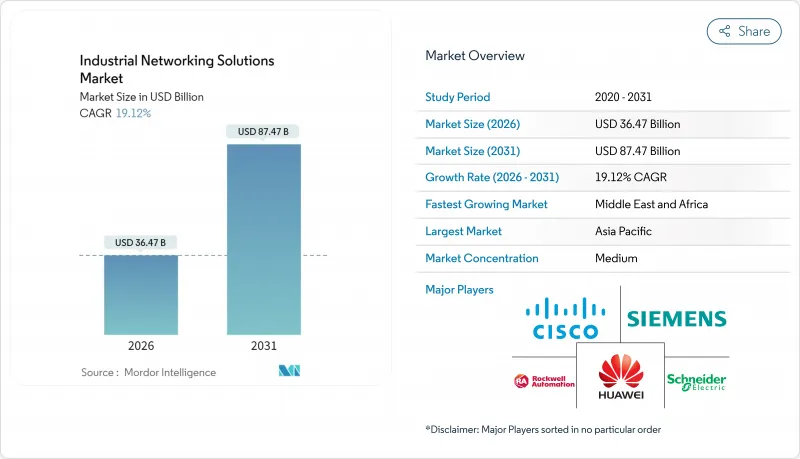

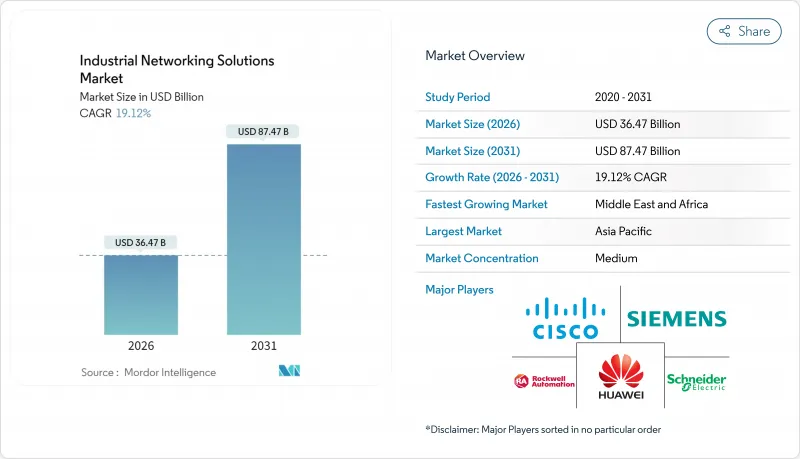

산업용 네트워크 솔루션 시장의 규모는 2026년에는 364억 7,000만 달러로 추정되고 있으며, 2025년 306억 1,000만 달러에서 성장할 전망입니다.

2031년에는 874억 7,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 19.12%로 확대될 전망입니다.

이러한 급성장은 운영 기술 자산과 기업 IT 네트워크의 급속한 융합을 반영하며 자동화가 진행되는 생산 환경 전체에서 실시간 가시성을 실현하고 있습니다. 레거시 필드 버스에서 이더넷 기반 생산으로의 전환은 수요를 더욱 확대하고 있으며 자율 설비를 위한 서브밀리초 수준의 지연 목표를 달성하고 있습니다. 프라이빗 5G와 엣지 AI의 조합은 예지보전을 통해 중공업 분야의 총 소유 비용을 최대 30% 절감하고 있습니다. 정부에 의한 스마트 제조 촉진책도 뒷받침하고 있으며 중국에서만 2024년에 28억 달러를 산업용 네트워크의 업그레이드에 투입했습니다. 이러한 요인들이 결합되어 산업용 네트워크 솔루션 시장은 구조적으로 높은 성장 궤도를 유지하고 있습니다.

공장이 1Gbps를 넘는 머신 비전 워크로드에 대응하기 위해 근대화를 진행하는 가운데, 신규 제조 네트워크 도입의 73%를 이더넷이 차지하게 되었습니다(2020년은 45%). BMW의 스파르탄버그 공장에서는 비전 구동형 품질 검사의 가동률 99.9%를 확보하기 위한 사설 5G 그리드를 운용하고 있습니다. 그러나 중견기업은 라인에 250만 달러의 비용이 발생하기 때문에 광범위한 도입이 지연되고 있습니다.

제조업의 SD-WAN 도입은 2024년 340% 급증했으며 이는 기업 보안 정책을 확정적인 현장 트래픽에 적용하기 때문입니다. 현대차 계열사인 현대오토에버는 47개 거점에서 네트워크 관리비를 60% 절감하고 용도 성능을 35% 향상시켰습니다. 기존의 VLAN 세분화는 자율 이동 로봇에 필요한 민첩성이 부족하기 때문에 OT 대응형 SD-WAN이 표준화되고 있습니다.

제조업체의 약 78%가 OT 사이버 인재를 확보하지 못하여 융합 계획이 지연되고 있습니다. 2024년에는 OT에 대한 사이버 침해사고가 87% 증가하여 레거시 시스템의 취약성이 노출되었습니다. 시스코와 로크웰의 'Digital Skills for Industry' 이니셔티브는 APAC 지역 전문가 100,000명을 육성하여 이러한 병목 현상을 해결하기 위해 노력하고 있습니다.

2025년 하드웨어는 수익의 60.35%를 차지하였으며 가혹한 환경을 위한 산업용 네트워크 솔루션 시장이 견고한 스위치, 라우터 및 액세스 포인트에 의존하고 있음을 확인했습니다. 프리미엄 팬리스 스위치는 기업용 가격의 3배로 제공되는 경우가 많으며 지속적인 고온과 진동에 견딜 수 있습니다. 그러나 소프트웨어 및 서비스는 CAGR 21.95%로 확대되었으며 이는 AI 구동 네트워크 모니터링 및 구독 모델로의 결정적인 전환을 보여줍니다. Siemens의 SIRIUS 3RC7 모듈은 제어 계층에 소프트웨어 정의 네트워크를 통합하여 하드웨어와 소프트웨어의 융합을 실증합니다. 그리고 기업이 사이버 강화와 24시간 365일 감시를 외부에 위탁한 결과, 매니지드 서비스 제공업체는 2024년에 45%의 연간 성장을 기록했습니다.

유선 이더넷은 결정론적 제어 요건과 이더넷 APL의 1,000m에 이르는 본질안전 거리로 2025년에 67.55%의 점유율을 달성했습니다. 프라이빗 5G가 자율형 로봇의 제약을 해소하고 공장의 재구성을 가속화하는 가운데, 무선 기술은 25.1%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 도요타의 자재 운반용 5G 도입은 99.5%의 신뢰성을 달성하여 구리선에 비해 설치 예산을 60% 절감했습니다. 텍사스 인스트루먼트의 초저전력 모듈은 에너지 소비를 90% 절감하여 배터리 구동 센서의 경제성을 강화하고 있습니다.

아시아태평양은 중국의 정책지원에 의한 디지털화와 일본의 고처리량 전자기기 제조 에코시스템에 견인되어 2025년 점유율 34.55%로 산업용 네트워크 솔루션 시장을 계속 견인하고 있습니다. 인도의 'Make in India'와 ASEAN의 'Industry4WRD' 프로그램에 의한 스마트 공장 도입의 확대에 따라 이 지역의 성장은 견조할 전망입니다. 북미는 성숙한 도입지역으로 이어져 안전한 OT-IT 통합을 지원하는 미국 연방 정부의 8억 달러 규모의 보조금에 의해 지원되고 있습니다. 유럽은 엄격한 사이버 탄력 지침과 독일 중소기업을 위한 12억 유로 기금의 혜택을 받아 광범위한 네트워크 현대화를 촉진하고 있습니다. 중동 및 아프리카는 규모가 작지만, 22.95%라는 가장 높은 CAGR을 나타내고 있습니다. 이는 걸프 지역의 석유 대기업이 부식성이 강한 사막과 해양 플랫폼에서 드릴링 설비의 운영에 개인 5G를 도입하고 있기 때문입니다. 라틴아메리카의 기회는 광업 및 재생에너지의 확대에 달려 있으며, 이는 내결함성이 높은 광섬유 이더넷(EoF) 토폴로지를 요구합니다.

Industrial networking solutions market size in 2026 is estimated at USD 36.47 billion, growing from 2025 value of USD 30.61 billion with 2031 projections showing USD 87.47 billion, growing at 19.12% CAGR over 2026-2031.

The surge reflects rapid convergence of operational-technology assets with enterprise IT networks, creating real-time visibility across increasingly automated production environments. Demand is amplified by a shift from legacy fieldbus to Ethernet-based factory floors that meets sub-millisecond latency targets for autonomous equipment. Private 5G in combination with edge AI is lowering total cost of ownership by up to 30% for heavy industries through predictive maintenance. Government smart-manufacturing stimulus is another catalyst: China alone routed USD 2.8 billion of 2024 funds into industrial networking upgrades. Together, these forces underpin a structurally high-growth trajectory for the Industrial networking solutions market.

Ethernet now powers 73% of new manufacturing network installs, up from 45% in 2020, as factories modernize for machine-vision workloads exceeding 1 Gbps. BMW's Spartanburg plant runs a private 5G grid that secures 99.9% uptime for vision-driven quality checks. Yet mid-size firms still face USD 2.5 million line-level retrofit costs that slow broad adoption.

SD-WAN deployments in manufacturing jumped 340% in 2024 as enterprises exported enterprise-security policies to deterministic shop-floor traffic. Hyundai AutoEver cut 60% in network management expense across 47 sites while boosting application performance 35%. Traditional VLAN segmentation lacks the agility required for autonomous mobile robots, so OT-aware SD-WAN is becoming standard.

Some 78% of manufacturers cannot find OT-cyber talent, slowing convergence plans. OT-oriented cyber incidents rose 87% in 2024, exposing legacy weaknesses. Cisco and Rockwell's Digital Skills for Industry initiative aims to train 100,000 APAC professionals to ease the bottleneck.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware commanded 60.35% revenue in 2025, reinforcing the Industrial networking solutions market's dependence on rugged switches, routers, and access points for harsh sites. Premium fanless switches often list at triple enterprise prices, supporting sustained temperatures and vibration. However, software and services are scaling at 21.95% CAGR, signaling a decisive pivot toward AI-driven network monitoring and subscription models. Siemens' SIRIUS 3RC7 module embeds software-defined networking at the control layer, evidencing hardware-software convergence. Managed-service providers booked 45% annual growth in 2024 as firms outsourced cyber-hardening and 24X7 monitoring.

Wired Ethernet secured 67.55% share in 2025 owing to deterministic control requirements and Ethernet-APL's 1,000-m intrinsic-safety reach. Wireless is rising at a 25.1% CAGR as private 5G untethers autonomous robots and accelerates plant re-configuration. Toyota's material-handling 5G rollout clocked 99.5% reliability while slicing install budgets 60% versus copper. Ultra-low-power modules from Texas Instruments now consume 90% less energy, strengthening battery-powered sensor economics.

The Industrial Networking Solutions Market Report is Segmented by Component (Hardware, Software and Services), Type of Connectivity (Wired, Wireless), Deployment Type (On-Premises, Cloud), End-User Industry (Automotive, Financial Services, Manufacturing, Telecommunications, Logistics and Transportation, Mining, Oil and Gas, Energy and Utilities), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific continues to anchor the Industrial networking solutions market with 34.55% 2025 share, propelled by China's policy-backed digitalization and Japan's high-throughput electronics manufacturing ecosystems. The region's growth outlook remains compelling as India and ASEAN economies scale smart-factory rollouts under Make-in-India and Industry4WRD programs. North America follows as a mature adopter, sustained by USD 800 million of US federal grants that subsidize secure OT-IT upgrades. Europe benefits from stringent cyber-resilience directives and Germany's EUR 1.2 billion SME fund, fostering broad-based network modernization. The Middle East & Africa region, though smaller, showcases the highest 22.95% CAGR, with Gulf oil majors installing private 5G to operate drilling assets in corrosive deserts and offshore platforms. Latin America's opportunity hinges on mining and renewable-energy build-outs that demand resilient Ethernet-over-fiber topologies.