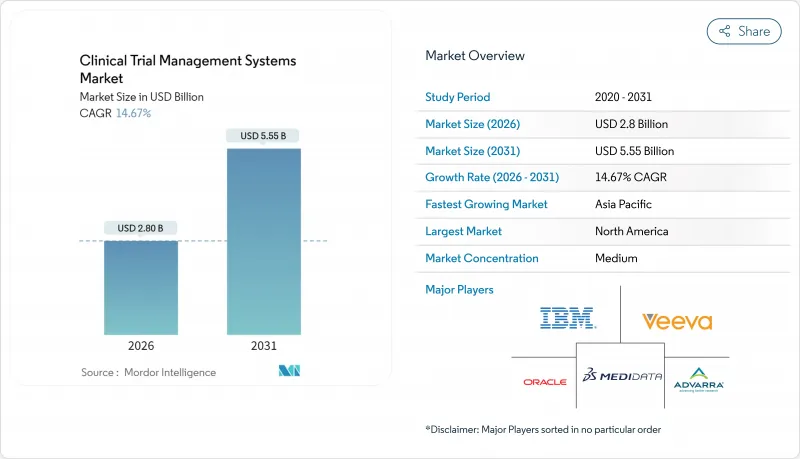

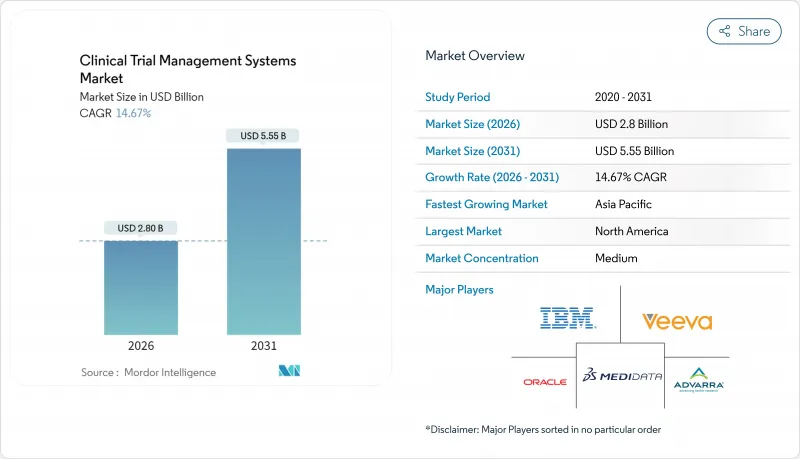

임상시험 관리 시스템 시장은 2025년 24억 4,000만 달러로 평가되었고, 2026년 28억 달러로 성장할 것으로 전망되며, 2026-2031년 연평균 복합 성장률(CAGR) 14.67%로 성장을 지속하여 2031년까지 55억 5,000만 달러에 달할 것으로 예측되고 있습니다.

이 성장의 주요 요인은 제약 연구 분야에서 디지털화 진전, 투명성에 대한 규제 강화, 프로토콜 설계의 복잡화를 포함합니다. 클라우드 컴퓨팅의 도입, 인공지능을 활용한 분석, 전문적인 CRO(계약연구기관)를 핵심적인 역할로 끌어올리는 아웃소싱의 물결은 모두 최신 플랫폼에 대한 수요를 뒷받침하고 있습니다. 분산형 및 하이브리드형 테스트로의 전환은 스폰서, 연구자 및 환자를 연결하는 실시간 모니터링 도구의 적용 대상 기반을 확대하고 있습니다. 규제에 대한 전문 지식과 유연한 도입 모델을 결합한 공급업체는 구매자가 단편적인 포인트 솔루션에서 통합된 임상 생태계로 전환하는 동안 계약을 획득했습니다.

2024년에만 암 영역 신규 증례 수는 2,800만 건을 넘었으며, 이 증가가 세계의 중개 연구의 기록적인 증가를 뒷받침하고 있습니다. 이에 대해 세계의 스폰서는 새로운 국가 및 적응증에 대한 시험 범위 확대로 대응하고 있어 프로젝트 매니저나 데이터 스튜어드의 부담이 증가하고 있습니다. 임상시험 관리 시스템(CTMS) 시장에서 기업 전체를 커버하는 플랫폼이 주목을 받고 있습니다. 이는 중앙 팀이 단일 작업 공간에서 여러 시설 및 여러 그룹의 프로그램에서 계획, 예산 관리 및 엔드 포인트 추적을 가능하게 하기 때문입니다. ICON plc는 이러한 수요 급증에 대응하기 위해 이러한 통합 서비스를 확대하여 2020-2024년 수익을 2배 이상으로 증가시켰습니다. 수요가 증가함에 따라 등록 지연을 조기에 감지하고 스케쥴 지연 이전에 스폰서가 자원을 전환하는 데 도움이 되는 분석 모듈에 대한 투자도 촉진합니다.

COVID-19에 의한 봉쇄는 원격 모니터링이 가능하고 현지 방문보다 효율적인 경우가 많다는 것을 입증했습니다. 그 후, 스폰서 기업은 노후화된 온프레미스 시스템을 클라우드 툴로 대체하여 즉시 데이터 액세스, 자동화된 감사 추적, 세계에 분산된 팀을 위한 안전한 협업을 실현하고 있습니다. 하이브리드 및 호스팅된 프라이빗 클라우드 옵션은 16.45%의 성장률을 보여줍니다. 이는 퍼블릭 클라우드의 민첩성 및 지역 프라이버시 규정을 충족하는 프라이빗 클라우드의 제어 기능을 융합하기 때문입니다. 데이터 마이그레이션과 검증을 고객에게 지도하는 벤더는 장기 계약을 받지만 레거시 아키텍처에 묶인 벤더는 비즈니스 규모의 축소 위험에 직면합니다.

엔터프라이즈 전반의 전개에는 라이선싱, 검증 및 통합을 포함하여 5년 동안 5백만 달러가 필요합니다. 임상예산이 핍박하고 있는 지역에서는 이 자본 부담이 도입을 늦추고 있습니다. 21 CFR Part 11 검증과 같은 추가 서비스 계층은 총 비용을 30%에서 50% 증가시킬 수 있습니다. 벤더는 초기 리스크를 줄이는 모듈식 구독과 '설정만으로 코딩 불필요' 템플릿을 가속화하여 대응하고 있지만, 중규모 생명공학 기업에게는 여전히 가격이 높은 장벽이 되고 있습니다.

2025년에도 클라우드 기반 시스템은 수익으로 57.22%의 우위를 유지하였고, CTMS 시장이 속도와 협업을 중시하는 웹 네이티브 툴을 지지하고 있는 것으로 확인되었습니다. 하이브리드 도입은 CAGR16.12%로 증가하고 있습니다. 이는 스폰서가 민감한 데이터 세트를 내부 서버에 저장하면서 클라우드에서 운영 대시보드를 스트리밍할 수 있기 때문입니다. 이 유연성은 데이터 주권에 관한 법률이 다른 유럽 연합과 중국의 두 지역에서 종양학 시험을 실시하는 기업에게 필수적입니다.

하이브리드 설계는 기존 온프레미스 자산의 임상시험 관리 시스템 시장 수명을 연장합니다. 많은 중견 바이오 의약품 기업들은 실험 장비와 함께 작동하는 검증된 미들웨어를 계속 운영하고 있습니다. 하이브리드 브리지를 통해 이러한 투자를 계속하면서 최신 등록 관리 및 사이트 결제 모듈을 상위 계층에 추가할 수 있습니다. 입증된 마이그레이션 로드맵이 있는 공급업체는 업데이트 속도가 높아지지만 온프레미스 전업 공급업체는 빠르게 점유율을 잃고 있습니다.

2025년 임상시험 관리 시스템 시장 수익의 63.88%는 소프트웨어 라이선싱이 차지하며 핵심 데이터베이스 스케줄링 도구 및 모니터링 대시보드의 기본 역할을 반영합니다. 그러나 서비스 분야는 16.48%의 연평균 복합 성장률(CAGR)로 확대되고 있어 설정 지원, 사용자 트레이닝 및 감사 대응 준비에 대한 높은 수요가 부각되고 있습니다. 국경을 넘는 연구에서는 현지화, 언어 지원 및 규제 적합 검증 등의 업무가 발생하지만, 스폰서 기업이 내부 자원만으로 대응할 수 있는 경우는 드뭅니다.

정밀의료 프로토콜을 통한 데이터 통합 수요가 증가함에 따라 임상시험 관리 시스템 도입 서비스 시장 규모가 확대되고 있습니다. 현대의 암 임상시험에서는 방사선 영상, 환자 보고 결과, 실험실 유전체 데이터가 거의 실시간으로 캡처됩니다. 전문 통합업체는 이러한 데이터를 통합 워크스트림에 통합하고 각 워크플로우를 규제 기관에 문서화합니다. 소프트웨어 및 관리 서비스 번들을 결합한 공급업체는 더 큰 점유율을 얻었습니다.

북미는 스폰서 기반의 밀도, 경험이 풍부한 연구자 네트워크, 예측 가능한 규제 지침을 통해 2025년 임상시험 관리 시스템 시장 수익의 35.12%를 차지했습니다. 인적 자원 풀이 21 CFR Part 11 검증 및 HIPAA 규칙을 이해하기 때문에 대기업은 플랫폼 업그레이드를 미국 및 캐나다 사이트에 우선적으로 전개하고 있습니다. 그러나 이 지역이 Tier 1 제약 기업 계정의 포화 상태에 가까워짐에 따라 성장률은 지난 몇 년에 비해 둔화되고 있습니다.

아시아태평양은 15.56%라는 가장 빠른 CAGR을 보여 향후 5년간 임상시험 관리 시스템 시장 규모를 대폭 확대될 전망입니다. 중국에 있어서의 '인간 유전 자원 관리 밸브 공실' 절차의 효율화와, 인도의 '신약 및 임상시험 규칙'은 모두 개시까지의 타임라인을 간소화해, 다국적 연구를 유치하고 있습니다. 각국 정부는 세액공제 등의 우대조치를 이용해 국내 바이오테크놀러지 업계를 육성해 새로운 국내 구매자층을 창출하고 있습니다. 다국어 지원과 현지 호스팅을 제공하는 공급업체가 가장 혜택을 누리고 있습니다.

유럽에서는 EU 임상시험 규칙에 따라 회원국 간의 승인 과정이 통일됨으로써 안정적이고 중간 정도의 단일 자리수 성장이 예상됩니다. 스폰서 기업은 과학적인 전문 지식 및 고품질 데이터를 평가하고 있지만, 브렉짓트는 영국과 EU 간의 월경 신청을 복잡하게 하고 일부 플랫폼에서는 이중 워크플로우를 강요하고 있습니다. 중동 및 아프리카, 남미는 현재 시장 규모로서는 비교적 작은 비율을 차지하고 있지만, 연구 인프라의 정비 및 공중 위생 자금의 확충에 의해 후기 단계의 환자 모집에 있어서 매력적인 지역이 되고 있습니다. 이 지역에서 활동하는 공급업체는 보다 광범위한 임상시험 관리 시스템 시장에서 발판을 구축할 수 있습니다.

The Clinical Trial Management Systems market is expected to grow from USD 2.44 billion in 2025 to USD 2.8 billion in 2026 and is forecast to reach USD 5.55 billion by 2031 at 14.67% CAGR over 2026-2031.

Rising digital maturity across pharmaceutical research, tighter transparency rules, and the growing complexity of protocol design are the main forces behind this climb. Cloud computing adoption, artificial-intelligence-enabled analytics, and an outsourcing wave that pushes specialist Contract Research Organizations (CROs) into central roles all reinforce demand for modern platforms. The shift toward decentralized and hybrid trials also enlarges the addressable base for real-time oversight tools that link sponsors, investigators, and patients. Vendors that marry regulatory expertise with flexible deployment models are winning contracts as buyers move away from fragmented point solutions toward integrated clinical ecosystems.

Oncology alone registered more than 28 million new cases in 2024, a rise that fuels record numbers of interventional studies worldwide. Global sponsors react by expanding trial footprints into new countries and indications, which raises the load on project managers and data stewards. Enterprise-wide platforms within the clinical trial management system (CTMS) market gain traction because they let central teams plan, budget, and track endpoints across multi-site, multi-arm programs in one workspace. ICON plc more than doubled revenue between 2020 and 2024 by scaling such integrated services to meet this surge. Heightened demand also stimulates investment in analytics modules that spot enrollment lags early and help sponsors shift resources before timelines drift.

COVID-19 lockdowns proved that remote monitoring is viable and often more efficient than on-site visits. Since then, sponsors have replaced aging on-premise stacks with cloud tools that provide instant data access, automated audit trails, and secure collaboration for globally dispersed teams. Hybrid and hosted private cloud options expand at 16.45% because they blend public-cloud agility with private-cloud controls that satisfy regional privacy statutes. Vendors that guide customers through data migration and validation win long contracts, while those tied to legacy architectures risk shrinking footprints.

An enterprise-wide deployment often requires USD 5 million over five years once licenses, validation, and integration are counted. In regions where clinical budgets remain lean, this capital burden slows adoption. Added service layers-such as 21 CFR Part 11 validation-can raise total cost by 30% to 50%. Vendors are responding with modular subscriptions and accelerated "configure-not-code" templates that lower up-front risk, but sticker shock persists for mid-size biotechs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud-based systems kept a 57.22% revenue lead in 2025, confirming that the CTMS market favors web-native tools for speed and collaboration. Hybrid deployments rise at 16.12% CAGR because they let sponsors park sensitive datasets on internal servers while streaming operational dashboards from the cloud. This flexibility is essential for companies that conduct oncology trials in both the European Union and China, two regions with divergent data-sovereignty laws.

Hybrid designs also extend the clinical trial management systems market life of older on-premise assets. Many mid-tier biopharma firms still run validated middleware that links to lab instruments. A hybrid bridge lets them keep those investments live while layering modern enrollment and site-payment modules on top. Vendors with proven migration roadmaps therefore see higher renewal rates, while pure-play on-premise providers lose ground rapidly.

Software licenses drove 63.88% of the clinical trial management system market revenue in 2025, reflecting the foundational role of core databases, scheduling tools, and monitoring dashboards. Yet services expand at 16.48% CAGR, highlighting buyer need for configuration, user training, and audit readiness. Every cross-border study triggers localization, language support, and regulatory validation tasks that sponsors are rarely staffed to manage internally.

The clinical trial management systems market size for implementation services is swelling as precision-medicine protocols raise data-integration demands. Modern oncology trials now ingest radiology images, patient-reported outcomes, and laboratory genomics in near-real time. Specialist integrators stitch these feeds into unified workstreams and document each workflow for regulators. Vendors that combine software with managed service bundles thus capture larger share of wallet.

The Clinical Trial Management Systems Market Report is Segmented by Delivery Mode (On-Premise, and More), Component (Software and Services), Type (Enterprise-Wide CTMS, and More), Clinical Trial Phase (Phase I, and More), End User (Medical Device Manufacturers, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America produced 35.12% of the clinical trial management systems market revenue in 2025, due to its dense sponsor base, experienced investigator networks, and predictable regulatory guidance. Large enterprises routinely roll out platform upgrades across U.S. and Canadian sites first because talent pools understand 21 CFR Part 11 validation and HIPAA rules. Growth, however, slows compared with earlier years as the region approaches saturation in Tier-1 pharma accounts.

Asia-Pacific returns the fastest 15.56% CAGR and is set to expand the clinical trial management systems market size materially over the next five years. China's streamlined Human Genetic Resources Administration Office procedures and India's New Drugs and Clinical Trial Rules both simplify start-up timelines, inviting multinational studies. Governments also employ incentives such as tax credits to grow local biotech scenes, creating fresh pools of domestic buyers. Vendors that offer multilingual support and local hosting benefit most.

Europe contributes steady mid-single-digit growth as the EU Clinical Trials Regulation harmonizes approvals across member states. Sponsors value the continent for scientific expertise and high-quality data, yet Brexit complicates UK-EU cross-border submissions, forcing dual workflows inside some platforms. The Middle East & Africa and South America collectively form a smaller slice today, but improvements in research infrastructure and public-health funding make them attractive for late-phase patient recruitment. Vendors active in these regions can secure a foothold in the broader clinical trial management system market.