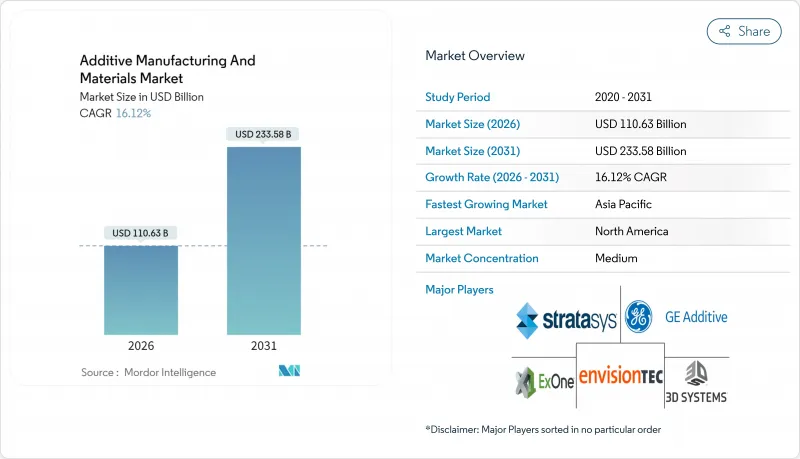

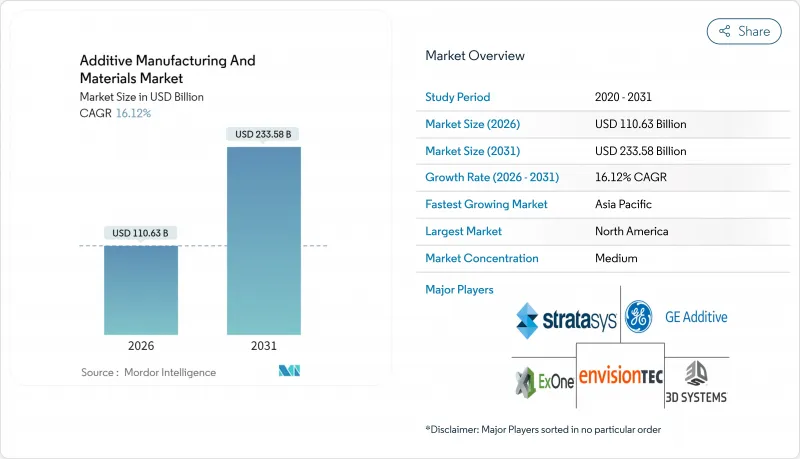

적층 제조 및 재료 시장은 2025년 952억 7,000만 달러로 평가되었고, 2026년에 1,106억 3,000만 달러로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 16.12%의 성장이 예상되며, 2031년까지 2,335억 8,000만 달러에 달할 것으로 예측되고 있습니다.

재료 가격 하락, 항공우주 분야의 경량 부품 수요 증가, 의료 분야의 신속한 도입으로 적층 제조 및 재료 시장은 시제품 제작에서 양산으로 전환되고 있습니다. NIST와 ASTM의 표준화 프로그램은 인증 비용을 낮추는 통합된 자격 인증 경로를 제공하며, 북미, 유럽, 아시아태평양 지역의 정부 인센티브는 공장 수준의 도입을 가속화합니다. 공급업체들이 소프트웨어, 프린터, 인증된 분말을 통합하여 산업용 가동 시간 요구사항을 충족하는 턴키 생산 라인을 제공함에 따라 경쟁 강도가 높아지고 있습니다. 동시에 순환경제 정책은 생산자들이 재활용 폴리머 및 금속 원료의 인증을 추진하도록 유도하여, 폐기물 처리 역량이 구축된 지역에 비용 및 지속가능성 측면의 이점을 창출합니다. 우주 기관들은 궤도상 금속 프린팅을 검증함으로써, 고비용 발사 질량을 제거하는 현장 소량 생산의 장기적 개척지를 열어둡니다.

항공우주 OEM 업체들은 다중 부품 조립체를 단일 프린팅 기하학 구조로 압축해 항공기 중량과 유지보수를 줄입니다. GE Aviation의 프린팅 연료 노즐은 20개 부품을 대체하며 항공사에 항공기당 수명 주기 운영 비용 160만 달러를 절감합니다. 보잉은 787에 티타늄 격자형 브래킷을 통합해 부품 비용을 200-300만 달러 절감하면서도 구조 기준을 충족합니다. 자동차 업체들은 배터리 하우징과 브레이크 시스템에서 이러한 통합을 재현하여 전기차 주행 거리를 연장합니다. 토폴로지 최적화 소프트웨어는 가공으로는 달성할 수 없는 유기적 형상을 구현하여 초기 도입 기업에 성능 우위를 제공합니다. ASTM F2792 정의는 용어와 시험을 표준화하여 인증 기관이 비행에 중요한 부품을 더 빠르게 승인할 수 있도록 돕습니다.

분말 용융법은 개인의 해부학적 구조에 맞춘 다공성 티타늄 임플란트를 가능케 하여 골유착을 개선하고 실패율을 낮춥니다. 스트라이커는 200만 개 이상의 해당 장치를 생산하며 병원 등급 적층 제조 워크플로의 확장성을 입증했습니다. 미국 FDA의 현장진료 지침으로 인증 병원은 수술 가이드를 현장에서 직접 출력할 수 있어 리드 타임과 재고 비용을 절감합니다. 분산 생산은 가치를 중앙 집중식 공장에서 임상 현장으로 전환하여 물류 발자국을 축소합니다. 프리미엄 수요로 인해 항공우주 산업의 할당량이 부족한 상황에서도 코발트-크롬 및 티타늄 분말 공급업체들은 분무화 설비 확장에 나서고 있습니다.

PEEK, PEKK 및 항공우주 등급 티타늄 분말은 소규모 작업장이 감당하기 어려운 프리미엄 가격에 거래됩니다. 원자화기 용량 제한과 에너지 집약적 플라즈마 공정은 구매자들이 대량 구매 가격을 요구하는 와중에 원자재 비용을 상승시킵니다. 공급업체들은 할인 요청하는 고객과 R&D 지출을 요구하는 투자자 사이에서 압박을 받아 차세대 소재 출시가 지연되고 있습니다. 따라서 자동차 및 소비자 부문은 비용 곡선이 하락할 때까지 구매를 프로토타입이나 고마진 부품으로 제한합니다.

지향성 에너지 적층(Directed Energy Deposition)은 항공우주 엔진 수리 분야에서 미터급 부품이 분말 적층 방식의 생산량을 능가함에 따라 16.98%의 연평균 복합 성장률(CAGR)을 기록합니다. 이 부문은 분말 대비 30-50% 저렴한 와이어 원자재를 활용하며, 타 시스템에서 미사용된 재료를 회수하는 이점이 있습니다. 그러나 융착 적층 모델링(FDM)은 교육, 설계, 저응력 산업용 고정 장치 분야에서 보편적으로 사용되어 39.68%의 적층 제조 및 소재 시장 점유율을 유지합니다. 하이브리드 CNC-적층 플랫폼은 레이저 클래딩과 5축 밀링을 결합하여 단일 설비로 공차 및 표면 거칠기 목표를 충족시킵니다.

분말 용융법은 80µm 미만의 레이어 높이가 필요한 격자 구조가 풍부한 임플란트 및 로켓 터보펌프 부품의 기준 기술로 남아 있습니다. 바인더 제팅은 강철 펌프 하우징 및 모래 주조 금형용으로 진화하며, 소결 병목 현상이 해결될 경우 처리량 이점을 제공합니다. 신흥 마이크로웨이브 체적 시스템은 속도에서 한 차원 높은 향상을 약속하며, 제작 시간이 더 이상 단위 경제성을 좌우하지 않는 미래를 예고합니다.

북미는 국방 예산, NASA 심우주 탐사 계획, 성숙한 공급망 생태계의 지원으로 2025년 적층 제조 및 소재 시장 규모에서 36.45%를 차지할 전망입니다. 연방 세제 혜택과 섹션 174 연구개발 비용 처리 규정은 신규 생산 라인에 대한 자본 투자를 장려합니다. 3D 프린팅 임플란트에 대한 FDA 510(k) 지침은 기기 OEM의 시장 출시 기간을 단축시켜 국내 분말 소비를 강화합니다.

아시아태평양은 16.55%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있으며, 중국이 국내 프린터 제조업체에 자금을 제공하여 수입 엔진 부품에 대한 의존도 저감을 도모하고 있는 것이 배경에 있습니다. 싱가포르의 국립 적층 조형 클러스터는 항공우주용 합금의 인증과 기술자의 육성을 실시해, 이 나라를 지역의 수출 거점으로 변모시키고 있습니다. 인도의 생산 연동형 인센티브 프로그램은 자동차 및 에너지 분야를 위한 금속 프린터 구매를 지원하고 있으며, 호주 공동 연구센터는 현지 광석에서 티타늄 분말의 미세화를 진행하고 있습니다.

유럽은 지속가능성에 주력합니다. EU의 ‘Fit-for-55’ 패키지는 OEM이 차량 배출량을 줄이는 경량 브래킷을 프린팅하도록 촉진합니다. 유럽우주국(ESA)은 국제우주정거장(ISS)에서 제작된 최초의 스테인리스강 부품을 시연하며 달 인프라용 미세중력 프린팅의 타당성을 입증했습니다. 독일 자동차 제조사들은 열균열 결함 없이 완벽하게 용접되는 알루미늄-실리콘 합금을 공동 개발해 충돌 관련 응용 분야의 기준을 제시했습니다.

The additive manufacturing and materials market is expected to grow from USD 95.27 billion in 2025 to USD 110.63 billion in 2026 and is forecast to reach USD 233.58 billion by 2031 at 16.12% CAGR over 2026-2031.

Falling material prices, aerospace demand for lightweight parts, and rapid healthcare adoption shift the additive manufacturing and materials market away from prototyping and into volume production. Standardization programs at NIST and ASTM provide unified qualification pathways that lower certification costs, while government incentives in North America, Europe, and Asia Pacific accelerate factory-level deployment.Competitive intensity rises as vendors integrate software, printers, and qualified powders to deliver turnkey production lines that meet industrial uptime requirements. Simultaneously, circular-economy policies motivate producers to qualify recycled polymer and metal feedstocks, creating cost and sustainability advantages for regions with established waste-processing capacity. Space agencies validate in-orbit metal printing, opening a long-term frontier for on-site micro-production that removes costly launch mass.

Aerospace OEMs condense multi-part assemblies into single printed geometries to trim aircraft weight and maintenance. GE Aviation's printed fuel nozzle replaces twenty components and saves carriers USD 1.6 million in lifetime operating costs per aircraft.Boeing integrates titanium lattice brackets on the 787 that cut part cost by USD 2-3 million while meeting structural standards. Automotive firms replicate this consolidation in battery housings and brake systems to extend electric-vehicle range. Topology-optimization software unlocks organic shapes unattainable with machining, giving early adopters a performance edge. ASTM F2792 definitions standardize terminology and testing, helping certifiers approve flight-critical parts faster.

Powder-bed fusion enables porous titanium implants that match individual anatomy, improving osseointegration and cutting failure rates. Stryker has produced over 2 million such devices, proving the scalability of hospital-grade additive workflows.The U.S. FDA's point-of-care guidance lets certified hospitals print surgical guides onsite, reducing lead times and inventory costs. Distributed production shifts value from centralized factories to clinical settings, shrinking logistics footprints. Premium demand pushes cobalt-chrome and titanium powder suppliers to scale atomization capacity despite tight aerospace allocation.

PEEK, PEKK, and aerospace-grade titanium powders trade at premiums that smaller job shops struggle to absorb. Limited atomizer capacity and energy-intensive plasma processes elevate raw-material costs just as buyers push for volume pricing. Suppliers face a squeeze between customers requesting discounts and investors demanding R&D spending, delaying next-generation material rollouts. Automotive and consumer sectors therefore confine purchases to prototypes or high-margin components until cost curves fall.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Directed Energy Deposition posts a 16.98% CAGR, underpinned by aerospace engine repair where meter-scale parts eclipse powder-bed build volumes. This segment benefits from wire feedstock that costs 30-50% less than powder and recoups material unused in other systems. Fused Deposition Modeling, however, retains 39.68% additive manufacturing and materials market share due to its ubiquity in education, design, and low-stress industrial fixtures. Hybrid CNC-additive platforms merge laser cladding with five-axis milling to meet tolerance and surface roughness targets in a single setup.

Powder Bed Fusion remains the benchmark for lattice-rich implants and rocket turbopump components requiring sub-80 µm layer heights. Binder Jetting evolves for steel pump housings and sand casting molds, offering throughput advantages when sintering bottlenecks are solved. Emerging microwave volumetric systems promise order-of-magnitude speed gains, foreshadowing a future where build time no longer dictates unit economics.

The Additive Manufacturing and Materials Market Report is Segmented by Technology (Polymer-Based, Metal-Based, Ceramic-Based, and More), Material Type (Polymers, Metals, Ceramics, Composite, and More), End User (Aerospace and Defense, Automotive, Healthcare, Industrial Machinery, Consumer Products, Construction, Education and Research, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America commands 36.45% additive manufacturing and materials market size in 2025, supported by defense budgets, NASA deep-space initiatives, and a mature supplier ecosystem. Federal tax incentives and Section 174 R&D expensing rules reward capital investment in new production lines. FDA 510(k) guidance for 3D-printed implants accelerates time-to-market for device OEMs, reinforcing domestic powder consumption.

Asia Pacific is the fastest-growing region at a 16.55% CAGR as China funds domestic printer champions to lessen dependence on imported engine parts. Singapore's National Additive Manufacturing cluster certifies aerospace alloys and trains technicians, turning the island into a regional export hub.India's Production-Linked Incentive program subsidizes metal-printer purchases for automotive and energy verticals, while Australia's Cooperative Research Centre advances titanium powder atomization from local ore.

Europe focuses on sustainability; the EU's Fit-for-55 package spurs OEMs to print lightweight brackets that reduce vehicle emissions. The European Space Agency demonstrates the first stainless-steel part fabricated aboard the ISS, validating micro-gravity printing for lunar infrastructure. German carmakers co-develop aluminum-silicon alloys that weld seamlessly without hot-crack defects, setting a benchmark for crash-relevant applications.