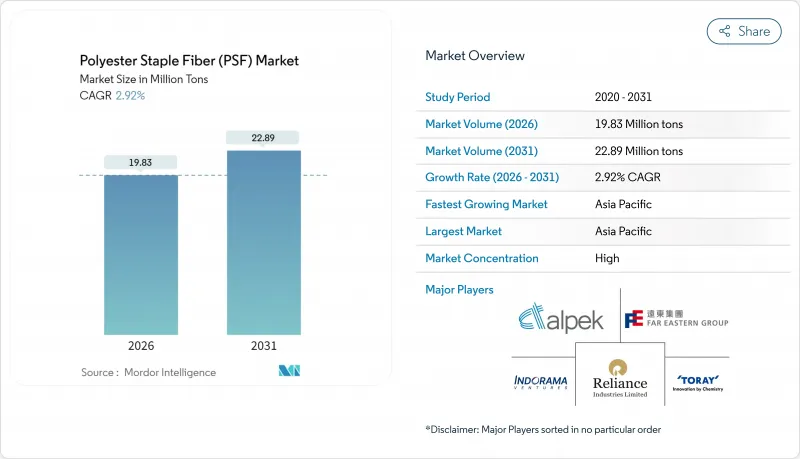

폴리에스테르 단섬유(PSF) 시장은 2025년 1,927만 톤으로 평가되었으며, 2026년 1,983만 톤에서 2031년까지 2,289만 톤에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 2.92%로 전망됩니다.

이 꾸준한 증가는 의류, 가정용 가구, 부직포 위생 제품, 자동차용 방음 부품, 그리고 확대하는 기술 응용 분야에서 소재의 확대 동향을 반영합니다. 비용 효율적인 합성 섬유에 대한 수요가 증가하고, 면으로부터의 구조적 전환, 폐루프 재활용에 대한 투자가 원유와 연동된 원료 비용과 무역 장벽이 변동 요인이 되는 가운데에서도 시장의 회복력을 강화하고 있습니다. 재활용 등급에 대한 경쟁은 치열해지고 있으며, 이는 세계 패션 소매업체, 자동차 제조업체, 위생용품 제조업체가 지속가능성에 대한 투자를 다운스트림 섬유 공급 계약으로 이동시키고 있기 때문입니다. 규모, 화학적 혁신, 추적 가능한 원료 공급원을 결합할 수 있는 생산자는 향후 10년간 이익률을 강화할 수 있는 입장에 있습니다.

소비자 모니터링 강화와 유럽의 새로운 디지털 제품 여권 제도는 세계 소매업체가 버진 폴리에스테르를 섬유 재활용 대체품으로 대체하는 것을 요구하고 있습니다. H&M은 폐쇄형 폴리머 재생 기술을 갖춘 Syre사에 6억 달러를 투자하여 페트병 원료로부터 영구적인 전환을 보였습니다. Shein은 자체 탈중합 공정을 도입하여 연간 3,000톤에 달하는 파일럿 생산량에 따라 제휴 공장에 대한 라이선싱을 계획하고 있습니다. 각 브랜드는 다개년 구매 계약을 체결했으며, 이로 인해 고품질 재생 단섬유 공급이 축소되어 유럽과 아시아의 선진적인 화학적 재활용 거점 확대가 촉진되고 있습니다. 추적 가능성이 필수 요건이 되는 가운데, 관리연속성을 검증할 수 있는 섬유 제조업체는 장기적인 수량 계약과 가격 프리미엄을 획득할 전망이며, 이는 폴리에스테르 단섬유 시장 전체의 성장을 뒷받침하고 있습니다.

면화 가격의 지속적인 변동으로 의류 제조업체는 예측 가능한 비용과 공급을 보장하는 합성 섬유 대체품에 주목하고 있습니다. 미국 농무부(USDA)의 2024년과 25년 전망에서는 세계의 면화 작물 면적이 증가하는 가운데, 미국 방적 공장의 면화 사용량이 수년에 걸쳐 낮은 수준에 있음이 나타났으며, 폴리에스테르 섬유의 상대적인 경제적 안정성이 부각되고 있습니다. 섬유 가공 제조업체는 면과 같은 촉감을 재현하면서 수축에 강한 폴리에스테르 실을 제공하여, 데님 혼방, 애슬레저, 대중용 패션 시장에서의 점유율을 획득하고 있습니다. 이 변화는 인도와 중국에서 가장 두드러지며 직물 제조업체는 니트 티셔츠와 폴로 셔츠 생산 전용 드로우 텍스처 원사 라인을 확대하고 있습니다. 이 구조적인 전환이 기준선 수요를 밀어 올려 2030년까지 폴리에스테르 단섬유 시장을 뒷받침하는 기반이 될 전망입니다.

파라크실렌(PX)과 PTA의 가격은 브렌트 원유의 동향을 반영하여 폴리에스테르 경제를 에너지 시장의 변동에 노출시키고 있습니다. 2024년에는 소위 '가솔린 효과'라는 정제소의 동향으로 북미 PX는 아시아에 비해 프리미엄 가격으로 거래되어 납품 비용의 차이가 확대되었습니다. 중국 석유화공(시노펙)의 강소성의 300만t 규모 PTA 플랜트가 공급압력을 완화하는 한편, 가격 급등에 의해 섬유 제조업체는 재고 관리와 헤징의 조정을 요구받아 마진 축소 시에는 설비 증강을 연기하는 경우가 빈발하고 있습니다. 이러한 변동성으로 인해 폴리에스테르 단섬유 시장의 CAGR은 0.6포인트 하락할 전망입니다.

2025년 시점에서 고형 섬유는 의류, 가정용 섬유, 포장재 등 폭넓은 용도에 힘입어 총 규모의 59.35%를 차지했습니다. 같은 해 중공 등급은 나머지 점유율을 획득했지만, 2031년까지 연률 5.62%의 성장이 전망되고 있어 폴리에스테르 단섬유(PSF) 시장 전체의 성장률을 크게 웃돌 것으로 예측되고 있습니다. 이 실적은 중공 코어의 단열성과 흡습 발산성에 의해 발생하며, 중공 섬유는 운동, 침낭, 퀼트 충전에 필수적입니다.

생산 기술의 진보에 의해 섬유의 붕괴가 줄어들면서 경량화와 높은 복원력의 양립이 가능해졌습니다. 자동차 내장재, 에어 필터, 위생용품의 톱 시트에는 액체의 이동을 촉진하는 친수성 가공을 실시한 2성분 중공 제품이 도입되고 있습니다. 아시아의 부직포 제조업체가 공급하는 13-100gsm의 열 접착 웹은 다양한 용도의 가능성을 보여줍니다. 기술계 고객이 경량화와 에너지 효율을 우선시하는 가운데, 중공 유형은 단열재 및 필터 분야에서 폴리에스테르 단섬유 시장 내 점유율 확대가 전망됩니다.

아시아태평양은 중국의 PTA, MEG 및 섬유의 통합 자산과 인도 및 타밀나두주에서의 니트웨어 산업의 확대에 견인되어, 2025년에는 세계 전체의 72.40%를 차지하는 규모로 시장을 리드했습니다. 지역 전체에 드로우 텍스처 원사와 중공사 라인을 도입함으로써, 아시아태평양은 5.18%의 연평균 복합 성장률(CAGR)로 지역에서 가장 빠른 속도로 성장할 전망입니다. 중국 석유화공(시노펙)의 300만 톤 규모 PTA 플랜트는 업스트림 공급안정성을 높이고, 다운스트림 방적업체의 손익 분기점을 낮추고 있습니다.

인도에서는 합성섬유 수출 확대를 위해 실적연동형 장려제도의 활용을 계속함과 동시에 국내의 도시화가 진행됨에 따라 가정용 섬유제품의 소비가 증가하고 있습니다. 베트남, 인도네시아, 태국에서는 위생용 부직포에 대한 투자가 집중되어 수지 수입을 견인하는 것과 동시에, 스펀본드 공장과 병설된 새로운 단섬유 라인이 개시되고 있습니다. 이러한 동향이 함께 지역의 폴리에스테르 단섬유 시장에 새로운 기세를 가져오고 있습니다.

북미와 유럽의 생산량은 소규모이지만, 자동차, 가구 및 필터 용도로 설계된 섬유는 고부가가치를 실현하고 있습니다. 양 지역의 안티덤핑 소송은 무역의 흐름을 바꾸고 있습니다. 라틴아메리카와 튀르키예는 아시아로부터 수송되는 선적을 수용하고 유럽 생산자는 가격에 민감하지 않은 기술 고객을 대상으로 하고 있습니다. 예측기간 동안 스페인, 프랑스, 미국 동부의 화학적 탈중합 플랜트 등 재활용 인프라에 대한 추가 투자로 버진 원료의 생산량 증가가 둔화되는 반면, 폴리에스테르 단섬유(PSF) 시장에서 재생재의 침투율은 상승할 전망입니다.

The Polyester Staple Fiber (PSF) Market was valued at 19.27 Million tons in 2025 and estimated to grow from 19.83 Million tons in 2026 to reach 22.89 Million tons by 2031, at a CAGR of 2.92% during the forecast period (2026-2031).

This steady rise mirrors the material's expanding footprint in apparel, home furnishings, non-woven hygiene products, automotive noise-control parts, and a growing range of technical uses. Rising demand for cost-effective synthetics, the structural shift away from cotton, and investment in closed-loop recycling are reinforcing the market's resilience even as oil-linked raw-material costs and trade barriers add volatility. Competition is intensifying around recycled grades as global fashion retailers, automakers, and hygiene converters move sustainability spending downstream into fiber supply contracts. Producers able to blend scale, chemistry innovation, and traceable feedstocks are positioned to strengthen margins over the decade.

Mounting consumer scrutiny and new European Digital Product Passports are compelling global retailers to replace virgin polyester with textile-to-textile recycled alternatives. H&M has committed USD 600 million to Syre for closed-loop polymer regeneration, signalling a permanent shift away from bottle-based feedstock. Shein has introduced a proprietary depolymerisation process and intends to license it to partner mills once pilot output scales to 3,000 tons per year. Brands are also locking multi-year offtake agreements, which is tightening supply of high-quality recycled staple and encouraging expansion of advanced chemical recycling hubs in Europe and Asia. As traceability becomes non-negotiable, fiber producers able to validate chain-of-custody data stand to win long-term volume contracts and price premiums, lifting overall growth in the polyester staple fiber market.

Persistent swings in cotton prices have sharpened apparel makers' focus on synthetic alternatives that guarantee predictable cost and supply. USDA's 2024 and 25 outlook shows U.S. mill cotton use at multi-year lows even as global cotton crops rise, underscoring polyester's relative economic security. Fiber converters are capturing share in denim blends, athleisure and mass-market fashion by offering polyester yarns that mimic cotton's hand feel while resisting shrinkage. The shift is most pronounced in India and China where fabric mills are scaling draw-texturised yarn lines dedicated to knitted t-shirt and polo production. This structural migration lifts baseline demand, underpinning the polyester staple fiber market through 2030.

Paraxylene and PTA prices mirror Brent movements, exposing polyester economics to energy market turbulence. In 2024 North American PX traded at premiums to Asia because of refinery dynamics referred to as the "gasoline effect," widening delivered-cost gaps. Although Sinopec's 3 million-ton PTA unit in Jiangsu eases supply pressure, price spikes compel fiber makers to juggle inventory cover and hedging, often deferring capacity upgrades when margins compress. Volatility therefore subtracts an estimated 0.6 percentage points from the polyester staple fiber market CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solid fibers accounted for 59.35% of volume in 2025, underpinned by broad usage in apparel, home textiles and stuffing materials. In the same year hollow grades captured the remaining share yet are predicted to expand 5.62% annually to 2031-well above the overall polyester staple fiber (PSF) market. Performance stems from the thermal-insulation value of hollow cores and their ability to wick moisture, essential for athleisure, sleeping bags and quilt fillings.

Production advances now prevent fiber collapse, allowing higher loft at lower weight. Automotive interior trims, air filters and hygiene topsheets are specifying bi-component hollow products designed with hydrophilic finishes that speed liquid transport. Thermal-bonded webs between 13-100 gsm supplied by Asian non-woven converters demonstrate the breadth of end-use possibilities. As technical customers prioritize weight savings and energy efficiency, hollow variants are set to capture a larger slice of the polyester staple fiber market size for insulation and filtration sub-segments.

The Polyester Staple Fiber (PSF) Market Report Segments the Industry by Product Type (Solid, Hollow), Origin (Virgin, Blended, Recycled), Application (Textile, Home Furnishing, Automotive, Filtration, Construction, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific dominated global volume with a 72.40% share in 2025, propelled by China's integrated PTA, MEG and fiber assets and India's expanding knitwear hub in Tamil Nadu. Region-wide adoption of draw-texturised yarns and hollow variant lines positions APAC to grow at a 5.18% CAGR, the fastest regional rate. Sinopec's megascale 3 million-ton PTA plant improves upstream security, lowering break-even costs for downstream spinners.

India continues to leverage the Performance-Linked Incentive scheme to boost man-made fiber exports while domestic urbanisation lifts household textile consumption. Vietnam, Indonesia, and Thailand attract hygiene-non-woven investments, drawing resin imports and sparking new staple lines co-located with spunbond units. Together, these trends inject momentum into the regional polyester staple fiber market.

North America and Europe account for a smaller volume, yet fibre engineered for automotive, furniture, and filtration draws premium margins. Anti-dumping cases in both regions alter trade flows: Latin America and Turkiye receive redirected Asian shipments while European producers target technical customers less sensitive to price. Over the forecast horizon, incremental investments in recycling infrastructure-such as chemical depolymerisation plants in Spain, France and the eastern United States, will taper virgin volume growth but raise recycled penetration within the polyester staple fiber (PSF) market.