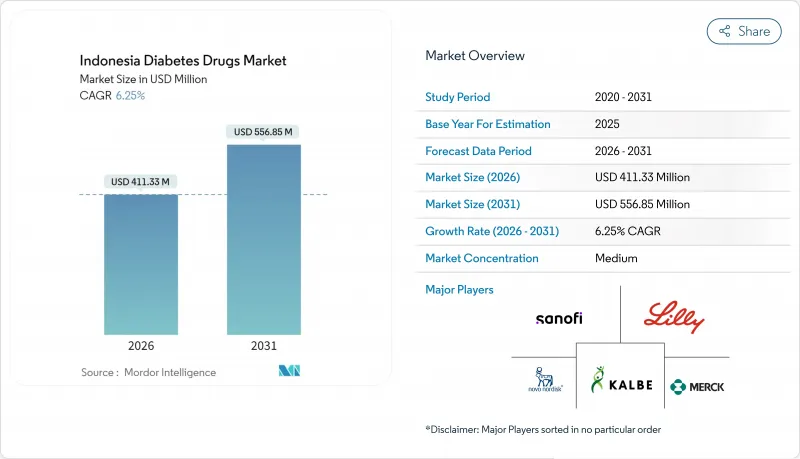

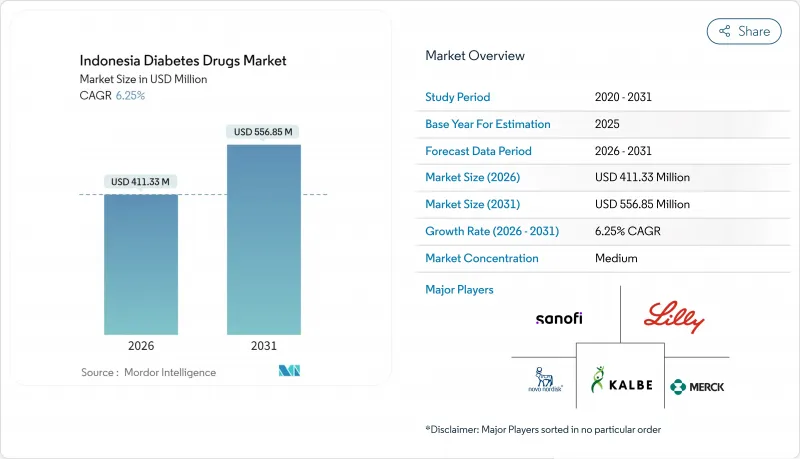

인도네시아의 당뇨병 치료제 시장은 2025년 3억 8,713만 달러에서 2026년에는 4억 1,133만 달러로 성장하고 2026년에서 2031년에 걸쳐 CAGR 6.25%로 성장을 지속하여 2031년까지 5억 5,685만 달러에 이를 것으로 예측됩니다.

꾸준한 성장은 세계 5위의 당뇨병 환자 수를 보유한 인도네시아의 상황, BPJS Kesehatan 건강보험제도, 그리고 확대하는 국내 제조 능력에 의해 뒷받침되고 있습니다. 신규 진단의 대부분이 노령 인구에서 발생하면서 처방량은 증가를 계속하고 있는 한편, 신규 GLP-1 및 SGLT-2 약제가 도시의 병원에서 임상적으로 받아들여지고 있습니다. 게다가 원료의약품(API)의 국내 생산 확대, 할랄 인증 의약품 추진, 적극적인 디지털 헬스 도입이 인도네시아의 당뇨병 치료제 시장에 더욱 기세를 더하고 있습니다.

인도네시아의 성인 당뇨병 유병률은 2011년 5.1%로 2024년 11.7%로 급증했으며, 전체 진단 사례의 절반이 65-74세층에 집중되고 있습니다. 이 장기적인 인구 역학의 변화는 전체 치료 영역에서 지속적인 수요를 유발하여 인도네시아의 당뇨병 치료제 시장의 안정적인 수요 기반을 형성하고 있습니다. 보건부는 당분 음료의 섭취 억제를 목적으로 한 설탕세의 틀을 계획하고 있으나, 생활 습관의 변화는 완만하기 때문에 치료 요구는 여전히 높은 수준에 있습니다. 또한 역학 연구를 통해 당뇨병이 심장병, 간 질환 및 폐 질환의 발생률 증가와 관련이 있음이 발견되었으며, 여러 병존 질환을 관리하는 병용 요법으로의 전환이 임상의사들 사이에서 진행되고 있습니다. 이러한 현실은 특히 연령층에 맞춘 고정용량 배합제 등 일상에서의 복약 준수를 용이하게 하는 치료법의 개발을 가속화하고 있습니다.

BPJS Kesehatan(국민건강보험)은 현재 2억명 이상의 국민을 대상으로 한 단일 급여 스케줄에 따라 당뇨병 치료제의 환급을 실시하고 있습니다. 2025년부터는 연간 무료 건강검진에 3조 3,000억 루피아의 예산이 할당되었고 조기 진단 건수 증가가 예상되어 인도네시아의 당뇨병 치료제 시장을 확대시킬 전망입니다. 신규 만성 질환 스크리닝 규제는 1차 의료시설이 구조화된 후속 프로토콜을 준수하도록 의무화하고 초기 진단 후에도 안정된 처방 흐름을 유지합니다. 2025년 7월에 시행된 표준 입원 클래스(KRIS) 제도는 병원 급여의 계층화를 폐지하고, 소득층에 관계없이 신규 당뇨병 치료에 대한 접근을 균일화합니다. 이러한 정책이 더해 보험 적용 범위의 격차를 해소하는 동시에 가이드라인을 준수하는 브랜드 의약품에 대한 처방 결정을 촉진합니다.

현지 기업은 여전히 원자재의 대부분을 중국과 인도에서 조달하고 있으며 공급망은 환율 변동과 운송 병목 현상에 민감한 상황입니다. 자바섬의 신규 API 공장이 취약성을 낮추는 반면, 전국적인 수요를 충당하기 위해서는 생산 능력이 부족하고, 지역 내의 경쟁사에 비해 단위 비용이 높아지고 있습니다.

인도네시아의 경구 당뇨병 치료제 시장의 규모는 2025년 1억 6,279만 달러에 이르렀으며 전체 매출의 42.05%를 차지했습니다. 메트포르민(처방율 33.85%)과 글리메피리드가 제1선택약으로서 주류이며, 국가 전자 처방전 리스트(e-Fornas) 등재가 선택을 뒷받침하고 있습니다. 의사가 여러 질환을 앓고 있는 고령 환자의 복약 준수율 향상을 목적으로 단제 투여를 요구하는 가운데 고정용량 배합제의 도입이 증가하고 있습니다. 더불어, 비인슐린 주사제는 GLP-1 수용체 작용제 및 이중 작용제의 임상시험 활동에 견인되어 8.45%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장 궤도를 기록할 전망입니다. 2024년 9월에 시작된 LeaderMed사와 Combiphar사의 LM-008 3상 시험은 차세대 주사제에 대한 현지 수요의 크기를 보여주고 있습니다. 프리미엄 아날로그 인슐린은 편의성이 뛰어나며 35%의 사용자가 프리믹스 펜을 선호하기 때문에 좁지만 수익성이 높은 점유율을 유지하고 있습니다.

부가가치형 주사제를 둘러싼 경쟁 격화에 의해 특히 자카르타와 반둥에서는 병원의 처방약 리스트가 변경되어 전문 위원회가 심혈관 결과 데이터를 보다 중시하게 되었습니다. 제약 그룹은 환자 지원 프로그램과 혈당 측정기의 번들 판매로 대응하고 있지만, 이러한 전략은 고객 충성도를 높이는 한편 이익률을 압박하고 있습니다. 현지 API 공장은 경구 정제의 총 매출 향상에 기여할 수 있지만, 주사용 복합 펩티드는 여전히 수입 중간체에 의존하기 때문에 가격의 즉각적인 완화는 불투명합니다.

The Indonesia Diabetes Drugs market is expected to grow from USD 387.13 million in 2025 to USD 411.33 million in 2026 and is forecast to reach USD 556.85 million by 2031 at 6.25% CAGR over 2026-2031.

The steady climb is underpinned by the country's status as the world's fifth-largest diabetes population, universal insurance coverage through BPJS Kesehatan, and expanding local manufacturing capacity. Prescription volumes keep rising as older adults account for most new diagnoses, while novel GLP-1 and SGLT-2 agents win clinical acceptance in urban hospitals. Greater domestic production of active pharmaceutical ingredients (APIs), a push toward halal-certified drugs, and aggressive digital-health roll-outs add further momentum to the Indonesia diabetes drugs market.

Indonesia's adult diabetes prevalence jumped to 11.7% in 2024, up from 5.1% in 2011, with half of all diagnoses in the 65-74 age bracket. This long-running demographic shift fuels consistent demand across every therapeutic class and sets a stable volume base for the Indonesia diabetes drugs market. The Ministry of Health plans a sugar-tax framework to curb sweet-beverage intake, yet treatment needs remain high as lifestyle patterns change slowly. Epidemiological studies also link diabetes with higher incidences of heart, liver, and lung disease, pushing clinicians toward combination regimens that manage multiple comorbidities. These realities keep the treatment pipeline accelerating, particularly for age-tailored fixed-dose combinations that simplify daily adherence.

BPJS Kesehatan currently reimburses diabetes drugs under a unifi ed benefits schedule that reaches more than 200 million citizens. Starting 2025, an allocated Rp 3.3 trillion budget for free annual medical check-ups will likely raise early diagnosis volumes, enlarging the Indonesia diabetes drugs market. New chronic-disease screening regulations oblige primary-care clinics to follow structured follow-up protocols, maintaining steady prescription flows beyond initial diagnosis. A mandatory Standard Inpatient Class (KRIS) regime, due July 2025, eliminates tiered hospital benefits and thus levels access to newer diabetes therapies across income groups. Together, these policies close coverage gaps while nudging prescription decisions toward guideline-compliant brands.

Local firms still source most raw materials from China and India, exposing supply chains to currency swings and freight bottlenecks. While Java's new API plants reduce vulnerability, capacity remains insufficient to cover nationwide demand, keeping unit costs elevated relative to regional peers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The Indonesia diabetes drugs market size for oral therapies reached USD 162.79 million in 2025, equal to a 42.05% revenue slice. Metformin (33.85% prescription rate) and glimepiride dominate first-line choices, aided by inclusion on the national e-Fornas list. Uptake of fixed-dose combinations is rising as physicians seek one-pill dosing to reinforce adherence among multi-morbidity seniors. In parallel, non-insulin injectables book the fastest trajectory, with an 8.45% CAGR linked to GLP-1 and dual-agonist trial activity. LeaderMed and Combiphar's Phase 3 study of LM-008-from September 2024-underscores local appetite for next-generation injectables. Premium analogue insulin retains a narrow but lucrative share because 35% of users prefer premixed pens for convenience.

Intensified competition around value-added injectables changes hospital formularies, especially in Jakarta and Bandung, where specialist panels now weigh cardiovascular-outcome data more heavily. Pharmaceutical groups answer with patient-assistance schemes and bundled glucometer packages, tactics that deepen loyalty but squeeze margins. Local API plants could improve gross margins for oral tablets; however, complex peptides for injectables still depend on imported intermediates, limiting immediate price relief.

The Indonesia Diabetes Drugs Market Report is Segmented by Drug Class (Oral Anti-Diabetics, Insulins, Combination Drugs and Non-Insulin Injectable Drugs), Diabetes Type (Type-1 Diabetes and Type-2 Diabetes), and Distribution Channel (Hospital Pharmacies, Retail Chain Pharmacies and Online Pharmacies). The Market Forecasts are Provided in Terms of Value (USD).