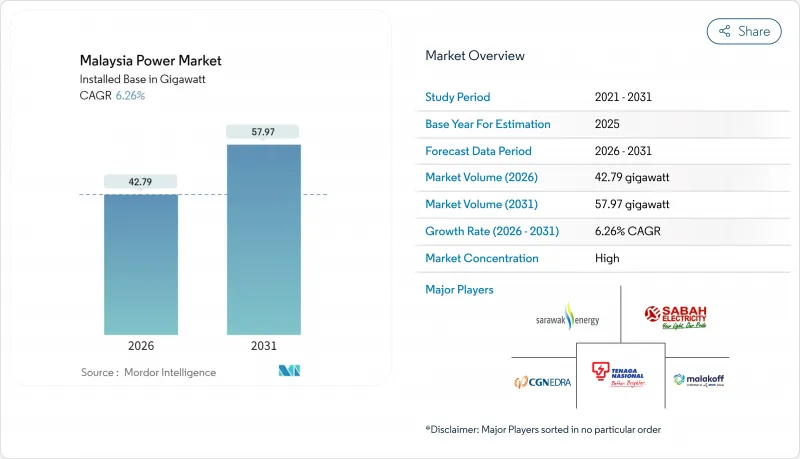

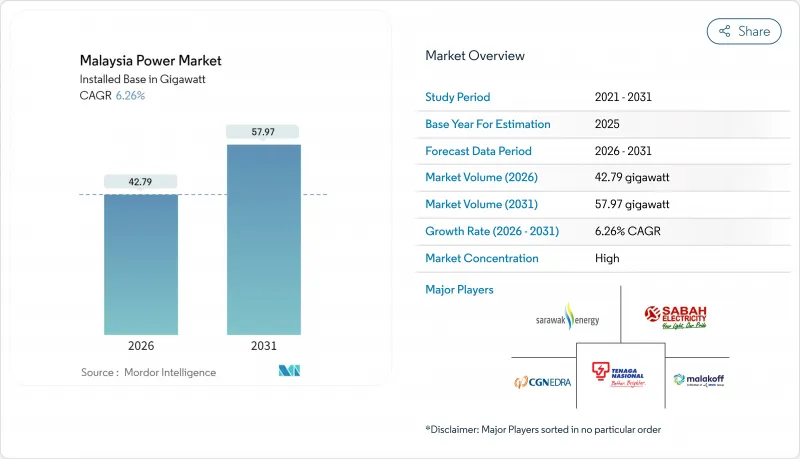

말레이시아의 전력 시장의 규모는 2026년에는 42.79기가와트에 달할 것으로 예측되고 있습니다.

이는 2025년의 40.27기가와트에서 성장한 수치이며, 2031년에는 57.97기가와트에 이를 것으로 전망되고 있습니다. 2026년부터 2031년까지는 CAGR 6.26%로 성장할 전망입니다.

하이퍼스케일 데이터센터 클러스터는 신규 부하 용도에서 11기가와트를 차지하고 있으며, 이 수치는 불과 2년 만에 두배로 증가하였고, Tenaga Nasional Berhad(TNB)에 발전 및 송전망에 대한 투자 가속화를 요구하고 있습니다. 2024년 기준에서 말레이시아 전력 시장의 75.6%를 화력 기술이 차지하였으나, 2030년까지 재생에너지가 가장 급속히 성장하여 석탄 대신 태양광, 수력, 축전지 프로젝트에 자본이 재분배될 전망입니다. 제3자 액세스 규칙에 의해 조달 권한이 기업 소비자로 이행하고 있으며, 요금 및 보조금 개혁에 의해 가격이 비용 회수와 정합됨으로써, 분산형 태양광 발전의 경제성이 향상하고 있습니다. 페낭, 셀랑골, 조호르의 반도체 제조 거점과 클라우드 인프라 허브는 지속적인 산업 수요를 지원하는 반면 천연가스 공급 제약과 동말레이시아의 취약한 송전망에서의 출력 억제 리스크가 주요 불확실성 요인이 되고 있습니다.

쿨림에 건설 중인 인피니언사의 20억 유로 규모 탄화규소 공장은 기존의 석유화학산업에서 정밀제조업으로의 구조적 전환을 상징하고 있으며, 이는 현재 말레이시아의 전력 시장의 기반이 되고 있습니다. 국영전력회사(TNB)는 데이터센터 용도만으로 총 11GW에 이르는 것을 파악하였으며 이러한 수요 증가에 대응하기 위해 163억 링깃에 해당하는 예비 자본 지출의 30%를 예기치 않은 부하 증가에 대비해 확보할 수 밖에 없는 상황입니다. 2030년까지 산업용 수요는 총 소비량의 절반을 유지할 것으로 예상되지만, 구성비는 저탄소 전력을 필요로 하는 반도체 및 클라우드 워크로드로 기울고 있습니다. 발전이나 송전망의 정비에 지연이 발생하면, 보다 선진적인 재생에너지 조달 틀을 가진 지역 경쟁자에게 이러한 투자를 빼앗길 위험이 있습니다. 이 때문에 지방정부는 예비율을 적절히 유지하기 위해 변전소 업그레이드를 신속하게 진행하여 축전지의 도입을 촉진하고 있습니다.

국가 에너지 전환 로드맵은 2025년까지 재생에너지 용량을 31%, 2035년까지 40%로 하는 목표를 정하고 있습니다. 이러한 목표를 달성하기 위해서는 연간 약 1.5기가와트의 신규 발전 용량 도입이 필요하며, 이는 과거의 건설 속도를 크게 초과합니다. 대규모 태양광 발전 5차 입찰에서는 2024년 말레이시아계 입찰자에게 2기가와트가 할당되어 국내 조달 비율 확보를 도모했지만 개발자의 선택은 좁아졌습니다. TNB(국영전력회사)의 수력저수지용 2.5기가와트 부체식 태양광발전계획은 기존의 송전회랑을 활용하여 토지 이용 경쟁을 최소화합니다. 한편 사라왁 에너지사의 7,300메가와트 수력발전설비군은 국경을 넘은 송전망이 정비되면 말레이시아 동부를 잠재적인 청정전력 수출지역으로 자리매김할 전망입니다. 2050년까지 재생에너지 비율 70%를 달성하려는 목표는 석탄 화력 발전의 거의 완전한 폐지를 의미합니다. 수소 대응형 복합 사이클 가스 터빈이 교량 기술로서 자리매김되고 있지만, 연료 공급의 불안정성이 과제가 되고 있습니다.

국내 가스 생산은 현저히 증가하는 상태에 있으며, 페트로나스는 LNG 수출을 선호하기 때문에 연료 부족 현상이 정기적으로 발생하고 발전 사업자는 더 높은 비용의 디젤 연료로 전환해야 합니다. 2022년 세계 LNG 가격이 급등했을 때, 말레이시아의 요금 전가 메커니즘은 연료 비용 증가를 따라잡지 못하고 독립 발전 사업자(IPP)의 이익률을 압박했습니다. 도입 계획 중인 수소 대응 터빈으로 인해 그린 수소가 서서히 가스를 대신할 것으로 예상되지만, 산업 규모의 수소 인프라는 아직 발전 가능성이 낮습니다. 저장, 수입, 가격 개혁이 동조하여 실현되지 않는 한, 가스에 대한 의존성은 유연한 화력 자산에 대한 투자 의욕을 억제하고 말레이시아의 전력 시장의 확대 속도를 둔화시킬 전망입니다.

말레이시아의 재생가능 에너지 시장의 규모는 CAGR 22.89%로 확대되어 2025년 말레이시아의 전력 시장의 74.92%를 차지한 화력 기술의 시장 점유율을 흡수한 것으로 나타났습니다. 태양광이 재생에너지 급증을 견인하고 있으며, TNB에 의한 2.5GW급 부체식 태양광 발전 도입과 대규모 태양광 5차 입찰로 할당된 2GW의 용량이 이를 뒷받침하고 있습니다. 수력 발전은 말레이시아 동부에서 여전히 중요한 역할을 하고 있지만, 환경 평가와 지역사회와의 협의에 의해 확장에는 제약이 있습니다. 석탄은 2030년까지 9.1기가와트 규모의 폐지가 예정되어 급격한 감소가 예상됩니다. 한편, 수소 대응 가스 터빈은 예비율을 향상시켜 미래의 연료 전환을 위한 송전망의 준비를 진행하고 있습니다. 축전지의 도입 또한 중요한 요소가 됩니다. 충분한 축전 용량이 있으면 태양광 발전의 보급률을 높일 수 있지만, 부족한 경우에는 중간 부하 가스 발전소의 가동 기간이 길어집니다.

태양광발전의 균등화 발전원가는 축전설비 도입 전단계인 2024년 이미 한계가스발전비용까지 다다랐으며 독립계발전사업자(IPP)가 유틸리티 입찰에 더해 기업용 전력구입계약(PPA)에 참가하는 요인이 되었습니다. 사라왁의 수력 자산은 변동 비용이 낮고 베이스로드에 가까운 전력을 공급하고 있으며, 송전망 연결이 실현되면 사라왁은 잠재적인 전력 수출지가 될 전망입니다. 풍력과 지열 발전은 여전히 시험 단계에 있으며, 바이오 매스는 원료 가격 상승으로 확대 속도가 둔화되고 있습니다. 이러한 변화하는 전력원 구성은 말레이시아의 전력 시장에서 발전 순서, 배출 강도, 투자 배분에 영향을 미칠 것입니다.

말레이시아의 전력 시장 보고서는 전력원별(화력, 원자력, 재생에너지) 및 최종 사용자별(전력 회사, 상업 및 산업, 주택)으로 분류됩니다. 시장 규모와 예측은 시설용량(GW) 단위로 제공됩니다.

Malaysia Power Market size in 2026 is estimated at 42.79 gigawatt, growing from 2025 value of 40.27 gigawatt with 2031 projections showing 57.97 gigawatt, growing at 6.26% CAGR over 2026-2031.

Hyperscale data-center clusters account for 11 GW of new load applications, a figure that has doubled in only two years and is forcing Tenaga Nasional Berhad (TNB) to accelerate generation and grid investments. While thermal technologies maintained 75.6% of the Malaysian power market in 2024, renewables are the fastest-growing through 2030 and will re-allocate capital toward solar, hydro, and battery projects at the expense of coal. Third-party access rules are shifting procurement power to corporate consumers, and tariff-subsidy reforms are aligning prices with cost recovery, which, in turn, improves the economics of distributed solar. Semiconductor fabrication and cloud infrastructure hubs in Penang, Selangor, and Johor underpin sustained industrial demand, yet natural-gas supply constraints and curtailment risk in weak East Malaysia grids serve as headline uncertainties.

Infineon's EUR 2 billion silicon-carbide fab in Kulim exemplifies the structural shift from legacy petrochemicals toward precision manufacturing that now underpins the Malaysian power market. TNB has confirmed that data-center applications alone total 11 GW, compelling the utility to reserve 30% of its RM 16.3 billion contingent capital expenditure for unanticipated load growth. Industrial demand is expected to maintain half of total consumption through 2030, but the composition tilts toward semiconductor and cloud workloads that require low-carbon electricity. Any lapse in generation or transmission build-out risks divesting these investments to regional competitors with more advanced renewable procurement frameworks. Consequently, local authorities are fast-tracking substation upgrades and incentivizing battery storage to keep reserve margins adequate.

The National Energy Transition Roadmap sets milestones of 31% renewable capacity by 2025 and 40% by 2035. Achieving these goals requires annual additions near 1.5 GW, notably faster than historical build-out rates. Large-Scale Solar Round 5 allocated 2 GW in 2024 to Malaysian-controlled bidders, favoring domestic content capture but narrowing the developer field. TNB's 2.5 GW floating-solar program across hydro reservoirs leverages existing transmission corridors and minimizes land-use conflicts, while Sarawak Energy's 7,300 MW hydro fleet positions East Malaysia as a potential clean-power exporter once cross-border interconnections advance. The 70% renewable aspiration by 2050 implies near-zero coal, with hydrogen-ready combined-cycle gas turbines providing a bridge technology, albeit with fuel-supply uncertainties.

Domestic gas production has plateaued, and Petronas prioritizes LNG exports, resulting in periodic fuel shortages that force generators to switch to costlier diesel back-up.When global LNG prices spiked in 2022, Malaysia's tariff-pass-through mechanism lagged fuel costs, compressing IPP margins. Planned hydrogen-ready turbines assume green hydrogen will gradually displace gas, yet industrial-scale hydrogen infrastructure remains nascent. Unless coordinated storage, import, and pricing reforms materialize, gas exposure will weigh on Malaysia's power market expansion speed by suppressing investor appetite for flexible thermal assets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The Malaysian power market size for renewables is projected to rise at a 22.89% CAGR, eating into thermal technology's 74.92% Malaysia power market share in Malaysia in 2025. Solar leads the renewable surge, propelled by TNB's 2.5 GW floating-solar roll-out and 2 GW of allocated capacity under Large-Scale Solar Round 5. Hydro remains pivotal in East Malaysia, yet expansion is bound by environmental assessment and community engagement. Coal will decline sharply, with 9.1 GW scheduled to retire by 2030, while hydrogen-ready gas turbines pick up reserve margins and prepare the grid for future fuel transitions. Battery storage adoption becomes a gating factor: adequate storage unlocks higher solar penetration, while shortfalls would keep mid-merit gas plants online longer.

Solar's levelized cost fell below marginal gas generation in 2024, even before storage, encouraging IPPs to stack corporate PPAs on top of utility tenders. Hydro assets in Sarawak supply near-baseload output at low variable cost, positioning the state as a potential exporter pending interconnection. Wind and geothermal remain exploratory, and biomass expansion slows due to rising feedstock prices. The evolving mix will influence dispatch order, emissions intensity, and investment allocation across the Malaysia power market.

The Malaysia Power Market Report is Segmented by Power Source (Thermal, Nuclear, and Renewables) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).