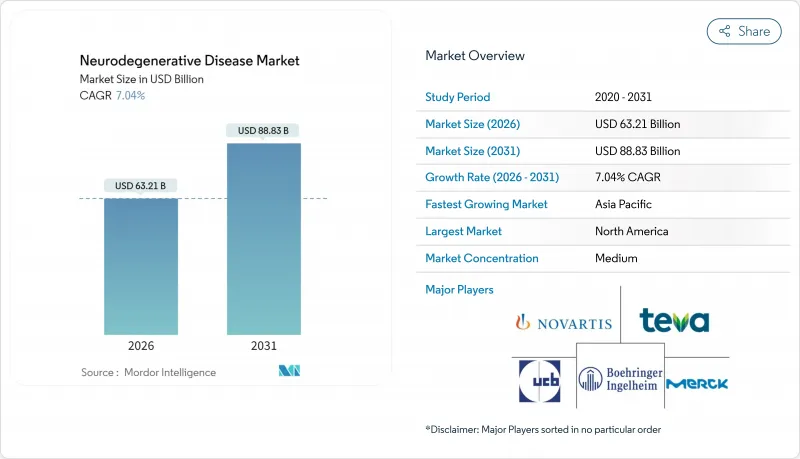

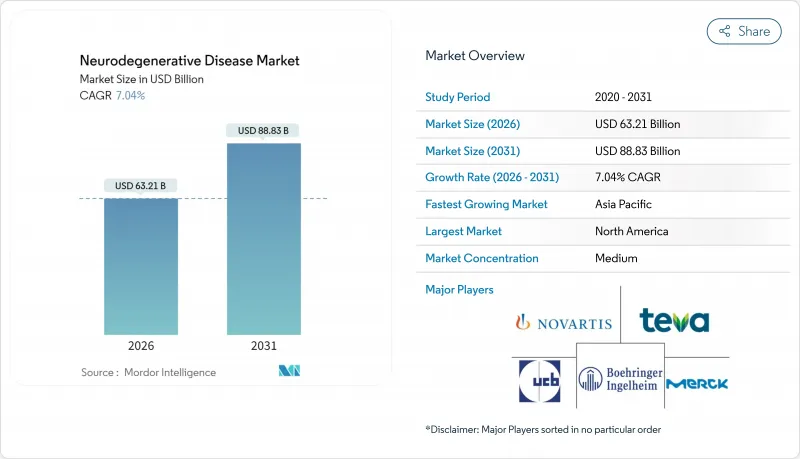

신경 퇴행성 질환 시장은 2025년 590억 6,000만 달러로 평가되었고, 예측 기간(2026-2031년) 동안 CAGR 7.04%로 성장할 전망이며, 2026년 632억 1,000만 달러에서 2031년에는 888억 3,000만 달러에 달할 것으로 추정됩니다.

견고한 수요는 세계 노령화, 질병 개질 생물학적 제제의 신규 승인, 조기 개입을 가능하게 하는 정밀한 진단 도구에 의해 지원됩니다. 기존 기업이 블록버스터 제품군을 지키는 한편, 바이오테크놀러지의 신흥기업이 유전자 치료나 RNA 치료를 후기 임상시험 단계로 추진하는 가운데 경쟁압력은 격화하고 있습니다. 미국에서는 프리미엄 가격에 대한 지불자의 의욕은 여전히 건재하지만, 대증 치료제에 있어서의 제네릭 의약품의 병행 유통에 의한 침식이 수익 구성을 변화시키고 있습니다. 이러한 요인들과 함께 신경 퇴행성 질환 시장은 단기적인 안정성 및 장기적인 혁신의 균형을 유지하면서 지속적인 성장 궤도를 타고 있습니다.

평균 수명이 연장되면 이환 곡선이 상승하는 경향이 있으며, 65세 이후에는 약 5년마다 알츠하이머병의 발병률이 두 배가 됩니다. 이 때문에 미국, 캐나다, 서유럽 국가, 일본, 한국에서는 시설 입소 시기 지연과 장기 케어 비용 절감을 약속하는 질병 수식 요법으로의 전환이 진행되고 있습니다. 정책 입안자는 치매 대책을 국가 의제에 통합하여 바이오 마커 검사의 보험 적용 촉진 및 조기 진단의 인센티브 강화를 추진하고 있습니다. 이에 대해 제약기업은 경도인지 장애(MCI) 환자층을 대상으로 한 임상시험 설계를 조정하여 대상 환자층을 확대하고 있습니다. 병행하여, 간병인 지원 단체에 의한 활동이 임상 도입을 가속시키고 있어, 특히 장기 간병 보험 제도가 정비된 시장에서 현저합니다. 이러한 요소들이 결합되어 단가압력이 높아지는 가운데 신경 퇴행성 질환 시장에서 지속적인 수량 성장을 지원하고 있습니다.

2024년에 승인된 도나네맙과 피하 투여형 레카네맙은 상업적 스토리를 증상 완화에서 질병 변형으로 전환시켰습니다. 이 출시는 아밀로이드 플라크의 제거와 인지 기능 안정화의 증거가 나타나면, 고액의 생물학적 제제에 대해서도 지불자가 상환을 실시하는 것을 증명했습니다. 현재, 15종 이상의 추가적인 항아밀로이드 항체 또는 항타우 항체가 3상 파이프라인에 존재하여 치료법의 경쟁 격화를 보여주고 있습니다. 바이오젠, 로슈, 존슨 엔드 존슨은 적응형 테스트 디자인과 유동적인 바이오마커 대체 엔드포인트를 채택하여 개발 기간을 단축하고 있습니다. 투자자의 신뢰감은 높아지고 있으며, 거시경제의 불확실성에도 불구하고 신경과학 분야의 IPO에 의한 자금조달액은 증가하고 있습니다. 중기적으로는 항체와 저분자 항염증제를 병용한 병용요법이 임상적 베네핏 창문을 넓혀 신경 퇴행성 질환 시장 전체의 수익 기회를 더욱 확대할 것으로 예측됩니다.

아리셉트의 독점권 상실(2026년)은 브랜드 상품 매출액 28억 달러가 소실되어 제네릭 도네페질 경쟁품 전체에서 가격 압축을 일으킵니다. 같은 매출 감소는 2029년까지 남자릭에도, 항체 요법이나 유전자 치료의 고가격 제품 발매와 시기가 겹칩니다. 포트폴리오 관리자는 라이프사이클 연장책(고정용량 배합제, 신규 전달 시스템, OTC 전환)을 다층적으로 강구하여 헤지하지만, 이익률의 희박화는 불가피합니다. 지적재산권 집행이 늦어진 신흥 시장에서는 가격 하락이 더욱 급격해지고 다국적 기업의 수익 회복 전략에 과제를 가져다 줍니다. 이 제약은 단기적인 매출 성장을 억제하는 한편, 기업에 고부가가치 혁신의 가속을 촉진하고 간접적으로 신경 퇴행성 질환 시장 전체를 지원하고 있습니다.

2025년 알츠하이머병은 높은 유병률 및 여러 적응증을 가진 치료제에 지지되어 신경 퇴행성 질환 시장에서 41.72%의 점유율을 차지했습니다. 레켄비의 2025년 매출액이 231억엔(1억 5,400만 달러)을 돌파한 것은 질환 수식 항체 치료제의 상업적 성장 여지를 재확인한 결과가 되었습니다. 파킨슨병과 다발성 경화증은 확립된 도파민 작용제 및 면역조절 요법에 의해 판매량을 유지하고 있지만, 점진적인 혁신의 진전은 여전히 완만합니다. 근위축성 측삭 경화증(ALS)은 규모가 작은 것, 유전자 침묵 후보약이나 신생아 스크리닝 프로그램의 확대에 의해 CAGR 9.36%로 성장을 지속하고, 있습니다. 헌팅턴 병은 프리도피딘의 유럽 승인에 의해 혜택을 받았고, 처음으로 구체적인 질병 개질 치료 옵션이 추가되었습니다. 예측 기간 동안, 알츠하이머병은 여전히 신경 퇴행성 질환 시장의 기간을 이루고 있지만, 희귀질환 영역으로부터의 수익 다변화는 집중 위험을 완화시킵니다.

규제 당국이 신경 퇴행성 성분을 수반하는 리소좀 축적증에 대한 신속한 승인 대상을 확대함으로써 두 번째 성장층이 부상하고 있습니다. 데날리사의 티비데노프스푸알파가 획기적 치료제로 승인된 사례가 이 동향을 나타내고 있으며, 지금까지 경시되어 온 희귀질환 영역에 자본이 유입되고 있습니다. 이러한 변화가 결합되어 치료 영역이 확대되고 신경 퇴행성 질환 시장 전체의 규모 상한이 인상되는 동시에, 바이오마커 표준화에 있어서의 부문 횡단적인 시너지 효과가 탄생하고 있습니다.

2025년 시점에서 콜린에스테라아제 억제제는 신경 퇴행성 질환 시장 규모의 27.98%를 차지하며, 확립된 제1선택 치료로서의 지위를 반영하고 있습니다. 그러나 벡터 설계 및 제조 규모의 향상에 따라 유전자 치료 및 세포 치료의 파이프라인 개발 속도가 우위가 되어 연간 9.21%의 성장이 예상됩니다. 솔리드 바이오사이언시스의 SGT-212가 프리드라이히 실조증의 승인을 얻은 것은 신경 및 심장 표현형에 대한 전신 AAV 전달을 시연하고 인접한 실조증 형태로의 길을 열었습니다. 한편, 단일클론항체는 아밀로이드를 넘어 α-시누클레인이나 TDP-43을 표적으로 하고, 투여량 최적화의 지견에 지지되고 있습니다. NMDA 수용체 길항제와 도파민 작용제는 주력 제품이며, 후발 의약품의 영향에 직면하고 있습니다. 스폰서 회사는 지속성 주사제와 디지털 복약 관리 도구를 통해 공유를 보호합니다. RNA 치료제는 생물학적 제형보다 생산 원가가 낮고 저분자 화합물보다 특이성이 높다는 전략적 중간 영역을 차지하며 신경 퇴행성 질환 시장에서 약물 등급의 리더십을 더욱 세분화합니다.

임상 데이터의 투명성 향상은 클래스 전환의 동향을 촉진하고, 실세계 데이터가 항체 및 조절제에 대한 반응의 이질성을 부각시키고 있습니다. 의사는 증상 완화 및 질병 변형을 결합한 다기전 전략을 채택하는 경향이 강해지고 있으며, 클래스 점유율이 변동하더라도 처방 총량은 확대됩니다. 그 결과 경쟁이 치열해지지만, 신경 퇴행성 질환 시장 전체의 규모는 계속 확대되고 있습니다.

북미는 2025년 전 세계 수익의 41.96%를 차지했습니다. FDA의 신속 승인 과정과 메디케어 상환 제도가 신규 생물학적 제제의 신속한 보급을 뒷받침하고 있기 때문입니다. 2025년 1월에 포스디네마브 및 티비데노프 스푸알파에 부여된 획기적인 지정은 규제 당국의 민첩한 대응을 상징합니다. 벤처 캐피탈은 보스턴 및 샌프란시스코의 거점에 집중하고, 로슈의 500억 달러 규모의 미국 확장 계획은 국내 바이오 의약품 생산 능력을 확보하고 있습니다. 캐나다는 조기 액세스 프로그램을 확충하고, 멕시코는 니어 쇼어링을 활용해 포장 업무를 유치했습니다. 이로 인해 북미 전역에 연속적인 공급 생태계가 형성되어 신경 퇴행성 질환 시장을 뒷받침하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 8.31%라는 가장 빠른 성장이 예상됩니다. 일본의 레켄비 신속 도입은 예산 감시하에서도 고가의 항체 의약의 상환을 인정하는 지역적인 선례가 되었습니다. 중국은 우선심사 채널에 의한 신약 승인 신청(NDA) 심사를 가속했습니다. 국내 기업이 바이오시밀러와 RNA 요법을 공동 개발하여 진입 가격을 인하했습니다. 한국은 AI 지원 스크리닝 툴에 자금을 투입했고, 호주는 유전체 검사를 공적 의료 급여에 통합했습니다. 인프라 확충 및 정책 조화가 결합되어 신경 퇴행성 질환 시장에서 환자 접근 확대 및 수익원의 다양화를 촉진했습니다.

유럽에서는 리스크와 액세스를 양립시키는 EMA(유럽 의약품청)의 중앙 심사 절차를 기반으로 꾸준한 성장을 계속하고 있습니다. 동청의 프리도피딘 승인 취소 결정은 사후 분석에 근거한 재평가에 대한 유연한 자세를 보여줍니다. 독일, 프랑스, 영국은 여전히 높은 가격 시장이지만 지출 억제를 위해 성과 연동형 리베이트를 협상하고 있습니다. 남유럽에서는 EU 결속 기금에 의한 공동 출자로 지역치매계획의 전개가 확대되어 조기진단 및 질병 진행 억제를 지원하고 있습니다. 각국 HTA 평가의 차이에 의해 출시 순서는 분단되는 반면, EU4 컨소시엄을 통한 공동 구입에 의해 가격 격차가 완화되어 신경 퇴행성 질환 시장 규모에의 대륙 규모의 공헌이 지속되고 있습니다.

The neurodegenerative disease market was valued at USD 59.06 billion in 2025 and estimated to grow from USD 63.21 billion in 2026 to reach USD 88.83 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031).

Robust demand is fuelled by an aging global population, fresh approvals for disease-modifying biologics, and sharper diagnostic tools that enable earlier intervention. Competitive pressure intensifies as incumbents defend blockbuster franchises while biotechnology newcomers push gene and RNA therapies toward late-stage trials. Payer appetite for premium pricing remains intact in the United States, yet parallel generic erosion in symptomatic drugs reshapes revenue mixes. Taken together, these forces put the neurodegenerative disease market on a durable growth path that balances near-term stability with long-term innovation.

Rising longevity pushes prevalence curves higher, doubling Alzheimer's incidence roughly every five years past age 65. Health systems in the United States, Canada, Western Europe, Japan, and South Korea, therefore, pivot toward disease-modifying regimens that promise delayed institutionalization and lower long-run care costs. Policy makers incorporate dementia plans into national agendas, spurring reimbursement for biomarker screening and incentivizing early diagnosis. Pharmaceutical firms respond by aligning trial designs with mild-cognitive-impairment cohorts, expanding addressable patient pools. In parallel, caregiver advocacy accelerates clinical uptake, particularly in markets with robust long-term-care insurance. Collectively, these elements underpin sustained volume growth for the Neurodegenerative disease market even as unit pricing pressures rise.

The 2024 approvals of donanemab and subcutaneous lecanemab shifted commercial narratives from symptom relief to disease alteration. Their launch proved payers will reimburse high-cost biologics when evidence shows amyloid plaque clearance and cognitive stabilization. More than 15 additional anti-amyloid or anti-tau antibodies now populate Phase III pipelines, signaling a therapeutic arms race. Biogen, Roche, and Johnson & Johnson deploy adaptive trial designs and fluid biomarker surrogate endpoints to shorten development timelines. Investor confidence surges, with neuroscience IPO proceeds rising despite macro uncertainty. Over the medium term, combination regimens pairing antibodies with small-molecule anti-inflammatories are expected to widen clinical benefit windows, further enlarging revenue opportunities across the neurodegenerative disease market.

Aricept's loss of exclusivity in 2026 erases USD 2.8 billion in branded revenue, triggering price compression across generic donepezil competitors. Similar erosion hits Namzaric by 2029, overlapping with premium launches of antibodies and gene therapies. Portfolio managers hedge by layering life-cycle extensions-fixed-dose combos, new delivery systems, and OTC switches-but margin dilution remains inevitable. Emerging markets, where intellectual-property enforcement lags, see even steeper price drops, challenging multinational revenue recapture strategies. This constraint suppresses near-term top-line growth yet nudges firms to accelerate higher-value innovation, indirectly sustaining the broader neurodegenerative disease market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Alzheimer's disease commanded 41.72% neurodegenerative disease market share in 2025, buoyed by high prevalence and multiple labeled therapies. The 2025 surge in Leqembi revenue, topping JPY 23.1 billion (USD 154 million), reaffirmed commercial headroom for disease-modifying antibodies. Parkinson's and multiple sclerosis sustain volume through entrenched dopaminergic and immunomodulatory regimens, yet incremental innovation remains slower. ALS, albeit small, posts a 9.36% CAGR, supported by gene-silencing candidates and expanded newborn-screening programs. Huntington's benefits from Pridopidine's European nod, adding a tangible disease-modifying option for the first time. Over the forecast, Alzheimer's still anchors the neurodegenerative disease market, but diversified revenue flow from rare indications mitigates concentration risk.

A second layer of growth emerges as regulators widen accelerated-approval eligibility to lysosomal storage diseases with neurodegenerative components. Denali's tividenofusp alfa breakthrough tag illustrates this trend, channelling capital toward previously neglected orphan indications. Collectively, these shifts broaden the therapeutic canvas, raising the ceiling for total neurodegenerative disease market size and creating cross-segment synergies in biomarker standardization.

Cholinesterase inhibitors generated 27.98% of the neurodegenerative disease market size in 2025, reflecting entrenched first-line use. Yet pipeline velocity now favors gene and cell therapies, which are set to grow 9.21% annually as vector design and manufacturing scale improve. Solid Biosciences' SGT-212 clearance for Friedreich ataxia validates systemic AAV delivery for neuro-cardiac phenotypes, opening paths to adjacent forms of ataxia. Meanwhile, monoclonal antibodies extend beyond amyloid to target alpha-synuclein and TDP-43, supported by learnings in dosing optimization. NMDA antagonists and dopamine agonists remain staples but face generic exposure; sponsors defend share through long-acting injectables and digital adherence tools. RNA therapeutics occupy a strategic middle ground with lower COGS than biologics and higher specificity than small molecules, further fragmenting drug-class leadership within the neurodegenerative disease market.

Clinical data transparency enhances class-switch dynamics, as real-world evidence highlights heterogeneity in response to antibodies versus modulators. Physicians increasingly adopt multi-mechanism strategies, combining symptomatic relief with disease modification, which expands overall prescription volumes even if class shares fluctuate. Consequently, competitive intensity rises, but the aggregate neurodegenerative disease market size continues to climb.

The Neurodegenerative Disease Market Report is Segmented by Indication (Parkinson's Disease, and More), Drug Class (NMDA Receptor Antagonists, and More), Molecule Type (Small-Molecule Drugs, and More), Route of Administration (Oral, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 41.96% of worldwide revenue in 2025 as the FDA's accelerated-approval pathway and Medicare reimbursement powers the quick uptake of novel biologics. Breakthrough tags for posdinemab and tividenofusp alfa in January 2025 exemplify regulatory agility. Venture capital funnels toward Boston and San Francisco hubs, while Roche's USD 50 billion U.S. expansion secures domestic biologics capacity. Canada broadens early-access programs, and Mexico leverages near-shoring to attract packaging operations, creating a contiguous North American supply ecosystem that boosts the neurodegenerative disease market.

Asia-Pacific holds the fastest 8.31% CAGR outlook through 2031. Japan's rapid Leqembi adoption set a regional precedent for reimbursing expensive antibodies despite budget scrutiny. China accelerates NDA reviews under its priority-review channel, with local firms co-developing biosimilars and RNA therapies that lower entry prices. South Korea funds AI-guided screening tools, and Australia integrates genomic testing into public health benefits. Collectively, infrastructure expansion and policy harmonization expand patient access and diversify revenue drivers within the neurodegenerative disease market.

Europe posts steady growth anchored by EMA's centralized procedures that balance risk and access. The agency's Pridopidine reversal signals an openness to re-evaluation based on post-hoc analyses. Germany, France, and the United Kingdom remain premium markets but negotiate outcome-based rebates to contain spending. Southern Europe increases deployment of regional dementia plans co-funded by EU cohesion funds, supporting earlier diagnosis and slowing disease progression. While differing national HTA assessments fragment launch sequencing, collective purchasing through EU4 consortia mitigates pricing gaps and sustains continental contribution to the neurodegenerative disease market size.