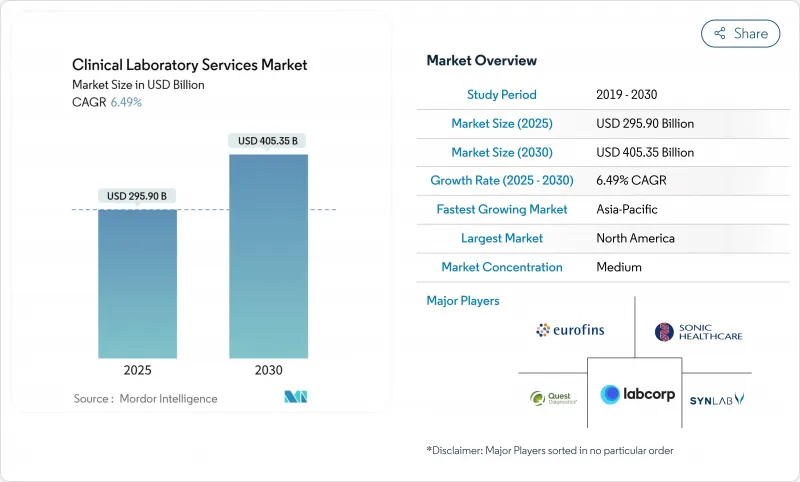

임상 검사 서비스 시장 규모는 2025년 2,959억 달러, 2030년 CAGR 6.49%로 4,053억 5,000만 달러에 이를 것으로 예측됩니다.

만성 질환 감시, 전염병 경보, 고정밀 종양학 등 시장 규모 확대는 진단이 의료 예산에서 점점 더 큰 비율을 차지하고 있음을 뒷받침합니다. 대규모 네트워크는 일상적인 가격 설정에 대한 하향 압력을 상쇄하기에 충분한 강력한 마진을 제공하는 고 복잡도 분석에 메뉴 방향타를 자릅니다. COVID-19 기간 동안 이루어진 자동화된 투자로 이들 네트워크는 검사 단가를 안정화시키면서 임금 인플레이션을 흡수할 수 있게 되었고, 지불자 협상에서 경쟁력이 강화되었습니다. 분자 프랜차이즈와 병원 아웃리치 부문을 대상으로 하는 활발한 프라이빗 에퀴티 딜의 흐름은 미국 메디케어 스케줄이 재설정되어도 시료량은 계속 증가할 것이라는 확신의 표현입니다. 아시아태평양에서는 새로운 그린필드 체인이 급속히 규모를 확대하고 있으며, 북미가 규모의 리더십을 유지하는 한편, 아시아가 시료수 증가를 가져온다는 듀얼 허브의 미래를 시사하고 있습니다. AI 트리어지 툴이나 큐레이션된 변이 데이터베이스 등의 지적재산 자산이 거래 가능한 코모디티로서 대두하고 있어, 오프라인 매장를 가지는 검사 시설과 늘어선 새로운 가치 획득 모델을 시사하고 있습니다.

당뇨병, 심혈관계 위험, 호흡기계 병원체의 생화학 패널 확대가 임상 검사 서비스 시장 전체의 기준선량을 수증하고 있습니다. 병원 시스템의 보고에 따르면, 대사 화학 검사의 요청 건수는 유행 이전의 수준을 웃돌았으며, 이는 뒤에 받은 의료 잡기를 반영합니다. COVID-19에 도입된 고처리량 분석기는 중앙 검사실이 선형 비용 증가 없이 더 많은 시료를 처리할 수 있게 함으로써 업무 레버리지를 계속 적용하고 있습니다. 통합 네트워크는 여러 시설에서 시료를 일괄 처리하여 가동률을 높이고 보다 강력한 시약 가격을 확보합니다. 이러한 효율성으로 인해 지불자의 요금 체계가 엄격해져도 조익이 유지됩니다.

65세 이상의 노인은 젊은층의 3배에 가까운 연간 시료 수가 있으며, 그 인구 구성비는 상승 경향이 있습니다. 지질, 갑상선, 신장 마커를 번들한 연 1회 건강검진은 계절적인 수요를 평준화하고 안정적인 현금흐름을 창출합니다. 검사 시설은 매월 검사 할당을 보장하고 보험자에게 예산의 확실성을 제공하면서 수령을 원활하게 하는 지불자와 구독 형식의 계약을 시험적으로 실시했습니다. 종단적인 결과를 바탕으로 구축된 집단 건강 대시보드는 분석적인 수입원을 추가하고 임상 검사 서비스 시장을 더욱 확대합니다.

지난 10년간 미국의 메디케어 루틴 화학 검사료는 4분의 1에 가까이 낮아졌습니다. 대규모 레퍼런스 랩은 전처리 및 벌크 시약 계약의 로봇화를 통해 이 압력을 상쇄했지만, 소규모 병원 시설은 이러한 효율에 필적하는 데 어려움을 겪고 있습니다. 따라서 까다로운 측정 방법의 아웃소싱이 가속되고 더 많은 시료가 더 낮은 단가로 운영할 수 있는 내셔널 그리드로 보내집니다.

임상 화학은 2024년 임상 검사 서비스 시장의 절반 이상을 차지하는 기간 시장입니다. 그 엄청난 설치 기반은 예측 가능한 시약 소비와 장비 공급업체와의 안정적인 관계를 보장합니다. 소량의 수량이 증가하더라도이 부문에 의미있는 추가 수익이 됩니다. CAGR 9.5%를 보일 것으로 예측되는 유전학·분자진단학은 경쟁시약에서 독자적인 바이오인포매틱스로 가치를 이동시킴으로써 경쟁의 해자를 재정의하고 있습니다. 초기 스크리닝 후 단일 유전자에서 다중 유전자 패널로 이동하는 반사 검사는 샘플의 보급률을 높이고 요청 1건당 평균 수익을 증가시킵니다. 큐레이션 된 변형 라이브러리가있는 실험실은 임상의의 스위칭 비용을 높이는 지식 자산을 관리합니다.

상품 화학과 이익률이 높은 유전체학의 상호 작용은 자본 배분을 형성합니다. 케미스트리와 면역분석을 조합한 통합분석장치는 일상 업무를 지원하기 때문에 리프레시 사이클에 대한 수요가 계속되고 있습니다. 한편, 유전체학 플랫폼은 종양학 및 희귀질환 프로그램과 관련된 프로젝트 기반 자금을 유치합니다. 미들웨어 분석을 케미스트리 라인에 번들하는 공급업체는 생태계의 잠금을 생성하고 시퀀싱 장비의 클라우드 파이프라인은 보고 시간을 단축하고 비학교 센터에서도 의사의 신뢰를 구축합니다.

북미가 2024년 매출액 점유율 41.3%로 임상 검사 서비스 시장을 선도했습니다. 폭넓은 보험 적용 범위와 1인당 검사 건수의 많음이 수요를 지지하고 있습니다. Quest Diagnostics와 Labcorp는 미국 검체량의 약 5분의 1을 함께 관리합니다. 두 그룹 모두 의료 필요성 검사를 포함한 전자 주문 진입 시스템을 채택하여 청구 거부를 줄이고 현금 흐름을 유지합니다. 퀘스트에 의한 라이플라보의 CAN13억 5,000만 달러로 인수와 같은 거래는 미국의 상업 지불자 믹스를 넘어 노출을 확대합니다.

아시아태평양은 도시화, 민간 보험 가입, 국가의 자금 지원이 집중되고 CAGR 7.84%로 가장 빠른 성장을 보일 것으로 예측됩니다. 중국의 2급 도시에서는 하이 스루풋의 화학 검사나 PCR 라인을 갖춘 집중 실험실의 건설이 진행되고 있어, 인도의 진단약 체인은 반도시에서도 검사를 받을 수 있는 프랜차이즈 방식의 수집 센터를 전개하고 있습니다. College of American Pathologists 인증과 같은 국제 인증은 품질 지표가 되고 있으며, 이 지역은 다국적 임상시험을 지원하는 능력을 가속화하고 있습니다.

유럽은 성숙하면서도 혁신적인 지역입니다. 광범위한 검사 메뉴가 환불되는 법정 보험이 뒷받침되며 독일에서만 이 지역의 수익의 18%를 차지할 것으로 추정됩니다. 유럽 연합(EU) 규정은 국경을 넘어 상호 운용성을 장려하고 있으며, 여러 법역의 데이터 공유에 대응하는 검사 정보 시스템에 대한 투자를 촉구하고 있습니다. 소닉 헬스케어가 4억 4,690만 달러로 독일 네트워크 LADR을 인수할 계획은 범유럽적인 번들 테스트 계약을 획득하기 위한 현재 진행 중인 통합을 이야기하고 있습니다. 코딩 규칙이 통일되면 결국 대륙 전체에서 입찰이 가능하고 시장 역학이 재구성될 수 있습니다.

The clinical laboratory services market size is valued at USD 295.9 billion in 2025 and is projected to reach USD 405.35 billion by 2030 at a 6.49% CAGR.

Rising volumes in chronic-disease surveillance, infectious-disease vigilance, and precision oncology confirm that diagnostics now command a growing slice of health-care budgets. Large networks are steering their menus toward high-complexity assays that carry margins strong enough to offset downward pressure on routine pricing. Automation investments made during the COVID-19 period let those networks absorb wage inflation while keeping per-test costs steady, which strengthens competitiveness in payer negotiations. Active private-equity deal flow-targeting molecular franchises and hospital outreach units-signals confidence that specimen volumes will continue to rise even as U.S. Medicare schedules reset. In Asia-Pacific, new greenfield chains are scaling rapidly, suggesting a dual-hub future in which North America safeguards scale leadership while Asia delivers incremental specimen growth. Intellectual-property assets such as AI triage tools and curated variant databases are emerging as tradeable commodities, pointing to fresh value-capture models that sit alongside brick-and-mortar laboratories.

Expanding biochemical panels for diabetes, cardiovascular risk, and respiratory pathogens are padding baseline volumes across the clinical laboratory services market. Hospital systems report that metabolic-chemistry requisitions now exceed pre-pandemic levels, reflecting deferred care catch-up. High-throughput analyzers installed during COVID-19 continue to deliver operational leverage, letting central labs process more tubes without linear cost growth. Consolidated networks batch specimens from multiple sites, which lifts utilization and secures stronger reagent pricing. These efficiencies preserve gross margin even when payer fee schedules tighten.

Individuals aged 65 years and older generate nearly triple the annual requisitions of younger cohorts, and their demographic share is climbing. Annual wellness visits that bundle lipid, thyroid, and renal markers flatten seasonal demand and create steady cash flow. Laboratories are piloting subscription-style agreements with payers that guarantee monthly test allocations, smoothing receipts while giving insurers budget certainty. Population-health dashboards built on longitudinal results provide added analytic revenue streams, further enlarging the clinical laboratory services market.

Successive fee-schedule cuts have shaved nearly one-quarter from U.S. Medicare rates for routine chemistry over the past decade. Large reference labs offset the squeeze with robotics in pre-analytics and bulk reagent contracts, but smaller hospital units struggle to match those efficiencies. Outsourcing of esoteric assays therefore accelerates, sending more specimens to national grids that can operate at lower unit cost.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Clinical chemistry remains the backbone, securing more than half of the clinical laboratory services market in 2024. Its vast installed base assures predictable reagent consumption and steady relationships with device suppliers. Even modest volume upticks translate into meaningful additional revenue for the segment. Genetics and molecular diagnostics, projected to grow at a 9.5% CAGR, are redefining competitive moats by shifting value from commodity reagents to proprietary bioinformatics. Reflex testing that moves from single-gene to multi-gene panels after an initial screen increases sample penetration and average revenue per requisition. Laboratories with curated variant libraries control a knowledge asset that lifts switching costs for clinicians.

The interplay between commodity chemistry and high-margin genomics shapes capital allocation. Integrated analyzers that combine chemistry and immunoassay continue to see refresh-cycle demand because they anchor day-to-day operations, whereas genomic platforms attract project-based funding tied to oncology and rare-disease programs. Vendors that bundle middleware analytics with chemistry lines create ecosystem lock-in, while cloud pipelines on sequencing instruments compress reporting times, building physician trust even in non-academic centers.

The Clinical Laboratory Services Market Report is Segmented by Test Type (Clinical Chemistry, Immunology/Serology, and More), Service Provider (Hospital-Based Laboratories, Stand-Alone/Independent Laboratories, and More), Application (Infectious Disease Testing, Oncology & Tumor Marker Testing, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led the clinical laboratory services market with a 41.3% revenue share in 2024. Broad insurance coverage and high per-capita testing volumes underpin demand. Quest Diagnostics and Labcorp together manage roughly one-fifth of U.S. specimen volume. Both groups employ electronic order-entry systems that embed medical-necessity checks, reducing claim denials and preserving cash flow. Deals such as Quest's CAN $1.35 billion purchase of LifeLabs expand exposure beyond the U.S. commercial payer mix.

Asia-Pacific posts the fastest forecast CAGR at 7.84% as urbanization, private-insurance uptake, and state funding converge. China's tier-two cities are building centralized labs equipped with high-throughput chemistry and PCR lines, while Indian diagnostic chains roll out franchised collection centers that bring testing within reach of semi-urban districts. International accreditation-such as College of American Pathologists certification-is becoming a quality marker, accelerating the region's ability to support multinational clinical trials.

Europe represents a mature yet innovative landscape. Germany alone accounts for an estimated 18% of regional revenue, boosted by statutory insurance that reimburses a broad test menu. European Union regulations encourage cross-border interoperability, prompting investment in laboratory information systems that handle multijurisdictional data sharing. Sonic Healthcare's USD 446.9 million plan to acquire German network LADR illustrates ongoing consolidation aimed at winning pan-European bundled-test contracts. Harmonized coding rules could eventually enable continent-wide tenders, reshaping bidding dynamics across the clinical laboratory services market.