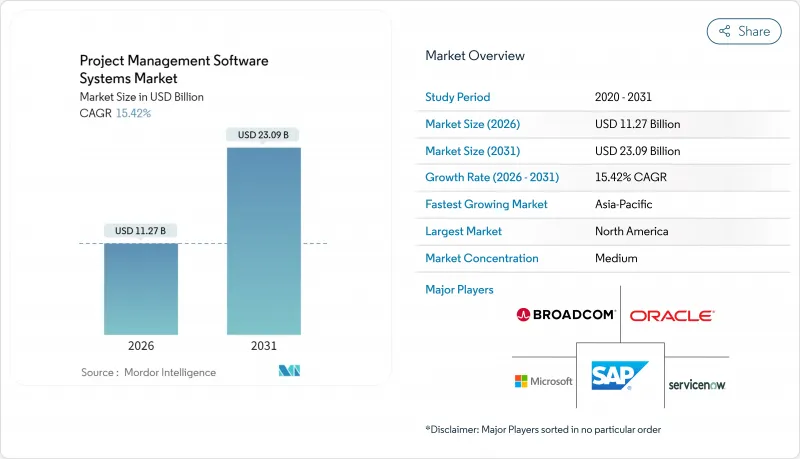

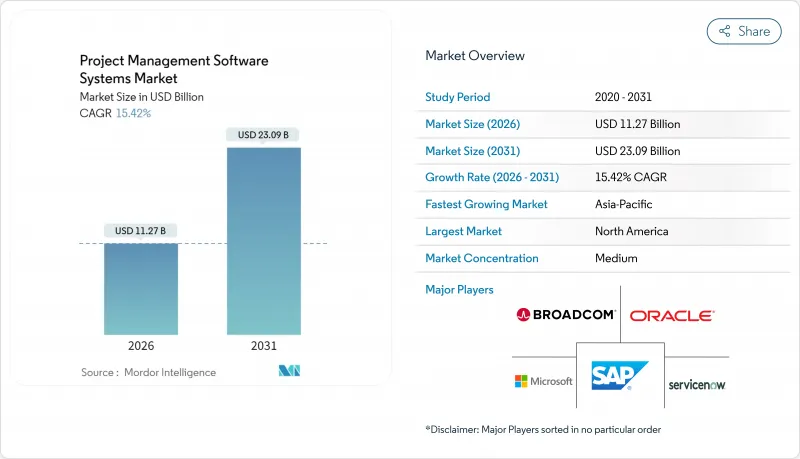

프로젝트 관리 소프트웨어 시스템 시장은 2025년에 97억 6,000만 달러로 평가되었으며, 2026년 112억 7,000만 달러에서 2031년까지 230억 9,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 15.42%로 전망됩니다.

확장의 기반은 클라우드 퍼스트 배포, 로우코드에 의한 설정 가능성, 예측 분석에 있으며, 이들이 함께 프로젝트 감시를 태스크 추적에서 전략적 조정으로 고도화합니다. 분산형 팀이 실시간 협업을 필요로 하고 기업이 프로젝트 데이터를 재무, 인사 및 고객 시스템과 통합하여 통일적인 가시성을 요구함으로써 수요가 높아지고 있습니다. 규제 산업에서는 여전히 로컬 데이터 관리가 필요하기 때문에 하이브리드 배포가 가장 빠른 성장을 기록하고 있습니다. 중소기업(SME)은 기존의 구현 장벽을 피함으로써 도입을 가속화하고 AI 네이티브 기능은 리스크 관리와 비용 예측을 강화합니다. 벤더가 업계 고유의 워크플로와 오픈 API 에코시스템을 통합함으로써 경쟁이 치열해지고 있습니다.

각 조직은 데스크톱 도구에서 클라우드 네이티브 플랫폼으로의 마이그레이션으로 작업 완료 속도가 54% 향상되었다고 보고했습니다. 실시간 동기화를 통해 분산 팀이 시간대를 넘어 작업을 유지할 수 있기 때문에 프로젝트 관리 소프트웨어 시스템 시장은 기세를 늘리고 있습니다. IT 부문은 용량 계획의 부담을 줄이는 클라우드의 확장성을 선호합니다. 규제 대상 부문은 접근성과 데이터 관리 간의 균형이 요구되기 때문에 하이브리드 모델 시장은 18.4%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다. 공급업체는 주권 요건을 충족하면서 마찰이 없는 협업을 유지하는 데이터 거주 옵션을 제공함으로써 대응합니다.

기업은 평균 976개의 애플리케이션을 운영하고 있지만 실질적으로 통합된 것은 28%에 불과하며 프로젝트 데이터의 흐름이 느려집니다. 현대 플랫폼은 재무, CRM, 인적 자원 시스템과 연계된 통합 허브로 자리매김하여 프로젝트 관리 소프트웨어 시스템의 기업 아키텍처에서 중요성을 높였습니다. SaaS 통합 부문은 2025년까지 150억 달러 이상에 달한 것으로 나타났으며, 종합적인 통합 전략을 도입한 기업에서는 생산성이 30% 향상된 것으로 보고되었습니다. 클라우드 네이티브 벤더는 고가의 맞춤형 코딩의 필요성을 줄이는 개방형 API와 사전 구축된 커넥터를 통해 우위를 얻습니다.

기업은 데이터 매핑, 검증, 사용자 교육이 노동 집약적이기 때문에 라이선스 비용의 3배에 이르는 도입 비용에 직면하고 있습니다. 마이그레이션 비용은 평균 30%를 초과하며 아카이브 테라바이트당 USD 15,000에 도달할 가능성이 있습니다. 이 장벽은 업데이트 주기를 늦추고 고도로 맞춤화된 워크플로가 있는 기존 기업의 프로젝트 관리 소프트웨어 시스템 시장 침투를 늦추고 있습니다.

2025년에는 클라우드 도입이 수익의 74.20%를 차지했지만 하이브리드 구성은 18.12%의 연평균 복합 성장률(CAGR)로 성장하여 프로젝트 관리 소프트웨어 시스템 시장에서 가장 강한 기세를 보이고 있습니다. 하이브리드 솔루션은 로컬 리포지토리와 클라우드 작업 공간을 동기화하며, 이러한 이중성이 데이터 거주지 규정에 속하는 기업을 유치합니다. 온프레미스 솔루션은 정부 및 방위 분야에서 지속되고 있지만, 클라우드 존의 보안 인증이 엄격해짐에 따라 점유율이 감소하는 추세에 있습니다.

하이브리드의 등장은 원활한 오프라인 동기화, 암호화 터널 및 선택적 스토리지를 관리하는 도구의 진화를 반영합니다. 건설 회사는 도면을 로컬 서버에 저장하면서 현장 업데이트 정보를 클라우드 대시보드에서 공유합니다. 벤더는 세분화된 테넌트 제어를 제공함으로써 차별화를 도모하고 컴플라이언스를 축으로 한 업셀 경로를 구축하고 있습니다.

2025년 지출액에서는 대기업이 60.35%를 차지했지만 중소기업은 16.89%의 연평균 복합 성장률(CAGR)을 나타내며 프로젝트 관리 소프트웨어 시장의 규모를 변화시키고 있습니다. 성장의 중심은 아시아태평양이며 지방 정부는 디지털 기술 향상 보조금을 제공합니다. 일본의 중소기업은 노동력 부족을 보완하기 위해 AI 지원 스케줄링을 도입하고 있습니다. 가격대에서 사용자 최소 요구사항이 사라지면서 진입 장벽이 저하되었습니다.

포화 상태의 지역에서는 대기업의 성장이 두드러지기 때문에 벤더는 중소기업용 라이트 버전이나 커뮤니티 이벤트를 전개하고 있습니다. 그러나 다국적 기업은 복잡한 통합 기능과 프리미엄 분석 패키지를 여전히 수익의 기반으로 삼고 있습니다. 이러한 이중 초점은 제품 팀이 배포 프로세스를 복잡하게 하지 않고 확장성을 유지할 것을 요구합니다.

북미는 2025년 시점에서 프로젝트 관리 소프트웨어 시스템 시장의 36.12%를 차지했습니다. 이 지역의 기업은 강력한 인프라와 대규모 IT 예산을 활용하여 엔드 투 엔드 프로젝트 생태계를 구축하고 있습니다. Microsoft는 2024년 16%의 수익 성장을 기록했으며 이는 2,450억 달러에 달했습니다. 이는 Microsoft 365의 통합 프로젝트 기능에 의해 지원됩니다. 혁신 거점에서는 AI 모듈의 개발이 계속되고 있지만, 보급률이 포화 상태에 가까워짐에 따라 지역 성장이 완만해지고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 16.06%로 확대될 전망이며 지역별로 가장 높은 성장률을 보였습니다. 중국의 SaaS 부문은 연간 약 30%의 속도로 확대되고 있으며, 다국적 기업은 국경을 넘어선 노력을 관리하기 위해 Salesforce와 Azure의 통합 스택을 도입하고 있습니다. 인도의 SaaS 수익은 클라우드 도입과 스타트업의 기세에 힘입어 2023년 71억 8,000만 달러에서 2032년까지 629억 3,000만 달러로 증가할 것으로 예측됩니다. 동남아시아 전역의 중소기업은 지역의 컴플라이언스 기준을 통합한 현지어 대응 PM 스위트를 도입하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)이 현지화 기능을 의무화하면서 EU 데이터센터와 첨단 암호화를 제공하는 공급업체가 꾸준히 성장하고 있습니다. 남미, 중동, 아프리카에서는 광대역과 결제 인프라가 정비되어 지금까지 인프라 부족으로 막혀 있던 클라우드 구독이 확대되고 있습니다. 연결 비용이 더 낮아지면 공급업체의 두 자릿수 성장이 기대됩니다.

The project management software systems market was valued at USD 9.76 billion in 2025 and estimated to grow from USD 11.27 billion in 2026 to reach USD 23.09 billion by 2031, at a CAGR of 15.42% during the forecast period (2026-2031).

Expansion remains anchored in cloud-first deployment, low-code configurability, and predictive analytics that collectively upgrade project oversight from task tracking to strategic orchestration. Demand intensifies as distributed teams require real-time collaboration, and enterprises integrate project data with finance, HR, and customer systems for unified visibility. Hybrid deployment registers the fastest growth because regulated industries still need local data control. Small and medium enterprises (SMEs) accelerate adoption by bypassing traditional implementation hurdles, while AI-native features strengthen risk management and cost forecasting. Competitive intensity increases as vendors embed industry-specific workflows and open API ecosystems.

Organizations report 54% faster task completion when shifting from desktop tools to cloud-native platforms. The project management software systems market gains traction because real-time synchronization enables distributed teams to sustain momentum across time zones. IT departments prefer cloud scalability that removes capacity planning burdens. Hybrid models are projected to grow at an 18.4% CAGR because regulated sectors balance accessibility with data control. Vendors respond by offering data-residency options that satisfy sovereignty mandates while maintaining friction-free collaboration.

Enterprises run an average of 976 applications, yet only 28% are meaningfully integrated, stalling project data flow. Modern platforms position themselves as integration hubs tied to finance, CRM, and HR systems, thereby increasing the relevance of project management software systems in enterprise architecture. The SaaS integration segment is projected to exceed USD 15 billion by 2025, and firms that deploy comprehensive integration strategies report 30% productivity lifts. Cloud-native vendors gain an advantage through open APIs and pre-built connectors, which reduce the need for expensive custom coding.

Enterprises face implementation bills that triple license fees because data mapping, validation, and user training are labor-intensive. Migration overruns average 30% and can reach USD 15,000 per terabyte of archives. The hurdle delays refresh cycles and slows the project management software systems market uptake among incumbents with heavily customized workflows.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud deployment accounted for 74.20% of revenue in 2025, but hybrid configurations grew at an 18.12% CAGR, signaling the strongest momentum within the project management software systems market. Hybrid solutions synchronize local repositories with cloud workspaces; this duality attracts firms bound by data residency statutes. On-premise solutions persist in government and defense, yet their share is shrinking as security certifications for cloud zones become tighter.

The hybrid rise reflects tools that now manage seamless offline sync, encrypted tunnels, and selective storage. Construction companies store drawings on local servers while sharing field updates through cloud dashboards. Vendors differentiate by offering granular tenancy controls, creating upsell paths around compliance.

Large enterprises controlled 60.35% of the 2025 spend, but SMEs chart a 16.89% CAGR, reshaping the project management software systems market size trajectory. Growth centers on the Asia-Pacific region, where local governments are funding digital upskilling grants. Japanese SMEs adopt AI-assisted scheduling to offset labor shortages. Pricing tiers remove user minimums, reducing the barrier to entry.

Enterprise growth plateaus in saturated regions, so vendors launch light editions and community events geared to smaller firms. Yet, multi-national corporations still anchor revenue with complex integrations and premium analytics bundles. Dual focus forces product teams to maintain scalability without complicating the onboarding process.

The Project Management Software Systems Market Report is Segmented by Deployment (Cloud and On-Premise), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (IT and Telecom, Healthcare, and More), Subscription Type (Monthly Subscription, Annual Subscription, and One-Time License), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 36.12% of the project management software systems market in 2025. Enterprises there leverage robust infrastructure and sizable IT budgets to roll out end-to-end project ecosystems. Microsoft recorded 16% revenue growth to USD 245 billion in 2024, supported by integrated project functions within Microsoft 365. Innovation hubs continue to pioneer AI modules, yet regional growth moderates as penetration nears saturation.

Asia-Pacific grows at a 16.06% CAGR through 2031, the fastest across regions. China's SaaS segment is expanding at nearly 30% annually, with multinationals installing integrated Salesforce and Azure stacks to manage cross-border initiatives. India's SaaS revenue is forecast to increase from USD 7.18 billion in 2023 to USD 62.93 billion by 2032, driven by cloud adoption and startup momentum. SMEs across Southeast Asia adopt local-language PM suites that embed regional compliance norms.

Europe posts steady gains as GDPR compels localization features, rewarding vendors offering EU data centers and advanced encryption. South America, and Middle East, and Africa are now improving broadband and payment rails, nurturing cloud subscriptions previously held back by infrastructure gaps. Vendors anticipate double-digit uptake once connectivity costs fall further.