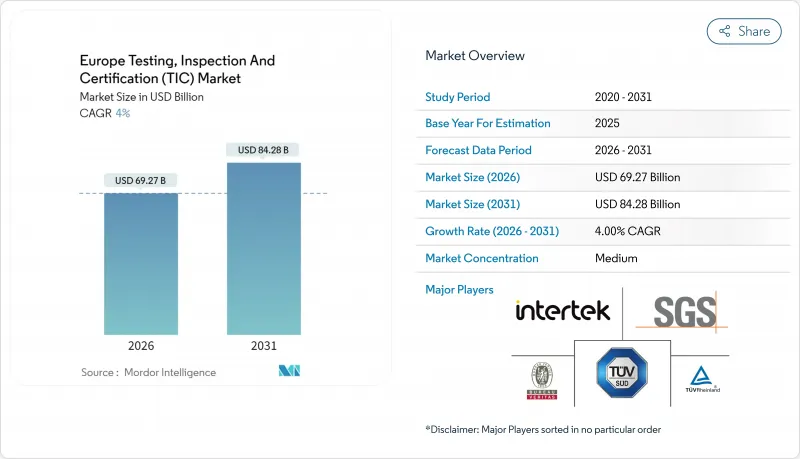

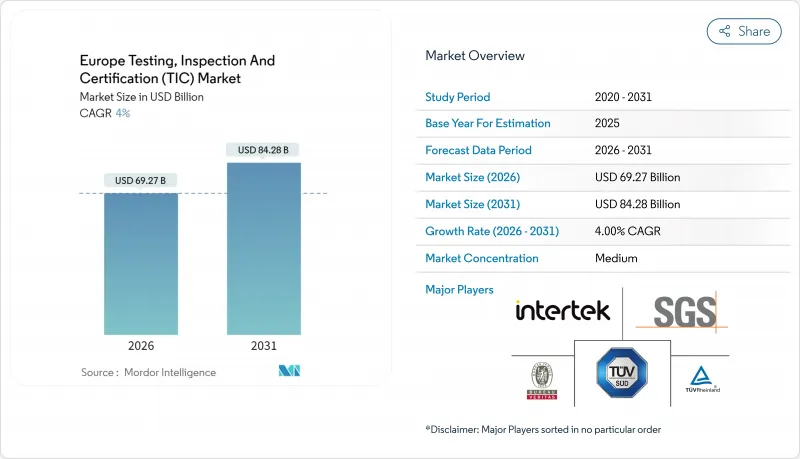

유럽의 TIC(시험, 검사 및 인증) 시장은 2025년에 666억 1,000만 달러로 평가되었고, 2026년 692억 7,000만 달러에서 2031년까지 842억 8,000만 달러에 이를 것으로 예측되고 있습니다.

예측기간(2026-2031년)의 CAGR은 4.00%로 예상됩니다.

시장의 구조적 성장은 EU 디지털 비즈니스 탄력성 법, 기업 지속가능성 보고 지침, 사이버 탄력성 법에 근거한 규제 요건 증가에 의해 뒷받침됩니다. 이 모든 법령은 금융, 지속가능성 및 연결 제품 분야에서 제3자가 입증 가능한 보증을 의무화합니다. 신재생에너지의 급속한 확대, 검증업무의 외부위탁으로의 지속적인 이행, AI를 활용한 검사기술의 급속한 대두는 회원국 간 경제 정세에 편차가 있는 가운데 성장 전망을 더욱 강화하고 있습니다. 한편 유럽의 TIC(시험, 검사 및 인증) 시장은 사이버 보안상의 제약에 의해 원격 검사의 전면 도입이 억제되는 상황에 있으며, 중소기업에서의 비용 압력에 의해 높은 가격 감응도가 유지되고 있습니다. SGS와 뷰로베리타스의 합병 중단 사례로 대표되는 통합의 움직임은 세계에서 가장 엄격한 비즈니스 서비스 분야 중 하나에서 규모 확대의 전략적 가치와 복잡성의 양면을 돋보이게 합니다.

DORA(데이터보호책임자지침), CSRD(기후관련재무정보공개지침), 사이버 레질리언스법이 2024년에 시행되었으며, 금융기업, 대기업, 연결제품업체는 각각 ICT 리스크, 지속가능성 공시, 제품 사이버보안에 대해 다층적인 제3자 보증 확보를 의무화하였습니다. 컴플라이언스 예산의 약 30%가 외부 감사에 할당되며, 사이버, ESG 및 운영 탄력성 영역을 단일 계약으로 커버할 수 있는 엔드 투 엔드 제공업체에게 새로운 수익원이 되었습니다. 이러한 분야의 수요 집계는 특히 통합 디지털 감사 플랫폼을 보유한 공급자에게 크로스셀링의 가능성을 확대합니다. 유럽의 TIC(시험, 검사 및 인증) 시장은 시장 진입이 법적으로 의무화되고 있는 몇 안되는 서비스 분야의 하나이기 때문에 광범위한 비용 억제의 움직임 속에서도 지출은 비교적 탄력성이 낮은 상태가 계속되고 있습니다. 따라서 중기 성장은 감독 당국이 수용할 수 있는 데이터 무결성 기준을 확보하면서 다분야에 걸친 전문 지식을 확대하는 공급자의 능력에 달려 있습니다.

REPowerEU 계획에 근거한 풍력 및 태양광 발전의 급속한 건설 확대에 따라, 터빈 건전성, 출력 특성 곡선 성능, 계통 연계 안전성의 철저한 검증이 요구되고 있으며, 해양 분류 및 환경 영향 평가 분야의 TIC 전문 기관에 대해 고수익 기회가 태어나고 있습니다. 프로젝트 개발회사는 각국 당국이 엄격한 기술기준을 유지하면서 허가기한을 단축하도록 하여 인증 병목현상에 직면하고 있으며, 깊은 전문지식을 가진 인증시험소의 전략적 가치가 높아지고 있습니다. 북해의 해상풍력발전 확대만으로도 복잡한 해저케이블 시험이나 가혹한 환경하에서의 재료인증이 필요하기 때문에 고액의 비용이 발생합니다. 신재생에너지 자산 소유자가 노후화 대책으로 AI 탑재 드론 감시를 도입하면서 하드웨어와 데이터 분석 알고리즘을 모두 검증할 수 있는 인증기관이 경쟁 우위를 획득하고 있습니다. 유럽의 TIC(시험, 검사 및 인증) 시장은 유럽 대륙의 넷 제로 달성 스케줄과 밀접하게 연동한 장기적인 성장 엔진을 확보하고 있습니다.

인증 비용은 중소기업의 수익의 2-3%에 상당하는 경우가 많으며, 소규모 기업은 완전한 컴플라이언스 달성을 연기해야만 하고, 경우에 따라서는 수출 기회를 포기해야 하는 압력에 직면하고 있습니다. 상호 승인 협정이 있음에도 불구하고 여러 국가 인증 기관이 중복 서류 제출을 요구하여 관리 부담을 높이고 있습니다. 디지털 감사 포털이 거래 비용을 줄이면서 ISO 인증 능력을 유지하는 경제성은 여전히 대규모 서비스 그룹에 유리하며, 특히 구매력이 낮은 동유럽에서 유럽의 TIC(시험, 검사 및 인증) 시장의 광범위한 침투를 저해하는 접근 격차를 초래하고 있습니다.

시험 서비스는 2025년 시점에서 유럽의 TIC(시험, 검사 및 인증) 시장의 54.20%에 해당하는 360억 9,000만 달러를 차지했습니다. 이는 첨단 전자기기, 의료기기, 자동차 부품이 모두 상품화 전에 다분야에 걸친 성능 평가를 필요로 하기 때문입니다. 클라우드 기반 테스트 데이터 포털과 같은 디지털 워크플로는 납기를 단축하고 고객의 투명성을 높여 조기 도입 기업의 경쟁 우위를 강화하고 있습니다. 인증서비스는 현재 규모가 작지만, CSRD(기업 지속가능성 보고지침)에 근거한 보증 요건이나 사이버 보안과 사업 지속 및 사회적 책임을 새롭게 커버하는 관리 시스템 규격의 확대에 의해 연률 4.58%의 복합 성장이 전망됩니다. 검사 서비스는 인프라 라이프사이클 관리에서 안정적인 수요를 유지하고 있으며, 특히 정기적인 구조평가가 의무화되고 있는 지역의 제조업 거점에서 중요성을 유지하고 있습니다.

테스트 스케줄링, 실시간 분석 및 인증서 발급을 통합하는 플랫폼은 기존 서비스 분야 간의 경계를 모호하게 만듭니다. 실험실 시험과 현지 및 원격 검사를 단일 계약으로 제공할 수 있는 사업자는 원스톱 컴플라이언스 솔루션을 요구하는 고객의 월렛 점유율을 획득하고 있습니다. 데이터 무결성을 유지하면서 실험실의 처리 능력을 향상시키는 AI 탑재 결함 인식 알고리즘에 대한 투자가 유입되어 유럽의 TIC(시험, 검사 및 인증) 시장에서의 시험의 우위성을 강화하고 있습니다.

2025년 시점에서 유럽의 TIC(시험, 검사 및 인증) 시장 규모의 63.05%를 외부 위탁 검증이 차지했으며, 이는 자본 집약적인 사내 랩으로부터의 결정적인 전환을 반영하고 있습니다. 재료과학의 진보와 안전기준의 진화에 직면하는 항공우주 및 자동차 부문의 제조업체는 생산량에 따른 변동비 모델을 선호합니다. 외부 위탁 서비스는 세계 인증에 대한 즉각적인 접근을 제공하여 수출 시장에서의 출시 기간을 단축하고 규제 위험을 줄입니다.

TIC 기업이 정의한 범위 내에서 컴플라이언스 책임을 부담하는 성과 기반 계약이 확대되고 있으며, 이는 지속적인 수익을 창출하고 지속적인 프로세스 개선을 촉진하고 있습니다. 지적재산상의 우려로 일부 시험활동은 내부에서 계속되지만, 광범위한 아웃소싱 동향은 4.37%의 연평균 복합 성장률(CAGR)을 유지할 것으로 예상되고, 유럽의 TIC(시험, 검사 및 인증) 시장은 장기 계약과 연동한 서비스 계약에 의한 안정된 두 자릿수의 수익 공헌이 전망됩니다.

The European TIC market was valued at USD 66.61 billion in 2025 and estimated to grow from USD 69.27 billion in 2026 to reach USD 84.28 billion by 2031, at a CAGR of 4.00% during the forecast period (2026-2031).

The market's structural momentum is anchored in escalating regulatory demands under the EU Digital Operational Resilience Act, Corporate Sustainability Reporting Directive, and Cyber Resilience Act, each of which now compels demonstrable third-party assurance across financial, sustainability, and connected-product domains. Accelerated renewable-energy build-outs, a sustained shift toward outsourced verification, and the rapid emergence of AI-enabled inspection technologies further reinforce growth prospects even as economic sentiment remains uneven across member states. At the same time, the European TIC market is navigating cybersecurity constraints that temper full-scale remote inspection uptake, while cost pressures on small and medium enterprises keep price sensitivity elevated. Consolidation attempts such as the terminated SGS-Bureau Veritas merger illustrate both the strategic value and complexity of achieving scale in one of the world's most heavily regulated business services arenas.

DORA, CSRD, and the Cyber Resilience Act became enforceable during 2024, compelling financial firms, large corporates, and connected-product manufacturers to secure multi-layered third-party assurance for ICT risk, sustainability disclosures, and product cybersecurity, respectively. Compliance budgets now allocate roughly 30% to external audits, translating into fresh revenue pools for end-to-end providers able to cover cyber, ESG, and operational-resilience scopes in a single engagement. Demand aggregation across these domains amplifies cross-selling potential, particularly for providers with integrated digital audit platforms. Because the European TIC market is one of the few service categories legally mandated for market entry, spending remains relatively inelastic even amid broader cost-containment drives. Medium-term growth, therefore, hinges on providers' capacity to scale multidisciplinary expertise while assuring data-integrity standards acceptable to supervisory authorities.

Record wind and solar build-outs under the REPowerEU plan require exhaustive verification of turbine integrity, power-curve performance, and grid-integration safety, creating high-margin opportunities for TIC specialists in marine classification and environmental impact assessment. Project developers face certification bottlenecks as national authorities uphold stringent technical codes but streamline permitting deadlines, magnifying the strategic value of accredited labs with deep domain know-how. Offshore wind growth in the North Sea alone commands premium fees because of complex subsea cabling tests and harsh-environment material qualification. As renewable-asset owners adopt AI-driven drone monitoring to manage aging fleets, certification bodies able to validate both hardware and data analytics algorithms gain a competitive advantage. The European TIC market consequently secures a long-run growth engine that is closely tied to the continent's net-zero timetable.

Certification expenses often equal 2-3% of SME revenue, pressuring smaller firms to postpone full compliance and, in some cases, forgo export opportunities. Multiple national accreditation bodies, despite mutual-recognition accords, still impose duplicative paperwork that raises administrative burdens. While digital audit portals are lowering transaction costs, the economics of maintaining ISO-accredited capacity continue to favor large service groups, creating an access gap that can inhibit broader European TIC market penetration, particularly in Eastern Europe, where purchasing power is lower.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Testing services contributed USD 36.09 billion, equivalent to 54.20% of the European TIC market in 2025, as advanced electronics, medical devices, and automotive components all require multi-disciplinary performance assessments before commercialization. Digital workflows such as cloud-based test-data portals shorten turnaround times and enhance client transparency, deepening competitive moats for early adopters. Certification, though smaller today, is forecast to compound at 4.58% annually, driven by CSRD-mandated assurance and expanding management-system standards that now cover cybersecurity, business continuity, and social responsibility. Inspection maintains steady relevance in infrastructure life-cycle management, especially in legacy manufacturing hubs where periodic structural assessments are compulsory.

Integrated platforms that unify test scheduling, real-time analytics, and certificate issuance are blurring boundaries between traditional service silos. Providers that can bundle lab tests with on-site and remote inspection in a single engagement are capturing wallet share as clients pursue one-stop compliance solutions. Investment is flowing into AI-enabled defect-recognition algorithms that raise lab throughput while preserving data integrity, reinforcing Testing's primacy within the European TIC market.

Outsourced verification accounted for 63.05% of the European TIC market size in 2025, reflecting a decisive shift away from capital-intensive in-house labs. Manufacturers in aerospace and automotive segments, faced with material science advances and evolving safety standards, prefer variable cost models that align spending with production volumes. Outsourced services also provide immediate access to global accreditations, which accelerate time-to-market for exports and mitigate regulatory risk.

Outcome-based contracts under which TIC firms assume compliance responsibility for a defined scope are expanding, generating recurring revenue, and incentivizing continuous process improvement. Although intellectual-property concerns keep some testing activities internal, the broader outsourcing trend is expected to sustain a 4.37% CAGR, positioning the European TIC market for stable double-digit revenue contribution from service contracts linked to long-term framework agreements.

The Europe TIC Market Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House and Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Automotive and Transportation, and More), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Country. The Market Forecasts are Provided in Terms of Value (USD).