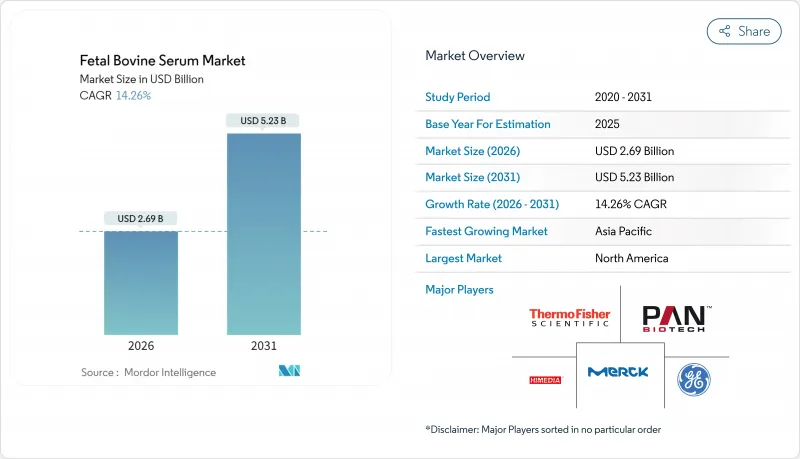

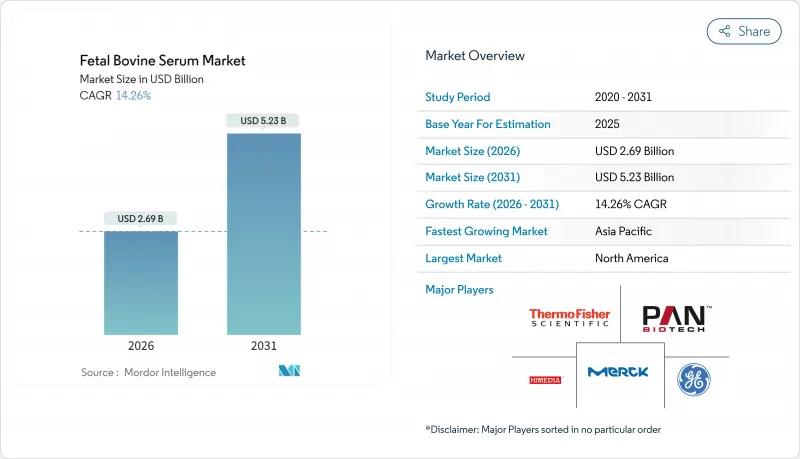

소 태아 혈청 시장은 2025년에 23억 5,000만 달러로 평가되었고, 2026년 26억 9,000만 달러에서 2031년까지 52억 3,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 14.26%로 전망됩니다.

미국의 소 개체수 축소, 쇠고기 가격 상승, 규제 감시 강화에 의한 원료 공급의 압박이 고품질 FBS 등급과 무혈청 대체품의 병행 투자를 촉진하고 있습니다. 바이오 의약품 제조업체는 복수 공급자의 선정과 재고 확보를 진행하는 동시에, 수탁 제조 기관(CMO)은 즉용형 혈청 포맷에 적합한 일회용 바이오리액터 플랫폼을 활용하고 있습니다. 개발기간의 단축이 진행되고 있음에도, 연속 제조 라인에서는 배치당 FBS 소비량이 증가하고 있어 수요는 견조하게 추이할 전망입니다. 한편, 히브리 대학의 연구에서는 세포 증식 성능이 동등한 유청 단백질 보충제와 리터당 USD 1 미만의 무혈청 배지의 효능이 입증되었으며 이는 장기적인 구조 변화를 시사합니다.

2024년 치료제 개발 기업은 생산 능력 확충에 주력했으며 써모피셔사이언티픽사가 바이오프로세싱 인프라에 20억 달러를 투입한 것이 그 전형적인 예입니다. 임상 개발 스케줄의 가속화로 인해 생산자는 연속 바이오리액터를 선호하는 경향이 있으며 배치 수는 감소하지만 생산 로트당 FBS 수요는 높일 수 있습니다. 안전시험 요건이 강화됨에 따라 일부 시장에서는 프리미엄급 병이 500mL당 3,200달러에 달했습니다. 여러 공급업체의 조달 전략은 조달 위험을 분산시키지만 판매자 시장을 정착시키고 있습니다. 이러한 압력은 비용 절감과 공정 안정성이 상업 제조업체에 촉구되는 무혈청 배지에 대한 투자를 동시에 촉진했습니다. 종합적으로 볼 때, 유력한 대안의 존재에도 불구하고 성장 엔진은 소 태아 혈청 시장의 확장을 유지할 전망입니다.

줄기세포 대응 로트나 감마선 조사 로트는 동물 유래 성분에 관한 FDA의 지침 초안의 대상이 되는 후기 임상시험 단계로 이행하는 파이프라인 자산으로서 주목을 받고 있습니다. 추적성 및 바이러스 안전성 테스트가 입찰 사양에 명시되어 소규모 공급업체의 진입 장벽이 증가하고 있습니다. 한편, 학술연구기관에서는 1리터당 0.63달러로 1,300억개의 세포를 유지할 수 있는 비동물성 배지의 실현이 입증되어 비용 곡선에 혁신적인 우위성을 가져오고 있습니다. 개발 기업은 두 가지 현실에 대응해야 합니다. 기존 프로그램은 비교 시험을 피하기 위해 검증된 FBS 프로토콜을 유지하는 반면, 새로운 양식은 인간에 대한 최초 투여 시부터 무혈청 플랫폼을 추구합니다. 이에 따라 공급업체는 재조합 성장 인자 칵테일을 포함한 제품 포트폴리오를 확충하고 있으며, 어느 경로가 주류가 되어도 수요에 대응할 수 있습니다.

2024년 쇠고기 가격 상승은 혈청 비용에 직접 영향을 주었으며 일부 제조업체에서는 전년 대비 40%의 가격 상승이 보고되어 임상 프로그램 예산을 압박했습니다. 그리고 도축률과의 근본적인 연동성에 의해 FBS 공급은 바이오의약품 기업의 관리를 벗어났으며, 기업은 재고 버퍼의 확대와 운전 자금의 구속을 요구받고 있습니다. 급격한 비용 변동은 특히 중소 바이오테크 기업에서 원가 예측을 왜곡하고 이익률을 감소시킵니다. 공급업체는 소 선물 가격과 연동한 장기 계약으로 변동을 평준화하려고 하지만, 스팟 가격이 급등하면 계약 상대의 준수가 어려워질 수 있습니다. 이러한 변동성은 대체 배지에 의한 위험 완화를 가속화하고 소 태아 혈청 시장의 장기적인 성장 여지를 제한합니다.

2025년에 해당 부문 시장의 규모는 8억 9,000만 달러에 이르렀고, 불멸화 세포주 전반에 적용 가능한 표준 및 일반 FBS가 37.86%의 점유율을 유지했습니다. 줄기세포 대응 FBS는 기반 규모가 작지만 엄격한 바이러스 안전성 클리어런스를 필요로 하는 후기 단계의 자가이식 및 동종이식 치료 파이프라인의 진전에 의해 CAGR 7.03%의 성장할 것으로 전망됩니다. 범용품은 이익률 감소에 직면하는 반면, 엑소좀 제거품, 감마선 조사품, 크로마토그래피 정제품은 두 자릿대의 가격 프리미엄을 달성합니다. 공급업체는 추적성 증명서와 로트 고유의 성장 촉진 시험을 통해 차별화를 도모하고 고객 충성도를 확립하고 있습니다. 경쟁업체 간의 적대관계는 수량에서 사양의 강화로 이행하여 소 태아 혈청 시장의 계층구조를 굳히고 있습니다.

틈새 등급의 상용화도 제품 구성을 개선합니다. 엑소좀 제거 FBS는 급성장하여 세포외소포체 분야를 뒷받침하고, 낮은 IgG 로트는 항체 제조에서 다운스트림 단계의 분석 간섭을 방지합니다. 투석 처리 제품은 정밀한 영양 관리가 필요한 대사 플럭스 연구를 대상으로 하며, 열불활성 혈청은 보체 감수성 분석에 필수적입니다. 이러한 계층 구조는 카탈로그의 폭을 넓혀 기존 기업이 단일 제품 상품화를 극복하고 있습니다. 첨단 치료법이 확대됨에 따라 프리미엄 등급은 광범위한 소 태아 혈청 시장 규모의 성장 궤도를 뛰어넘을 전망입니다.

소 태아 혈청 시장의 보고서는 제품 유형(표준 및 일반 FBS, 열불활성 FBS 등), 용도(바이오의약품 제조, 백신 제조 등), 최종 사용자(생명공학 및 제약기업, 학술기관 및 연구기관, CMO 및 CRO 등), 지역(북미, 유럽 등)별로 분석했습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

북미는 2025년 매출의 36.88%를 차지했으며, 성숙한 생물 제제 부문과 견조한 자금 조달 생태계를 기반으로 성장했습니다. 미국 규제 당국의 FBS 시험에 대한 숙련도에 따라 인증주기는 단축되었지만 국내 공급 제약으로 호주와 라틴아메리카로부터의 수입 의존도가 높아지고 있습니다. 캐나다는 정부 보조금을 활용하여 세포 치료 인큐베이터를 확대하고 있는 반면, 멕시코의 비용 효율적인 시설은 2차 조달 프로그램을 이끌고 있습니다. 가격 감응도가 높아짐에도 불구하고, 이 지역 전체는 수요의 중심지 역할을 유지하고 있습니다.

유럽은 가치면에서 약간의 차이로 뒤를 잇고 있으며 엄격한 동물 복지법과 첨단 약물감시 체제가 특징입니다. 독일과 영국이 산업 도입을 견인하고 프랑스와 이탈리아의 학술 소비가 뒷받침합니다. EU 규제는 도축장까지의 추적성을 의무화하고 비용 상승을 초래하는 한편, 고품질 생산자를 지원합니다. 동물 유래 성분을 사용하지 않는 프로토콜로의 전환은 생산량을 억제하는 반면 평균 판매 가격을 밀어 올려 소 태아 혈청 시장의 지역 수익을 안정화시키고 있습니다.

아시아태평양은 예측 CAGR 7.05%로 확대의 최전선에 있는 지역입니다. 중국은 생물 제제 제조를 동남아시아의 위성 거점에 집약하여 새로운 수입 경로를 창출하고 있습니다. 인도는 진단약 붐이 안정된 상품 수요를 낳는 한편, 일본과 한국은 재생 의료용 고사양 혈청을 중시하고 있습니다. 호주는 뛰어난 축산 기술을 가지고 있으며 지역 및 세계 구매자 모두에게 공급함으로써 북미의 공급 부족을 보완하고 있습니다. ICH 가이드라인에 따른 규제 간의 조화는 시장 진입을 가속화하고 아시아태평양은 소 태아 혈청 시장의 규모에서 특히 큰 성장이 예상되고 있습니다.

The fetal bovine serum market was valued at USD 2.35 billion in 2025 and estimated to grow from USD 2.69 billion in 2026 to reach USD 5.23 billion by 2031, at a CAGR of 14.26% during the forecast period (2026-2031).

Tight raw-material supply caused by the U.S. cattle-herd contraction, record beef prices, and rising regulatory scrutiny are driving parallel investment in premium FBS grades and serum-free alternatives. Biopharmaceutical manufacturers are qualifying multiple suppliers and stockpiling inventory, while CMOs leverage single-use bioreactor platforms that favor ready-to-use serum formats. Continuous manufacturing lines are consuming more FBS per batch even as development timelines shorten, keeping demand resilient. Concurrently, research at Hebrew University validated whey-protein supplements and sub-USD 1 per liter serum-free media that match cell-growth performance, signaling a long-term structural shift.

Therapeutics developers doubled down on capacity additions in 2024, typified by Thermo Fisher Scientific's USD 2 billion outlay for bioprocessing infrastructure. Accelerated clinical timelines pushed producers to favor continuous bioreactors, which can raise FBS demand per production run even as batch numbers fall. Premium-grade bottles reached USD 3,200 per 500 mL in some markets amid heightened safety testing requirements. Multiple-vendor qualification strategies spread procurement risk but have entrenched a seller's market. These pressures simultaneously catalyzed investment in serum-free media, where cost savings and process consistency appeal to commercial manufacturers. Altogether, the growth engine keeps the fetal bovine serum market expanding despite compelling alternatives.

Stem-cell-qualified and gamma-irradiated lots gained traction as pipeline assets moved into late-stage trials subject to FDA draft guidance on animal-derived components. Traceability and viral safety testing now feature in tender specifications, raising barriers for small suppliers. Concurrently, animal-component-free media capable of sustaining 130 billion cells per liter at USD 0.63 per liter were demonstrated in academic labs, offering a disruptive cost-curve advantage. Developers confront a dual-track reality: legacy programs stay with validated FBS protocols to avoid comparability studies, while new modalities pursue serum-free platforms from first-in-human dosing. Suppliers are therefore broadening portfolios to include recombinant growth factor cocktails, positioning for demand whichever path wins out.

Record beef prices in 2024 fed directly into serum costs, with some manufacturers reporting 40% year-over-year increases that strained budgets for clinical programs. The fundamental linkage to slaughter rates places FBS supply outside biopharma control, compelling firms to expand inventory buffers and tie up working capital. Sudden cost swings distort cost-of-goods forecasts and erode margins, particularly for smaller biotech entities. Suppliers attempt to smooth fluctuations via long-term contracts indexed to cattle futures, but counter-party adherence can falter when spot prices soar. Such volatility accelerates risk mitigation through alternative media, capping long-run upside for the fetal bovine serum market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The segment generated USD 0.89 billion in 2025, with Standard/Regular FBS retaining 37.86% share due to universal applicability across immortalized lines. Stem-Cell-Qualified FBS, though a smaller base, is forecast to post a 7.03% CAGR, propelled by late-stage autologous and allogeneic therapy pipelines that require stringent viral safety clearance. Commodity lots face margin compression, whereas exosome-depleted, gamma-irradiated, and chromatographically purified variants enjoy double-digit pricing premiums. Suppliers differentiate via traceability certificates and lot-specific growth-promotion assays, anchoring customer loyalty. Competitive rivalry has shifted from volume to specification depth, solidifying a tiered structure in the fetal bovine serum market.

Commercialization of niche grades also improves mix; exosome-depleted FBS supports the burgeoning extracellular-vesicle field, and low-IgG lots prevent downstream analytical interference in antibody manufacturing. Dialyzed preparations target metabolic-flux studies needing precise nutrient control, and heat-inactivated serum remains essential for complement-sensitive assays. These layers create a catalog breadth that shields incumbents from single-product commoditization. As advanced therapies scale, premium grades are poised to outpace the broader fetal bovine serum market size growth trajectory.

The Fetal Bovine Serum Report is Segmented by Product Type (Standard/Regular FBS, Heat-Inactivated FBS, and More), Application (Biopharmaceutical Production, Vaccine Manufacturing, and More), End User (Biotechnology & Pharmaceutical Companies, Academic & Research Institutes, Cmos & CROs, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 36.88% of 2025 revenue, anchored by its mature biologics sector and robust funding ecosystem. U.S. regulatory familiarity with FBS testing enables shorter qualification cycles, yet domestic supply constraints intensify import reliance from Australia and Latin America. Canada leverages government grants to expand cell-therapy incubators, whereas Mexico's cost-efficient facilities attract secondary sourcing programs. Collectively, the region remains the demand center even as price sensitivity rises.

Europe follows closely in value terms, characterized by stringent animal-welfare statutes and sophisticated pharmacovigilance regimes. Germany and the United Kingdom drive industrial uptake, complemented by France and Italy's academic consumption. EU regulations mandate traceability back to the slaughterhouse, pushing costs higher but favoring premium producers. Ongoing transition toward animal-component-free protocols tempers volume but raises average selling price, stabilizing regional returns for the fetal bovine serum market.

Asia-Pacific is the expansion frontier at a forecast 7.05% CAGR. China channels biologics manufacturing to Southeast Asian satellites, creating fresh import corridors. India's diagnostics boom adds steady commodity demand, while Japan and South Korea emphasize high-specification serum for regenerative medicine. Australia, with strong cattle husbandry practices, supplies both regional and global buyers, offsetting North American shortages. Regulatory harmonization under ICH guidelines accelerates market access, positioning Asia-Pacific for outsized growth within the fetal bovine serum market size landscape.