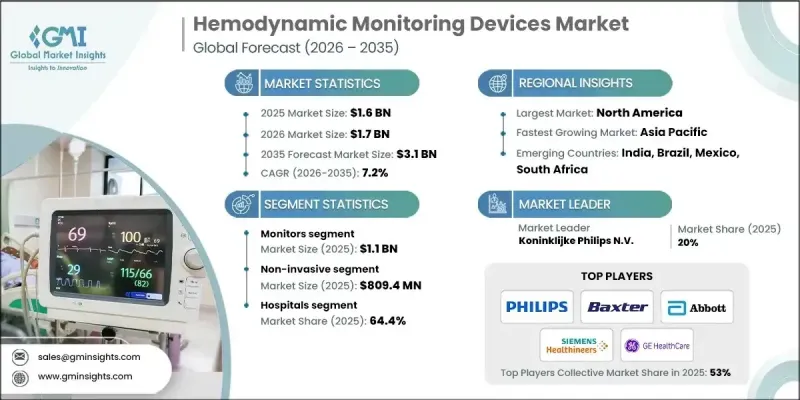

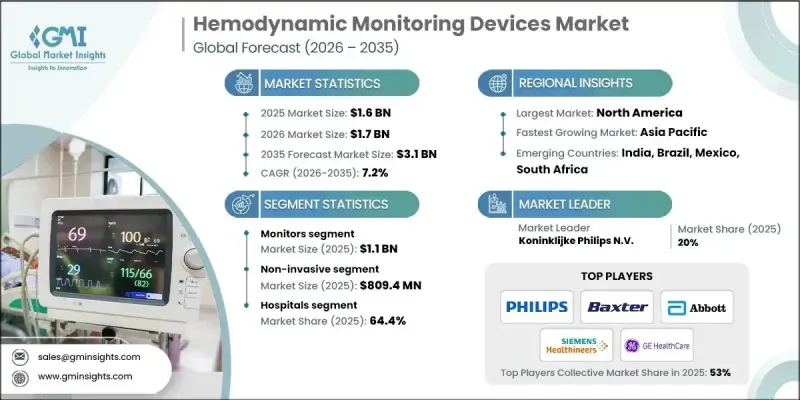

세계의 혈역학 모니터링 기기 시장은 2025년에 16억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.2%로 성장할 전망이며, 31억 달러에 이를 것으로 예측되고 있습니다.

이 성장은 세계의 만성 질환 증가, 모니터링 기술의 지속적인 혁신, 원격 의료 기반 케어 모델의 보급 확대 및 세계 수술 수 증가로 설명됩니다. 혈역학 모니터링 기기는 혈압, 혈류 및 전신 순환 효율을 실시간으로 추적하여 심혈관 기능의 성능을 평가하는 시스템으로 정의됩니다. 이러한 도구는 심박출량, 혈관저항 및 관련 생리학적 지표에 대한 지속적인 발견을 제공함으로써 임상 판단을 지원합니다. 그 역할은 수술실, 집중 치료 환경 및 고도의 의존이 필요한 병원 환경에서 특히 중요합니다. 만성 질환의 확산 확대는 특히 신속한 개입이 필요한 상황에서 정밀한 심혈관 평가 도구 수요를 높이고 있다고 합니다. 이러한 질병과 관련된 합병증은 시기적절하고 정확한 치료 결정을 지원하는 첨단 모니터링 플랫폼의 채택을 의료 제공업체에게 촉구합니다. 인공지능(AI) 및 원격 연결 기능이 모니터링 솔루션에 깊숙히 통합됨에 따라 시장 동향은 더욱 가속화될 것으로 예상되고 있으며, 혈역학 모니터링은 현대 임상 관리 제공의 핵심 요소로서의 지위를 확립하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 당초 시장 규모 | 16억 달러 |

| 시장 규모 예측 | 31억 달러 |

| CAGR | 7.2% |

모니터 분야는 2025년에 11억 달러 시장 규모를 창출했습니다. 이 범주에는 고급 침대측 시스템, 모바일 플랫폼, 심박출량, 동맥압, 중심 정맥압 등 지속적인 심혈관 데이터를 제공하도록 설계된 통합 모니터링 솔루션이 포함됩니다. 이러한 모니터링 시스템은 심각한 임상 환경에서 환자의 안정성을 유지하고 치료 정책을 결정하는 중요한 도구로 간주됩니다. 이용률은 집중 치료실(ICU)에서 가장 높고 중증 또는 불안정한 상태의 환자를 관리하기 위해서는 중단 없는 심혈관 모니터링이 필수적입니다.

비침습성 부문은 2025년에 8억 940만 달러에 이르렀으며, 2035년까지 연평균 복합 성장률(CAGR) 7.3%로 성장할 것으로 예측됩니다. 비침습적 순환 역학 모니터링 솔루션은 피부를 손상시키거나 카테터를 삽입하지 않고 심혈관 매개변수를 평가하는 기술로 자리매김하고 있습니다. 이 시스템은 환자의 안전성 및 운영 효율성에 중점을 두고 고급 생리학적 측정 기법을 사용하여 심박출량 및 주입 반응성을 평가합니다. 의료 시설에서는 수술기 및 집중 치료 워크플로우 전반에 걸쳐 치료 위험을 줄이고, 설치 시간을 단축하며, 비용 효율성을 개선할 수 있기 때문에 비침습적 접근이 점점 더 중요해지고 있습니다.

미국의 혈역학 모니터링 기기 시장은 2025년 5억 2,040만 달러 규모에 달했습니다. 미국은 심혈관 질환의 발생률이 높고 의료 인프라가 정비되어 있기 때문에 시장을 선도하고 있습니다. 국내 병원 및 첨단 의료센터에서는 복잡한 수술, 외상 관리, 고급 심장 인터벤션을 받는 환자를 지원하기 위해 광범위한 모니터링 솔루션에 크게 의존하고 있다고 합니다.

The Global Hemodynamic Monitoring Devices Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 3.1 billion by 2035.

The growth is explained by the rising global burden of long-term medical conditions, continuous innovation in monitoring technologies, wider acceptance of telehealth-based care models, and an increasing volume of surgical procedures worldwide. Hemodynamic monitoring devices are described as systems that assess cardiovascular performance by tracking blood pressure, blood flow, and overall circulatory efficiency in real time. These tools support clinical decision-making by delivering continuous insights into cardiac output, vascular resistance, and related physiological indicators. Their role is emphasized across surgical suites, intensive care environments, and high-dependency hospital settings. The expanding prevalence of chronic illnesses is said to be increasing demand for precise cardiovascular assessment tools, particularly where rapid intervention is required. Complications linked to these conditions are driving healthcare providers to adopt advanced monitoring platforms that support timely and accurate treatment decisions. Market momentum is expected to intensify as artificial intelligence and remote connectivity features become more deeply embedded in monitoring solutions, positioning hemodynamic monitoring as a core element of modern clinical care delivery.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 7.2% |

The monitors segment generated USD 1.1 billion in 2025. This category includes advanced bedside systems, mobile platforms, and integrated monitoring solutions designed to deliver continuous cardiovascular data, including cardiac output, arterial pressure, and central venous pressure. These monitoring systems are regarded as critical tools for maintaining patient stability and guiding therapeutic actions in high-acuity clinical settings. Utilization levels are highest in intensive care units, where uninterrupted cardiovascular monitoring is essential for managing patients with severe or unstable conditions.

The non-invasive segment reached USD 809.4 million in 2025 and is projected to grow at a CAGR of 7.3% throughout 2035. Non-invasive hemodynamic monitoring solutions are positioned as technologies that evaluate cardiovascular parameters without breaching the skin or requiring catheter placement. These systems rely on advanced physiological measurement methods to assess cardiac output and fluid responsiveness with a focus on patient safety and operational efficiency. Healthcare facilities are increasingly favoring non-invasive approaches due to reduced procedural risks, faster setup times, and improved cost efficiency across perioperative and critical care workflows.

U.S. Hemodynamic Monitoring Devices Market captured USD 520.4 million in 2025. The United States is described as leading the market due to a high incidence of cardiovascular disorders and a well-established healthcare infrastructure. Hospitals and advanced care centers across the country are said to rely heavily on a broad range of monitoring solutions to support patients undergoing complex surgical procedures, trauma management, and advanced cardiac interventions.

Key participants active in the Global Hemodynamic Monitoring Devices Market include Siemens Healthineers, Koninklijke Philips N.V., Edwards Lifesciences Corporation, GE HealthCare Technologies, Abbott Laboratories, Masimo Corporation, Mindray, Baxter International, Getinge, Nihon Kohden Corporation, Canon Medical Systems Corporation, Becton, Dickinson and Company, ICU Medical, Deltex Medical Group, and OSYPKA MEDICAL. Companies operating in the Global Hemodynamic Monitoring Devices Market are described as strengthening their market position through a combination of innovation, strategic partnerships, and geographic expansion. Product development efforts are focused on improving accuracy, usability, and data integration to support real-time clinical decision-making. Many players are investing in digital health capabilities, including remote monitoring and intelligent analytics, to align with evolving care models. Strategic collaborations with hospitals and research institutions help companies validate technologies and accelerate adoption.