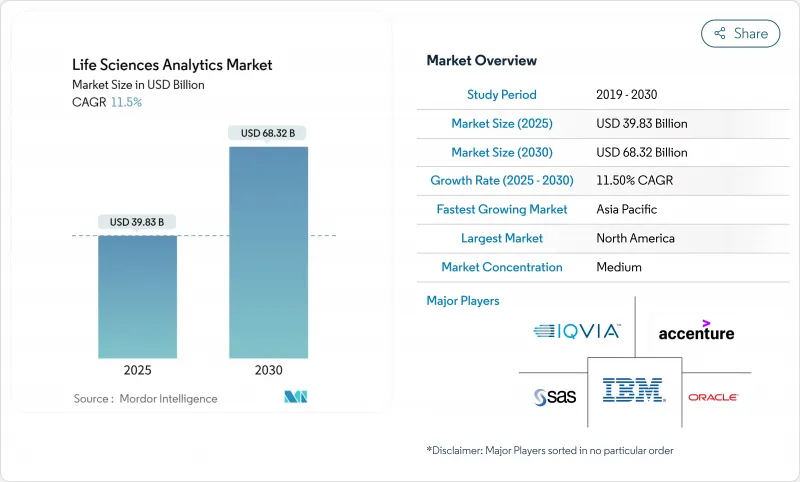

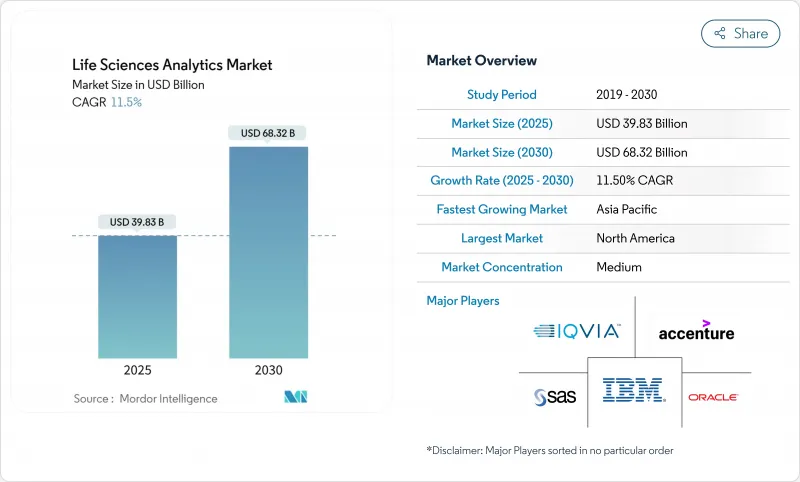

세계의 생명과학 분석 시장 규모는 2025년 398억 3,000만 달러로, 2030년까지 683억 2,000만 달러에 이를 것으로 보이며, 2025년부터 2030년까지 CAGR 11.5%로 확대될 것으로 예측됩니다.

이 기세는 증가하는 생물 의학 데이터를 연구, 개발, 제조 및 상용화에 걸쳐 빠르고 신뢰할 수 있는 실용적인 인텔리전스로 변환하는 것이 급선무가 되었기 때문입니다. 클라우드 아키텍처의 채용이 가속화되고, 생성형 AI가 진보하고, 규제 당국이 실세계의 근거를 중시하는 것으로, 발견 사이클이 단축되어, 출시 성공률이 향상하고 있습니다. 공급업체는 유전체, 임상 및 상업 정보를 단일 프레임워크로 통합하는 멀티모달 분석에 진출하고 있으며 생명 과학 기업은 데이터 거버넌스를 재설계하고 대규모 협업을 지원합니다. 기술 대기업이 이 영역에 진입해, AI 네이티브의 스페셜리스트가 워크플로우의 갭을 노리고 있는 가운데, 경쟁은 격렬해지고 있습니다.

조직은 현재 페타바이트급 구조화 및 비구조화 생물의학 정보를 처리하고 있습니다. 단일 세계 데이터 어그리게이터는 이미 64페타바이트 이상을 관리하고 있으며 현대 애널리틱스에 필요한 규모의 극적인 변화를 드러내고 있습니다. 통합의 과제는 단순한 집계에서 임상, 유전체, 실세계의 데이터를 연결하는 시맨틱 모델의 작성으로 발전하고 있습니다. 통합 데이터 패브릭에 투자하는 팀은 탐색주기를 단축하고 초기 단계에서 성공 확률을 높입니다. 일반 AI 워크플로우의 급속한 보급은 반복적인 가설 검증과 지속적인 학습을 지원하는 멀티모달 리포지토리에 대한 수요를 강화하고 있습니다. 데이터의 다양성이 이미지와 웨어러블로 확대되는 동안 자동 데이터 정합을 제공하는 공급업체는 생명 과학 분석 시장에서 점유율을 확대하는 입장에 있습니다.

실세계 증거를 중시하는 규제로 데이터 거버넌스는 비용 센터에서 혁신 기폭제로 바뀌었습니다. 제조업체는 안전 신호를 조기에 감지하고 지속적인 이익 위험 평가에 대한 규제 당국의 기대에 부응하기 위해 애널리틱스를 시판 후 조사 시스템에 통합합니다. 컴플라이언스 워크플로우를 통찰력 엔진으로 전환한 기업은 전통적으로 수작업으로 보고한 리소스를 되찾았습니다. 주목할 만한 성과는 신호 검증의 신속화, 검사 소견의 감소, 라벨의 확대를 서포트하는 근거의 확대 등을 들 수 있습니다. 지역간 규제기술 스택을 조정하는 다국적 기업도 성장 시장에서 제품 제공을 가속화하고 있어 생명과학 분석 시장의 확대 전망을 강화하고 있습니다.

GDPR(EU 개인정보보호규정) 및 CCPA와 같은 규정은 엄격한 동의, 보존 및 이전 규칙을 도입하고 애널리틱스 프로젝트의 규정 준수 장애물을 제고합니다. 다국적 스폰서는 지역별 규정을 충족하기 위해 중복된 데이터 환경을 유지해야 하며 운영상의 간접비가 증가합니다. Privacy-By-Design(PBD) 아키텍처, 토큰화 및 페더레이티드 학습은 정보 유출을 줄이면서 도입 기간을 늘립니다. 규칙은 사회적 신용을 향상시키지만 복잡성이 증가하면 실험에 시간이 걸리고 국경을 넘은 데이터 풀도 제한되기 때문에 생명 과학 분석 시장의 단기적 및 중기적인 성장은 억제됩니다.

기술적 분석은 2024년 생명과학 애널리틱스 시장 점유율의 45.0%를 차지했습니다. 이는 기업이 시험 이정표, 제조 편차, 판매 패턴을 모니터링하기 위해 소급 대시보드에 의존하기 때문입니다. 이 부문은 과거의 맥락이 모든 다운스트림 모델링의 기초가 되기 때문에 여전히 중심적인 역할을 합니다. 새로운 기능 향상에는 비기술적 사용자에 대한 액세스를 확대하는 자연 언어 요약과 검토 주기를 단축하는 자동화된 근본 원인 분석이 포함됩니다.

그러나 2030년을 향해 가장 빠르게 성장하는 것은 처방적 분석입니다. 기업이 리포팅에서 의사 결정 오케스트레이션으로 중심을 옮기고 최적화 알고리즘을 테스트 디자인, 공급망 라우팅 및 옴니채널 참여에 통합하면 채택이 가속화됩니다. 조기 진출 기업은 프로토콜 수정을 줄이고 타겟팅된 캠페인에서 응답률을 높였다는 기록을 남기고 처방적 접근에 대한 신뢰를 강화하고 있습니다. 통합 AI 모듈이 성숙하고 클라우드 용량이 유비쿼터스화가 됨에 따라 처방 솔루션의 생명 과학 분석 시장 규모가 빠르게 확대될 것으로 예측됩니다. 분석가들은 10년이 끝날 무렵에는 기술적 지출과 처방적 지출 간의 균형이 역전되고 데이터 중심의 의사결정이 업계의 핵심에 자리매김할 것으로 예상하고 있습니다.

대규모의 구현, 커스터마이즈, 트레이닝의 필요성으로부터, 2024년 매출은 서비스가 55.3%를 차지했습니다. 컨설팅 팀은 데이터 클렌징, 모델 개발, 사용자 도입을 지도하고 지속적인 서비스 매출을 견인합니다. 그러나 플랫폼의 표준화와 셀프 서비스 툴의 개선으로 순수한 서비스 수요는 감소하고 있습니다.

현재 가장 높은 증가율을 보인 부문은 소프트웨어 플랫폼입니다. 공급업체는 데이터 레이크, 피처 스토어, 모델 팩토리 및 시각화 레이어를 통합하고 엔드 투 엔드 워크플로우를 지원하는 통합 제품을 제공합니다. 로우코드 인터페이스를 통해 도메인 전문가는 프로그래밍 없이 예측 파이프라인을 구축할 수 있어 민주화가 가속화되고 있습니다. 플랫폼 구독과 관련된 생명 과학 분석 시장 규모는 경상 수익 가능성과 클라우드를 통한 신속한 세계 배포에서 혜택을 누릴 수 있습니다. 업계 이해관계자들은 구성 가능성이 넓어지고 패키징된 규정 준수 기능이 지역 간의 커스터마이즈 요구를 억제하기 때문에 5년 이내에 소프트웨어가 서비스를 추월할 것으로 예측했습니다.

북미는 2024년 생명과학 분석 시장의 41.3%를 차지했으며 견조한 바이오의약품 R&D 파이프라인, 광범위한 실제 데이터 네트워크, 유리한 지불자 인센티브가 이를 지원하고 있습니다. 미국은 AI에 특화된 생명과학 분석 시장을 보유하고 있으며 이 지역 수요를 지배하고 있습니다. 실세계에서의 증거 수집과 신속한 패스웨이를 촉진하는 연방 정부의 이니셔티브는 개발 라이프사이클 전반에 걸쳐 애널리틱스 채택에 계속 박차를 가하고 있습니다.

아시아태평양은 가장 급성장하는 지역으로 2025년부터 2030년까지 CAGR 12.6%를 보일 것으로 예측되고 있습니다. 중국과 인도는 임상시험 생태계 확대, 정밀의료에 대한 정부 인센티브, 벤처캐피탈 유입 급증으로 이끌고 있습니다. 국경을 넘어서는 라이선스 계약은 세계적인 분자를 현지 프로그램에 도입하여 분산된 시험 업무를 조정하고 이종 환자 코호트를 평가하기 위한 분석에 대한 의존도를 높이고 있습니다. 싱가포르와 한국과 같은 국가들은 생물 의학 AI에 대한 보조금 제공을 강화하고 있으며 지역 기세를 더욱 가속화하고 있습니다.

유럽은 여전히 영향력 있는 지역입니다. 독일, 영국, 프랑스의 강력한 학술 네트워크가 참신한 분석 기법을 창출하고 유럽 의약품청(European Medicines Agency)이 새로운 증거 유형에 개방되어 플랫폼 수요를 뒷받침하고 있습니다. GDPR(EU 개인정보보호규정)의 엄격한 요건은 즉각적인 규모 확장을 억제하지만 프라이버시 보호 계산의 진보를 촉진하고 있습니다. 중동 및 아프리카, 남미에서는 소규모이면서 가속도적으로 제조거점과 연구협력이 확대되어 미래의 생명과학 분석 시장 성장의 무대가 갖추어지고 있습니다.

In 2025, the life science analytics market size is valued at USD 39.83 billion and is projected to reach USD 68.32 billion by 2030, growing at an 11.5% CAGR from 2025 to 2030.

Momentum stems from the urgent need to convert growing biomedical data volumes into fast, reliable, and actionable intelligence across research, development, manufacturing, and commercialization. Accelerated adoption of cloud architectures, progress in generative AI, and regulatory emphasis on real-world evidence are combining to shorten discovery cycles and improve launch success. Vendors are expanding into multimodal analytics that unify genomic, clinical, and commercial information in a single framework, while life science companies are redesigning data governance to support collaboration at scale. Competitive intensity is rising as technology giants enter the domain and AI-native specialists target workflow gaps.

Organizations now process petabytes of structured and unstructured biomedical information. A single global data aggregator already manages more than 64 petabytes, underscoring the dramatic scale shift required for contemporary analytics. The integration challenge has evolved from simple aggregation to the creation of semantic models that connect clinical, genomic, and real-world data. Teams that invest in unified data fabrics are trimming discovery cycles and boosting early-stage success probabilities. Rapid uptake of generative AI workflows is reinforcing demand for multi-modal repositories, which support iterative hypothesis testing and continuous learning. As data diversity broadens to include imaging and wearables, vendors offering automated data harmonization stand to gain share in the life science analytics market.

Regulatory focus on real-world evidence has turned data governance from a cost center into an innovation catalyst. Manufacturers are embedding analytics into post-market surveillance systems to detect safety signals earlier and meet regulator expectations for ongoing benefit-risk evaluation. Companies that transform compliance workflows into insight engines are reclaiming resources otherwise reserved for manual reporting. Notable results include faster signal validation, reduced inspection findings, and a larger body of evidence to support label expansions. Multinational firms that align regulatory technology stacks across regions are also accelerating product availability in growth markets, reinforcing expansion prospects for the life science analytics market.

Regulations such as GDPR and CCPA introduce strict consent, storage, and transfer rules that raise the compliance bar for analytics projects. Multinational sponsors must maintain duplicative data environments to satisfy territorial mandates, increasing operational overhead. Privacy-by-design architectures, tokenization, and federated learning mitigate exposure yet lengthen deployment timelines. While the rules improve public trust, the added complexity can slow experiments and limit cross-border data pooling, tempering short-to-mid-term growth of the life science analytics market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Descriptive analytics commanded 45.0% of the life science analytics market share in 2024 as companies relied on retrospective dashboards to monitor trial milestones, manufacturing deviations, and sales patterns. The segment remains central because historical context underpins all downstream modeling. Emerging enhancements include natural language summaries that widen access to non-technical users and automated root-cause analysis that shortens review cycles.

Prescriptive analytics, however, delivers the fastest growth trajectory to 2030. Adoption accelerates as enterprises pivot from reporting to decision orchestration, embedding optimization algorithms into study design, supply chain routing, and omnichannel engagement. Early movers record reduced protocol amendments and higher response rates in targeted campaigns, reinforcing confidence in prescriptive approaches. The life science analytics market size for prescriptive solutions is projected to expand rapidly as integrated AI modules mature and cloud capacity becomes ubiquitous. Analysts expect the balance between descriptive and prescriptive spend to invert by the decade's close, positioning data-driven decisioning at the industry core.

Services captured 55.3% revenue in 2024 due to extensive implementation, customization, and training needs. Consulting teams guide data cleansing, model development, and user adoption, driving sustained service billings. Growing platform standardization and improved self-service tooling, however, are chipping away at pure service demand.

Software platforms now post the highest incremental growth. Vendors combine data lakes, feature stores, model factories, and visualization layers in unified offerings that support end-to-end workflows. Low-code interfaces enable domain experts to build predictive pipelines without programming, accelerating democratization. The life science analytics market size tied to platform subscriptions benefits from recurring revenue potential and rapid global deployment via the cloud. Industry stakeholders anticipate that software will overtake services within five years as configurability widens and packaged compliance features curb customization needs across regions.

The Life Science Analytics Market Report is Segmented by Product Type (Descriptive Analytics, and More), Component (Software Platforms, and Services), Deployment Mode (On-Premise, and More), Application (Research & Development, and More), End User (Pharmaceutical & Biotech Companies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 41.3% of the life science analytics market in 2024, anchored by robust biopharma R&D pipelines, extensive real-world data networks, and favorable payer incentives. The United States dominates regional demand, with its AI-specific life science analytics market. Federal initiatives that promote real-world evidence collection and fast-track pathways continue to spur analytics adoption across the development lifecycle.

Asia-Pacific is the fastest-growing region, projected to record a 12.6% CAGR from 2025 to 2030. China and India lead with expanding clinical trial ecosystems, government incentives for precision medicine, and surging venture capital inflows. Cross-border licensing agreements channel global molecules into local programs, increasing reliance on analytics to coordinate distributed study operations and evaluate heterogenous patient cohorts. Nations such as Singapore and South Korea are stepping up grant funding for biomedical AI, further amplifying regional momentum.

Europe remains an influential player. Strong academic networks in Germany, the United Kingdom, and France generate novel analytical methods, while the European Medicines Agency's openness to new evidence types boosts platform demand. Strict GDPR requirements temper immediate scaling but encourage advances in privacy-preserving computation. Smaller but accelerating markets in the Middle East, Africa, and South America are also expanding their manufacturing bases and research collaborations, setting the stage for future life science analytics market growth.