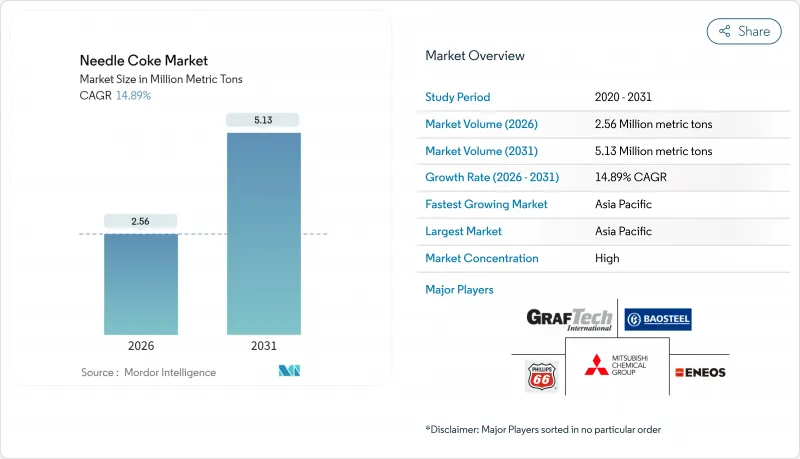

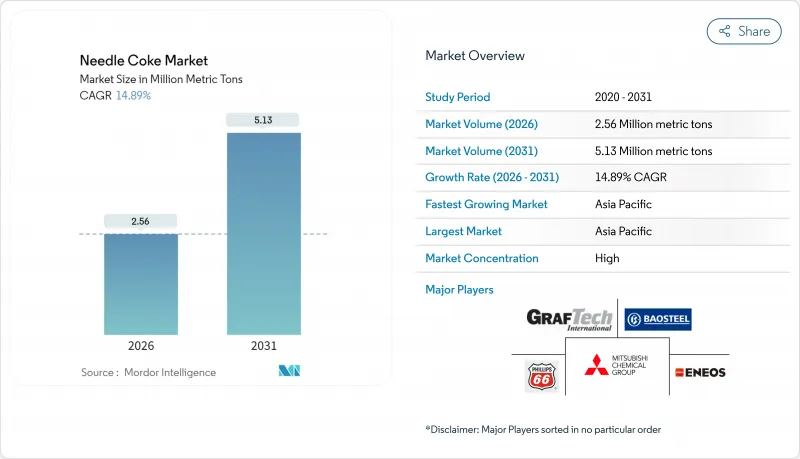

니들 코크스 시장은 2025년 223만 메트릭톤으로 평가되었으며, 2026년 256만 메트릭톤에서 2031년까지 513만 메트릭톤에 이를 것으로 예상됩니다.

예측 기간(2026-2031년)에 있어서 CAGR은 14.89%를 나타낼 것으로 전망되고 있습니다.

이 급격한 상승은 전기 아크로(EAF) 제강과 리튬 이온 배터리 제조라는 세계의 탄소 재료 수요를 재구성하는 두 분야의 병렬 성장으로 인한 것입니다. 철강 산업에서 EAF 기술로의 전환은 초고전력 흑연 전극 수요를 가속화하고 전기자동차 붐은 합성 흑연 음극재 수요를 확대하고 있습니다. 원료 공급 희박, 생산 지리적 집중, 새로운 무역 규제가 함께 니들 코크스 시장 전체에서 지속적인 공급 희박 상태가 생겨 가격 상승 동향을 강화하고 있습니다. 안정적인 디캔트 오일 공급과 첨단 지연 코크스화 설비를 보유한 생산자들은 여전히 가격 결정력을 장악하고 있습니다.

세계 철강 제조업체는 탄소 배출량을 줄이고 원료 유연성을 향상시키기 위해 고로에서 전기로(EAF) 기술로의 전환을 가속화하고 있습니다. 전기로 설비는 이미 세계 철강 생산량의 30%를 차지하고 있으며 2025년 말까지 계획된 증산 용량의 43%를 차지했습니다. 인도의 국가철강 정책에서는 2030년까지 전기로 비율 40%를 목표로 하고 있으며, 중국도 2025년까지 15%의 전기로 비율을 달성했습니다. 신규로의 가동에는 고품질의 석유 니들 코크스를 원료로 하는 초고전력 전극이 필수적이며, 철강 탈탄소화는 니들 코크스 시장 전체 수요 증가에 직결합니다. 전기로 프로젝트에 대한 설비투자는 여전히 아시아태평양이 중심이지만, 북미의 주요 철강 제조업체도 지속가능성 목표 달성과 풍부한 스크랩 공급 활용을 목적으로 전기로를 증설 중입니다. 이 동향에 의해 복수년에 걸친 인수 계약이 확정되어, 코크스 통합 생산 제조업체의 증산 의욕이 높아지고 있습니다.

리튬 이온 배터리의 제조 규모는 기존 예측을 능가하는 속도로 확대되고 있습니다. 2023년에는 세계 EV용 배터리 공장에서 63만 톤 이상의 흑연이 소모되어 새로운 기가팩토리의 가동 개시에 따라 이 수치는 2020년대 중반까지 두배로 될 것으로 전망되고 있습니다. 합성 흑연은 급속 충전시 안정성과 순도에서 중요한 성능 우위를 가지며 고에너지 밀도 음극재의 보급률 상승을 지지하고 있습니다. 공급 확보를 위해, 자동차 제조업체 각사는 니들 코크스계 합성 흑연 공급자와 장기 계약을 체결하고 있습니다. 예를 들어 파나소닉 에너지는 NOVONIX사와 2025년 납입 개시 계약을 체결했습니다. 부극재 수요의 급증에 의해 석유 유래의 니들 코크스가 종래 철강 고객용으로부터 전용되고, 세계의 원료 공급원이 희박합니다. 이것은 니들 코크스 시장에서 우량 생산자의 이익률 상승을 지원합니다.

미국 환경보호청(EPA)의 2024년 코크스로 규제에서는 문에서의 누출 제로와 벤젠 계속 감시가 의무화되어 사업자는 배출제어장치의 개수를 촉구했습니다. 40 CFR Part 63에 근거한 유사한 조치는 정유소 코크스 드럼의 모니터링을 강화하고 컴플라이언스 비용과 가동 중단 위험을 증가시킵니다. 이러한 의무는 단기적으로 생산량을 압박하고 확장 의욕을 억제함과 동시에 신규 생산 능력을 보다 규제가 느린 지역으로 이동시킬 가능성이 있습니다. 니들 코크스 시장에서는 수요 감속보다 공급 제약이 먼저 나타나고 가격 변동성을 증폭시킬 전망입니다.

석유계 원료는 2025년에 니들 코크스 시장 점유율의 85.12%를 차지했고 2031년까지 연평균 복합 성장률(CAGR) 16.05%로 확대될 것으로 예측되고 있습니다. 본 부문은 확립된 지연 코크스화 인프라, 신뢰할 수 있는 FCC 디캔터 오일 공급, 초고출력 전극의 공차를 만족하는 우수한 결정 배향성을 강점으로 하고 있습니다. 2025년에는 약 190만 톤으로 성장했고 2031년까지 450만 톤을 넘을 전망이며, 탄소 재료 밸류 체인 전체에 있어서 석유계 니들 코크스 시장의 확대 경향이 부각되고 있습니다. 합성 흑연 음극의 채용이 더욱 성장의 추풍이 되는 한편, 미국 및 서유럽에 있어서 정유소의 합리화에 의해 지역적인 원료 부족이 발생하고 있습니다. 아시아의 정유소는 플렉서블 코크스 장치의 가동을 계속하고 있어, 다른 지역에서공급 감소분을 일부 상쇄하고 있습니다.

콜타르 피치계 제품이 남은 시장을 차지하고 있습니다만, 전극·전지 제조업체에 있어서 중요한 다양화 수단을 제공합니다. 기술적 과제가 있는 것, 2개의 상업용 석탄 니들 플랜트는 2024년까지 안정된 생산을 유지했습니다. 야금용 코크스로와의 업스트림 통합은 철강 사이클이 호조인 시기에 사업자에게 추가적인 비용 우위성을 가져옵니다. 성장 가능성은 피치 공급량의 제약으로 인해 두드리는 상태이지만, 단계적인 병목 현상 해소에 의해 부문의 중요성은 유지되고 있습니다. 촉매 보조 그라파타이제이션에 관한 조사의 진전에 의해 석탄 니들 코크스의 품질 향상을 도모하면, 니들 코크스 시장에서 이 제품의 점유율 확대가 기대됩니다.

본 니들 코크스 시장 보고서는 제품 유형(석유계 니들 코크스, 콜타르 피치계 니들 코크스), 용도(흑연 전극, 리튬 이온 전지, 기타 용도), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분석했습니다. 시장 예측은 수량(메트릭톤)으로 제공됩니다.

아시아태평양은 니들 코크스 시장의 87.74%를 차지하며 2031년까지 연평균 복합 성장률(CAGR) 15.49%를 유지할 것으로 예측됩니다. 중국은 공급과 수요를 모두 견인하고 있으며, 2023년에는 9억톤 이상의 조강을 생산하여 세계 최대의 배터리용 음극재 생산 능력을 보유하고 있습니다. 2023년 말 도입된 고순도 흑연의 수출 허가 요건으로 베이징의 수출량은 전년 대비 91% 감소했습니다. 이 움직임은 서유럽 구매자공급망 경계감을 높였습니다. 인도는 2035년까지 연간 2억 4,000만-2억 6,000만 톤의 강철 생산을 목표로 하고 전기로(EAF)의 보급률을 40%로 끌어올릴 의향이기 때문에 수요 증폭 요인으로 부상하고 있습니다.

북미는 기반 규모가 작은 것, 현지화를 통한 전략적 중요성을 늘리고 있습니다. 중국산 흑연에 대한 93.5%의 관세 제안은 워싱턴의 자급자족에 대한 주력을 부각하고 있습니다. 유럽에서는 순환형 경제의 철강 생산과 전지 재활용을 정책이 뒷받침해 완만한 수량 성장이 전망됩니다. 핀란드의 스토라 엔소 사에 의한 리그닌 흑연 플랜트는 저탄소 음극재에 대한 대처를 상징하고 있습니다.

남미, 중동, 아프리카 등의 지역은 도입 단계가 비교적 초기이지만 관심이 높아지고 있습니다. 사우디아라비아는 2024년 셰브론 램머스 세계에 연간 7만 5,000톤의 니들 코크스 복합 시설의 라이선스를 수여해 중동의 특수 코크스에 최초의 대규모 진출이 되었습니다. 한편 이집트와 브라질 등 신흥 철강 클러스터에서는 수입 의존도를 줄이기 위해 현지에서의 전극 공급 가능성을 모색하고 있습니다.

The Needle Coke Market was valued at 2.23 million metric tons in 2025 and estimated to grow from 2.56 million metric tons in 2026 to reach 5.13 million metric tons by 2031, at a CAGR of 14.89% during the forecast period (2026-2031).

This rapid upswing stems from the parallel rise of electric-arc-furnace (EAF) steelmaking and lithium-ion battery manufacturing, two sectors that together reshape global carbon material demand. The steel industry's move toward EAF technology is intensifying the call for ultra-high-power graphite electrodes, while the electric-vehicle boom is expanding synthetic-graphite anode requirements. Tight feedstock availability, geographic concentration of production, and new trade controls are creating persistent supply tension that reinforces upward pricing trends across the needle coke market. Producers with secure decant-oil supply and advanced delayed-coking assets continue to control pricing power.

Global steelmakers are accelerating the shift from blast furnaces to EAF technology to cut carbon emissions and improve raw-material flexibility. EAF installations already contribute 30% of world steel output and account for 43% of planned capacity additions slated for late 2025. India's National Steel Policy targets an EAF share of up to 40% by 2030, while China seeks a 15% EAF contribution by 2025. Each new furnace requires ultra-high-power electrodes that rely on premium petroleum-needle coke, so steel decarbonization directly enlarges overall needle coke market demand. Capital spending on EAF projects remains focused in Asia-Pacific, yet North American steel majors are also adding arc furnaces to meet sustainability goals and capitalize on abundant scrap supply. The trend locks in multi-year offtake commitments and encourages integrated coke producers to expand capacity.

Lithium-ion battery manufacturing is scaling at a pace that exceeds earlier forecasts. Global EV battery plants consumed more than 630,000 tons of graphite in 2023, a figure expected to multiply by mid-decade as new giga-factories begin operations. Synthetic graphite holds critical performance advantages in fast-charge stability and purity, underpinning rising penetration rates within high-energy-density anodes. To secure supply, automotive OEMs have struck long-term agreements with needle-coke-based synthetic-graphite suppliers such as Panasonic Energy's pact with NOVONIX that commences deliveries in 2025. The surge in anode demand draws petroleum-based needle coke away from traditional steel customers, tightening the global feedstock pool and supporting elevated margins for qualified producers inside the needle coke market.

The U.S. Environmental Protection Agency's 2024 coke-oven rule mandates zero leaking doors and continuous benzene monitoring, pushing operators to retrofit emission controls. Similar measures under 40 CFR Part 63 tighten oversight of refinery coking drums, escalating compliance spend and downtime risk. These obligations strain output in the near term, curb expansion appetite, and may shift new capacity to regions with less stringent frameworks. For the needle coke market, supply constraints materialize faster than demand moderation, amplifying volatility.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Petroleum-based material captured 85.12% of the needle coke market share in 2025 and is forecast to advance at a 16.05% CAGR to 2031. The segment benefits from established delayed-coking infrastructure, reliable FCC decant-oil supply, and superior crystalline orientation that meets ultra-high-power electrode tolerances. It grew to roughly 1.90 million tons in 2025 and should exceed 4.50 million tons by 2031, underscoring the rising petroleum needle coke market size within the larger carbon-materials value chain. Adoption of synthetic-graphite anodes injects additional momentum, but refinery rationalization in the United States and Western Europe introduces regional feed shortages. Asian refiners continue to commission flexi-coker units, offsetting partial supply loss elsewhere.

Coal-tar-pitch-based products occupy the remaining volume but supply an important diversification lever for electrode and battery producers. Despite technical hurdles, the two commercial coal-needle plants maintained stable output through 2024. Upstream integration with metallurgical coke ovens gives operators incremental cost advantages when steel cycles are favorable. Growth potential stays capped by limited pitch availability, yet incremental debottlenecking keeps the segment relevant. Ongoing research into catalyst-assisted graphitization may elevate coal-needle quality, broadening its addressable share in the needle coke market.

The Needle Coke Market Report is Segmented by Product Type (Petroleum-Based Needle Coke and Coal-Tar Pitch-Based Needle Coke), Application (Graphite Electrodes, Lithium-Ion Batteries, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Metric Tons).

Asia-Pacific leads with 87.74% of the needle coke market and is projected to preserve a 15.49% CAGR through 2031. China anchors both supply and demand, producing more than 900 million tons of crude steel in 2023 and operating the world's largest battery-anode capacity. Beijing's export license requirement for high-purity graphite introduced in late 2023 reduced outbound shipments by 91% year on year, a development that heightened supply-chain vigilance among Western buyers. India emerges as a demand multiplier as it targets 240-260 million tons of annual steel by 2035 and intends to lift EAF penetration to 40%.

North America accounts for a smaller base yet gains strategic relevance through localization. Tariff proposals of 93.5% on Chinese graphite underscore Washington's focus on self-reliance. Europe holds moderate volume growth as policy favors circular-economy steel production and battery recycling. Stora Enso's lignin-graphite plant in Finland signals commitment to lower-carbon anode material.

Other territories such as South America, the Middle East, and Africa are at earlier adoption stages but record growing interest. Saudi Arabia awarded Chevron Lummus Global a 75,000 TPA needle-coke complex license in 2024, marking the Middle East's first large-scale entry into specialty coke, while emerging steel clusters in Egypt and Brazil explore local electrode supply to reduce import exposure.