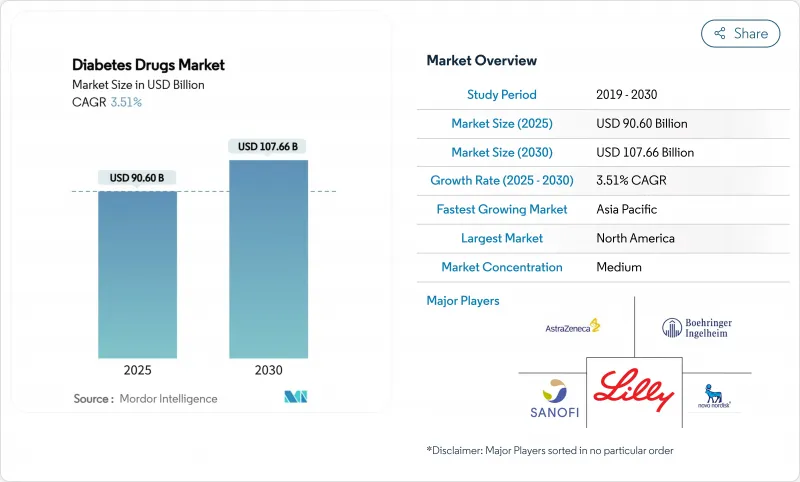

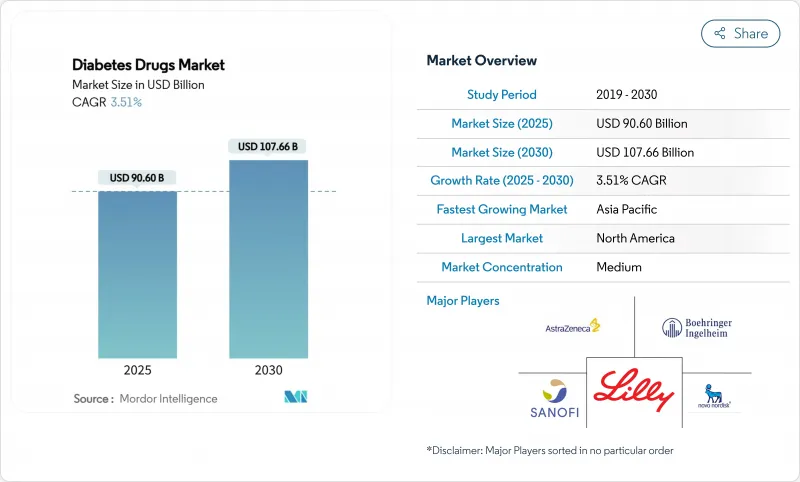

당뇨병 치료제 시장 규모는 2025년에 906억 달러로 추정되고, 예측 기간(2025-2030년) CAGR 3.51%로 성장할 전망이며, 2030년에는 1,076억 6,000만 달러에 달할 것으로 예측됩니다.

지속적인 성장의 배경은 세계적인 당뇨병 부담의 가속화, 진단의 조기화, 혈당 조절 및 체중 관리 효과를 결합한 혁신적인 치료법의 급속한 보급입니다. 인슐린은 여전히 필수적이지만, 수요는 GLP-1 수용체 작용제 및 기타 비인슐린 주사제에 기울어지고 있습니다. 경구 펩타이드 기술, 바이오시밀러 기저 인슐린, 디지털화된 케어 모델은 비용을 절감하면서 환자 접근을 확대하고 있습니다. 경쟁 환경은 치열해지고 있으며 기존 기업은 제조 및 디지털 에코시스템의 규모를 확대하고 가치 중심의 환경에서 점유율을 보호하려고 합니다.

2024년에는 8억 2,800만 명 이상의 성인이 당뇨병을 앓았고, 1990년의 4배가 되었습니다. 저소득 지역의 조기 스크리닝 프로그램은 치료 대상을 확대하고 치료 기간을 연장하고 있습니다. GLP-1 효능제의 조기 사용을 지지하는 WHO의 새로운 지침은 1차 치료에 대한 고급 주사제의 통합을 강화하는 것입니다. 비만과 당뇨병의 중복은 많은 GLP-1 제형이 이중 적응을 갖게 되었기 때문에 수요를 더욱 증가시키고 있습니다. 이러한 변화는 당뇨병 치료제 시장의 장기적인 수량 성장을 지원합니다.

당뇨병에 대한 의약품 지출은 2023년 19% 상승해 의료 전체 인플레이션을 웃돌았습니다. 당뇨병 시장 조사에 따르면, 합병증의 발생률이 감소함에 따라 목표 지출이 상쇄되기 때문에 지불자는 보다 고액의 치료제에 자금을 제공합니다. 고용주의 의료보험제도는 이용관리를 강화하면서도 가치가 높은 의약품에 대한 접근을 유지한다는 큰 압력에 직면하고 있습니다. 이러한 지출의 기세는 단가가 정밀하게 되어도 가격 실현을 유지하고 임상적 및 경제적 리턴이 명확한 혁신적 제품에 이익을 가져오고 있습니다.

췌장염 보고는 파마코비질런스의 강화와 보수적인 환자 선택을 촉진하고 있습니다. 췌장염의 발생률은 여전히 낮으며, 처방자에 의한 주의 환기가 고위험군에서의 복용을 지연시켜 GLP-1의 급격한 매출 증가를 억제할 가능성이 있습니다. 제조업체 각 회사는 이익 위험 프로파일을 보호하기 위해 교육 및 시판 후 조사를 지원합니다.

2024년 당뇨병 치료제 시장에서 인슐린의 점유율은 55%를 유지했고, 1형 및 진행 2형 관리에서 인슐린의 중심적인 역할이 강조되었습니다. 그러나 GLP-1 수용체 작용제의 CAGR은 4.5%로 확대되고 있으며, 이는 기존의 혈당 조절 이외에도 처방의 폭을 넓히는 체중 감량 효과에 뒷받침되고 있습니다. GLP-1 제제 시장 규모는 2030년까지 1,500억 달러에 달할 것으로 예상되며, 이는 GLP-1 제제의 이중 적응의 매력을 반영합니다. 경구 SGLT-2 억제제는 당뇨병 치료 시장에서 주사제의 귀중한 보조제 또는 대체제로 자리매김하는 장기 보호 데이터에 의해 지원되며, 계속해서 지지를 모으고 있습니다.

이 부문에서 경쟁 구도는 격렬합니다. 현재 노보 노르디스크와 엘리 릴리가 거의 모든 점유율을 차지하고 있는 것으로 추정되지만, 듀얼 효능자와 트리플 효능제 파이프라인이 새로운 경쟁을 약속하고 있습니다. 인슐린 데글루데크 및 릴라글루티드펜과 같은 합제는 투여 방법의 혁신이 어떻게 어드히어런스의 이점을 보장하고 제품 수명주기을 연장할 수 있는지를 보여줍니다.

북미가 2024년 매출액에 42% 기여해 리더십을 유지했습니다. 광범위한 보험 적용 범위, 강력한 전문 의료 인프라, GLP-1 제제의 조기 도입이 이 지역의 이점을 지원합니다. 인슐린의 저가격화에 관한 법률도 가격 확대를 억제하면서도 환자의 비용 부담을 경감함으로써 수요를 자극하고 있습니다. 고용주는 GLP-1의 성장을 관리하기 위해 사전 승인 프로토콜을 개선했지만 지속적인 임상 가치가 광범위한 접근을 유지하고 있습니다.

아시아태평양은 가장 급성장하고 있는 지역으로 2025-2030년 CAGR 5.3%로 성장이 예측되고 있습니다. 도시화의 진전, 식생활의 변화, 고령화가 2형 당뇨병 유병률의 급상승을 촉진하고 있습니다. 중국과 인도에서는 보험 급여 확대로 브랜드 인슐린 제제와 신규 주사제에 대한 접근이 확대되고 있습니다. 디지털 헬스툴과 모바일 일 플랫폼은 케어 제공의 갭을 메우고, 원격지 환자의 어드히어런스와 연속성을 지원하고 있습니다. 따라서 아시아태평양의 당뇨병 치료제 시장 규모는 2030년까지 구미 시장과의 갭의 일부를 채울 것으로 예측됩니다.

유럽은 견고한 바이오 시밀러 프레임워크와 비용 효과를 조사하는 가치 평가 기관에 의해 형성된 성숙하면서도 진화하는 상황을 보여줍니다. 바이오시밀러 의약품의 높은 보급률이 오리지네이터의 가격 설정을 압박하고 있지만, 배합제나 첨단 GLP-1 제제의 보급이 수익의 바닥 견고함을 지원하고 있습니다. 중동 및 라틴아메리카의 신흥 시장은 당뇨병 유병률의 상승에 대처하기 위해 정부가 자금을 투입하고 다국적 기업이 제조와 판매를 현지화함으로써 새로운 비즈니스 기회를 가져오고 있습니다.

The Diabetes Drugs Market size is estimated at USD 90.60 billion in 2025, and is expected to reach USD 107.66 billion by 2030, at a CAGR of 3.51% during the forecast period (2025-2030).

Sustained growth is rooted in the accelerating global diabetes burden, earlier diagnosis, and rapid uptake of innovative therapies that combine glycemic control with weight-management benefits. Insulin remains indispensable, yet demand is tilting toward GLP-1 receptor agonists and other non-insulin injectables that improve cardiometabolic outcomes . Oral peptide technologies, biosimilar basal insulins, and digitally enabled care models are widening patient access while tempering costs. Competitive intensity is high as incumbents scale manufacturing and digital ecosystems to defend share in an increasingly value-driven environment.

More than 828 million adults were living with diabetes in 2024, quadruple the 1990 level. Earlier screening programs in lower-income regions are enlarging the treated population and lengthening therapy duration . New WHO guidance endorsing earlier use of GLP-1 agonists signals tighter integration of advanced injectables into first-line care. The overlap between obesity and diabetes further amplifies demand because many GLP-1 drugs now carry dual indications. These shifts collectively underpin long-run volume growth for the diabetes drugs market.

Pharmaceutical spending on diabetes climbed 19% in 2023, outpacing overall health inflation . As per diabetes market research, payers are funding costlier therapies because lower complication rates offset near-term outlays. Employer health plans face mounting pressure, driving tighter utilization management yet preserving access to high-value medicines. This spending momentum sustains price realization even as unit costs come under scrutiny, benefiting innovative products that demonstrate clear clinical and economic returns.

Isolated pancreatitis reports have prompted enhanced pharmacovigilance and conservative patient selection. Although incidence rates remain low, prescriber caution may slow uptake in high-risk cohorts, moderating the meteoric rise of GLP-1 sales. Manufacturers are supporting education and post-marketing surveillance to safeguard benefit-risk profiles.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Insulin maintained a 55% share of the diabetes drugs market in 2024, underscoring its central role in both Type 1 and advanced Type 2 management. However, GLP-1 receptor agonists are expanding at a 4.5% CAGR, propelled by weight-loss efficacy that broadens prescribing beyond traditional glycemic control. The diabetes drugs market size for GLP-1 products is projected to reach USD 150 billion by 2030, reflecting their dual-indication appeal. Oral SGLT-2 inhibitors continue to gain favor, supported by organ-protective data that positions them as valuable adjuncts or alternatives to injectables in the diabetes treatment market.

Competitive dynamics within this segment are intense. Novo Nordisk and Eli Lilly currently hold an estimated near-total share, yet a pipeline of dual and triple agonists promises fresh competition. Fixed-dose combinations, such as insulin degludec / liraglutide pens, illustrate how delivery innovation can lock in adherence benefits and extend product life cycles within the diabetes drugs industry.

The Diabetes Drug Market Report Segments the Industry Into by Drugs (Oral Anti-Diabetic Drugs, Insulin, and More), Route of Administration (Oral, Subcutaneous, and Intravenous), Distribution Channel (Online Pharmacies, and Offline), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America retained leadership with a 42% contribution to 2024 revenue. Broad insurance coverage, strong specialty-care infrastructure, and early adoption of GLP-1 agents underpin regional dominance. Insulin affordability legislation has also stimulated unit demand by lowering patient cost exposure, even as it constrains price expansion. Employers are refining prior-authorization protocols to manage GLP-1 growth, but sustained clinical value is preserving broad access.

Asia-Pacific is the fastest-growing territory, registering a projected 5.3% CAGR from 2025-2030. Rising urbanization, dietary shifts, and aging populations are driving a steep rise in Type 2 prevalence. Expanded insurance benefits in China and India are widening access to branded insulins and novel injectables. Digital health tools and mob ile platforms are bridging care-delivery gaps, supporting adherence and continuity for patients in remote areas. The diabetes drugs market size in Asia-Pacific is therefore expected to close part of the gap with entrenched Western markets by 2030.

Europe presents a mature but evolving landscape shaped by robust biosimilar frameworks and value-assessment bodies that scrutinize cost-effectiveness. High biosimilar penetration is pressuring originator pricing, yet uptake of combination devices and advanced GLP-1 agents is supporting revenue resilience. Emerging markets in the Middle East and Latin America add incremental opportunity as governments commit funds to address escalating diabetes prevalence and as multinational firms localize manufacturing and distribution.