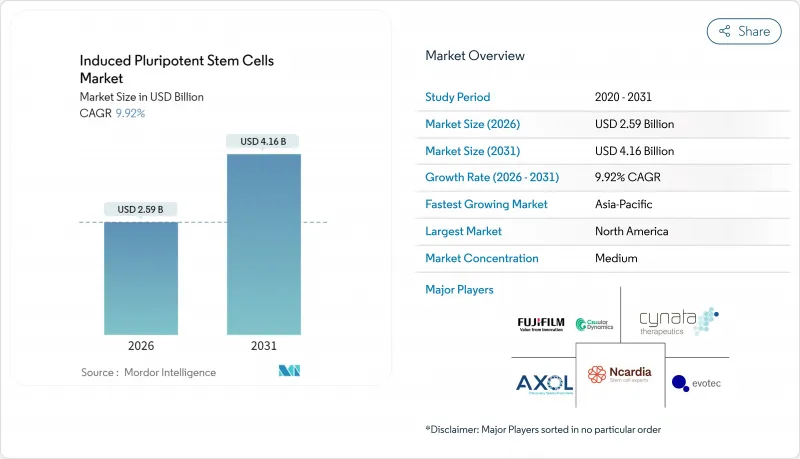

2026년 유도 만능 줄기세포(iPS 세포) 시장 규모는 25억 9,000만 달러로 평가되었고, 2025년 23억 6,000만 달러에서 성장할 것으로 예상됩니다. 2031년까지의 예측으로는 41억 6,000만 달러에 달하고, 2026-2031년에 걸쳐 CAGR 9.92%로 성장할 전망입니다.

이러한 성장은 임상 등급 제조 기술 발전, 치료제 승인 확대, 세포 기반 제품에 대한 규제 지원 강화에서 비롯됩니다. 북미는 국립보건원(NIH) 재생 의료 프로그램을 통해 지속적으로 대규모 투자를 진행 중이며, 일본의 신속 심사 절차는 아시아태평양 지역 성장을 촉진하고 있습니다. 제약사들은 후기 임상시험 실패율을 낮추기 위해 iPSC 모델을 활용하고 있으며, 파킨슨병 및 각막 재생 분야의 획기적인 임상시험 성과가 임상적 유용성을 입증했습니다. 비용 효율적인 바이오 제조 플랫폼, 인공지능 기반 품질 관리 및 광범위한 산업 간 컨소시엄이 시장 모멘텀을 더욱 가속화하고 있습니다.

미국 식품의약국(FDA)의 2024년 지침이 독성학 제출용 플랫폼으로 인간 iPSC 모델을 공식 승인함에 따라 제약 파이프라인이 인간 iPSC 모델로 전환되고 있으며, 이는 개발사들에게 규제 명확성을 제공합니다. 후지필름 셀룰러 다이내믹스는 약물 스크리닝을 위해 일일 생산량을 수십억 개 세포로 확대하며 산업 수요를 입증했습니다. 위탁 연구 기관과 세포주 전문가 간의 협력은 즉시 사용 가능한 품질 관리(QC) 검증 세포주 접근성을 더욱 확대합니다. 공급업체처 자금은 배양 모니터링을 자동화하여 수동 작업량과 주기 시간을 단축하는 인공지능(AI) 기반 이미지 분석 솔루션에 점점 더 집중되고 있습니다. 이러한 발전들은 종합적으로 유도만능줄기세포(iPSCs) 시장이 동물 실험의 대안으로서 신뢰도를 강화하고 후보물질 선정까지의 시간을 단축시키고 있습니다.

세계적 고령화 추세는 신경퇴행성 및 대사성 질환 발생률을 높여 치료적 해결책으로 의료 우선순위를 재편하고 있습니다. 일본의 iPSC 유래 췌도 세포 이식 임상 연구는 제1형 당뇨병 환자의 인슐린 생산을 회복시켜 치료 가능성을 입증했습니다. 각막 iPSC 시트를 이용한 시력 회복 임상시험은 거부 반응 없이 기능적 회복을 달성해 자가 이식의 이점을 부각시켰습니다. 미국에서 진행된 파킨슨병 임상시험은 환자 맞춤형 iPSC를 활용해 도파민 신경세포를 대체함으로써 지속적인 운동 기능 개선을 입증했습니다. 이러한 성과는 재생 의료에 대한 정책적 관심을 강화하고 유도만능줄기세포(iPSC) 시장의 장기적 성장을 지속시킬 것입니다.

여러 계약 제조업체에서 50% 미만의 가동률은 공정 비효율성을 시사하며, 이는 투여량당 비용을 부풀립니다. 리네아바이오의 즉시 사용 가능한 GMP 라인과 옴니아바이오의 AI 기반 시설은 수율 표준화를 시도하지만, 자본 집약도는 여전히 장애물입니다. 단위 비용이 하락하기 전까지는 가격에 민감한 의료 시스템이 보험 적용을 제한할 수 있어 단기 도입이 위축될 수 있습니다.

심근세포는 2025년 총 매출의 28.62%를 차지하며 안전성 약리학 및 초기 단계 심장 복구 치료법의 핵심으로 자리매김했습니다. 이러한 우위는 약물 유발성 심근독성에 대한 엄격한 규제 초점과 영장류 연구에서 수축성을 회복시킨 유망한 공학 심근 이식편과 연관되어 있습니다. 심근세포용 유도만능줄기세포(iPSCs) 시장 규모는 엄격한 심장 스크리닝이 필요한 생물학적 제제의 확대되는 파이프라인에 비례하여 꾸준히 성장할 것으로 전망됩니다. 신경세포는 가장 빠르게 성장하는 부문로, 척수 및 파킨슨병 임상시험이 질병 수정 능력을 입증함에 따라 10.96%의 연평균 복합 성장률(CAGR)을 기록하며 발전하고 있습니다. 간세포는 미소체 대사 연구에 여전히 필수적이며, 섬유아세포와 각질세포는 피부 및 근골격계 분야의 조직 복구 연구를 지원합니다.

제조 기술 발전은 기능적으로 성숙한 심근세포의 광범위한 유통을 뒷받침하며, 여기에는 전기생리학과 성인 유사 표현형을 조화시키는 자동화된 성숙 프로토콜이 포함됩니다. 신경계 계통 프로토콜은 정교화된 패턴화 인자의 혜택을 받아 고함량 스크리닝에 적합한 하위 유형 특이적 집단을 생성합니다. 유럽 유도만능줄기세포 은행(European Bank for Induced Pluripotent Stem Cells)을 통한 선별된 세포 은행의 가용성은 실험실 간 재현성을 보장합니다. 미분화 세포를 제거하는 화학 기술이 개선됨에 따라 배치 출시 장벽이 완화되어 유도만능줄기세포(iPSCs) 시장 전반에 걸친 상업적 채택이 확대되고 있습니다.

북미는 2025년 수익의 37.13%를 차지하며 미국 국립위생연구소(NIH)의 자금 배분과 활발한 공급업체처 캐피탈 에코시스템에 지지되고 있습니다. 지역 병원에서는 획기적인 파킨슨병과 심근증에 대한 최초의 인간 임상시험이 실시되어 트랜스레이셔널 리서치에서 주도적 입장을 나타냈습니다. FDA의 대체 방법에 대한 진보적인 지침은 시험관 내 패널의 채택을 가속화하고 국내 수요를 심화시키고 있습니다. 그러나 높은 인건비와 시설 비용으로 기업은 특정 제조 공정을 저비용 지역으로 아웃소싱하는 경향이 있습니다.

아시아태평양 지역은 일본의 신속 승인 및 상당한 정부 자금 지원에 힘입어 2031년까지 연평균 12.14%의 성장률을 보일 것으로 예상됩니다. 중국은 GMP 공장 건설에 지방 보조금을 투입하는 반면, 한국은 전자 산업 수준의 자동화 전문성을 활용해 폐쇄형 시스템 바이오리액터의 규모를 확대하고 있습니다. 이에 따라 유도만능줄기세포 시장은 북미 개발사가 신속한 시장 진입을 위해 일본 파트너사에 임상 후보 물질을 라이선스하는 등 국경을 초월한 제휴가 이루어지고 있습니다.

유럽은 성숙한 시장이면서도 신중한 자세를 유지하고 있습니다. 유럽 의약품청(EMA)은 환자 안전을 보장하는 상세한 선진 의료 가이드라인을 발행했는데, 이에 따라 신청 서류의 준비 기간이 장기화되고 있습니다. 유럽 iPS 세포 은행의 지원을 받는 조화 시험 방법 컨소시엄은 과학적 리더십을 유지하고 있습니다. 그러나 보험상환의 제약이 임상도입의 확산을 방해하고 있으며 기업은 개념실증연구를 우선해야 할 수 없는 상황입니다.

중동, 아프리카, 남미 등 신흥 지역은 특히 안과 분야에서 관심의 포켓을 보이지만, 인프라 격차와 초기 단계의 규제로 인해 유도만능줄기세포(iPSCs) 시장 내 즉각적인 상업적 규모 확대는 제한됩니다.

induced pluripotent stem cells market size in 2026 is estimated at USD 2.59 billion, growing from 2025 value of USD 2.36 billion with 2031 projections showing USD 4.16 billion, growing at 9.92% CAGR over 2026-2031.

Gains arise from clinical-grade manufacturing advances, growing therapeutic approvals and increasing regulatory support for cell-based products. North America continues to invest heavily through the National Institutes of Health (NIH) Regenerative Medicine Program, while Japan's expedited review pathway is catalyzing Asia-Pacific growth. Pharmaceutical companies use iPSC models to cut late-stage trial failures, and breakthrough Parkinson's and corneal regeneration trials have validated clinical relevance. Cost-efficient biomanufacturing platforms, artificial-intelligence-enabled quality controls and broader cross-sector consortia further accelerate market momentum.

Pharmaceutical pipelines are pivoting toward human iPSC models because the U.S. Food and Drug Administration's 2024 guidance formally accepted these platforms for toxicology submissions, giving developers regulatory clarity. FUJIFILM Cellular Dynamics scaled daily output to billions of cells for drug screens, underscoring industrial demand. Collaborations between contract research organizations and cell-line specialists further widen access to off-the-shelf, QC-tested lines. Venture funding increasingly targets AI-driven image analysis suites that automate culture monitoring, shrinking manual workloads and cycle times. Together, these developments strengthen confidence in the Induced pluripotent stem cells (iPSCs) market as an alternative to animal testing and accelerate time-to-candidate selection.

The global aging trend raises incidences of neurodegenerative and metabolic disorders, reshaping healthcare priorities toward curative solutions. Japan's clinical study that transplanted iPSC-derived pancreatic islet cells restored insulin production in type 1 diabetes patients, exemplifying therapeutic promise. Vision-restoration trials using corneal iPSC sheets achieved functional recovery with no rejection episodes, highlighting autologous benefits. Parkinson's disease trials in the United States applied patient-specific iPSCs to replace dopaminergic neurons, demonstrating durable motor improvement. These successes reinforce policy focus on regenerative medicine and sustain long-run expansion of the Induced pluripotent stem cells (iPSCs) market.

Sub-50% utilization at several contract manufacturers signals process inefficiencies that inflate per-dose costs. LineaBio's off-the-shelf GMP lines and OmniaBio's AI-enabled facilities attempt to standardize yields, yet capital intensity remains a hurdle. Until unit costs fall, price-sensitive health systems may restrict reimbursements, tempering near-term adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cardiomyocytes captured 28.62% of total 2025 revenue, positioning them as the anchor for safety pharmacology and nascent heart-repair therapies. This dominance is tied to strict regulatory focus on drug-induced cardiotoxicity and to promising engineered-heart-muscle grafts that restored contractility in primate studies. The Induced pluripotent stem cells (iPSCs) market size for cardiomyocytes is projected to grow steadily in proportion to the expanding pipeline of biologics requiring rigorous cardiac screening. Neurons form the fastest-rising segment, advancing at an 10.96% CAGR as spinal-cord and Parkinson's trials underline disease-modifying capacity. Hepatocytes remain indispensable for microsomal metabolism studies, while fibroblasts and keratinocytes support tissue-repair research in dermal and musculoskeletal fields.

Manufacturing advances underpin wider distribution of functionally mature cardiomyocytes, including automated maturation protocols that align electrophysiology with adult-like phenotypes. Neuronal lineage protocols benefit from refined patterning factors that yield subtype-specific populations suitable for high-content screening. Availability of curated cell banks via the European Bank for Induced Pluripotent Stem Cells assures reproducibility across laboratories. As chemistries to purge undifferentiated cells improve, lot-release hurdles ease, broadening commercial uptake across the Induced pluripotent stem cells (iPSCs) market.

The Induced Pluripotent Stem Cells Market Report is Segmented by Derived Cell Type (Cardiomyocytes, Neurons, Hepatocytes, Fibroblasts, and More), Application (Drug Discovery and Development, Disease Modeling and More), End User (Academic and Research Institutes, Pharmaceutical and Biotechnology Companies and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America controlled 37.13% of 2025 revenue, supported by NIH allocations and an active venture-capital ecosystem. Regional hospitals hosted pivotal first-in-human Parkinson's and cardiomyopathy trials, demonstrating translational leadership. The FDA's progressive guidance on alternative methods accelerated uptake of in vitro panels, deepening domestic demand. Despite this, high labor and facility costs prompt firms to outsource certain manufacturing steps to lower-cost jurisdictions.

Asia-Pacific is projected to expand at a 12.14% CAGR to 2031, buoyed by Japan's fast-track approvals and significant sovereign funding. China deploys provincial subsidies for GMP plant construction, while South Korea leverages electronics-grade automation expertise to scale closed-system bioreactors. The Induced pluripotent stem cells market has thus seen cross-border alliances where North American developers license clinical candidates to Japanese partners for rapid path-to-market access.

Europe remains a mature but cautious participant. The European Medicines Agency has issued detailed advanced-therapy guidelines that safeguard patient safety yet prolong dossier preparation. Harmonized test-method consortia, backed by the European Bank for Induced Pluripotent Stem Cells, maintain scientific leadership. However, constrained reimbursement landscapes hinder broad clinical adoption, compelling firms to prioritize proof-of-concept studies.

Emerging regions-including the Middle East, Africa and South America-display pockets of interest, particularly in ophthalmology, but infrastructural gaps and nascent regulation limit immediate commercial scale within the Induced pluripotent stem cells (iPSCs) market.