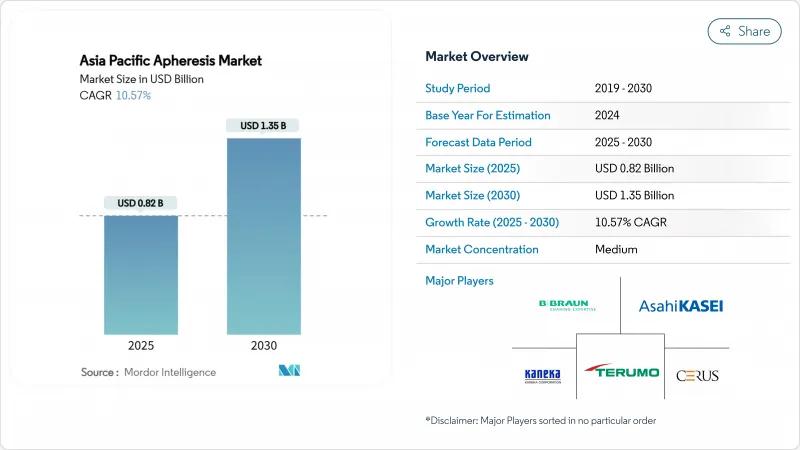

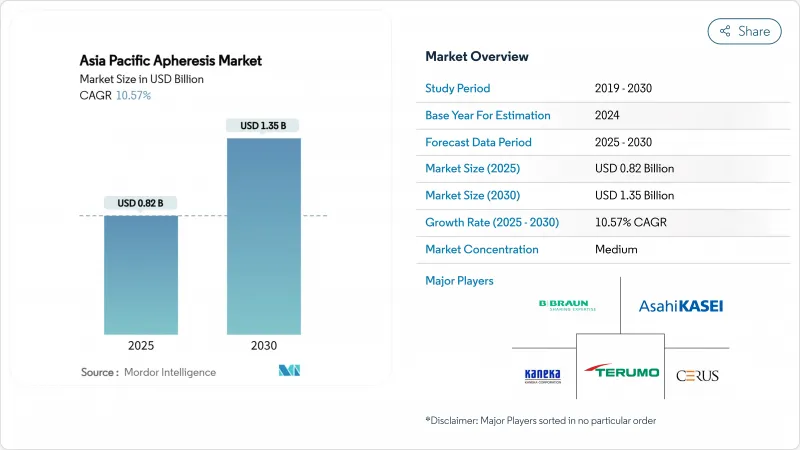

아시아태평양의 아페레시스 시장 규모는 2025년에 8억 2,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 10.57%로, 2030년에는 13억 5,000만 달러에 달할 것으로 예상됩니다.

자동 혈액 성분 기술의 급속한 채용, CAR-T 세포 요법 물류 확대, "Healthy China 2030"과 같은 국가 건강 관리 의제 하에서의 공공 투자는이 지역 전체의 기술을 총체적으로 증가 시켰습니다. 병원과 혈액 센터는 처리 시간을 단축하는 차세대 시스템으로 채혈실을 근대화하고 연구 기관은 세포 치료에 특화된 백혈구 회수 플랫폼에 보조금을 돌리고 있습니다. 한편, 다국적 기업의 전략적 현지화는 수입 리드타임을 단축하고 정부 조달의 의무에 맞추어 공급업체에 대한 충성심을 깊게 하고 있습니다. 그러나 정밀치료에 대한 수요 증가는 이러한 제약을 상회하고 있으며, 아시아태평양의 아페레시스 시장의 견조한 장기 성장 전망을 유지하고 있습니다.

중국이 'Healthy China 2030' 로드맵 하에서 450개 이상의 혈액 센터를 업그레이드하고 있는 것처럼 정부가 지원하는 혈액 안전 프로그램은 수술을 재구성하고 있습니다. Termo는 항저우에 1,500만 달러를 투자하여 Trima Accel 키트를 현지 생산하여 단가를 낮추고 통관 지연을 줄였습니다. 2026년까지 60만 리터를 목표로 하는 인도네시아 최초의 혈장 분획 플랜트는 자급자족을 향한 지역 전체의 변화를 강조하는 것입니다. 이러한 프로그램에서 나온 표준화된 조달 프레임워크는 폐쇄형 루프 추적성과 바이러스 불활성화 모듈을 갖춘 시스템을 지원하고, 프리미엄 플랫폼에 대한 구매 선호를 강화하고, 아시아태평양의 제휴 시장을 추진합니다.

일본, 호주, 한국은 고령화 사회와 암 환자 수 증가에 따라 혈소판 공급 확보를 위한 예산을 앞당겨 계상하고 있습니다. 일본 적십자의 "나라요법"은 자동혈소판요법장치의 능력을 향출시키는 대학과 연동한 트레이닝을 통해 인증 오퍼레이터 풀을 확대하고 있습니다. Sanquin의 Reveos 배포는 기증자 1인당 혈소판 생산 단위가 4에서 5로 증가하여 단위당 20%의 비용 절감을 가져왔습니다는 증거를 제시합니다. 이러한 경제성은 보건부가 일회용 예산을 맡을 것을 촉구하고 아시아태평양의 아페레시스 시장에서의 보급을 가속시킵니다.

신흥 시장의 요금 체계가 일회용을 완전히 커버하는 경우는 거의 없으며, 제공업체는 치료적 조율의 절차 비용의 20-40%를 흡수하게 됩니다. 대한민국 제네릭 의약품 가격 재검토는 정책 입안자가 수술 확대보다 예산 상한을 강조한다는 것을 보여줍니다. 인도의 희귀 질병 정책은 재정적 제약을 강조하고 있으며, 14억 명의 인구에 대해 매년 360만 달러만 할당되고 있습니다. 그 결과, 현금 페이 모델이 주류가 되고, 환자 접근을 억제하고, 아시아태평양의 아페레시스 시장의 단기적인 성장에 멈추고 있습니다.

2024년 아시아태평양의 아페레시스 시장 점유율은 튜브 세트, 분리 키트 및 필터에 대한 지속적인 수요로 인해 일회용 제품이 62.33%를 차지했습니다. 절차의 꾸준한 성장, 엄격한 무균 규칙, 단일 청소년 의무화로 예측 가능한 수량 증가가 보장됩니다. 국영혈액사업이 협상하는 번들 가격계약은 벤더의 포위를 강화하고 마진을 안정시킵니다. 한편, CAGR 14.08%를 나타내는 장비 부문은 서비스 수명을 맞은 기존의 원심분리기 교체 사이클과 운영자 개입을 최대 65% 절감하는 자동화 업그레이드로 이익을 얻고 있습니다. FDA의 승인을 받은 프레제니우스 곰팡이의 Adaptive Nomogram 소프트웨어는 분석 오버레이가 성능 향상을 가져오는 방법을 보여주며, 예산에 제약이 있는 병원이 함대를 새롭게 설득하고 있습니다.

병원은 독자적인 디스포저블이 장비의 펌웨어와 동기화하고 공급업체의 장기 소모품 수입을 지원하는 통합 플랫폼을 점점 더 추구하고 있습니다. Termo의 Reveos 플랫폼은 수작업 단계를 26에서 9로 줄이고 처리량을 향출시키고 직원을 부가가치가 높은 임상 업무로 해방합니다. 경쟁의 치열성은 현장 서비스의 적용 범위와 소프트웨어의 상호 운용성을 중심으로 전개되어, 전자 의료 기록과 데이터를 연동시키는 프리미엄 기기와 연계된 아시아태평양의 아페레시스 시장 규모를 높이고 있습니다.

혈장 유래의 면역글로불린 수요가 고령화 사회에서 높아지는 가운데 2024년 총 매출액의 42.87%를 플라즈마페레시스가 차지했습니다. 국가 혈장 분획 목표로 병원은 기증자 모집을 늘리고 안정적인 키트 소비를 유지합니다. CAGR 12.87%를 나타낼 것으로 예측되는 백혈구분리술(백혈구 제거 수혈)는 고순도 단핵구 채취를 필요로 하는 혈액학과 CAR-T 파이프라인을 활용합니다. 중국의 임출시험은 최적화된 원심분리 프로토콜이 생존율을 유지하면서 2시간 이내에 백혈구 증가를 감소시키는 것으로 나타났으며, 보다 광범위한 치료법의 채택을 뒷받침하고 있습니다.

혈소판분리술는 여전히 암 치료를 지원하는데 필수적이지만, 공정의 효율화가 진행됨에 따라 양의 신장은 안정적입니다. 적혈구 타페레이시스는 겸상 적혈구 프로그램에서 틈새 견인력을 획득하고 있으며 특히 유병률이 1.8% 이상의 인도 부족 지역에서는 현저합니다. 라이트 페레시스와 지질 아페레시스와 같은 새로운 치료법은 전문센터를 매료시키고 규제 당국의 승인이 확대됨에 따라 아시아태평양의 아페레시스 산업에 상승을 가져옵니다.

The Asia Pacific Apheresis Market size is estimated at USD 0.82 billion in 2025, and is expected to reach USD 1.35 billion by 2030, at a CAGR of 10.57% during the forecast period (2025-2030).

Rapid adoption of automated blood-component technologies, expanding CAR-T cell therapy logistics, and public investment under national healthcare agendas such as "Healthy China 2030" collectively amplify procedure volumes across the region. Hospitals and blood centers are modernizing collection rooms with next-generation systems that shorten processing times, while research institutes channel grant funding toward cell-therapy-oriented leukapheresis platforms. Meanwhile, strategic localization by multinationals reduces import lead times and aligns with government procurement mandates, deepening supplier loyalty. Market risks persist around reimbursement gaps, consumable-approval inconsistencies, and shortages of certified operators, yet rising demand for precision therapies continues to outweigh these constraints, sustaining a robust long-term growth outlook for the Asia Pacific apheresis market.

Government-backed blood-safety programs are reshaping procedure volumes as China upgrades more than 450 blood centers under its "Healthy China 2030" roadmap. Capital expenditure aims squarely at automated component separation, illustrated by Terumo's USD 15 million facility in Hangzhou that manufactures Trima Accel kits locally, lowering unit cost and reducing customs delays. Indonesia's first plasma-fractionation plant targeting 600,000 liters by 2026 underscores a region-wide shift toward self-sufficiency. Standardized procurement frameworks emerging from these programs favor systems with closed-loop traceability and virus-inactivation modules, reinforcing purchasing preferences for premium platforms and propelling the Asia Pacific apheresis market.

Japan, Australia, and South Korea are front-loading budgets to secure platelet supply as aging demographics and oncology caseloads intensify. The Japanese Red Cross "Nara Regimen" expands certified operator pools through university-linked training that enhances competence on automated plateletpheresis devices. Evidence from Sanquin's deployment of Reveos shows platelet units produced per donor rising from four to five, yielding a 20% cost saving per unit. These economics encourage ministries of health to underwrite disposable budgets, accelerating uptake in the Asia Pacific apheresis market.

Fee schedules in emerging markets seldom cover disposables fully, leaving providers to absorb 20-40% of procedure cost for therapeutic apheresis. South Korea's overhaul of generic-drug pricing illustrates policymaker focus on budget ceilings rather than procedure expansion. India's Rare Diseases Policy highlights fiscal constraints, allocating only USD 3.6 million annually for a population of 1.4 billion. Consequently, cash-pay models dominate, curtailing patient access and capping near-term growth for the Asia Pacific apheresis market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Recurring demand for tubing sets, separation kits, and filters kept disposables at 62.33% of Asia Pacific apheresis market share in 2024. Steady procedure growth, stringent sterility rules, and single-use mandates ensure predictable volume gains. Bundled-pricing contracts negotiated by national blood services enhance vendor lock-in, stabilizing margins. Meanwhile, the devices segment, supported by a 14.08% CAGR, benefits from replacement cycles for legacy centrifuges reaching end-of-life and from automation upgrades that cut operator intervention by up to 65%. Fresenius Kabi's Adaptive Nomogram software, cleared by the FDA, exemplifies how analytics overlays deliver incremental performance, persuading budget-constrained hospitals to refresh fleets.

Hospitals increasingly demand integrated platforms whereby proprietary disposables synchronize with device firmware, anchoring long-run consumable revenue for suppliers. Terumo's Reveos platform reduces manual steps from 26 to 9, improving throughput and releasing staff for value-added clinical tasks. Competitive intensity revolves around field-service coverage and software interoperability, elevating the Asia Pacific apheresis market size tied to premium devices that interlock data with electronic medical records.

Plasmapheresis accounted for 42.87% of total procedure revenue in 2024 as plasma-derived immunoglobulin demand rises among aging populations. National plasma-fractionation targets push hospitals to increase donor recruitment, sustaining steady kit consumption. Leukapheresis, forecast to grow at 12.87% CAGR, capitalizes on hematology and CAR-T pipelines that require high-purity mononuclear cell collections. Clinical trials in China showed optimized centrifugation protocols lowering leukocytosis within two hours while preserving viability, supporting broader therapy adoption.

Plateletpheresis remains indispensable for oncology support, yet volume growth stabilizes as process efficiencies emerge. Erythrocytapheresis gains niche traction in sickle-cell programs, notably in India's tribal regions where prevalence exceeds 1.8%. Emerging modalities such as photopheresis and lipid-apheresis attract specialist centers, offering upside to the Asia Pacific apheresis industry as regulatory approvals widen.

The Asia Pacific Apheresis Market Report is Segmented by Product (Devices, Disposables), Procedure (Plasmapheresis, and More), Indication (Renal Disorders, and More), Technology (Centrifugal Separation, Membrane Separation), End User (Hospitals & Transfusion Centers, and More), and Country (China, Japan, India, South Korea, Australia & New Zealand, Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).