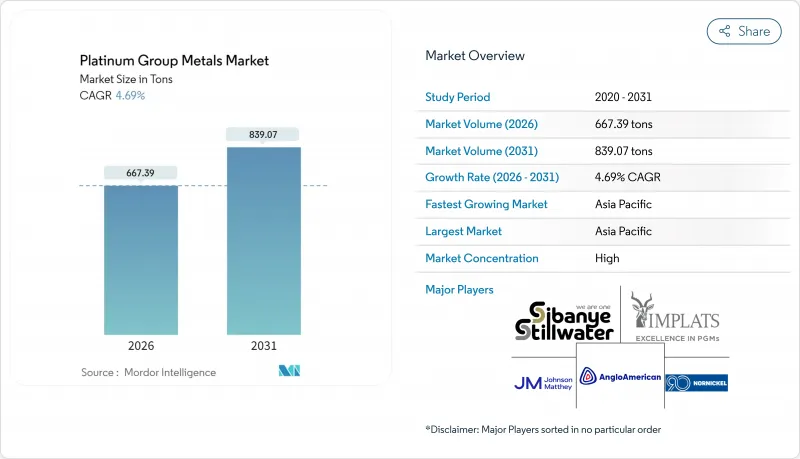

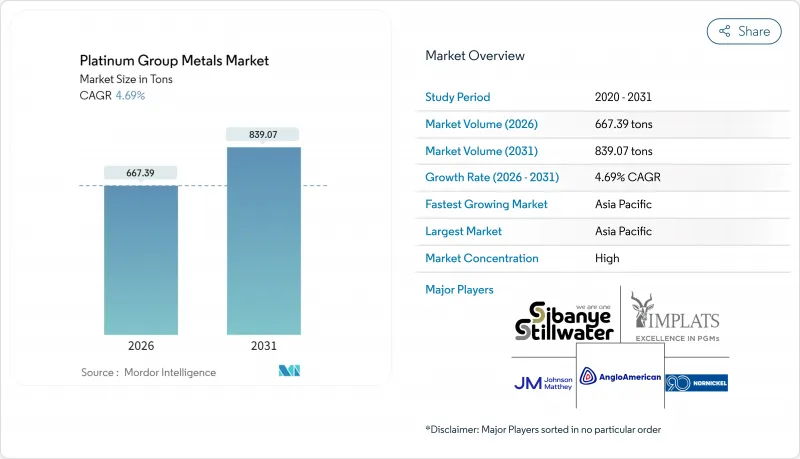

백금족 금속 시장은 2025년 637.51톤으로 평가되었으며, 2026년 667.39톤, 2031년까지 839.07톤에 이를 것으로 예측되고 있습니다. 예측기간(2026-2031년) CAGR은 4.69%를 나타낼 전망입니다.

백금족 금속 시장은 두 가지 수요원의 혜택을 누리고 있습니다. 가솔린 및 하이브리드 자동차용 자동차 촉매의 지속적인 수요와 양성자 교환막(PEM) 수소 기술의 급속한 보급 확대의 혜택을 누리고 있습니다. 촉매에서 팔라듐에서 백금으로의 전환은 단기적인 시장 심리를 밀어 올리는 반면 장기적인 기회는 그린 수소의 확대에서 유래합니다. 이에 따라 2025년까지 PEM 전해장치용 백금 수요가 전년 대비 두배로 될 것으로 예측됩니다. 이리듐공급 제약, 아시아의 보석품의 견고함, 첨단 전자기기에서의 PGM 사용량 증가가 함께 가격의 기반을 지원하고 있습니다. 한편, 가격 변동의 지속과 남아프리카의 생산 비용 상승은 특히 연료전지 OEM 제조업체에서 장기 공급 계약의 체결을 억제하고 있습니다.

승용차, 하이브리드차, 대형 트럭을 합친 PGM 소비량은 2024년 전체의 60%를 차지했습니다. 보다 엄격한 유로 7 및 중국 VI-b 기준으로 차량당 PGM 사용량이 증가하고 가솔린 생산량 감소를 상쇄하고 있습니다. 하이브리드 자동차용 촉매는 특히 PGM 함량이 높고 2025년 자동차 촉매용 백금 수요 예측을 8년 만의 높은 수준인 324만 온스로 끌어 올리고 있습니다. 대형 차량은 더욱 고농도의 PGM이 필요하며, 승용차 수요 감속의 영향을 받기 어려운 수익성이 높은 틈새 시장을 형성하고 있습니다. 아시아 시장 규모와 청정 엔진 추진을 위한 정부 지원책이 함께 플래티넘족 금속 시장은 자동차 수요에 강하게 의존한 상태를 유지하고 있습니다.

수소 관련 플래티넘 수요는 2030년까지 875koz에 이른 후 2025년에는 다시 배가 될 것으로 전망됩니다. 캐나다의 클린 수소 세액 공제(40%)와 미국의 인플레이션 억제법은 몇 기가와트 규모의 전해조 주문을 지원합니다. 이리듐공급 부족이 장벽이 되어 2024년의 생산량은 불과 7.7톤이었습니다. 스몰텍의 나노스케일 코팅 기술 등 PEM 셀에서의 이리듐 사용량을 95% 삭감하는 기술적 돌파구는 공급 확대에 필수적입니다. 이러한 진전이 백금족 금속 시장의 장기적인 성장 기반을 확고하게 하고 있습니다.

남아프리카의 전력 제한과 노동 쟁의가 채굴 비용을 끌어 올렸습니다. 앵글로 아메리칸 플래티넘사의 2024년 단위 비용은 6E 온스당 20,922랜드(전년 대비 5% 증가)가 되었습니다. 깊은 광상에서는 첨단 냉각 기술과 광맥 안정화가 필요하며 고정비 기반을 밀어 올리고 있습니다. 가격 침체 기간 동안 스윙 생산자는 손익 분기점 또는 적자로 운영하므로 확장을 위한 자본 능력이 감소합니다. 이러한 역학은 공급 안정성에 하향 위험을 추가하고 백금족 금속 시장에서 장기 계약을 제한합니다.

팔라듐은 가솔린 촉매가 소비를 계속 견인한 2025년 PGM 시장의 46.55%를 차지했습니다. 주로 PEM 전해조 애노드에 사용되는 이리듐은 2031년까지 연평균 복합 성장률(CAGR) 8.92%를 보일 것으로 예측되어 전체 PGM 중에서 가장 높은 성장률을 나타냅니다. 공급 박멸과 기술 의존성에 의해 이리듐의 가격 프리미엄이 유지되고 향후 수년간 PGM 시장 규모에 대한 공헌도가 확대됩니다. 백금의 부활은 가솔린 촉매에 대한 대체 수요로 인해 2023년에만 60만 온스 이상 수요 전환이 발생했습니다. 로듐은 대체품이 한정되기 때문에 고가격을 유지하고 루테늄과 오스뮴은 틈새 화학·데이터 스토리지 용도로 수요를 확대하고 수익원의 다양화를 도모하고 있습니다.

PEM 시스템과 고급 메모리의 지속적인 부하 증가로 이리듐과 루테늄은 특수 용도에서 주류 용도로 전환하고 있습니다. 2024년 로듐 가격은 평균 5,375달러/온스와 공급 제약을 시사합니다. 백금 공급 확대와 대체 수요 정착으로 견고한 수요가 유지되고 PGM 시장은 안정화되고 있습니다. 디스크 드라이브 등의 기술 폐기물의 리사이클율 향상은 루테늄공급 안정성을 높여 가격 상승 압력을 완화하는 한편, 전자 기기 제조업체가 중시하는 순환형 경제에의 공헌도를 강화하고 있습니다.

보석품 분야는 2025년에 있어서도 PGM 소비량의 28.75%를 차지했고, 특히 중국, 일본, 인도에 있어서 최대의 용도로서의 지위를 확고한 것으로 하고 있습니다. 거시경제의 연조함에도 불구하고 조용한 사치 동향과 백금의 투자 매력이 기초 수요를 지지하고 있습니다. 한편, 연료전지 분야는 멀티기가 와트급 전해장치 프로젝트나 고정형 전원 프로그램에 지지되어 28.47%의 연평균 복합 성장률(CAGR)로 급성장하고 있습니다. 따라서 연료전지 스택용 백금 금속 시장 규모는 2031년까지 급속히 확대될 것으로 예측됩니다.

배출 규제 기준이 강화됨에 따라 자동차 촉매는 여전히 필수적입니다. 반도체 노드가 3nm 이하로 미세화됨에 따라 전자기기 용도도 계속 증가하고 있습니다. 유리 섬유 제조와 안료 용도에서는 백금의 높은 융점이 활용되고, 의료기기 분야에서는 카테터나 스텐트에의 생체 적합성이 중시되고 있습니다. 화학공정용 촉매, 특히 질산제조 및 정유소의 수소화분해공정에서는 여전히 다량이고 안정된 PGM 소비량이 예상되어 경기변동을 헤지하는 다양한 용도기반을 제공합니다.

백금족 금속 보고서는 금속종별(플래티넘, 팔라듐, 로듐 등), 용도별(자동차 촉매, 전기 및 전자기기 등), 공급원별(1차(채굴), 재생/2차), 최종 이용 산업별(자동차, 공업용 화학제품 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류 시장 예측은 수량(톤) 단위로 제공됩니다.

2025년 아시아는 백금족 금속 시장에서 51.60%라는 압도적인 점유율을 차지했습니다. 이는 자동차 촉매용 팔라듐 및 보석품용 백금의 최대 소비국인 중국의 지위에 의해 뒷받침됩니다. 베이징이 국내 가격 결정권을 얻기 위해 광저우 선물 거래소는 백금 및 팔라듐 선물 계약을 상장했습니다. 이로 인해 유동성이 깊어지고 산업 사용자가 장기 포지션 헤지를 할 것을 촉구합니다(닛케이 아시아). 일본의 보석품 수요 회복과 인도의 혼례 수요에 견인된 장식품 수요가 지역적인 수요를 강화하는 한편, 대만과 한국의 전자기기 산업 클러스터가 공업용 소비를 지지하고 있습니다.

유럽에서는 독일과 영국의 엄격한 배출 규제를 배경으로 소비량이 크게 증가하고 촉매 부하량이 증가하고 있습니다. 향후 도입 예정인 유로 7 규제에 의해 승용차 및 대형 차량 양쪽의 PGM 사용량이 증가할 전망입니다만, 전기자동차로의 이행이 수요 밸런스를 복잡화시키고 있습니다. 유럽은 PGM 재활용의 첨단 지역이기도 합니다. 존슨 매세이와 우미코어는 배출량을 최소화하면서 자동차 촉매 금속을 회수하는 최첨단 시설을 운영하고 있으며, 순환형 경제의 목표 달성을 지원함과 동시에 백금족 금속 시장의 안정화에 공헌하고 있습니다.

북미는 수소정책과 가솔린차 판매의 지속으로 성장 거점으로 대두하고 있습니다. 캐나다는 세계 3위의 팔라듐 생산국, 4위의 백금 생산국으로 2022년에는 주로 온타리오주에서 71만 온스가 채굴되었습니다. 오타와 정부의 청정수소세제 우대책은 전해장치 프로젝트를 가속화하고, 이 지역에 대한 백금 및 이리듐의 추가 수요를 공급합니다. 미국의 인플레이션 억제법은 수소허브에의 자금 제공에 의해 이 흐름을 강화해, 백금족 금속 시장의 장기적인 전망을 확고하게 하고 있습니다.

The Platinum Group Metals Market was valued at 637.51 tons in 2025 and estimated to grow from 667.39 tons in 2026 to reach 839.07 tons by 2031, at a CAGR of 4.69% during the forecast period (2026-2031).

The Platinum group metals market benefits from a dual-track demand profile: sustained autocatalyst requirements in gasoline and hybrid vehicles and fast-accelerating adoption in proton-exchange-membrane (PEM) hydrogen technologies. The ongoing palladium-for-platinum shift in catalysts buoys short-term sentiment, while longer-term opportunity stems from green-hydrogen build-outs expected to double platinum demand for PEM electrolysers year-on-year through 2025. Iridium supply constraints, jewelry's resilience in Asia, and increasing PGM intensity in advanced electronics collectively support price fundamentals. Simultaneously, persistent price volatility and rising South African production costs inhibit long-dated offtake contracts, especially for fuel-cell OEMs.

Passenger cars, hybrids, and heavy-duty trucks together consumed 60% of all PGMs in 2024. Stricter Euro 7 and China VI-b standards raise PGM loadings per vehicle, offsetting lower gasoline production volumes. Hybrid-vehicle catalysts are especially PGM-dense, pushing projected platinum autocatalyst demand to an eight-year high of 3.24 million oz in 2025. Heavy-duty vehicles require even higher PGM doses, creating a profitable niche that shields producers from passenger-car headwinds. Asia's scale, coupled with government incentives for cleaner engines, keeps the Platinum group metals market firmly reliant on automotive offtake.

Platinum demand linked to hydrogen is expected to double again in 2025, after reaching 875 koz by 2030, roughly 10% of total platinum use. Canada's 40% clean-hydrogen tax credit and the United States' Inflation Reduction Act underpin multi-gigawatt electrolyser orders. Iridium scarcity is an obstacle: 2024 production barely reached 7.7 tons. Technology breakthroughs, such as Smoltek's nanoscale coatings that reduce iridium loading in PEM cells by 95%, are vital for scaling supply. These developments solidify a long-run growth platform for the Platinum group metals market.

Electricity load shedding and labor unrest in South Africa elevated mining costs: Anglo American Platinum's unit cost rose 5% to ZAR 20,922 per 6E oz in 2024. Deep-level deposits require advanced refrigeration and reef stabilization, elevating the fixed-cost base. During price troughs, swing producers operate at breakeven or losses, reducing capital capacity for expansion. These dynamics add downside risk to supply stability and limit long-term contracts for the Platinum group metals market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Palladium captured 46.55% of the Platinum group metals market in 2025 as gasoline catalysts continued to dominate consumption. Iridium, used chiefly in PEM electrolyser anodes, is projected to grow at a 8.92% CAGR through 2031, the fastest among all PGMs. Tight supply and technological reliance sustain iridium's price premium, magnifying its contribution to the Platinum group metals market size in later years. Platinum's renaissance stems from its substitution into gasoline catalysts; over 600 koz converted demand in 2023 alone. Rhodium's limited substitutes command high pricing, while ruthenium and osmium gain traction in niche chemical and data-storage applications, diversifying revenue streams.

Persistent load-growth in PEM systems and advanced memory drives iridium and ruthenium from specialty to mainstream status. Prices for rhodium averaged USD 5,375 /oz in 2024, indicative of constrained supply. Platinum's wider availability and ongoing substitution lock-in robust demand, stabilizing the Platinum group metals market. Recycling yields of technological scraps such as disk drives improve ruthenium supply security, tempering upward price pressure but reinforcing circular-economy credentials prized by electronics firms.

Jewelry retained 28.75% of PGM consumption in 2025, cementing its status as the largest application, especially across China, Japan, and India. Quiet-luxury trends and platinum's investment appeal sustain baseline volumes despite macroeconomic softness. The fuel-cell segment, however, is racing ahead with a 28.47% CAGR, supported by multi-gigawatt electrolyser initiatives and stationary power programs. The Platinum group metals market size allocated to fuel-cell stacks is thus expected to expand rapidly through 2031.

Autocatalysts remain indispensable as lawmakers raise emission-control thresholds. Electronics applications keep climbing as semiconductor nodes shrink below 3 nm. Glass fibre production and pigment uses leverage platinum's high melting point, while medical devices rely on its biocompatibility for catheters and stents. Chemical-process catalysts, notably in nitric-acid and refinery hydrocracking, continue to consume sizable but steady PGM volumes, offering a diversified application base that hedges cyclical swings.

The Platinum Group Metals Report is Segmented by Metal Type (Platinum, Palladium, Rhodium, and More), Application (Auto Catalysts, Electrical and Electronics, and More), Source (Primary (Mined), Recycled/Secondary), End-Use Industry (Automotive, Industrial Chemicals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Asia held a commanding 51.60% share of the Platinum group metals market in 2025, underpinned by China's status as the largest consumer of palladium for autocatalysts and platinum for jewelry. Beijing's pursuit of domestic pricing power led the Guangzhou Futures Exchange to list platinum and palladium contracts, deepening liquidity and encouraging industrial users to hedge long-term positions Nikkei Asia. Japan's jewelry rebound and India's wedding-driven ornament demand strengthen regional pull, while the region's electronics clusters in Taiwan and South Korea reinforce industrial consumption.

Europe, driven by stringent emissions mandates in Germany and the United Kingdom, has experienced significant growth in consumption, leading to heightened catalyst loadings. The forthcoming Euro 7 framework stimulates additional PGM intensity in both passenger and heavy-duty platforms, although the electric-vehicle transition creates a complex demand balance. Europe also champions PGM recycling: Johnson Matthey and Umicore run state-of-the-art facilities that recover autocatalyst metals with minimal emissions, supporting circular-economy targets and stabilizing the Platinum group metals market.

North America is emerging as a growth pole thanks to hydrogen policies and sustained gasoline vehicle sales. Canada is the world's third-largest palladium and fourth-largest platinum producer, with 710,000 oz mined in 2022, chiefly in Ontario Natural Resources Canada. Ottawa's clean-hydrogen tax incentive accelerates electrolyser projects, channelling additional platinum and iridium demand into the region. The United States' Inflation Reduction Act amplifies this trajectory by funding hydrogen hubs, reinforcing long-run prospects for the Platinum group metals market.