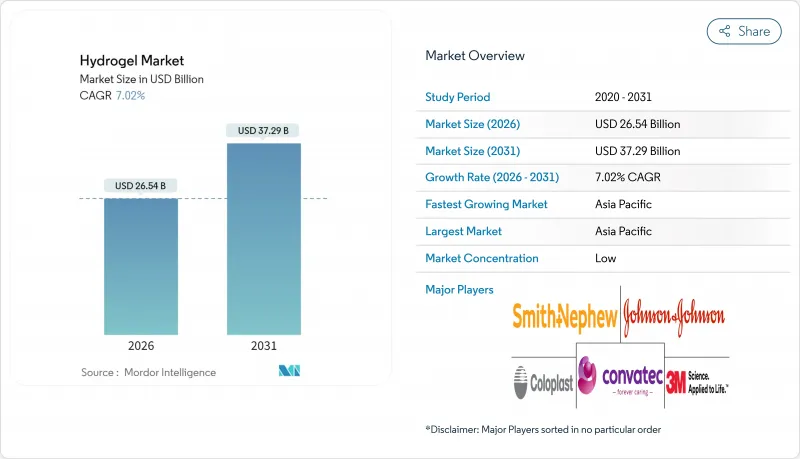

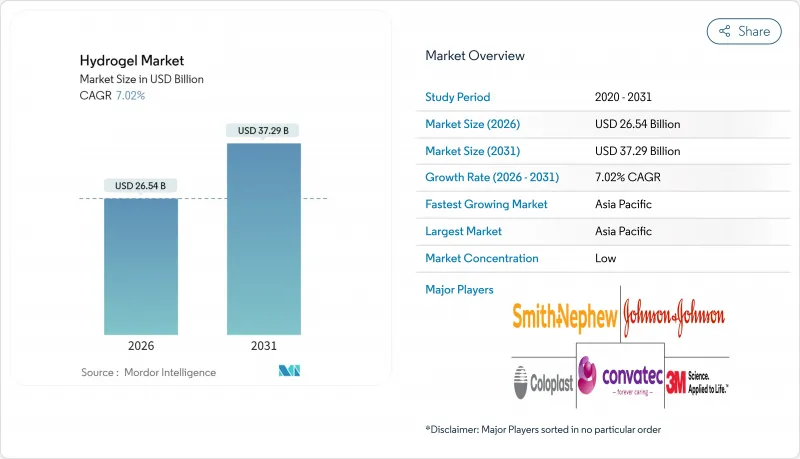

2026년 하이드로겔 시장 규모는 265억 4,000만 달러로 추정되며, 2025년 248억 달러에서 성장한 수치입니다. 2031년에는 372억 9,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.02%로 성장할 전망입니다.

이 확장은 급속한 재료 혁신, 의료, 농업, 개인 관리 분야의 응용 범위 확대 및 바이오 화학이 엄격한 지속가능성 요구 사항과 일치한다는 것을 반영합니다. 장기 착용형 실리콘 하이드로겔 콘택트렌즈, 4D 프린트 임플란트, 토양 개량용 고흡수성 폴리머는 측정 가능한 임상 효과와 자원 효율 향상을 제공함으로써 수요 증가의 대부분을 견인하고 있습니다. 아시아태평양은 지속적으로 상당한 수량 성장을 유지하고 있지만, 북미와 유럽은 규제에 대한 전문 지식과 신속한 혁신 사이클을 통해 프리미엄 가격의 실현을 유지하고 있습니다. 원료 가격의 변동과 비생분해성 고흡수성 폴리머에 대한 매립 규제는 이익률을 억제하는 한편, 재생 가능 모노머나 분해성 네트워크로의 이행을 가속화하고 있습니다. 전반적으로 비용 중심의 상품 제품이 현금 흐름을 지원하고 고 부가가치 의료기기와 스마트 농업이 평균 판매 가격을 밀어 올려 하이드로겔 시장은 균형 잡힌 성장 기세를 누리고 있습니다.

임상적 증거는 하이드로겔 드레싱이 거즈나 폼에 비해 상피화를 촉진하고 드레싱 교환 빈도를 감소시키는 것으로 나타났으며, 병원 네트워크에 의한 프로토콜에 대한 광범위한 채택이 진행되고 있습니다. 2025년 1월 FDA가 승인한 콜라겐 기반 DermiSphere hDRT는 세포외 매트릭스를 모방하는 스캐폴드가 수동 코팅이 아닌 재생 의료 플랫폼으로 효과적임을 입증했습니다. 포괄 지불 모델을 채택하는 의료 시스템에서는 단가는 높고, 총 의료비의 삭감 효과가 인정되고 있습니다. ISO 13485 준수 및 CE 마킹은 다국적 개발을 효율화하고 저품질 모방품으로부터 혁신 기업을 보호합니다. 지불기관이 치료성과를 중시하는 가운데, 치유기간의 단축과 감염률의 저감을 실증하는 공급업체는 가격 결정력을 유지합니다.

현대의 아기용 기저귀와 여성용 생리용 냅킨에는 무게의 500-1000배를 흡수 가능한 하이드로겔 입자가 내장되어 있어 누출이 없는 얇은 제품을 실현하고 있습니다. 중국과 일본의 대규모 제조업체는 확립된 폴리아크릴레이트 네트워크를 활용하는 한편, 신규 참가 기업은 유럽 및 아시아의 마이크로 플라스틱 규제에 대응하기 위해, 식물 유래의 아크릴산 프로세스를 추구하고 있습니다. 소비자의 편안함에 대한 요구는 입자 크기와 겔 강도에 대한 기술 개발을 촉진하고 지속적인 R&D 투자를 필요로 합니다. 인도, 인도네시아, 나이지리아의 도시화가 두 자릿수의 수량 성장을 지원하고 위생 용품 시장이 하이드로겔 시장 규모에서 최대의 단일 수요원으로 지속되는 것을 보증하고 있습니다.

원유가격의 변동으로 아크릴산가격은 연간 최대 40%의 변동폭을 나타내며, 프로파일렌EIA에의 후방통합이 불충분한 생산자의 이익률을 압박하고 있습니다. 실리콘 단량체 시장은 중국에서 폴리실록산 생산 능력의 향상을 반영하여 추가 비용 불확실성을 창출하고 있습니다. 헤징, 복수 조달처 확보, 지수 연동형 고객 계약에 의해 리스크는 부분적으로 경감됩니다만, 소량 생산의 특수 배합 제조업체는 조달면에서 불리한 입장에 놓여 있습니다. 바이오 제조 루트는 가격 안정성을 약속하지만 높은 자본 집약성과 스케일 업 타임라인이 필요합니다.

2025년 시점에서 반결정성 등급은 하이드로겔 시장 점유율의 45.35%를 차지했습니다. 그 규칙적인 결정 영역이 하중을 지지하는 상처 피복재나 토양 개량제에 필수적인 인장 강도를 제공하기 때문입니다. 예측 가능한 팽윤 역학은 제어된 약물 방출 매트릭스를 지원하고, 낮은 크리프 변형률은 장기 착용 응용에서 제품 고장 위험을 감소시킵니다. 제조업체는 동아시아를 기반으로 하는 확립된 공급망을 활용하여 규모의 우위성과 경쟁력 있는 가격 설정을 확보하고 있습니다. 그러나 연구기관에서는 기계적 무결성과 확산속도의 밸런스를 취하기 위해 결정성-비정질 비율의 개량을 진행하고 있어 근골격 재생을 위한 차세대 스캐폴드 실현을 가능하게 하고 있습니다.

비정질 하이드로겔은 급속한 용매 교환 및 세포 침윤을 필요로 하는 주사용 치료제 및 3D 바이오프린트 조직 수요에 힘입어 7.96%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다. 그것의 무작위 코일 네트워크는 전단 감점 특성을 촉진하고 복잡한 해부 부위에 맞는 낮은 침습 투여를 허용합니다. 바이오의약품 기업은 체온에서 겔화하는 열 응답성 공중합체를 통합하여 외과적 고정 없이 부위 유지성을 향상시키고 있습니다. 급속한 분해의 영향으로 하중 지지 용도는 제한되는 것, 가교 제어와 나노셀룰로오스에 의한 복합 보강에 의해 재건 외과, 안과, 약제 저장소 등 폭넓은 이용 사례가 확대되고 있습니다.

아시아태평양은 2025년에 세계 하이드로겔 시장 매출의 41.00%를 차지했고, 2031년까지 연평균 복합 성장률(CAGR)7.98%로 확대해 세계 평균을 상회할 전망입니다. 중국의 이점은 통합된 아크릴산 생산 능력과 가뭄 다발 지역에서 고흡수성 토양 개량제의 보조금 정책에 의해 뒷받침됩니다. 일본에서는 HOYA 주식회사 등의 기업이 고정밀 중합 기술과 세계 유통망을 구사해 실리콘 하이드로겔 콘택트렌즈 분야의 혁신을 견인하고 있습니다. 한국은 규제 대응의 신속성과 전자기기 제조 노하우를 융합시켜 유연한 바이오 일렉트로닉스용 하이드로겔 부품공급에 있어서 국내 기업의 우위성을 확립하고 있습니다.

북미는 의료·농업 분야에서 고부가가치를 확립하고 있으며, FDA의 명확한 규제, 벤처 자금, 첨단적 제조 인프라의 혜택을 받고 있습니다. 미국에서는 당뇨병 환자 증가에 따라 만성 상처 치료에 하이드로겔 드레싱의 채택이 진행되고 서부 제주에서는 심각한 물 부족 대책으로서 고흡수성 토양 개량제가 도입되고 있습니다. 캐나다의 공공 의료 제도는 비용 효율적인 첨단 드레싱을 요구하고 있으며 가치 증명 제품의 조달 기회를 창출하고 있습니다. 멕시코는 니어 쇼어 제조 거점으로 비용 우위를 미국 수요와 연결하면서 지역 소비를 촉진하고 있습니다.

유럽에서는 지속가능성이 강조되어 생분해성 하이드로겔의 조기 도입과 매립처분방법의 엄격한 감시가 진행되고 있습니다. 독일의 프라운호퍼 연구소에서는 4D 프린트에 의한 임플란트 프로토타입이 가속되고, 정부는 바이오 베이스 폴리머 프로젝트에 연구 보조금을 투입하고 있습니다. 영국은 브렉짓 후 규제 재편을 진행하면서 CE 규격과의 무결성을 유지함과 동시에 의료기술 분야의 스케일업 기업을 위한 인센티브를 정비하고 있습니다. 북유럽 국가들은 순환형 경제소재를 우선하여 셀룰로오스계 하이드로겔의 연구개발을 촉진하고 있습니다. 프랑스와 이탈리아는 고급 화장품 유통망을 활용하여 프리미엄 하이드로겔 시트 마스크와 피부 컨디셔닝 세럼을 시장 전개하고 있습니다.

Hydrogel market size in 2026 is estimated at USD 26.54 billion, growing from 2025 value of USD 24.80 billion with 2031 projections showing USD 37.29 billion, growing at 7.02% CAGR over 2026-2031.

The expansion reflects rapid material innovation, a widening application spectrum across health care, agriculture and personal care, and the alignment of bio-based chemistries with tightening sustainability requirements. Extended-wear silicone-hydrogel contact lenses, 4D-printed implants and soil-conditioning superabsorbent polymers anchor much of the incremental demand by offering measurable clinical or resource-efficiency gains. Asia-Pacific maintains outsized volume growth, yet North America and Europe retain premium price realization through regulatory expertise and fast innovation cycles. Feedstock price volatility and landfill rules on non-biodegradable superabsorbent polymers temper margins but simultaneously accelerate the shift to renewable monomers and degradable networks. Overall, the hydrogel market enjoys balanced momentum as cost-driven commodity volumes underpin cash flow while high-value medical devices and smart agriculture lift average selling prices.

Clinical evidence shows that hydrogel dressings accelerate epithelialization and reduce dressing-change frequency versus gauze or foam, prompting broader protocol inclusion by hospital networks. FDA clearance of collagen-based DermiSphere hDRT in January 2025 validated extracellular-matrix-mimicking scaffolds as regenerative platforms rather than passive coverings. Health systems that employ bundled-payment models recognize lower total cost of care despite premium unit pricing. ISO 13485 alignment and CE marking streamline multinational launches and protect innovators against low-spec imitators. As payors focus on outcomes, suppliers that document faster healing and lower infection rates retain pricing power.

Modern baby diapers and feminine hygiene pads integrate hydrogel particles capable of absorbing 500-1000 times their weight, enabling thinner products without leakage. Large-scale producers in China and Japan capitalize on well-established polyacrylate networks, while new entrants target plant-based acrylic acid routes to meet microplastics regulations in Europe and Asia. Consumer demand for comfort drives engineering around particle size and gel strength, forcing continuous R&D investment. Urbanization in India, Indonesia and Nigeria sustains double-digit unit volumes, ensuring that hygiene remains the single largest outlet for hydrogel market volume.

Crude-oil fluctuations drive acrylic-acid swings of up to 40% annually, eroding margins for producers not backward-integrated into propylene EIA. Silicone monomer markets mirror polysiloxane capacity additions in China, injecting further cost uncertainty. Hedging, multi-sourcing and index-linked customer contracts partially alleviate risk, but specialty formulators with low volumes face purchasing disadvantages. Bio-based routes promise pricing stability but require high capital intensity and scale-up timelines.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Semi-crystalline grades represented 45.35% of hydrogel market share in 2025 because their ordered domains deliver tensile strength essential for load-bearing wound dressings and soil conditioners. Predictable swelling kinetics support controlled drug-release matrices, and the lower creep deformation rate reduces product failure risk in extended-wear applications. Manufacturers capitalize on established supply chains anchored in East Asia, ensuring scale advantages and competitive pricing. Research laboratories nevertheless refine crystalline-amorphous ratios to balance mechanical integrity with diffusion rates, enabling next-generation scaffolds for musculoskeletal regeneration.

Amorphous hydrogels are forecast to post an 7.96% CAGR, propelled by injectable therapeutics and 3D-bioprinted tissues requiring rapid solvent exchange and cellular infiltration. Their random coil networks facilitate shear-thinning behavior, allowing minimally invasive delivery that conforms to complex anatomical sites. Biopharma firms integrate thermo-responsive copolymers that gel at body temperature, improving site retention without surgical fixation. Although susceptibility to rapid degradation can limit load-bearing applications, cross-link modulation and composite reinforcement with nanocellulose broaden use cases across reconstruction, ophthalmology and drug depots.

The Hydrogel Market Report is Segmented by Structure (Semi-Crystalline, Amorphous, and Crystalline), Material (Polyacrylate, Polyacrylamide, and Other Materials), End-User Industry (Personal Care and Hygiene, Pharmaceuticals and Healthcare, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific contributed 41.00% of global hydrogel market revenue in 2025 and is projected to expand at an 7.98% CAGR through 2031, outpacing the global average. China's dominance rests on integrated acrylic-acid capacity and a policy agenda that subsidizes superabsorbent soil conditioners in drought-prone provinces. Japan leads innovation in silicone-hydrogel contact lenses through firms such as HOYA Corporation, which leverage high-precision polymerization and global distribution networks. South Korea combines regulatory agility with electronics manufacturing know-how, positioning local players to supply hydrogel components for flexible bioelectronics.

North America secures high value density across medical and agricultural applications, benefiting from FDA clarity, venture funding and advanced manufacturing infrastructure. Hospitals in the United States increasingly adopt hydrogel dressings for chronic wounds tied to diabetes prevalence, while western states deploy superabsorbent soil amendments to offset severe water scarcity. Canada's public health system seeks cost-effective advanced dressings, creating procurement opportunities for value-demonstrated products. Mexico serves as a near-shore manufacturing hub, aligning cost advantages with United States demand while spurring regional consumption.

Europe foregrounds sustainability, driving early adoption of biodegradable hydrogels and rigorous scrutiny of landfill disposal practices. Germany's Fraunhofer institutes accelerate 4D-printed implant prototyping, and the government channels research grants toward bio-based polymer projects. The United Kingdom, navigating post-Brexit regulatory realignment, aims to preserve alignment with CE standards while tailoring incentives for med-tech scale-ups. Nordic countries prioritize circular-economy materials, fostering cellulose-based hydrogel R&D. France and Italy exploit luxury cosmetics channels to market premium hydrogel sheet masks and skin-conditioning serums.