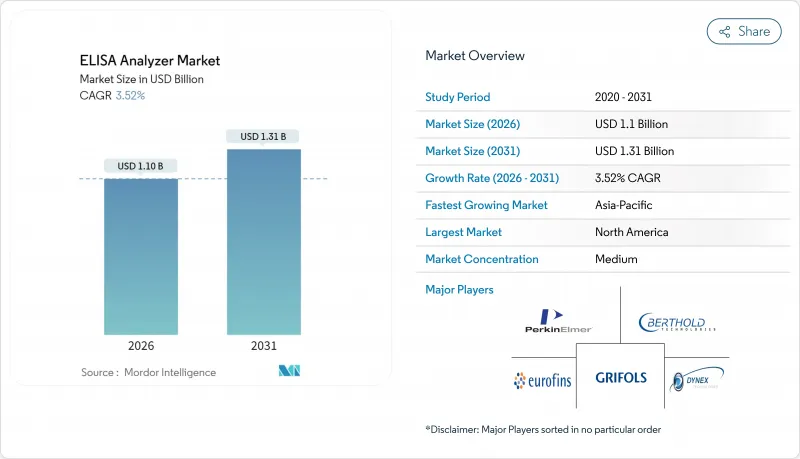

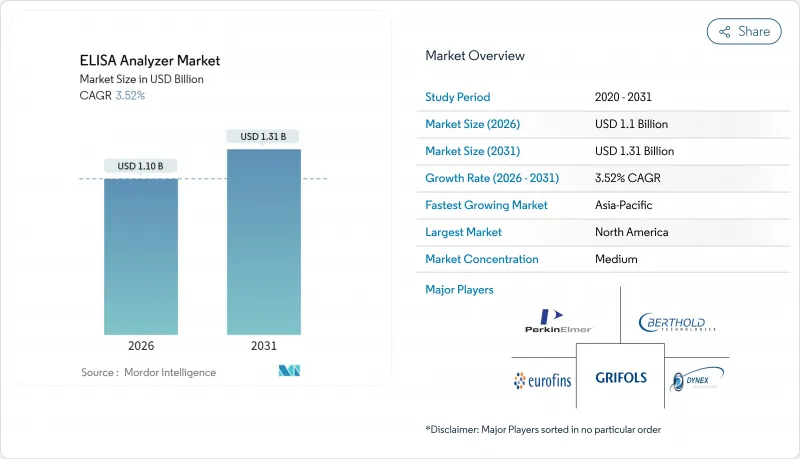

2026년 ELISA 분석기 시장의 규모는 11억 달러로 추정되며, 2025년 10억 6,000만 달러에서 성장하여, 2031년에는 13억 1,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 3.52%를 나타낼 전망입니다.

수요 증가는 수동 면역 측정법에서 통합 및 고처리량 자동화 시스템으로의 전환을 반영합니다. 이로 인해 작업 시간이 줄어들고 진화하는 문서화 규제를 준수하여 만성적 인력 부족 현상을 해소할 수 있습니다. 임상 화학 검사와 면역 측정 메뉴를 연계할 수 있는 자동화 플랫폼이 현재 설비 투자 판단의 기반이 되고 있는 한편, 저농도 표적 물질의 검출에 높은 감도를 요하는 치료제 모니터링 분야에서는 화학 발광 검출법의 도입이 계속 확대되고 있습니다. 지리적 확장은 아시아태평양의 인프라 투자에 의해 추진되고 있지만, 북미의 실험실은 여전히 고용량 시스템의 최첨단 도입지로 남아 있습니다. 이는 최신 분석 장비에 내장된 감사 추적 기능이 2024년 시행된 LTD(실험실 개발 검사) 규제에 따른 컴플라이언스를 단순화하기 때문입니다. 플랫폼 구매는 워크로드가 증가함에 따라 처리 능력을 확장할 수 있는 모듈 설계에 점점 의존하고 있으며, 기존에 기술 업데이트 사이클을 저해한 완전 교체 비용을 줄이고 있습니다.

2024년, 비감염성 질환은 세계 사망 원인의 74%를 차지했으며, 이 부담에 의해 일상적인 바이오마커 감시 프로그램의 급속한 확충 동향이 강해지고 있습니다. 동시에 팬데믹 후 모니터링 프로토콜은 감염성 병원체의 기준선 검사량을 증가 시켰습니다. ELISA 플랫폼은 높은 처리량과 낮은 단가의 검사 비용을 결합하여 두 시나리오 모두에 적합합니다. 따라서 검사건수의 급증에 직면하는 실험실에서는 플레이트에 대한 시료 주입, 세정, 및 판독을 자동화하는 시스템을 우선적으로 도입하여 검사자가 보다 많은 1차 검사를 관리할 수 있도록 하고 있습니다. 각 공급업체는 현재 검사 결과를 검사 정보 시스템에 직접 전송하는 연결 도구를 번들로 제공하여 실수 위험을 최소화하면서 지불자 및 규제 당국이 요구하는 감사 추적성을 엄격하게 실현하고 있습니다. 만성 질환과 감염 모두에 의해 팬데믹의 직접적인 영향을 받은 후에도 이용률은 장기간에 걸쳐 높은 수준을 유지할 것으로 예측됩니다.

실험실 통합 및 인력 감소는 완전 자동 분석기의 도입 이점을 더욱 강화하고 있습니다. 바이오-테크네사의 Ella 플랫폼은 주로 수동 피펫팅 공정을 줄임으로써 중간 규모 실험실에서 도입 비용을 2년 이내에 회수할 수 있음을 입증하고 있습니다. FDA의 2024년 '실험실 개발 검사(LDT) 규정'으로 인해 수동 ELISA에서는 효율적으로 제공할 수 없는 전자적인 추적성이 컴플라이언스의 요점이 되면서 자동 분석기의 매력을 한층 더 높이고 있습니다. 결과적으로 조달위원회는 바코드 추적, 온보드 품질 관리 및 양방향 LIS 통신을 통합하는 분석 장비를 점점 더 선택하고 있습니다. 도입 후 이러한 시스템은 종종 여러 구형 장비를 대체하여 공급업체의 시약 지출 점유율을 확대하고 고객을 다년간 서비스 계약에 연결합니다.

미국 임상병리학회(ASCP)의 보고에 의하면, 2024년 기준으로 핵심 검사 업무직의 공석률은 89%에 이르렀고, 검사자의 평균 근속 연수는 하락을 계속하고 있습니다. 또한 지멘스 헬시니어스의 병행 조사를 통해 현직 직원의 3분의 2가 2034년까지 퇴직을 고려하는 것으로 나타났습니다. 자동화가 진행되더라도 실험실에는 플래그 검토, 분석 문제 해결, 새로운 분석을 검증하는 자격을 갖춘 과학자가 필요합니다. 인원 부족으로 인해 일부 시설에서는 일일 면역 측정 검사량에 상한을 두거나 전문 검사를 외부에 위탁할 수밖에 없으며, 환자 치료의 지연이나 분석기의 수익 기회 손실을 초래하고 있습니다. 벤더는 원격 진단 서비스나 유지관리 가이드 동영상의 제공으로 대응하고 있지만, 교육 프로그램의 수용 능력이 한정되어 있는 현재 상황에서는 인재 확보의 과제가 조기에 해소될 전망이 희박합니다.

자동화 시스템은 2025년 매출액의 67.92%를 차지하였으며, 이는 수동 스테이션으로는 실현할 수 없는 무인 배치 처리와 전자 품질 관리 추적 기능에 대한 실험실 수요를 반영하고 있습니다. 통합이 진행됨에 따라 처리 능력 목표가 인적 피펫팅 능력을 초과하는 허브 앤 스포크형 검사 네트워크가 형성되기 때문에 자동화 라인 수요는 CAGR 5.38%로 확대될 전망입니다. 높은 볼륨의 기준 실험실용 ELISA 분석기 시장에서도 자동화 유닛은 밀폐형 로봇 기술에 의해 조작자의 시약 및 환자 검체와의 접촉을 줄여 생물학적 위험에 대한 노출 리스크를 최소화합니다. 반자동장치는 1일 검사량이 그다지 많지 않은 진료소나 소규모 지역 병원에 있어서는 여전히 매력적인 옵션이지만, 이러한 시설에서도 인건비의 압력에 의해 소유 비용의 차이는 축소되고 있습니다. ELISA 분석기 업계 전반에 걸쳐, 조달 기준은 순수한 구매 가격에서 라이프 사이클 비용, 가동 시간 보장, 병원 캠퍼스 내의 여러 분석기 간에 결과를 조화시키는 미들웨어 연결성으로 전환하고 있습니다.

자동화로 전환하는 실험실은 면역 측정 및 화학 측정 메뉴에서 시약 팩을 공유할 수 있는 플랫폼을 선호합니다. 시간당 최대 1,550개의 검사를 수행할 수 있는 Abbott의 Alinity ci 시리즈가 그 예입니다. 분야 횡단적인 기능을 통해 분석기는 일상적인 워크플로에 추가로 통합되어 시약 소비량이 증가하고 기존 장치의 교체 가능성이 낮아집니다. 서비스 계약에는 부품, 인건비, 소프트웨어의 업그레이드가 포함되어 벤더는 연구개발비를 회수할 수 있고 실험실은 예기치 않은 비용의 발생을 억제하면서 5년간의 예산을 예측할 수 있습니다. 애널리스트는 장기적으로 완전 자동화가 ELISA 분석기 시장을 독점할 것으로 예측하고 있지만, 자본 예산이 제약된 경우나 샘플의 혼합에 의해 유연한 싱글 플레이트 처리가 필요한 경우 등, 틈새 반자동화 수요는 앞으로도 계속될 것으로 예상하고 있습니다.

2025년에는 벤치탑형 분석기가 61.78%의 점유율을 차지했습니다. 이는 업그레이드된 병원 실험실의 공간 제약에 의해 기존 캐비닛 아래에 수납 가능한 컴팩트 케이스가 선호되기 때문입니다. 많은 기종은 플레이트를 수직으로 적재하는 방식이나 듀얼 판독 헤드의 도입에 의해 중간 정도의 처리 능력을 실현하여 종래 벤치탑의 생산성을 제한하고 있던 사이즈 제약을 회피하고 있습니다. 그러나 공간 제약이 적고 검사 메뉴의 폭이 넓어 여러 개의 병렬 인큐베이터를 필요로 하는 핵심 실험실에서는 독립형 플로어 설치 모델이 신규 도입을 획득하고 있습니다. ELISA 분석기 시장에서 플로어 유닛은 자동 벌크 로딩과 연속 공급 모드에 의해 아침 피크 시 채혈 업무를 지원하므로 5.49%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다. 벤치탑 모델의 ELISA 분석기 시장 내 점유율은 작업 공간이 이미 최적화된 경우 대부분의 교체 사이클이 동등한 모델로 교체되기 때문에 약간 감소할 것으로 예측됩니다.

벤더 각사는 공통의 소프트웨어 에코시스템을 통해 두 가지 모달리티의 요구에 대응하고 있어, 벤치탑 장치로 훈련을 받은 오퍼레이터는 플로어 모델에 원활하게 적응 가능합니다. 워펜사의 BIO-FLASH는 벤치탑에서 전문적인 자가면역검사 메뉴를 지원하며, QUANTA-Lyser 3000은 고용량시설용으로 동일한 시약 팩을 스케일업합니다. 이러한 모듈성은 의료 네트워크가 다양한 시설 수준에서 소모품 가격을 고정하면서 훈련과 품질 지표를 표준화하는 다년간의 조달 틀의 기반이 됩니다. 이 추세는 공통 정보 기반을 잇는 유연한 도입 옵션으로 ELISA 분석기 업계 전반의 전환을 반영합니다.

2-3장의 플레이트를 동시에 처리하는 중처리 능력 플랫폼은 200-500 병상 규모의 병원 대부분에 효과적인 비용과 처리 능력 간의 균형을 실현하여 2025년에는 47.10%의 수익을 창출했습니다. 그러나 ELISA 분석기 시장에서의 실험실의 규모는 1회당 4장 이상의 플레이트 처리가 가능한 고처리량 장치로의 이행이 가속화되어 2031년까지 연평균 복합 성장률(CAGR) 5.69%가 전망됩니다. 그 요인으로는 종양학 및 신경학 바이오마커 승인에 수반하는 검사 메뉴의 확충, 코어 생화학 검사 패널을 증가시키는 선택적 수술의 회복을 들 수 있습니다. 저처리량 장비는 검사 유연성을 우선시하는 연구기관에서 일정한 수요를 유지하고 있지만, 중급기종의 가격 저하로 인해 기존의 점유율은 축소세에 있습니다.

자동화기기 제조업체는 구형 중급기기를 상위 기종으로 교체할 때 평가하는 인수 인센티브를 제공함으로써 처리 능력의 계층화를 강화하고 있습니다. 예를 들어, bioMerieux사의 VIDAS KUBE는 장치의 설치 면적을 증가시키지 않고 배양 포지션을 배증시킴으로써 기존 기종의 성능을 비약적으로 능가하고 있습니다. 인적 부족 현상이 지속되는 ELISA 분석기 업계에서 처리 능력의 향상은 추가 전환 없이 서비스 레벨의 개선을 실현하고 의료 시스템의 확장 계획을 뒷받침합니다.

북미는 성숙한 의료 인프라, 엄격한 FDA 감독, 핵심 실험실 자동화의 대규모 도입 실적으로 2025년에도 41.60%의 점유율을 유지했습니다. 2024년 시행된 실험실 개발 검사(LDT) 규제를 활용하는 시설에서는 검증 패키지를 효율화하는 전자 기록 기능 내장 분석기에 대한 투자가 진행되었습니다. 이러한 컴플라이언스 혜택과 시약 렌탈 방식의 자금 조달은 자본 예산의 엄격화에도 불구하고 갱신 주기를 유지합니다. 캐나다는 미국의 도입 패턴을 반영하지만, 전국적인 조달 계약을 통해 주 네트워크 전체에서 수량 할인을 확보할 수 있는 이점이 있습니다.

아시아태평양은 중국과 인도에서 3차 의료기관 및 지역 기준 실험실의 증가에 따라 2031년까지 연평균 복합 성장률(CAGR) 4.49%라는 가장 빠른 성장할 것으로 전망되고 있습니다. 정부 주도로 건강 보험의 적용 범위가 확대되고 1인당 진단 지출이 증가하고 있습니다. 중국은 국내 제조 장려책에 의해 현지 조립 분석기의 수입 관세가 줄어들어, 세계와 로컬의 하이브리드 플랫폼으로의 조달 경향이 촉진되고 있습니다. 일본과 한국의 ELISA 분석기 시장의 규모는 양 시장의 첨단 바이오마커 포트폴리오와 일치하는 화학발광 시스템으로 기울고 있습니다. 반면 ASEAN 국가에서는 공중보건 프로그램을 위한 비용 효율적인 비색법 키트가 여전히 중시되고 있습니다.

유럽은 의약품 제조 클러스터와 면역 측정 스크리닝을 의무화하는 식품 안전 기준에 의해 큰 점유율을 차지합니다. EU의 그린딜은 환경 친화적인 소모품에 대한 수요를 더욱 촉진하고 공급업체는 재활용 가능한 플레이트와 저독성 기판을 개발하고 있습니다. 남미 및 중동 및 아프리카는 여전히 성장 기회를 가지고 있으며, 브라질과 사우디아라비아의 주요 병원 프로젝트에서는 자동 면역 측정 시스템의 도입이 명시되어 있지만, 지역 전체의 보급은 경제 안정성과 현지 서비스 인프라에 의존합니다.

ELISA analyzer market size in 2026 is estimated at USD 1.1 billion, growing from 2025 value of USD 1.06 billion with 2031 projections showing USD 1.31 billion, growing at 3.52% CAGR over 2026-2031.

Demand growth reflects laboratories' shift from manual immunoassay procedures toward integrated, high-throughput automation that reduces hands-on time, aligns with evolving regulatory documentation rules and offsets persistent staffing shortages. Automated platforms able to link clinical chemistry and immunoassay menus now anchor capital-spending decisions, while chemiluminescent detection continues to gain traction for therapeutic drug monitoring where low-abundance targets require greater sensitivity. Geographic expansion is paced by infrastructure investments in Asia-Pacific, yet North American laboratories remain the earliest adopters of high-capacity systems because audit trails built into modern analyzers simplify compliance under the 2024 Laboratory Developed Test rule. Platform purchases increasingly ride on modular designs that scale throughput as workload rises and avoid the full replacement costs that have historically discouraged technology refresh cycles.

Noncommunicable diseases accounted for 74% of worldwide deaths in 2024, a burden that forces routine biomarker surveillance programs to scale rapidly. At the same time, post-pandemic surveillance protocols have elevated baseline testing volumes for communicable pathogens. ELISA platforms suit both scenarios because they combine high throughput with low per-test cost. Laboratories facing surging caseloads have therefore prioritized systems that automate plate loading, washing and reading so staff can manage larger daily runs. Vendors now bundle connectivity tools that push results directly into laboratory information systems, minimizing transcription risk while tightening audit trails demanded by payers and regulators. The double drive of chronic and infectious diseases is expected to keep utilization rates high long after the immediate pandemic effects subside.

Laboratory consolidation and workforce attrition strengthen the business case for fully automated analyzers. Bio-Techne's Ella platform demonstrates that labor savings offset its capital price within two years in midsize laboratories, mainly by cutting manual pipetting steps. The FDA's 2024 Laboratory Developed Test rule magnifies the appeal because compliance now hinges on electronic traceability that manual ELISA cannot supply efficiently. Consequently, procurement committees increasingly select analyzers that integrate bar-code tracking, onboard quality controls and bidirectional LIS communication. Once installed, these systems often replace several legacy instruments, broadening the vendor's share of reagent spend and tying accounts into multiyear service contracts.

The American Society for Clinical Pathology reported an 89% vacancy rate across core laboratory roles in 2024, with median technologist tenure continuing to fall. Siemens Healthineers' parallel survey suggests two-thirds of current staff plan retirement by 2034. Even with automation, laboratories need qualified scientists to review flags, troubleshoot runs and validate new assays. Staff deficits force some facilities to cap daily immunoassay volume or outsource specialized tests, delaying patient care and eroding potential analyzer revenue. Vendors respond by embedding remote-service diagnostics and guided maintenance videos, but recruiting challenges are unlikely to abate soon given constrained academic program capacity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Automated systems held 67.92% revenue in 2025, reflecting laboratories' preference for unattended batch processing and electronic QC tracking that manual stations cannot match. Demand for automated lines will expand at 5.38% CAGR as consolidation generates hub-and-spoke testing networks where throughput goals exceed human pipetting capacity. In the ELISA analyzer market size for high-volume reference labs, automated units also minimize biohazard exposure because enclosed robotics reduce operator contact with reagents and patient samples. Semi-automated instruments remain attractive to physician-office labs and small community hospitals with modest daily volumes, yet even those sites face wage pressures that narrow the ownership-cost gap. Across the ELISA analyzer industry, procurement criteria have pivoted from pure acquisition price toward lifecycle cost, uptime commitments and middleware connectivity that harmonizes results across multiple analyzers on a hospital campus.

Laboratories migrating to automation favor platforms with shared reagent packs across immunoassay and chemistry menus, a practice exemplified by Abbott's Alinity ci-series that outputs up to 1,550 tests per hour. This cross-discipline capability further embeds the analyzer into daily workflow, boosting reagent pull-through and making incumbent replacement less likely. As service contracts bundle parts, labor and software upgrades, vendors recoup R&D spend while laboratories forecast five-year budgets with fewer surprise costs. Long term, analysts anticipate full automation will dominate the ELISA analyzer market, but niche semi-automatic demand will persist where capital budgets remain constrained or sample mix warrants flexible single-plate handling.

Benchtop analyzers accounted for 61.78% share in 2025 because space premiums in renovated hospital labs favor compact chassis that slide beneath existing cabinetry. Many deliver mid-range throughput by stacking plates vertically or utilizing dual reading heads, sidestepping the size limits that once capped benchtop productivity. Stand-alone floor models nevertheless capture new installation at core labs where space is less constrained and menu breadth demands multiple parallel incubators. In this ELISA analyzer market, floor units are set to grow 5.49% CAGR owing to automated bulk loading and continuous-feed modes that free staff during peak morning draws. The ELISA analyzer market share of benchtop models thus faces only slight erosion because most replacement cycles keep to like-for-like swaps when bench space is already optimized.

Vendors meet both modality needs through shared software ecosystems so operators trained on a benchtop unit can rotate seamlessly to a floor model. Werfen's BIO-FLASH suits specialty autoimmune menus on a bench, while its QUANTA-Lyser 3000 scales identical reagent packs for high-volume centers. Such modularity underpins multiyear procurement frameworks where health networks lock in consumable pricing across diverse facility tiers yet standardize training and quality metrics. The trend reflects the ELISA analyzer industry's broader move to flexible deployment options tethered by common informatics layers.

Mid-throughput platforms that process 2-3 plates simultaneously generated 47.10% revenue in 2025 because they strike an effective cost-capacity balance for most 200-500-bed hospitals. The ELISA analyzer market size within reference labs, however, shows an accelerating pivot to high-throughput units rated for four or more plates per run, translating to a 5.69% CAGR through 2031. Drivers include test-menu expansion following oncology and neurology biomarker approvals and a rebound in elective procedures that inflate core chemistry panels. Low-throughput instruments keep pockets of demand in research institutes that prioritize assay flexibility, but falling price points on mid-range systems erode their traditional share.

Automation suppliers reinforce the throughput ladder by offering trade-in incentives that credit older mid-range systems toward top-tier models. bioMerieux's VIDAS KUBE, for instance, leapfrogs past earlier generations by doubling incubation positions without enlarging the instrument footprint. In the ELISA analyzer industry environment where personnel shortages persist, throughput upgrades can deliver service-level improvements without adding shifts, supporting health-system scaling initiatives.

The ELISA Analyzer Market Report is Segmented by Type of Operation (Automated ELISA Analyzer, and More), Modality (Bench-Top and Stand-alone/Floor-standing), Throughput (Low-Throughput, and More), Assay Format (Sandwich ELISA, and More), Detection Technology (Colorimetric, and More), Application (Vaccine Development, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 41.60% share in 2025 thanks to mature healthcare infrastructure, stringent FDA oversight and a sizable installed base of core-lab automation. Facilities taking advantage of the 2024 Laboratory Developed Test regulations invested in analyzers with built-in e-logs that streamline validation packages. Such compliance perks, coupled with reagent-rental financing, keep replacement cycles active despite capital-budget scrutiny. Canada mirrors U.S. adoption patterns but benefits from national procurement contracts that secure volume discounts across provincial networks.

Asia-Pacific is projected for the fastest 4.49% CAGR through 2031 as China and India add tertiary hospitals and regional reference labs. Government initiatives expand health-insurance coverage, prompting higher diagnostic expenditure per capita. Domestic manufacturing incentives in China reduce import tariffs on locally assembled analyzers, nudging procurement toward hybrid global-local platforms. The ELISA analyzer market size in Japan and South Korea leans toward chemiluminescent systems coherent with those markets' advanced biomarker portfolios, while ASEAN economies still emphasize cost-effective colorimetric kits for public-health programs.

Europe commands significant share rooted in pharmaceutical manufacturing clusters and food-safety standards that mandate immunoassay screening. The EU's Green Deal has further catalyzed demand for environmentally friendly consumables, prompting vendors to develop recyclable plates and low-toxic substrates. South America and Middle East & Africa remain emerging opportunities; flagship hospital projects in Brazil and Saudi Arabia specify automated immunoassay corridors, yet wider regional uptake depends on economic stability and local service infrastructure.