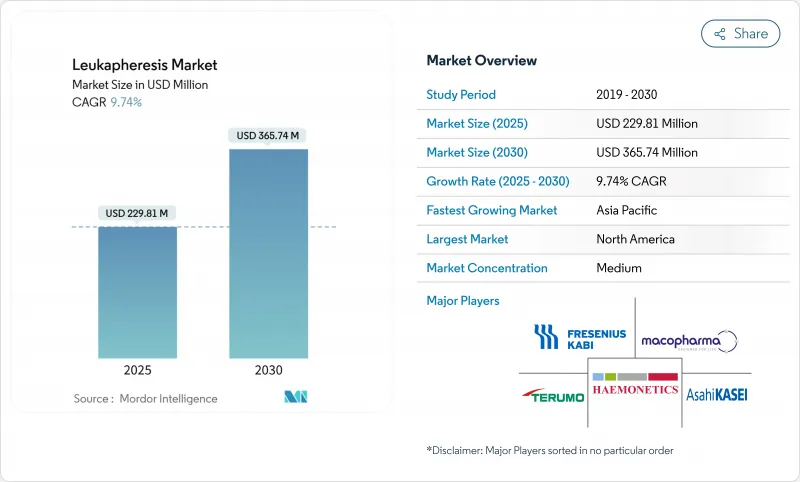

백혈구 성분채집술 시장 규모는 2025년에 2억 2,981만 달러, 예측 기간 중(2025-2030년) CAGR은 9.74%를 나타내고, 2030년에는 3억 6,574만 달러에 달할 것으로 예측됩니다.

백혈병 이환율 증가, CAR-T 상업화의 가속화, 자동 연속 흐름 애페레시스 시스템으로의 이동이 이러한 확대를 지원합니다. 병원은 고백혈구 혈증 외에도 치료 용도를 넓히고, 세포 요법 제조업체는 수집 능력을 확장하고 자가 및 새로운 동종 파이프라인을 지원합니다. 포인트 오브 케어 장비와 AI 가이드를 통한 기증자 스케줄링에 대한 투자는 처리량을 향상시키고 숙련된 전문가 부족으로 인한 압력을 완화합니다. 콜드체인 기술 혁신은 장거리 수송 중 세포 생존력을 보호하고 제조 불량률을 낮추고 최고 품질의 류코팩에 대한 수요를 강화합니다.

급성 골수성 백혈병의 발생 동향은 계속 증가하고 있으며, 세계 환자 수는 1990년 7만 9,372명에서 2021년 14만 4,645명으로, 2040년 18만 4,287명으로 증가하는 경향이 있습니다. 백혈구 수가 100,000/μl를 초과하는 것으로 정의되는 고백혈구혈증은 호흡 곤란과 신경학적 합병증을 예방하기 위해 신속한 세포 재환원이 필요합니다. 그러므로 백혈구 성분채집술은 선택적 치료에서 표준 응급 치료로 전환하고 있습니다. 남성 환자의 이환율은 여성보다 급상승하고 있으며, 80-84세의 성인이 가장 높은 이환 밀도를 나타내고 있습니다. 의료시스템의 프로토콜은 현재 적격한 백혈병 입원 환자를 자동적으로 어페레시스 유닛에 라우팅하고, 당일 액세스를 확보하고, 백혈구 어페레시스 시장의 3차 의료기관 전체의 수기량을 확고하게 하고 있습니다.

CAR-T와 천연 킬러 세포 제조업체는 1회 채취로 100억 개 이상의 단핵구를 공급하는 류코팩을 지정하는 것이 늘고 있습니다. 제조 실패율은 출발 재료의 품질과 직접 상관되며, 로이코팩이 손상되면 30만 달러의 제조가 무효화될 수 있습니다. 현재 500개 이상의 임상시험이 기증자 유래의 면역세포에 의존하고 있으며, 동종 "기성품"요법에 대한 축족이 재삼 수요를 높이고 있습니다. 자동화된 연속 유동 원심분리는 백혈구 농도를 엄격하게 설정하고 적혈구 오염을 줄이고 하류 농축을 간소화합니다. AI 스케줄링 소프트웨어가 지원하는 표준화된 공여자 스크리닝 알고리즘은 시설당 용량을 향상시켜 공급자가 직원에게 과도한 부담을 주지 않으면서 증가하는 백혈구 요구량을 수용할 수 있도록 합니다.

단일 용량 CAR-T 요법의 환자 청구 금액은 일상적으로 500,000달러를 초과하고 복잡한 소아 경우에는 1000,000달러에 도달합니다. 독립적인 민간수집센터는 병원을 거점으로 하는 것보다 32% 저렴하게 운영되고 있지만 대부분의 중저소득지역에는 그러한 시설이 없습니다. 장비의 감가상각비, 단독사용 키트, 강제적인 무균성 감사가 기준비용을 늘리고 있습니다. 메디케어의 2025년 규칙은 상환의 정의를 넓혔지만 많은 공공 시스템에는 커버 갭이 남아 있습니다. 지불 기관이 일괄 지불 모델을 중심으로 조화를 이룰 때까지는 고액의 수수료 비용은 가격에 민감한 지역에서 수요를 억제하는 것으로 예측됩니다.

백혈구 성분채집술 장치는 센터가 광검출 센서가 장착된 연속 흐름 플랫폼으로 업그레이드됨에 따라 2025-2030년 CAGR 10.85%로 성장할 전망입니다. 백혈구 성분채집술 장치 시장 규모는 2025년에 1억 1,190만 달러에 이르고, 예측 기간 동안 소모품(disposables) 시장 성장률을 웃돌 것으로 전망됩니다. Spectra Optia의 알고리즘 인터페이스와 FDA 인증 Rika Plasma Donation System V2.1은 장비 수준의 혁신의 예입니다. 제품 파이프라인에는 현재 혈액 병동과 응급실에서의 포인트 오브 케어 백혈구 감소를 목표로 하는 휴대용 침대 측 유닛이 포함되어 있습니다.

일회용은 단일 사용 안전성과 지속적인 수익 모델을 통해 2024년 백혈구 성분채집술 시장 점유율의 51.27%를 유지합니다. 처리 횟수가 증가하면 키트 판매가 안정화되고 제조업체의 현금 흐름이 향상되고 프라이밍 시간을 단축하는 통합 튜브 세트에 대한 투자가 촉진됩니다. 백혈구 제거 필터는 성숙한 틈새 분야이지만 많은 혈액 은행 프로토콜이 여전히 보편적 인 백혈구 제거를 강요하기 때문에 수요가 뿌리 깊습니다. 컬럼과 세포 분리기는 특수 병원체 제거 워크플로우를 지원하지만, 그 보급은 학술 센터에 집중되어 있습니다. 전반적으로 소모품을 자본 설비 리스로 패키징함으로써 계정 충성도를 확보하고, 이 부문의 백혈구 애페레이시스 시장에서의 리더십을 지원하고 있습니다.

북미가 2024년 점유율 45.84%로 백혈구 성분채집술 시장을 선도했습니다. 미국의 리더십은 2024년 afamitresgene autoleucel 및 obecabtagene autoleucel의 허가를 포함한 FDA 규정의 명확성과 타의 추종을 불허하는 CAR-T 승인 수에 기인합니다. 메디케어에 의한 2025년 치료적 연합에 대한 상환의 확대는 재무적 실행 가능성을 더욱 강화할 것입니다. 캐나다와 멕시코는 기증자의 물류를 간소화하는 국경을 넘는 임상시험 네트워크와 공동 제조 이니셔티브를 통해 기여하고 있습니다. Termo BCT와 Haemonetics와 같은 장비 제조업체들이 이 지역에 집중함으로써 기술 도입의 사이클이 빨라지고 북미 백혈구 애퍼레이시스 시장에서 우위를 유지할 수 있습니다.

유럽은 성숙하면서도 역동적인 시장입니다. EMA 지침은 CAR-T 제품의 일관된 평가 경로를 제공하여 고성능 백혈구 성분채집술 시스템에 대한 안정적인 수요를 촉진합니다. 유럽 혈액 동맹은 200만 명의 자발적 기증자를 추가할 것을 요구하는 캠페인을 실시하고, 혈소판 수율과 기증자의 쾌적성을 극대화하는 연속 흐름 플랫폼의 도입을 센터에 촉구하고 있습니다. 독일, 프랑스, 영국은 국가의 암 치료 계획과 관련된 통합 연합 시설에 투자하고 이탈리아와 스페인은 지역의 세포 치료 노드를 확장합니다. 공급망의 회복력, 특히 콜드체인 트럭 운송은 투자 과제를 지배하고 절차 처리 능력을 안정시킵니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 11.57%로 가장 빠른 성장을 이룹니다. 일본에서는 선진 노인의료가 프리미엄 의료기기의 보급을 견인하고 인도에서는 하이데라바드와 벵갈루루에 있어서의 정부 지원의 세포요법 클러스터가 혜택을 가져옵니다. 호주와 한국의 규제 당국은 FDA의 RMAT 지정을 반영한 가속 심사 경로를 도입하여 조기 상업 전개를 촉진합니다. 전반적으로 인프라의 현대화와 현지 제조 인센티브가 결합되어 아시아는 기술 수입처에서 백혈구 성분채집술 시장에서 완전히 통합된 공급망의 허브로 이동합니다.

The Leukapheresis Market size is estimated at USD 229.81 million in 2025, and is expected to reach USD 365.74 million by 2030, at a CAGR of 9.74% during the forecast period (2025-2030).

Rising leukemia incidence, accelerating CAR-T commercialization, and the shift toward automated continuous-flow apheresis systems anchor this expansion. Hospitals broaden therapeutic use beyond hyperleukocytosis, while cell-therapy manufacturers scale collection capacity to support autologous and emerging allogeneic pipelines. Investment in point-of-care devices and AI-guided donor scheduling improves throughput, easing the pressure created by skilled professional shortages. Cold-chain innovation safeguards cell viability during long-distance transport, lowering manufacturing failure rates and reinforcing demand for premium-quality leukopaks.

Incidence curves for acute myeloid leukemia continue to climb, with global cases moving from 79,372 in 1990 to 144,645 in 2021 and trending toward 184,287 by 2040. Hyperleukocytosis, defined as white-blood-cell counts above 100,000/µl, demands urgent cytoreduction to prevent respiratory distress and neurologic complications. Leukapheresis has therefore transitioned from elective therapy to standard emergency intervention. Male patients register steeper growth in incidence than females, while adults aged 80-84 exhibit the highest case density. Health-system protocols now automatically route eligible leukemia admissions to apheresis units, ensuring same-day access and cementing procedure volumes across tertiary centers in the leukapheresis market.

CAR-T and natural-killer-cell manufacturers increasingly specify leukopaks that deliver 10 billion or more mononuclear cells per collection. Manufacturing failure rates correlate directly with starting-material quality; a compromised leukopak can invalidate a USD 300,000 manufacturing run. Over 500 active clinical trials now depend on donor-derived immune cells, and the pivot toward allogeneic "off-the-shelf" therapies elevates recurring demand. Automated continuous-flow centrifugation secures tight leukocyte concentration windows and reduces red-cell contamination, streamlining downstream enrichment. Standardized donor-screening algorithms supported by AI scheduling software raise per-center capacity, enabling suppliers to meet escalating leukopaks requisitions without overtaxing staff.

Patient invoices for single-dose CAR-T therapies routinely exceed USD 500,000 and reach USD 1 million in complex pediatric cases, with leukapheresis comprising a meaningful early share. Stand-alone private collection centers operate 32% cheaper than hospital-based settings, yet most low- and middle-income regions lack such facilities. Equipment depreciation, single-use kits, and mandatory sterility audits inflate baseline costs. Although Medicare's 2025 rule broadened reimbursement definitions, coverage gaps linger in many public systems aabb.org. Until payors harmonize around bundled-payment models, high procedural outlay will temper demand in price-sensitive geographies.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Leukapheresis devices are expanding at a 10.85% CAGR from 2025-2030 as centers upgrade to continuous-flow platforms with optical-detection sensors. The leukapheresis market size for devices equaled USD 111.9 million in 2025 and is positioned to outpace disposables growth through the forecast. Spectra Optia's algorithmic interface and the FDA-cleared Rika Plasma Donation System V2.1 exemplify device-level innovation. Product pipelines now include portable bedside units that target point-of-care leukoreduction in hematology wards and emergency departments.

Disposables retained 51.27% of leukapheresis market share in 2024 due to their single-use safety profile and recurring-revenue model. Elevated procedure volumes ensure consistent kit sales, reinforcing manufacturer cash flows and incentivizing investment in integrated tubing sets that cut priming times. Leukoreduction filters remain a mature niche, yet demand persists because many blood-bank protocols still enforce universal leukocyte reduction. Columns and cell separators support specialized pathogen-reduction workflows, though their penetration concentrates in academic centers. Overall, packaging disposables with capital-equipment leases locks in account loyalty, anchoring the segment's leadership within the leukapheresis market.

The Leukapheresis Market Report is Segmented by Product Type (Leukapheresis Devices [Apheresis Devices, and More], and Leukapheresis Disposables), Application (Therapeutic Applications and Research Applications), End User (Blood Centers & Donor Clinics, Hospitals & Transplant Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led the leukapheresis market with a 45.84% share in 2024. U.S. leadership stems from FDA regulatory clarity and unmatched CAR-T approval volume, including the 2024 clearances of afamitresgene autoleucel and obecabtagene autoleucel. Medicare's 2025 reimbursement expansion for therapeutic apheresis further bolsters financial viability. Canada and Mexico contribute through cross-border clinical-trial networks and joint manufacturing initiatives that streamline donor logistics. Concentration of device makers such as Terumo BCT and Haemonetics within the region speeds tech adoption cycles, sustaining North America's prime position in the leukapheresis market.

Europe remains a mature yet dynamic arena. EMA guidelines deliver consistent evaluation pathways for CAR-T products, fostering steady demand for high-performance leukapheresis systems. The European Blood Alliance campaigns for two million additional voluntary donors, incentivizing centers to adopt continuous-flow platforms that maximize platelet yield and donor comfort. Germany, France, and the United Kingdom invest in integrated apheresis suites tied to national cancer plans, while Italy and Spain expand regional cell-therapy nodes. Supply-chain resilience, particularly in cold-chain trucking, dominates investment agendas and stabilizes procedure throughput.

Asia Pacific posts the fastest growth at an 11.57% CAGR to 2030. Japan's advanced geriatric care drives premium device uptake, whereas India benefits from government-backed cell-therapy clusters in Hyderabad and Bengaluru. Regulatory authorities in Australia and South Korea introduce accelerated review pathways mirroring FDA's RMAT designation, catalyzing early commercial rollouts. Overall, infrastructure modernization, coupled with local manufacturing incentives, transitions Asia from technology import destination to fully integrated supply-chain hub in the leukapheresis market.