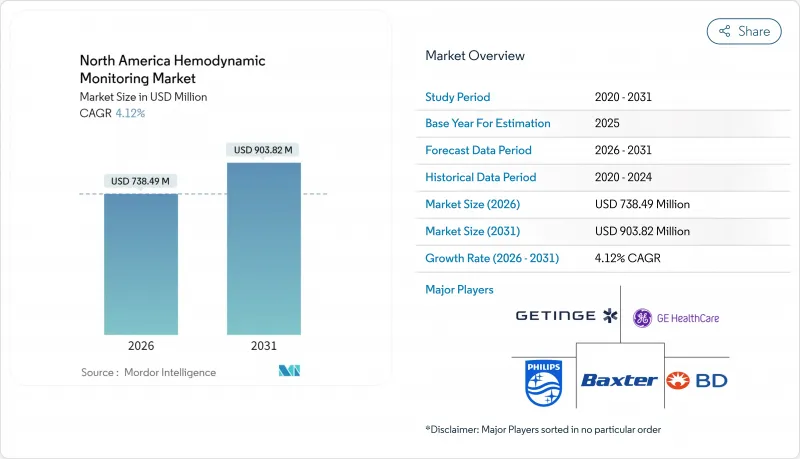

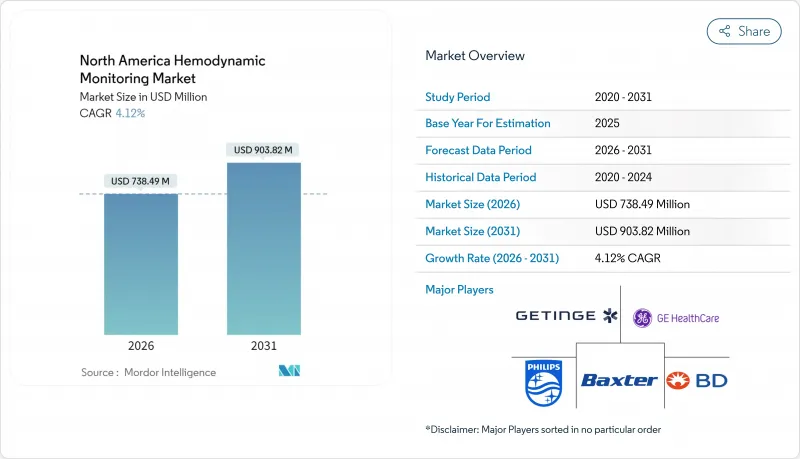

북미의 혈역학 모니터링 시장 규모는 2026년 7억 3,849만 달러로 평가되었습니다.

이는 2025년 7억926만 달러에서 성장한 수치이며, 2031년에는 9억382만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에 걸쳐 CAGR 4.12%로 성장이 전망됩니다.

이 성장 궤적은 병원 통합, 품질 연계 보상 제도, 압력 또는 유량 값을 실행 가능한 예측으로 전환하는 AI 기반 분석 기술의 급속한 도입을 반영합니다. 공급업체 플랫폼은 이제 하드웨어, 소프트웨어, 일회용 소모품 및 클라우드 구독을 묶어 의료 시스템에 예측 가능한 총소유비용(TCO)을 제공합니다. 최소 침습적 또는 웨어러블 센서로 신속히 전환함으로써 감염 위험을 줄이고 중환자실(ICU)을 넘어 사용 범위를 확대하는 한편, 메디케어의 원격 모니터링 코드는 운영 예산이 긴축되는 상황에서도 자본 지출을 유지하는 데 기여합니다.

예측 알고리즘은 혈역학 모니터링을 사후 대응적 측정에서 사전 예방적 치료로 전환시키고 있습니다. 에드워즈 라이프사이언스(Edwards Lifesciences)의 저혈압 예측 지수(HPI)는 수술 중 저혈압을 최대 15분 전에 경고하는 데 83%의 민감도와 특이도를 보여주며, 표준 치료 대비 시간 가중 평균 저혈압 발생률을 85% 감소시킵니다. 초기 임상시험에서는 중환자실 체류 기간 단축 및 신장 지표 개선이 보고되었으나, 명확한 사망률 혜택은 여전히 불분명하여 예측과 폐쇄 루프 약물 조절을 융합한 차세대 플랫폼의 발전 여지가 남아 있습니다. 미국 식품의약국(FDA)은 현재 보조 심혈관 지표를 21 CFR 870.2200에 따라 분류하여 AI 기반 소프트웨어 모듈에 대한 명확한 승인 경로를 제공합니다. 이러한 승인은 채택을 가속화하고 북미 혈역학 모니터링 시장을 기술 갱신 주기로 유지합니다.

고령화 인구는 심부전 유병률을 상승시키고 지속적인 압력 추세 모니터링 수요를 촉진합니다. 1,500명 이상의 환자를 대상으로 한 3건의 무작위 임상시험 메타분석에 따르면, 이식형 혈역학 모니터는 사망률을 25%(위험비 0.75) 감소시키고 심부전 입원률을 36%(위험비 0.64) 낮췄습니다. 비용 효과성 모델링에 따르면 재입원 방지를 통해 원격 혈압 모니터링은 5년간 환자당 6,723달러를 절감합니다. 이러한 근거는 메디케어의 원격 생리학적 모니터링 비용 보상 결정의 토대가 되어 출하량을 촉진하고 북미 혈역학 모니터링 시장을 RPM 핵심 시장으로 공고히 합니다.

지역 병원의 25%를 초과하는 이직률은 지속적인 재교육을 강요하고 정교한 콘솔의 도입을 지연시킵니다. 수요 평가에 따르면 파형 해석 및 장비 설정의 격차가 모니터링 정확도를 저해하는 것으로 나타났습니다. 공급업체들은 색상 코드 대시보드, 상황 인식 경보, 내장형 튜토리얼로 대응하고 있으나, 인력 불균형은 북미 혈역학 모니터링 시장의 연평균 성장률(CAGR)을 약 0.6% 포인트 하락시키는 요인으로 지속되고 있습니다.

혈역학 모니터링 시스템은 2025년 북미 혈역학 모니터링 시장의 56.12%를 차지하며, 구매자들이 중환자실 워크플로우에 맞춰 조정된 엔드투엔드 생태계를 선호함을 보여줍니다. 단위 성장률은 소폭이지만 꾸준한 일회용 제품 수요가 공급업체의 서비스 수익을 유지시키고 있습니다. 병원들의 교체 주기 연장으로 인해 북미 혈역학 모니터링 시스템 시장 규모는 2026년 4억 110만 달러에서 2031년 3억 8,290만 달러로 감소할 전망이지만, AI 소프트웨어 업그레이드 및 사이버 보안 모듈이 마진을 견인할 것입니다.

연평균 4.98% 성장률을 보이는 센서 부문이 혁신의 선봉을 이루고 있습니다. 소형화된 광학 또는 임피던스 센서는 텔레메트리 패치와 직접 통합되어 만성 치료 및 외래 채널을 개방합니다. 수술실에서 22개 매개변수를 표시하는 테루모의 CDI OneView는 고도 중증도와 다중 지표 분석의 융합을 보여줍니다. 움직임이나 낮은 관류 상태에서도 신호 품질을 완벽하게 하는 알고리즘이 개발됨에 따라 센서 제조사들은 북미 혈역학 모니터링 시장 점유율 확대를 준비 중입니다.

심박출량은 의료진의 친숙도와 강력한 절차 코딩 덕분에 39.12% 점유율로 여전히 핵심을 유지합니다. 비침습적 맥파형상 및 생체저항 플랫폼은 카테터 사용 감소분을 상쇄하며 중환자실과 심혈관실 전반의 지출을 유지합니다. 반면 산소포화도 모니터링은 다중 파장 프로브가 조직 산소측정 및 정맥 포화도까지 활용 범위를 확장함에 따라 5.43% CAGR을 기록합니다. 마시모의 레인보우 SET는 2025년 1분기 의료 매출을 3억 7,200만 달러로 끌어올리며 비침습적 진단 확대에 대한 수요를 입증했습니다. 압력 및 용적 지표는 여전히 임상 필수 요소로 남아 있지만, 진정한 차별화는 여러 매개변수를 단일 실행 가능한 수치로 종합하는 복합 점수에 있습니다. 이는 간호사 부족 속에서 인지 부하를 줄여줍니다.

The North America hemodynamic monitoring market size in 2026 is estimated at USD 738.49 million, growing from 2025 value of USD 709.26 million with 2031 projections showing USD 903.82 million, growing at 4.12% CAGR over 2026-2031.

This trajectory reflects hospital consolidation, reimbursement tied to quality, and the rapid integration of AI-enabled analytics that transform pressure or flow values into actionable predictions. Vendor platforms now bundle hardware, software, disposables, and cloud subscriptions, giving health systems a predictable total cost of ownership. A swift pivot toward minimally invasive or wearable sensors reduces infection risk and broadens usage beyond the intensive-care unit, while Medicare's remote-monitoring codes help preserve capital spending even as operating budgets tighten.

Predictive algorithms are turning hemodynamic monitoring from reactive measurement into proactive therapy. Edwards Lifesciences' Hypotension Prediction Index (HPI) shows 83% sensitivity and specificity in flagging intraoperative hypotension up to 15 minutes in advance, cutting time-weighted average hypotension by 85% versus standard care. Early trials report shorter ICU stays and better renal metrics, yet clear mortality benefit remains elusive, leaving space for next-generation platforms that fuse prediction with closed-loop drug titration. The U.S. Food and Drug Administration now classifies adjunctive cardiovascular indicators under 21 CFR 870.2200, providing an explicit path for AI-rich software modules. These clearances accelerate adoption and keep the North America hemodynamic monitoring market on a technology refresh cycle.

An aging population pushes heart-failure prevalence upward and boosts demand for continuous pressure trending. Meta-analysis of three randomized trials with over 1,500 patients found implantable hemodynamic monitors cut mortality by 25% (HR 0.75) and heart-failure hospitalizations by 36% (HR 0.64). Cost-effectiveness modeling shows remote pressure monitoring saves USD 6,723 per patient over five years by avoiding readmissions. Such evidence underpins Medicare's decision to reimburse remote physiologic monitoring, propelling shipments and cementing the North America hemodynamic monitoring market as an RPM cornerstone.

Turnover exceeding 25% at community hospitals forces continuous retraining and slows deployment of sophisticated consoles. Needs assessments show gaps in waveform interpretation and equipment setup that undermine monitoring accuracy. Vendors counter with color-coded dashboards, context-aware alarms, and embedded tutorials, yet staffing imbalances continue to dampen the North America hemodynamic monitoring market CAGR by an estimated 0.6 percentage point.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hemodynamic Monitoring Systems secured 56.12% of the North America hemodynamic monitoring market in 2025, underscoring buyers' preference for end-to-end ecosystems calibrated for ICU workflows. Although unit growth is modest, steady disposable pull-through keeps vendors' service revenue intact. The North America hemodynamic monitoring market size for systems should slip from USD 401.1 million in 2026 to USD 382.9 million by 2031 as hospitals stretch replacement cycles; however, AI software upgrades and cybersecurity modules will buoy margins.

Sensors, rising at a 4.98% CAGR, represent the innovation vanguard. Miniaturized optical or impedance sensors integrate directly with telemetry patches, opening chronic-care and ambulatory channels. Terumo's CDI OneView, which displays 22 parameters in the OR, illustrates convergence of high acuity and multi-metric analytics. As algorithms perfect signal quality under motion or low perfusion, sensor makers are primed to lift their slice of the North America hemodynamic monitoring market share.

Cardiac Output remains the backbone at 39.12% share thanks to clinician familiarity and robust procedural coding. Non-invasive pulse-contour and bioreactance platforms offset declining catheter use, sustaining spending across ICUs and cath labs. Oxygen Saturation Monitoring, however, shows a 5.43% CAGR as multi-wavelength probes extend utility to tissue oximetry and venous saturation. Masimo's rainbow SET drove healthcare revenue to USD 372 million in Q1 2025, validating appetite for broadened non-invasive diagnostics. Pressure and volume indices persist as clinical staples, but the real differentiation lies in composite scores that synthesize multiple parameters into single actionable numbers, reducing cognitive load amid nurse shortages.

The North America Hemodynamic Monitoring Market Report is Segmented by Product Type (Hemodynamic Monitoring Systems, Catheters, Sensors, Disposables & Accessories), Monitoring Type (Cardiac Output, Pressure, Volume, Oxygen Saturation, Others), End User (Hospitals, Cath Labs, Ascs, Home-Care, Others), and Geography (United States, Canada, Mexico). Market Forecasts are Provided in Terms of Value (USD).