유럽의 RV(레저용 차량) 시장은 2025년의 333억 8,000만 달러에서 2026년에는 370억 7,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 11.08%로 성장을 지속하여 2031년까지 626억 9,000만 달러에 이를 전망입니다.

이 견조한 성장 궤도는 팬데믹 이후의 회복과 유럽의 레저 패턴의 구조적 변화에 따른 부문의 회복력을 반영합니다. 시장 확대는 유럽 의회가 규제면에서의 지원과 특히 2028년까지 4.25톤급 모터홈에 대한 B클래스 면허 적용 확대를 승인한 것에 뒷받침되고 있으며 수백만명의 추가 운전자 확대가 예상됩니다.

유럽의 캠핑 활동은 역대 최대 수준에 이르렀으며, 독일에서는 2024년에 4,290만 건의 캠핑 숙박수를 기록했고, 팬데믹 전인 2019년 대비 19.9% 증가를 달성했습니다. 이 지속적인 국내 관광 증가는 유럽의 레저 선호에 대한 근본적인 변화를 반영하고 있으며, 근거리 중심의 여행은 계절적 필요성에서 선호되는 라이프스타일 선택으로 진화하고 있습니다. 이 동향은 독일에 머무르지 않고, 노르웨이의 캠핑장에서도 숙박자수가 증가해, 전년 대비 대폭적인 성장을 나타내고 있습니다. 캠핑 활동의 활성화가 2025년까지 지속된 점은 특히 캠핑이 독일의 투숙객 수의 대부분을 차지하는 역대 최대 수준에 비해 일시적인 유행 요인이 아니라 구조적 수요임을 시사합니다. 이러한 관광의 재편은 도시 근교의 여행을 가능하게 하는 소형 캠핑카부터 장기 국내 여행을 지원하는 대형 모터홈에 이르기까지 모든 차량 부문에서의 RV 수요에 지속적인 원동력을 가져옵니다.

유럽의 RV 공유 생태계는 빠르게 성숙하고 있습니다. 2025년 4월에 Roadsurfer사가 Avellinia Capital로부터 3,000만 유로의 자금 조달에 성공하였고 특히 차량 수를 8,500대에서 1만대로 확대하는 계획이 이 분야의 성장 가속을 뒷받침하고 있습니다. 이 자금 투입은 개인 간 RV 플랫폼이 초기 신뢰 장벽을 극복하고 사업 규모를 달성했다는 기관 투자자의 인식을 반영합니다. 주목할 점은 플랫폼이 동유럽 시장으로 확대되고 있다는 점입니다. Ruuts는 API 연계를 통해 동유럽 시장을 타겟으로 하고 유럽 주요 지역에서 RV에 대한 접근을 제공함으로써 지금까지 서비스가 미치지 못했던 지역에 대응하고 있습니다. 또한 공유 이코노미가 RV 소유 패턴에 침투하여 이중 시장 효과가 탄생했습니다. 즉, 첫 이용자의 접근을 민주화하는 동시에 개인 소유자에게 이용 기반 수익원을 창출함으로써 기존 소유 모델을 넘은 잠재 시장을 효과적으로 확대하고 있습니다.

유럽의 RV 가격은 급등하고 있으며 시장 세분화 전체에서 저렴한 가격대가 축소되고 있습니다. 이 상승은 밸류체인의 혼란, 섀시 부족, 팬데믹에 의한 수요 증가를 배경으로 한 제조업체의 가격 인상 때문입니다. 대체 가치 상승과 특수 수리 요구에 따른 보험료 증가도 재정적 부담을 더욱 가중시킵니다. 중산층 구매자는 중고차와 렌탈을 선택하는 경향이 강해지는 한편, 젊은 층이나 최초 구매자는 장벽에 직면해 수요가 견조함에도 불구하고 시장의 성장이 제한되고 있습니다. 재고 조정이 이루어지더라도 높은 가격이 지속되는 점이 구조적 비용 상승을 부각시키고 있으며, 접근성을 유지하려면 소득 증가 또는 대체 소유 모델이 필수적입니다.

모터홈은 2025년 시점에서 유럽의 RV(레저용 차량) 시장의 53.72%를 차지하면서 지배적인 지위를 유지했습니다. 이는 유럽 소비자가 외부 의존 없이 종합적인 설비를 제공하는 자립형 이동 생활 솔루션을 선호하는 경향을 반영합니다. 이 부문의 이점은 이동 제약보다 편안함과 편의성을 선호하는 부유층(55-75세)층에 대한 홍보에 기인합니다. 그러나 캠핑카는 2031년까지 연평균 복합 성장률(CAGR) 11.62%라는 가장 높은 성장률을 보일 전망이며, 밴 라이프 문화를 받아들이는 젊은 층과 유연한 워크 트래블 솔루션을 요구하는 도시 전문층에 견인되고 있습니다. 트래블 트레일러와 피프스 휠 트레일러는 소규모이면서도 안정적인 틈새 시장을 차지하며 일상 사용을 위해 별도의 견인 차량을 유지하는 것을 선호하는 소비자들에게 지지를 받고 있습니다. 팝업 캠퍼와 접이식 캠퍼는 엔트리 레벨 부문을 구성하여 가격에 민감한 구매자와 계절 사용자를 끌어들입니다.

규제 환경은 이러한 세분화를 뒷받침하고 있으며, EU의 형식 인증 프레임워크(규정 2018/858)는 안전 기준을 유지하면서 캠핑카 개조를 용이하게 하는 다단계 차량 인증의 명확한 경로를 제공합니다. A클래스 모터홈은 고가격대이지만, 도시 지역의 저배출 구역 규제에 의한 어려움에 휩싸이고 있습니다. 한편, B클래스 캠핑카는 도시 지역에 대한 접근성과 주차 유연성 향상의 이점이 있습니다.

2025년 유럽의 RV(레저용 차량) 시장에서 디젤 내연기관(ICE) 파워트레인은 91.10%의 점유율을 차지하였습니다. 이는 고중량 차량 응용 분야에서 디젤이 가진 우수한 토크 특성과 연료 효율에 대한 부문의 전통적인 의존성을 반영한 결과입니다. 가솔린 내연기관(ICE) 모델은 중량면에서 가솔린 엔진이 유리한 경량 캠핑카 용도를 중심으로 보다 작은 존재감을 유지하고 있습니다. 그러나 배터리형 전기자동차(BEV) 모델은 EU의 배출가스 규제 강화와 충전 인프라 확대를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 36.91%로 급성장할 전망입니다. 하이브리드 전기 솔루션은 과도기적인 위치를 차지하고 항속 거리를 우려하는 소비자를 위한 타협을 제공하는 동시에 도시 지역 접근 시 배출 가스 감소 효과를 제공합니다.

노르웨이는 승용차의 BEV 점유율 96%로 전동화 도입을 선도하고, 이는 상용차나 RV(레저용 차량) 부문에도 파급 효과를 가져오고 있습니다. 제조업체 각사는 전동 솔루션에 거액의 투자를 실시하고 있으며, 트루마사는 보쉬사 전동 솔루션 부문의 Joachim Weckwerth 박사를 제품 개발 책임자로 임명했으며 이는 전기화에 대한 전략적 헌신을 보여줍니다.

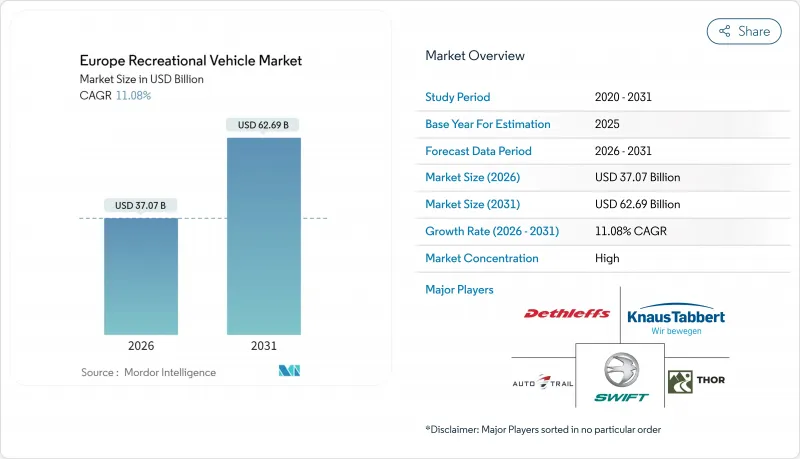

The Europe Recreational Vehicle market is expected to grow from USD 33.38 billion in 2025 to USD 37.07 billion in 2026 and is forecast to reach USD 62.69 billion by 2031 at 11.08% CAGR over 2026-2031.

This robust growth trajectory reflects the sector's resilience following post-pandemic recovery and structural shifts in European leisure patterns. The market's expansion is underpinned by regulatory tailwinds, particularly the EU Parliament's approval of extending B-license eligibility to 4.25-tonne motorhomes by 2028, which will unlock access for millions of additional drivers.

European camping activity has reached unprecedented levels, with Germany recording 42.9 million camping overnight stays in 2024, representing a 19.9% increase compared to 2019 pre-pandemic levels. This sustained elevation in domestic tourism reflects a fundamental shift in European leisure preferences, where proximity-based travel has evolved from pandemic necessity to preferred lifestyle choice. The trend extends beyond Germany, with Norway's camping sites witnessing a rise in guest nights, marking significant year-over-year growth. The persistence of elevated camping activity well into 2025 suggests this represents structural demand rather than temporary pandemic-driven behavior, particularly as camping accounts for most German guest overnight stays compared to historical levels. This tourism reorientation creates sustained tailwinds for RV demand across vehicle segments, from compact campervans enabling urban-adjacent exploration to larger motorhomes supporting extended domestic touring.

The European RV-sharing ecosystem has matured rapidly. The sector's growth acceleration is evidenced by Roadsurfer securing EUR 30 million from Avellinia Capital in April 2025, specifically for fleet expansion from 8,500 to 10,000 vehicles. This capital deployment reflects institutional recognition that peer-to-peer RV platforms have overcome initial trust barriers and achieved operational scale. Notably, platforms are expanding eastward, with Ruuts targeting Eastern European markets through API integrations, providing access to major European RVs, and addressing previously underserved regions. The sharing economy's penetration into RV ownership patterns creates dual market effects: democratizing access for first-time users while generating utilization-based revenue streams for private owners, effectively expanding the addressable market beyond traditional ownership models.

European RV prices have surged, straining affordability across market segments. This increase stems from supply chain disruptions, chassis shortages, and manufacturers leveraging pandemic-driven demand. Rising insurance premiums, driven by higher replacement values and specialized repair needs, add to the financial burden. Middle-market buyers increasingly opt for used vehicles or rentals, while younger and first-time buyers face barriers, limiting market growth despite strong demand. Even with inventory corrections, persistent high prices highlight structural cost inflation, necessitating income growth or alternative ownership models to sustain accessibility.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Motorhomes maintained their dominant position with a 53.72% share of the Europe recreational vehicle market in 2025, reflecting European consumers' preference for self-contained mobile living solutions that provide comprehensive amenities without external dependencies. The segment's leadership stems from its appeal to the affluent 55-75 demographic, prioritizing comfort and convenience over mobility constraints. However, campervans are experiencing the fastest growth at 11.62% CAGR through 2031, driven by younger demographics embracing van life culture and urban professionals seeking flexible work-travel solutions. Travel and fifth-wheel trailers occupy smaller but stable niches, appealing to consumers who prefer to maintain separate towing vehicles for daily use. Pop-up and folding campers represent the entry-level segment, attracting price-sensitive buyers and seasonal users.

The regulatory environment supports this segmentation evolution, with EU type-approval frameworks under Regulation 2018/858 providing clear pathways for multi-stage vehicle approvals that facilitate campervan conversions while maintaining safety standards. Class A motorhomes command premium pricing but face headwinds from urban low-emission zone restrictions, while Class B campervans benefit from improved urban accessibility and parking flexibility.

Diesel ICE powertrains command 91.10% share of the Europe recreational vehicle market in 2025, reflecting the segment's traditional reliance on diesel's superior torque characteristics and fuel efficiency for heavy vehicle applications. Petrol ICE variants maintain a smaller presence, primarily in lighter campervan applications where weight considerations favor gasoline engines. However, battery-electric variants are surging at a 36.91% CAGR through 2031, driven by tightening EU emission regulations and expanding charging infrastructure. Hybrid-electric solutions occupy a transitional position, offering compromise solutions for range-anxious consumers while providing emission benefits for urban access.

Norway leads electric adoption with 96% BEV share in passenger cars, creating spillover effects into commercial and recreational vehicle segments. Manufacturers are investing heavily in electric solutions, with Truma appointing Dr. Joachim Weckwerth from Bosch's Electric Solutions division to lead product development, signaling a strategic commitment to electrification.

The Europe Recreational Vehicle Market Report is Segmented by Type (Towable RVs, Motorhomes), Propulsion and Fuel (Diesel ICE, Petrol ICE, Hybrid-Electric, Battery-Electric), Ownership Model (Private Owners, Rental and Sharing Fleets), Sales Channel (OEM-Franchised Dealers, and More), and Country (Germany, United Kingdom, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).