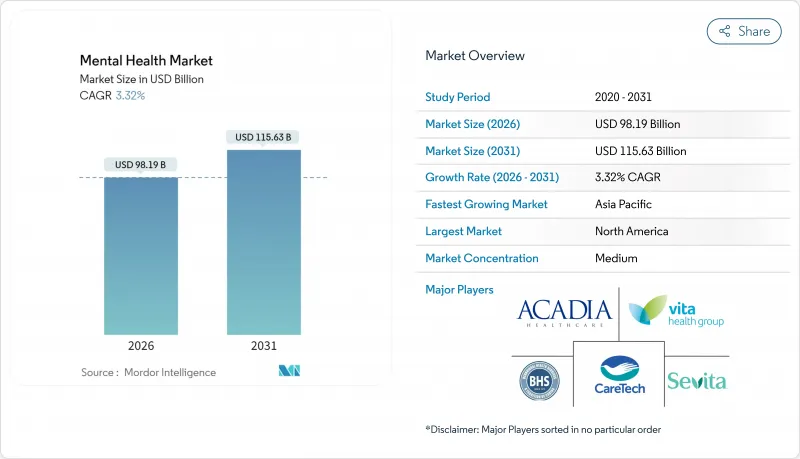

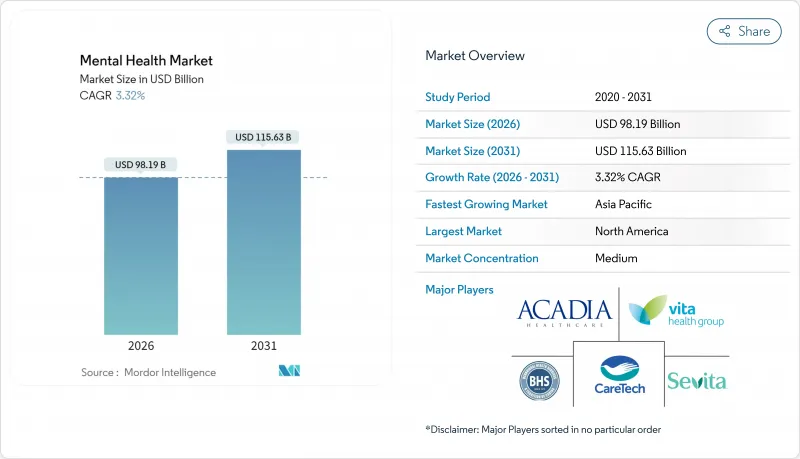

2026년 정신건강 시장 규모는 981억 9,000만 달러로 추정되며, 2025년 950억 3,000만 달러에서 성장한 수치입니다.

2031년에는 1,156억 3,000만 달러에 달할 전망으로, 2026년부터 2031년에 걸쳐 CAGR 3.32%로 성장할 것으로 예측되고 있습니다.

행동 의료에 대한 지속적인 정부 지출, 원격 의료의 보급, AI를 활용한 트리어지 툴의 도입 가속이, 이 안정된 성장 궤도를 지지하고 있습니다. 고용주에 의한 ESG 연동형 웰빙 시책, 미국 및 유럽에 있어서의 의료보험 적용균등법, 디지털 치료제의 상환확대가 더욱 접근 확대를 촉진하고 있습니다. 프로바이더가 오프라인 매장의 능력과 확장 가능한 가상 모델을 융합시키는 중, 경쟁의 격화가 진행되고 있습니다. 한편, 데이터 프라이버시 의무와 노동력 부족이 단기적인 공급 확대를 제한하고 있습니다. 투자자들은 사춘기 플랫폼과 아시아태평양의 신규 진출기업에 대한 지원을 계속하고 있으며 정신건강 시장에서 서비스가 잘 알려져 있지 않은 분야에 대한 신뢰를 보여주고 있습니다.

2020년 이후 세계의 이환율은 급격히 상승하고 최근 WHO 조사에서 유의미한 감소 경향은 보이지 않았습니다. 대학 학생을 대상으로 한 2024년 조사에서는 55%가 불안, 41%가 우울함을 보고하고 있으며, 리스크 대상층의 확대가 부각되고 있습니다. 유병률의 상승은 지속적인 수요를 낳고, 특히 임상 인프라가 미정비인 중소득국에서는 의료 제공 능력에 부하가 걸려 있습니다. 다국간 보건기관은 현재 국가계획에 있어서 만성질환 관리와 동등한 자리매김으로 정신건강 대책을 추진하고 있으며, 예산을 지역밀착형 서비스나 측정틀에 재분배하고 있습니다.

2025년 메디케어 의사 보상 일정에서 영구적인 상환 코드를 채택하여 가상 행동 의료가 주류 치료법으로 인정되었습니다. 결과 데이터는 대면 세션과 동등한 효능을 나타내며 대규모 메타 분석에서는 환자 수용률이 71%에 달할 전망입니다. 시장 접근은 아시아태평양에서 가장 빠르게 확대되고 있으며 스마트폰 보급이 물리적 시설 부족을 보완하고 있습니다. 주를 넘는 라이선싱 제도와 광대역 격차는 여전히 장벽이지만, 양자간 협정이나 관민 연계의 접속 프로젝트에 의해 격차는 축소되고 있습니다.

현재 미국 정신건강 수요의 불과 28%만 채워지고 있으며, 2024년 기준에서 30,000개 이상의 정신과 의사 포스트가 부족합니다. 호주에서도 비슷한 격차가 존재하며 정신건강 간호 공급 능력은 수요의 56%만을 충족합니다. 연수의 병목, 초기 경력의 번아웃, 보상 격차가 인재 공급의 확대를 방해하고 있습니다. 지방의 진료권에서는 1명의 정신과 의사가 3만명을 넘는 인구를 커버하는 경우도 있어, 원격 정신 의료나 공동 케어 모델에의 의존을 촉구하고 있습니다.

2025년 정신 건강 시장 규모에서 우울증은 38.41%를 차지하고 있습니다. 이것은 확립된 진단 프로토콜과 안정적인 약물 요법의 보급을 반영한 것입니다. 한편 불안장애는 4.05%의 연평균 복합 성장률(CAGR)로 확대가 전망되고 있어 광범위한 스크리닝과 문화적으로 배려된 치료 앱의 보급이 이를 지원하고 있습니다. 기분 장애 시장 점유율은 여전히 견고하지만, 아시아태평양의 불안 장애의 유병률 상승은 수익 구조의 전환을 나타내는 중요한 징후입니다. 제약 파이프라인과 AI를 활용한 노출요법은 이 증가분을 끌어들이는 태세를 갖추고 있습니다.

자연어처리기술에 의한 아임상 증상의 검출은 진단 정밀도를 향상시켜 치료 대상자의 확대로 이어지고 있습니다. 통합 케어 패스웨이에서는 병존하는 약물 사용 장애와 불안 장애를 동시 관리하고, 각 부문에서 치료 건수를 증가시키고 있습니다. 정신 분열증과 양극성 장애는 지속적인 주사제와 전문 의료 네트워크의 확장으로 꾸준한 확대를 계속하고 있으며, 디지털 재발 예측 도구가 입원 빈도를 줄이고 있습니다.

2025년 수익의 41.86%는 외래 상담이 차지했지만, 디지털 치료제 및 앱은 2031년까지 연평균 복합 성장률(CAGR)4.18%가 전망되고 있습니다. FDA 승인 소프트웨어를 위한 새롭게 설정된 메디케어 코드는 지불자의 신뢰를 확고히 하고, 디바이스 지원형 행동 개입의 정당성을 확립합니다. 소프트웨어 치료로서의 정신건강 시장 규모는 현재 작지만 효과 데이터가 성숙함에 따라 상대적으로 큰 벤처 자금을 모으고 있습니다. 가상 및 원격정신의료는 임상의의 지리적 편재를 해소하고 환자의 편리성에 대한 요망에 부응함으로써 기세를 유지하고 있습니다.

긴급 정신건강 서비스는 수요 급증으로 구급 부문의 용량이 박박해 원격 위기 대응 제공업체와의 제휴를 촉진하고 있습니다. 가상 트리아지와 단기 대면 안정화를 융합한 하이브리드 케어 패키지로 평균 입원일수가 단축되었습니다. 입원 치료 건수는 병존 질환의 복잡성이나 강제 치료 규정에 의해 안정을 유지하고 있습니다만, 상환 상한이 이익률을 압박하고 있습니다.

2025년에도 북미는 정신 건강 시장의 중심지이며 확립된 보험 적용 범위, 성숙한 제공업체 네트워크, 조기 디지털 헬스 도입으로 41.84%의 매출 점유율을 차지했습니다. 지속적인 치료법 균등법의 시행과 영구적인 원격 의료 상환 코드가 기세를 유지하는 한편, AI 규제 치료 기기가 서비스 확장성을 가속화하고 있습니다. 미국 지방군의 인력 부족은 지속적으로 수용 능력을 압박하고 있으며 원격 정신과 의료 거점에 대한 투자를 촉진하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 4.78%로 가장 빠르게 성장하는 지역으로 공중보건 지출 증가와 거의 보편적인 모바일 보급이 견인하고 있습니다. 일본, 싱가포르, 호주 정부는 국민 모두 보험 제도의 청사진에서 정신건강 예산을 할당하고 다국어 앱의 출시와 국경을 넘어 임상의 마켓플레이스의 활성화를 촉구하고 있습니다. 문화적 편견은 여전히 장벽이지만, 공중 계발 캠페인은 특히 젊은층을 중심으로 지원을 요구하는 것이 정상화되고 있습니다. 중국에서는 지방도시의 진료소에서 AI 기반의 트리어지가 도입되어 곧 지방 네트워크 전체에의 보급이 시사되고 있습니다.

유럽에서는 '유럽 건강 데이터 공간'에 의한 디지털 건강 규제의 조화가 진행되어 성장은 안정되고 있습니다. GDPR(EU 개인정보보호규정)은 데이터 처리 모니터링을 강화하고 있지만 증거 기반 소프트웨어 요법에 대한 명확한 상환 일정이 제공업체의 도입을 지원합니다. 중동 유럽 국가에서는 의료 종사자 부족을 보완하기 위해 원격 위기 핫라인을 시험 도입하고, 북유럽 국가에서는 1차 케어의 전자 건강 기록(EHR)에 정신건강 대시보드를 통합하고 있습니다.

남미 및 중동 및 아프리카은 절대적인 지출액으로는 늦어지는 것, 특정 분야에서의 진전을 볼 수 있습니다. 브라질의 SUS 네트워크는 원격 지역을 위한 원격 심리 상담의 시험 도입을 진행하고, 걸프 국가에서는 국가 전자 정부 포털에 웰니스 앱을 통합하고 있습니다. 기부자 자금에 의한 노력으로 기초적인 상담의 커버율이 확대되고, 해외 거주 의료 종사자가 원격 진료 계약을 통해 현지의 의료 체제를 보강하고 있습니다. 인프라, 지불, 인재면에서의 장벽이 성장을 억제하는 한편, 미개척 수요가 존재하는 것을 부각하고 있습니다.

Mental Health market size in 2026 is estimated at USD 98.19 billion, growing from 2025 value of USD 95.03 billion with 2031 projections showing USD 115.63 billion, growing at 3.32% CAGR over 2026-2031.

Sustained government spending on behavioral health, normalization of virtual care, and accelerating uptake of AI-enabled triage tools underpin this steady trajectory. Employers' ESG-linked wellbeing mandates, parity legislation in the United States and Europe, and growing digital-therapeutics reimbursement further widen access. Competitive intensity is rising as providers blend bricks-and-mortar capacity with scalable virtual models, while data-privacy obligations and workforce shortages limit near-term supply growth. Investors continue to back adolescent-focused platforms and Asia-Pacific entrants, signaling confidence in underserved segments of the mental health market.

Global incidence climbed sharply after 2020, and recent WHO surveys signal no meaningful reversion. Among college students, 55% reported anxiety and 41% reported depression in 2024, underscoring a widened risk pool. Elevated prevalence drives sustained demand that strains care capacity, particularly in middle-income economies where clinical infrastructure remains thin. Multilateral health agencies now position mental health parity alongside chronic-disease management in national plans, redirecting budget lines toward community-based services and measurement frameworks.

Permanent reimbursement codes in the 2025 Medicare Physician Fee Schedule validate virtual behavioral health as a mainstream modality. Outcome data show comparable efficacy to in-person sessions, and patient acceptance has reached 71% in large meta-analyses. Market access expands most rapidly in Asia-Pacific where smartphone penetration offsets brick-and-mortar gaps. Cross-state licensing and broadband inequity remain friction points, but bilateral compacts and public-private connectivity projects are narrowing disparities.

Only 28% of U.S. mental-health needs are currently met, and more than 30,000 psychiatric positions remained unfilled in 2024. Similar gaps exist in Australia, where mental-health nursing capacity meets just 56% of demand. Training bottlenecks, early-career burnout, and compensation differentials limit pipeline growth. In rural catchment areas, one psychiatrist may cover populations exceeding 30,000, prompting dependence on tele-psychiatry and collaborative-care models.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Depression held 38.41% of the 2025 mental health market size, reflecting entrenched diagnostic protocols and steady pharmacotherapy uptake. Anxiety disorders, however, are forecast to climb at a 4.05% CAGR, supported by broader screening and culturally sensitive therapy apps. The mental health market share for mood disorders remains secure, yet rising anxiety prevalence in Asia-Pacific signals a pivotal revenue shift. Pharmaceutical pipelines and AI-mediated exposure therapies are positioning to capture this incremental growth.

Improvements in diagnostic precision, powered by natural-language processing that flags sub-clinical symptoms, are expanding treatment candidacy. Integrated care pathways now co-manage comorbid substance-use and anxiety, raising treatment volumes across segments. Schizophrenia and bipolar disorder continue steady expansion through long-acting injectables and specialty network rollouts, while digital relapse-prediction tools reduce hospitalization frequency.

Out-patient counselling generated 41.86% of 2025 revenues, yet digital therapeutics & apps are set for a 4.18% CAGR through 2031. Newly established Medicare codes for FDA-cleared software anchor payor confidence and legitimize device-supported behavioral interventions. The mental health market size for software-as-treatment remains modest today but attracts disproportionate venture funding as efficacy data matures. Virtual & tele-psychiatry retains momentum by resolving geographical mal-distribution of clinicians and aligning with patients' convenience preferences.

Emergency mental-health services observe surging demand that strains ED capacity, propelling collaborations with tele-crisis providers. Hybrid care packages that merge virtual triage with brief in-person stabilization are reducing average length of stay. In-patient treatment volumes remain stable, buffered by comorbidity complexity and compulsory-care statutes, though reimbursement ceilings pressure margins.

The Mental Health Market Report is Segmented by Disorder (Depression, Anxiety, and Others), Service Type (In-Patient Treatment, Out-Patient Counselling, and Others), Age Group (Children & Adolescents, Adults, Geriatric), End User (Hospitals & Clinics, Community Mental-Health Centres, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America remained the epicenter of the mental health market in 2025, posting 41.84% revenue share due to established insurance coverage, mature provider networks, and early digital-health uptake. Ongoing enforcement of parity laws and permanent virtual-care reimbursement codes sustain momentum, while AI-regulated therapeutic devices accelerate service scalability. Workforce scarcity in rural U.S. counties continues to pinch capacity, channeling investment toward tele-psychiatry hubs.

Asia-Pacific is the fastest-growing region at a 4.78% CAGR through 2031, propelled by incremental public-health spending and near-ubiquitous mobile penetration. Governments in Japan, Singapore, and Australia earmark mental health allocations within universal-coverage blueprints, spurring multi-lingual app launches and cross-border clinician marketplaces. Cultural stigma remains a hurdle, but public education campaigns are normalizing help-seeking, especially among younger cohorts. China's tier-two cities adopt AI-based triage at community clinics, signaling eventual diffusion into provincial networks.

Europe's growth remains steady as the region harmonizes digital-health regulations under the European Health Data Space. GDPR heightens data-handling scrutiny, but clear reimbursement schedules for evidence-based software therapies support provider adoption. Central and Eastern European countries pilot tele-crisis hotlines to offset clinician shortages, while Nordic systems integrate mental health dashboards into primary-care EHRs.

South America and the Middle East & Africa trail in absolute spending yet exhibit targeted progress. Brazil's SUS network integrates tele-psychology pilots for remote provinces, while Gulf states embed wellness apps in national e-government portals. Donor-funded initiatives expand basic counseling coverage, and diaspora clinicians augment local capacity via tele-consult contracts. Infrastructure, payment, and workforce barriers temper growth but underscore untapped demand.