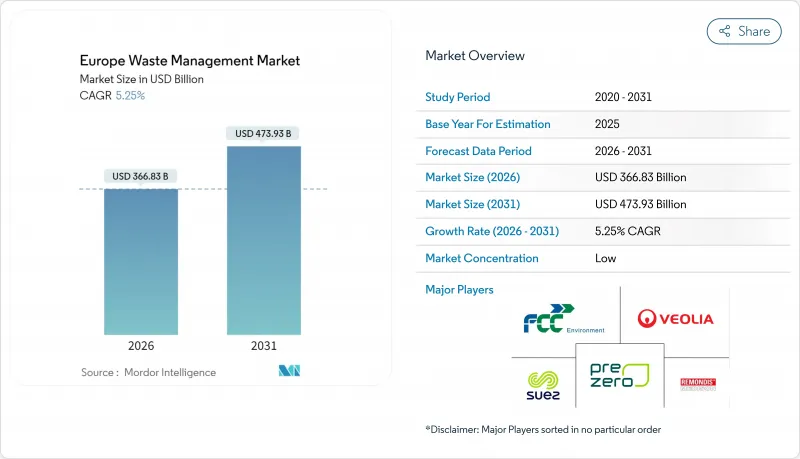

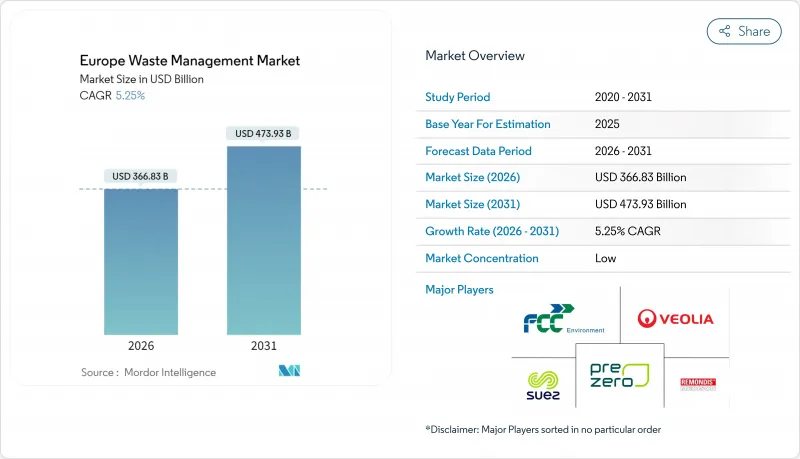

유럽의 폐기물 관리 시장 규모는 2026년에는 3,668억 3,000만 달러로 평가되었습니다. 이는 2025년 3,485억 4,000만 달러에서 성장한 수치이며, 2031년에는 4,739억 3,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에 걸쳐 CAGR 5.25%로 성장할 전망입니다.

이러한 견고한 성장 경로는 유럽의 폐기물 관리 시장이 엄격한 매립지 감축 의무, 폐기물 에너지화(WtE) 자산에 대한 급증하는 투자, 그리고 순환 경제 원칙으로의 뚜렷한 전환으로부터 어떻게 혜택을 받고 있는지 보여줍니다. 규제 압박, 특히 2035년까지 도시 매립을 10%로 제한하라는 유럽연합의 요구는 재활용, 화학 물질 회수 및 AI 기반 수거 시스템으로의 자본 유입을 가속화하는 동시에 첨단 처리 기술에 대한 수요의 급격한 변화를 만들어내고 있습니다. 독일은 성숙한 생산자 책임 확대(EPR) 제도와 견고한 WtE 네트워크를 바탕으로 여전히 핵심 시장으로 자리매김하고 있으나, 대규모 화학 재활용 플랜트와 스마트 쓰레기통 시범 사업이 새로운 역량을 창출하면서 스페인이 현재 가장 주목받는 성장 사례로 부상하고 있습니다. 가치 사슬 전반에 걸쳐 선도 기업들은 완전 통합형 서비스 제공을 위해 상호 보완적 자산을 인수하고 있으며, 데이터 중심 스타트업들은 트럭 주행 거리, 탄소 배출량, 운영 비용을 절감하는 분석 기술을 통해 수익을 창출하고 있습니다.

매립 10% 상한선은 유럽 폐기물 관리 시장 전반의 지자체 예산과 계획 일정을 재편하고 있습니다. 독일은 이미 거의 제로 매립 수준을 운영 중이지만, 스페인과 이탈리아는 2035년 규정 준수를 위해 WtE 라인과 고처리량 MRF(재활용 분류 시설)를 빠르게 추가하고 있습니다. 규정 미준수 시 부과되는 벌금과 EU 자금 지원 제한으로 인해 도입 속도가 느린 업체들조차 잔여 폐기물을 에너지 회수 또는 고급 재활용으로 전환하도록 압박받고 있습니다. SUEZ와 같은 운영사는 툴루즈에 연간 360GWh의 열을 공급하는 폐기물 에너지화(WtE) 지역난방 프로젝트로 대응하며, 규정 준수가 어떻게 새로운 유틸리티 수익을 창출할 수 있는지 보여주고 있습니다. 최저비용 처리 옵션이 사라짐에 따라 모든 이해관계자는 이제 순환경제를 강화하는 고부가가치 처리 경로 중심으로 최적화를 진행 중입니다.

온라인 쇼핑 급증으로 복잡한 다층 포장재가 발생해 기존 재활용 시스템을 무력화시키고 있습니다. 2025년 3월부터 시행되는 영국 신규 규정은 기업에 음식물 쓰레기와 건식 재활용품 분리 의무를 부과해 역물류 협력 및 전용 처리 라인 구축을 강제합니다. 리온델바젤의 4,400만 달러 규모 베셀링 공장과 같은 화학 재활용 시설은 기존 시스템이 처리하지 못하는 복합 필름을 대상으로 합니다. 이 틈새 시장을 장악한 운영사들은 프리미엄 처리 수수료를 부과하며 유럽 폐기물 관리 시장에 새로운 수익원을 창출하고 있습니다.

일반적인 WtE 시설 건설 비용은 2억 2천만-4억 4천만 달러에 달하며, 허가 절차는 7년까지 소요될 수 있어 투자자는 정책 변화와 금리 상승 위험에 노출됩니다. 특히 인구 밀집 지역에서의 지역사회의 반발은 검증된 배출 제어 기술에도 불구하고 승인 절차를 지연시킵니다. “제로 소각” 정책을 요구하는 활동가의 압박으로 개발사는 실시간 배출 모니터링 시스템과 탄소 포집 부가 설비에 투자해야 하며, 이는 프로젝트 경제성을 악화시키고 설비 증설 규모를 제한합니다.

2025년 시점에서 유럽의 폐기물 관리 시장에서 주택 폐기물이 55.02%라는 압도적인 점유율을 차지하고 있습니다. 이는 예측 가능한 주택 폐기물 발생 패턴이 수거 경로, 요금 구조 및 지방 자치 단체 예산의 기반이 된다는 점을 강조합니다. 베를린과 코펜하겐의 스마트 쓰레기통 도입은 수거 빈도를 최적화하고 트럭 주행 거리를 줄여 비용 상승을 억제하고 있습니다. 주택이 여전히 주요 발생원이지만, 상업 폐기물이 2031년까지 연평균 7.18% 성장률로 주요 성장 동력으로 부상하고 있습니다. 이 급증은 전자상거래 포장재와 가볍지만 부피가 큰 폐기물을 발생시키는 유연한 업무 공간의 급증에 기인하며, 이는 특수 압축 및 역물류 처리가 필요합니다.

상업 폐기물의 확대는 골판지, 다층 필름, 폐기 IT 장비 등 새로운 재료를 유럽 폐기물 관리 시장에 유입시켜 맞춤형 분리 및 고급 처리를 요구하고 있습니다. 마드리드와 밀라노 인근 물류 허브에서는 골판지와 플라스틱을 사전 분류하는 로봇 기술을 시범 운영 중이며, 파리의 오피스 타워에는 적기 수거를 위한 잔량 센서가 내장되고 있습니다. 산업 폐기물은 꾸준한 기여 요인으로 남아 있으나 공정 효율성 향상과 근접 조달로 인해 성장세가 완화되는 반면, 의료 폐기물은 고령화 인구 증가에 맞춰 규모가 확대되며 열소독 및 오토클레이브 서비스 분야의 틈새 사업자들을 지원하고 있습니다.

European Waste Management Market size in 2026 is estimated at USD 366.83 billion, growing from 2025 value of USD 348.54 billion with 2031 projections showing USD 473.93 billion, growing at 5.25% CAGR over 2026-2031.

This solid growth path underscores how the European waste management market is benefiting from strict landfill-reduction mandates, fast-rising investment in waste-to-energy (WtE) assets, and an unmistakable shift toward circular economy principles. Regulatory pressure, most notably the European Union's requirement to cap municipal landfilling at 10% by 2035, is accelerating capital inflows into recycling, chemical recovery, and AI-enabled collection systems, while creating a step-change in demand for advanced treatment technologies. Germany remains the anchor market, leveraging mature Extended Producer Responsibility (EPR) systems and robust WtE networks, yet Spain is now the headline growth story as large-scale chemical recycling plants and smart-bin pilots unlock new capacity. Across the value chain, leading operators are acquiring complementary assets to build fully integrated service offerings, and data-centric start-ups are monetizing analytics that cut truck mileage, carbon emissions, and operating costs.

The 10% cap on landfilling is rewriting municipal budgets and planning calendars across the European waste management market. Germany already operates near-zero landfill levels, yet Spain and Italy are quickly adding WtE lines and high-throughput MRFs to stay on track for 2035 compliance. Penalties for non-compliance, coupled with restricted EU funding, are pushing even slower adopters to redirect residual waste toward energy recovery or advanced recycling. Operators such as SUEZ have responded with district-heating WtE projects that convert waste into 360 GWh of heat annually for Toulouse, demonstrating how compliance can unlock new utility revenue. As the lowest-cost disposal option disappears, every stakeholder now optimizes around higher-value treatment pathways that strengthen the circular economy.

A spike in online shopping yields complex, multi-layer packages that frustrate conventional recycling. New UK rules starting March 2025 obligate firms to separate food waste and dry recyclables, forcing reverse-logistics partnerships and dedicated processing lines. Chemical recycling plants, such as LyondellBasell's USD 44 million Wesseling unit, target composite films that traditional systems reject. Operators who master this niche command premium gate fees, giving the European waste management market fresh revenue streams.

Typical WtE units cost USD 220-440 million, and permitting can stretch seven years, exposing sponsors to policy shifts and rising interest rates. Community push-back, especially in densely populated corridors, slows approvals despite proven emission controls. Activist pressure for "zero-incineration" policies has forced developers to invest in real-time emissions dashboards and carbon-capture add-ons, elevating project economics and capping capacity additions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Residential sources held a commanding 55.02% share of the European waste management market in 2025, underscoring how predictable household generation patterns underpin collection routes, fee structures, and municipal budgets. Smart-bin rollouts in Berlin and Copenhagen are optimizing collection frequency and cutting truck miles, keeping cost escalation in check. Although households remain the volume anchor, commercial sources are emerging as the primary growth lever with a forecast 7.18% CAGR through 2031. The surge is rooted in e-commerce packaging and the mushrooming of flexible workspaces that generate light but bulky streams requiring specialized baling and reverse logistics.

Commercial waste expansion injects new materials corrugated board, multi-layer films, and discarded IT equipment, into the European waste management market, demanding tailored segregation and advanced treatment. Logistics hubs near Madrid and Milan are piloting robotics that pre-sort cardboard and plastic, while office towers in Paris are embedding fill-level sensors to trigger just-in-time pickups. Industrial waste remains a steady contributor, yet its growth is tempered by process efficiency gains and near-sourcing, whereas healthcare waste scales in line with aging populations, supporting niche operators in thermal disinfection and autoclave services.

The European Waste Management Market Report is Segmented by Source (Residential, Commercial, Industrial, and More), by Service Type (Collection, Transportation, Sorting & Segregation, and More), by Waste Type (Municipal Solid, Industrial Hazardous, E-Waste, Plastic, and More), and by Geography (UK, Germany, France, Italy, Spain, BENELUX, NORDICS, and the Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).