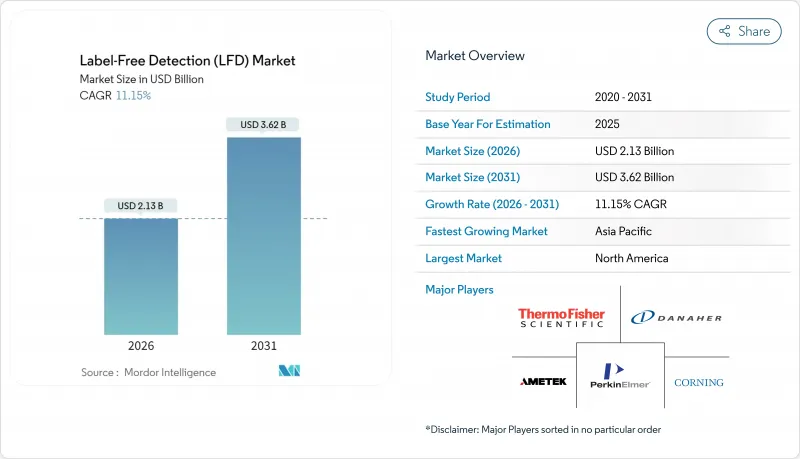

무표지 검출(LFD) 시장은 2025년 19억 2,000만 달러로 평가되었으며, 2026년 21억 3,000만 달러에서 2031년까지 36억 2,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 11.15%로 예상됩니다.

이 확장은 제약 산업에서 실시간 운동 분석으로의 전환, 인공지능 구동 데이터 분석의 광범위한 통합 및 아티팩트가 없는 스크리닝 워크플로에 대한 수요 증가로 인한 것입니다. 표면 플라즈몬 공명(SPR) 및 바이오 레이어 간섭법(BLI) 시스템이 현재 설치를 지배하고 있지만, 소형화된 광섬유 센서와 클라우드 네이티브 소프트웨어가 새로운 프로젝트 구매 기준을 재구성하고 있습니다. 벤더 각사는 기기, 소모품 및 머신러닝 소프트웨어를 구독 모델로 제공해, 신약 개발 타임라인의 단축을 실현하고 있습니다. 한편, 아시아태평양의 투자 우대책은 분석 단가를 줄이는 현지 제조를 촉진하고 있습니다. 나노구조 칩 공급망의 집중화와 숙련 오퍼레이터의 부족이 성장의 기세를 억제하지만, 주요 공급자의 두 자릿수 수익 성장은 둔화되지 않았습니다.

제약연구소에서는 ELISA 대신 SPR 및 BLI 장치를 도입하여 동적, 열역학적 및 화학양론적 파라미터를 실시간으로 생성함으로써 분석 개발 사이클을 수주에서 수일로 단축하고 있습니다. 싸토리우스사는 2024년에 Octet R8e를 도입하여 증발 제어를 개선함으로써 저분자 리드 화합물의 장시간 연속 분석을 실현했습니다. 미국 식품의약국(FDA)은 현재 임상시험약 신청서류에서 무표지 동태해석을 승인하고 있어 검증의 부담이 줄어듭니다. 이들 장치는 미정제 추출물을 분석할 수 있으며, 이는 항체-약물 복합체(ADC)에 있어서 매우 중요한 이점입니다. 그 결과, 위탁연구기관(CRO)은 외부 위탁에 의한 동태특성 평가의 수주 증가를 보고하고 있으며, 이는 북미와 유럽에서 SPR 및 BLI 시스템의 도입 기반 확대를 촉진하고 있습니다.

1,500억 달러 규모의 이중특이적 항체 파이프라인에서는 정확한 사슬의 페어링을 확인하고 오프타겟 효과를 줄이기 위해 정밀한 역학 프로파일링이 요구되고 있습니다. 무표지 분석은 형광 태그에 의해 왜곡을 일으킬 수 있는 결합의 화학양론적 비율과 협조적 상호작용을 정량화합니다. 센서 통합형 프로테옴 랩온어칩 플랫폼에 의해 수천가지 유형의 항체 변이체를 SPR 칩상에서 직접 제조하는 것이 가능해져 암 치료나 자가면역 질환 치료에서의 리드 화합물의 선정이 가속화됩니다. CRO(위탁연구기관)의 생물학적 제제에 관한 키네틱 측정 요구는 40% 증가하고 있으며, 단일클론항체, 이중특이적 항체, 항체-약물 복합체(ADC)의 개발과 관련된 무표지 검출(LFD) 장치 및 소모품에 대한 지속적인 수요가 예상됩니다.

고급 멀티 채널 SPR 시스템은 30만-80만 달러로 판매되며 구매 가격의 15-20%에 해당하는 연간 유지보수 계약이 필요합니다. 따라서 소규모 생명공학기업은 장비를 공유하거나 CRO(위탁연구기관)에 위탁하고 따라서 사내 능력 구축이 지연되고 있습니다. 임대 계약은 초기 비용을 줄이지만 연간 샘플 금액에 상한선이 존재하여 유연성이 제한됩니다. 높은 고정비는 무표지 기술의 보급에서 주요 장벽이며, 구입 사이클은 주요 제약회사나 자금력 있는 연구소에 집중되는 상태가 계속되고 있습니다.

2025년에는 장비 등급이 수익 점유율 51.72%를 차지하면서 제약 R&D 파이프라인에서 핵심 분석 능력을 지원했습니다. 그러나 소프트웨어 및 서비스는 11.55%의 연평균 복합 성장률(CAGR)로 계속 성장하고 있으며, 이는 클라우드 네이티브 분석 기술이 원시 센서그램을 실용적인 SAR 발견으로 변환하고 있기 때문입니다. 구독 라이선스 및 매니지드 분석 서비스에 대한 지출은 연구소가 내부 기술 부족을 회피하는 데 도움이 됩니다. 소모품은 신규 화학 기술이 센서 수명을 연장하고 검출 가능한 분석 대상 물질의 유형을 확대하고 있기 때문에 중간 정도의 성장 기여 요인으로 계속되고 있습니다.

AI 강화 워크플로에는 재생 프로토콜 제안, 질량 운송 아티팩트 플래그 지정 및 추적 적정 권장을 위한 알고리즘이 내장되어 있습니다. 클라우드 리포지토리를 사용하면 여러 사이트의 팀이 실시간으로 곡선을 확인할 수 있으며 이는 일관된 의사결정 프로세스를 보장합니다. 장비 서비스형(Instrument-as-a-Service) 번들은 운용 경비를 프로젝트의 목표와 더욱 연동시켜 스타트업 기업의 무표지 검출(LFD) 시장 진입을 돕는 동시에 설비 투자 장벽을 완화합니다.

2025년 매출액에서 SPR은 46.02%를 차지하였으며 감도와 규제 대응의 숙지도를 바탕으로 주도적 지위를 유지했습니다. 한편, BLI는 일회용 프로브 설계가 미정제 시료를 다루고 세척 사이클을 단축하기 때문에 11.76%의 연평균 복합 성장률(CAGR)로 확대가 예상됩니다. 시차 주사 열량측정법과 등온 적정 열량측정법은 특히 바이러스 단백질 분해효소 억제제 프로그램을 위한 틈새 열역학적 발견을 계속 제공합니다.

SPR과 BLI의 경쟁은 처리 능력과 감도의 균형에 초점을 맞추고 있습니다. 벤더 각사는 SPR의 굴절률 안정성을 향상시키고 자동 마이크로플레이트 핸들러를 갖춘 BLI 시스템을 도입하고 있습니다. 신규 전기화학법 및 임피던스법은 포인트 오브 케어 형식을 타겟으로 하고 있어, 기존에 광학 플랫폼의 도입 자금이 부족했던 환경 분석 연구소의 기술 선택지를 확대하고 있습니다. 이러한 대체 기술은 핵심 SPR/BLI에 대한 지출을 대체하지 않으면서 새로운 기회를 창출하고 있습니다.

북미는 2025년 매출의 38.85%를 차지했으며, 바이오센서 기반 생물 방어 프로젝트를 선호하는 NIH와 BARDA의 견조한 보조금이 이를 지원했습니다. 미국의 주요 제약 기업에서 자본 예산은 단일 채널 SPR 장비에서 하루에 10,000번 상호 작용할 수 있는 16채널 플랫폼으로의 설비 갱신을 자금 측면에서 지원했습니다. 정부의 신속심사제도에서는 생물제제 신청에서 무표지 동태 해석이 인정되고 있으며, 이는 승인까지의 기간 단축과 지역의 주도적 지위 강화로 이어지고 있습니다.

아시아태평양은 2031년까지 12.12%의 연평균 복합 성장률(CAGR)을 나타내 세계에서 가장 빠른 성장이 예상됩니다. 중국의 5개년 생명공학 계획은 국내 SPR 칩 생산을 보조해 소모품 비용을 줄이고 있습니다. 한편 인도의 위탁개발기관(CDO)은 무표지 분석 시스템을 도입하여 바이오의약품 위탁계약의 획득에 주력하고 있습니다. 일본에서는 바이오시밀러의 비교 연구용 장치 도입 기반이 확대되고, 한국에서는 동태 데이터 분석에 특화된 AI 스타트업 기업에 벤처 캐피탈이 유입되고 있습니다. 구미의 장치 제조업체와 지역 제조업체에 의한 크로스보더 합작 사업은 중가격대를 타겟으로 현지 제약 클러스터 전체에서의 도입 기반 확대를 도모하고 있습니다.

유럽은 호라이즌 및 유럽 조성금과 엄격한 동태 비교를 요구하는 성숙한 바이오시밀러 시장에 견인되어 안정적인 성장 지역으로서의 지위를 유지하고 있습니다. 독일과 영국에서는 종합적인 무표지 서비스를 제공하는 CRO(위탁연구기관)의 밀집 거점을 유지하고 있습니다. 반면 프랑스와 이탈리아에서는 EU의 엄격한 오염 역치와 관련된 식품 안전 용도에 기반을 둡니다. 브렉시트 후 규제의 차이로 인해 이중 컴플라이언스 워크플로가 필요하며, 크로스채널의 생명공학 협력에서 조화를 이루는 분석 플랫폼에 대한 수요가 증가하고 있습니다.

The label free detection market was valued at USD 1.92 billion in 2025 and estimated to grow from USD 2.13 billion in 2026 to reach USD 3.62 billion by 2031, at a CAGR of 11.15% during the forecast period (2026-2031).

This expansion stems from the pharmaceutical sector's pivot to real-time kinetic assays, widespread integration of AI-driven data interpretation, and heightened demand for artifact-free screening workflows. Surface plasmon resonance (SPR) and bio-layer interferometry (BLI) systems dominate present installations, yet miniaturized fiber-optic sensors and cloud-native software are reshaping purchasing criteria for new projects. Vendors bundle instruments, consumables, and machine-learning software in subscription models that compress drug-discovery timelines, while regional investment incentives in Asia-Pacific nurture local manufacturing that lowers per-assay costs. Supply chain concentration in nanostructured chips and shortages of skilled operators temper momentum but have not slowed double-digit revenue growth for leading suppliers.

Pharmaceutical laboratories are replacing ELISA with SPR and BLI instruments that generate kinetic, thermodynamic, and stoichiometric parameters in real time, shrinking assay development cycles from weeks to days. Sartorius introduced the Octet R8e in 2024, improving evaporation control that supports extended run times for low-molecular-weight leads. The U.S. Food and Drug Administration now accepts label-free kinetics in investigational new drug dossiers, which reduces validation overhead. These instruments analyze crude lysates without purification, a critical advantage for antibody-drug conjugates. Consequently, contract research organizations (CROs) report rising orders for outsourced kinetic characterization, amplifying installed-base growth of SPR and BLI systems in North America and Europe.

The USD 150 billion bispecific-antibody pipeline requires precise kinetic profiling to confirm correct chain pairing and mitigate off-target effects. Label-free assays quantify binding stoichiometry and cooperative interactions that fluorescent tags can distort. The Sensor-integrated Proteome On Chip platform enables thousands of antibody variants to be produced directly on SPR chips, expediting lead selection for oncology and autoimmune therapies. CROs record a 40% rise in biologics-related kinetic requests, indicating that the label free detection market will continue to see sustained instrument and consumable demand linked to monoclonal, bispecific, and antibody-drug conjugate development.

Advanced multi-channel SPR systems sell for USD 300,000-800,000 and require annual service contracts equal to 15-20% of purchase price. Smaller biotechs therefore share instrumentation or outsource to CROs, slowing in-house capability build-out. Leasing schemes reduce initial cash outlay but often cap annual sample volumes, limiting flexibility. High fixed costs remain the primary hurdle to wider diffusion of label-free technology, keeping the purchasing cycle concentrated among top-tier pharmaceutical firms and well-funded research labs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The instrument class dominated with 51.72 % revenue share in 2025, underpinning core assay capacity across pharmaceutical R&D pipelines. Software and services, however, are advancing at an 11.55 % CAGR because cloud-native analytics convert raw sensorgrams into actionable SAR insights. Spending on subscription licences and managed-analysis services helps laboratories sidestep internal skill shortages. Consumables remain a moderate growth contributor as novel chemistries extend sensor life and broaden detectable analyte classes.

AI-augmented workflows embed algorithms that suggest regeneration protocols, flag mass-transport artifacts, and recommend follow-up titrations. Cloud repositories enable multi-site teams to view curves in real time, ensuring consistent decision gates. Instrument-as-a-service bundles further align operating expenses with project milestones, drawing startups into the label free detection market while tempering capital-expenditure barriers.

SPR accounted for 46.02 % of 2025 revenues, retaining leadership based on sensitivity and regulatory familiarity. BLI, though, is projected to expand at a 11.76 % CAGR as disposable probe designs tolerate crude samples and shorten cleaning cycles. Differential scanning calorimetry and isothermal titration calorimetry continue to supply niche thermodynamic insights, especially for viral protease inhibitor programs.

Competition between SPR and BLI centers on throughput versus sensitivity. Vendors enhance SPR with higher refractive-index stability and introduce BLI systems featuring automated microplate handlers. Emerging electrochemical and impedance methods target point-of-care formats, widening technology options for environmental labs that historically lacked capital for optical platforms. These alternatives create incremental opportunities without displacing core SPR/BLI spend.

The Global Label-Free Detection Market Report is Segmented by Product Type (Instruments, Consumables, Software & Services), Technology (Surface Plasmon Resonance, Bio-Layer Interferometry, and More), Application (Binding Kinetics & Affinity, and More), End User (Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 38.85 % of 2025 revenue, underpinned by robust NIH and BARDA grants that favor biosensor-based biodefense projects. Capital budgets at major U.S. pharmaceutical firms funded fleet upgrades from single-channel SPR instruments to 16-channel platforms capable of 10,000 interactions per day. Government fast-track review pathways recognize label-free kinetics in biologics filings, shortening time-to-approval and reinforcing regional leadership.

Asia-Pacific is projected to log a 12.12 % CAGR to 2031, the fastest worldwide. China's five-year biotech plan subsidizes domestic SPR chip production, lowering consumable costs while India's contract-development organizations add label-free suites to capture biologics outsourcing contracts. Japan deepens its installed base for biosimilar comparability studies, and South Korea channels venture capital into AI-analytics startups focused on kinetic data. Cross-border joint ventures between Western instrument makers and regional manufacturers target mid-tier pricing that broadens installed base across local pharma clusters.

Europe retains its status as a steady growth region, driven by Horizon-Europe grants and a maturing biosimilar market that demands rigorous kinetic comparability. Germany and the United Kingdom maintain dense footprints of CROs offering full-spectrum label-free services, while France and Italy anchor food-safety applications connected to strict EU contamination thresholds. Regulatory divergence post-Brexit necessitates dual compliance workflows, elevating demand for harmonized analytics platforms in cross-channel biotech collaborations.