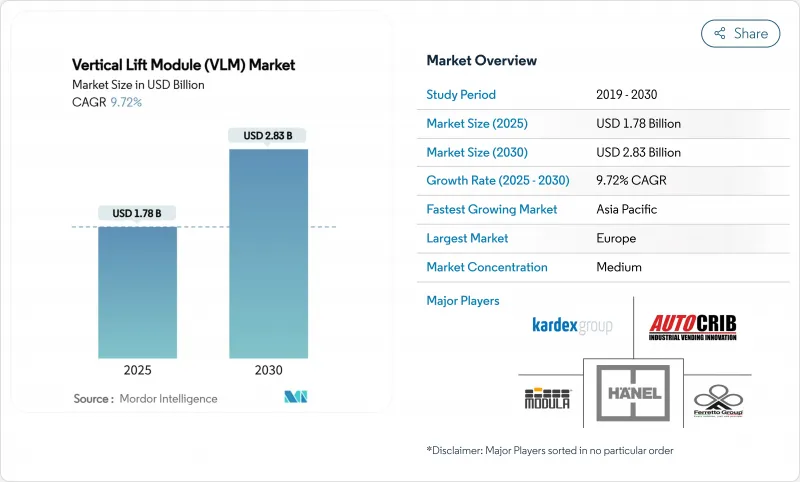

수직 리프트 모듈 시장 규모는 2025년에 17억 8,000만 달러, 2030년에는 28억 3,000만 달러에 이르고, CAGR 9.72%로 성장할 것으로 예측됩니다.

전자상거래 회사가 부피가 큰 팔레트 래킹을 완성 사이클을 며칠에서 몇 시간으로 압축하는 상품 대인 시스템으로 대체함에 따라 수요가 가속화됩니다. 자동차 제조업체는 저스트 인 타임의 생산 리듬을 유지하기 위해 자동 버퍼 스토리지를 추가하고, 생명 과학 클린 룸은 추적 성과 오염 제어 요구 사항을 충족하는 밀폐형 모듈을 채택합니다. 콜드체인 운영자는 에너지 효율적인 듀얼 드라이브 모터를 24개월 이내에 ROI를 얻는 루트로 생각하며, 예측 유지보수 소프트웨어 패키지는 장비 제조업체에 판매 후 수익원을 엽니다.

소매업체는 지역 배송 센터에서 기존 매장 또는 상점에 인접한 자동화된 마이크로 불필요한 노드로 이동합니다. 2030년까지 세계에서 7,300개 이상의 자동화 마이크로플루필먼트 센터가 가동될 것으로 예상되며, 거의 절반은 미국에서 가동하기 때문에 10,000평방피트의 설치 면적에 맞는 컴팩트한 고밀도 모듈에 대한 수요가 지속되고 있습니다. VLM은 로봇 피커와 통합하여 99.99%의 주문 정확도를 달성하는 동시에 필요한 노동력을 최대 66%까지 절감합니다. 공급망의 제약으로 인해 일부 소매업체에서는 도입이 지연되고 있지만, 조기 도입 기업은 라스트원 마일의 배송 리드타임을 단축함으로써 신속한 투자 회수를 실현하고 있습니다.

아시아의 주요 도시에서 산업용 창고의 임대료는 지역 평균을 초과하고 있으며, 사업자는 수직 공간을 확보해야합니다. 천장 높이가 98피트가 되는 VLM은 보관 밀도를 4배로 높이는 동시에 노동력이 부족하고 비싼 장소에서는 필수적인 이동에서 피킹으로 작업을 전환시킵니다. 인도에 있는 다이후쿠의 새로운 제조 공장은 이러한 도시 지역에서 자동화 수요의 급증에 대응하기 위해 건설되었습니다. 따라서 부동산 제약과 임금 인플레이션은 VLM 투자를 경영 우선 순위 목록의 상위 수준으로 끌어 올리기 위해 함께 작동합니다.

1990년 이전에 건설된 유럽 공장의 대부분은 VLM의 최고 효율을 이끌어내는 25피트 이상의 천장 높이를 갖추지 못했습니다. 리트로핏(retrofitting) 작업에는 바닥 보강과 구조물 점검이 포함되어 프로젝트 비용을 증가시킵니다. AutoStore는 유럽에서의 설치의 65%가 이러한 리노베이션 시나리오에서 이루어질 것으로 예상하며 기회와 제약을 모두 강조합니다.

1층 건물 시스템은 2024년 매출의 57%를 차지했지만 기존 건물의 높이와의 호환성과 간단한 작업을 반영한 것입니다. 일반적인 처리 능력은 시간당 평균 250개이며 중속 환경에 충분합니다. 그러나 듀얼 레벨은 2030년까지의 CAGR은 11.9%를 나타낼 전망입니다. 이 기종은 꺼내기와 트레이를 동시에 제시할 수 있게 함으로써 매시간 350개의 품목을 처리할 수 있으며, 브라운필드의 토지에 충분한 수직 공간이 있는 경우에 선호되는 선택이 됩니다. Kardex는 컨트롤러의 펌웨어를 업그레이드하여 동일한 WMS에서 두 구성 모두를 조화시킬 수 있으며 운영자에게 주문 프로파일의 진화에 맞게 시스템 유형을 혼합 할 수있는 유연성을 제공합니다. 수직 리프트 모듈 시장은 시설이 더 높은 픽 퍼 스퀘어 피트를 추구함에 따라 2단 투자에 계속 기울고 있습니다.

모듈 설계 프레임워크는 엔지니어링 비용을 낮추고 설치를 가속화합니다. OEM은 현재 플러그 앤 플레이 컨베이어 독과 로봇 인터페이스를 제공하고 있으며, 2단 유닛이 고속 이동체를 처리하는 반면, 1단 모듈이 인접한 고 처리량 영역의 버퍼 역할을 할 수 있습니다. 이 하이브리드 전략은 평균 수요에 대한 장비의 과도한 크기 없이 계절 급등 사이의 지속성을 보장하고 균형 잡힌 설비 투자 계획에 대한 수직 리프트 모듈 시장의 가치 제안을 강화합니다.

20-50 톤 등급의 유닛은 2024년에 43% 시장 점유율을 차지하며, 이는 박스형 자동차 부품, 토트 취급 전자상거래 재고, 트레이당 1,000 파운드를 초과하지 않는 의약품 페이로드에 적합하다는 것을 반영한 것입니다. 이러한 시스템은 특별한 바닥재와 크레인에 의한 지원이 필요 없기 때문에 다업종 전개의 기간을 형성하고 있습니다. 50톤 이상의 모듈은 CAGR 12.6%를 기록했으며, 이는 항공우주 및 중장비 공급업체가 대형 구성요소를 단일 저장 지점으로 통합한 결과입니다. 반대로 20 톤 미만의 기계는 청결과 정밀도가 중량 지표를 초과하는 전자 및 의료기기의 조립 라인에서 틈새 역할을 담당합니다.

셰이퍼의 LOGIMAT는 이 트렌드를 보여주며 트레이당 최대 1톤의 용량을 제공하며 통합 시간을 30% 단축하는 ERP 커넥터를 갖추고 있습니다. Industry 4.0이 보급됨에 따라 시설은 일반적인 경험 법칙이 아니라 디지털 트윈 시뮬레이션을 기반으로 부하 클래스를 선택합니다. 그 결과, 조달 사이클은 데이터 모델링을 포함할 때까지 연장되지만, 수직 리프트 모듈 시장 규모는 정량화 가능한 생산성 향상과 밀접하게 일치하기 때문에 채택의 기세는 지속됩니다.

수직 리프트 모듈(VLM) 시장은 유형(싱글 레벨 딜리버리, 듀얼 레벨 딜리버리), 부하 용량(20톤까지, 20-50톤, 50톤 이상), 용도(저장 및 버퍼링 등), 최종 사용자 산업(자동차, 전기 및 전자 등), 지역에 따라 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

유럽은 독일, 스페인, 프랑스의 자동차 제조 회랑을 중심으로 2024년 매출 점유율 36%로 선두를 달리고 있습니다. 많은 시설이 최신 천장 높이 기준보다 오래되었기 때문에 브라운필드의 개수가 주류가 되고 있습니다. 추적성과 에너지 실적 감소를 요구하는 OEM 지침은 엄격한 근로자 안전 규범과 함께 신축 프로젝트가 감속하더라도 이 지역의 수직 리프트 모듈 시장의 성장을 유지하고 있습니다. 독일 Tier-1 공급업체는 예기치 않은 라인 정지를 방지하기 위해 AI 기반 모터 진단을 통합하고 있으며, 이 기능은 현재 대부분의 유럽 구매 사양에 내장되어 있습니다.

2030년까지의 CAGR은 아시아태평양이 가장 빠른 12.3%로 중국은 셀 기반 제조가 소형 POS 스토어를 필요로 하는 그린필드 스마트 공장에 VLM을 도입하고 있습니다. 인도의 물류 자동화에 대한 지출은 새로운 산업 회랑이 통합 공급망 공원에 대한 공적 자금을 받고 고밀도 수직 스토리지에 대한 지역적 의지가 커짐에 따라 증가하고 있습니다. 일본과 한국은 인구동태의 고령화로 인한 노동력 부족을 완화하기 위해 모듈을 적용하고 있습니다. 이 지역의 규모와 그린필드의 성질은 공급업체가 VLM 하드웨어, WMS, AMR 플릿 등 에코시스템 세트를 원턴키 패키지로 판매하는 것을 의미하며, 수직 리프트 모듈 시장 규모를 10년 동안 수직 리프트 모듈 시장 규모를 강화할 수 있습니다.

북미는 꾸준한 확대 노선을 유지하고 있습니다. 소매업체는 교외 매장을 마이크로 필필먼트 노드로 개조하고 미국 북동부의 생명 과학 클러스터는 생물 제제용 GMP 대응 모듈을 채택합니다. 미국 중서부와 캐나다의 냉장 창고업체는 피크시 광열비를 억제하는 듀얼 드라이브 호이스트의 효율성을 높이 평가했습니다. 라틴아메리카와 중동 및 아프리카는 대두되고 있지만, 균일하지 않습니다. 브라질의 계약 물류 기업은 설비 투자 장벽을 피하기 위해 임대 모델을 모색하고 있으며, 남아프리카 유통업체는 가까운 미래의 수직 리프트 모듈 시장 침투를 억제하는 요인인 전압 조정 애드온이 필요한 전력 품질 문제에 직면하고 있습니다.

The vertical lift module market size stands at USD 1.78 billion in 2025 and is forecast to reach USD 2.83 billion by 2030, advancing at a 9.72% CAGR.

Demand accelerates as e-commerce firms replace bulky pallet racking with goods-to-person systems that compress fulfillment cycles from days to hours. Automakers add automated buffer storage to sustain just-in-time production rhythms, while life-sciences cleanrooms adopt enclosed modules that meet traceability and contamination-control mandates. Cold-chain operators view energy-efficient dual-drive motors as a route to ROI in less than 24 months, and predictive-maintenance software packages open an after-sales revenue stream for equipment makers.

Retailers are shifting from regional distribution centers to automated micro-fulfillment nodes located inside or adjacent to existing stores. More than 7,300 automated micro-fulfillment centers are expected to be operational worldwide by 2030, almost half of them in the United States, creating sustained demand for compact, high-density modules that fit within 10,000 square-foot footprints . VLMs integrate with robotic pickers to achieve 99.99% order-accuracy rates while reducing labor needs by up to 66% . Although supply-chain constraints have slowed some retailer roll-outs, early adopters demonstrate rapid payback by compressing last-mile delivery lead times.

Industrial rents in key Asian capitals outpace regional averages, forcing operators to reclaim vertical space. VLMs that reach ceiling heights of 98 feet quadruple storage density while shifting work from travel to picking, essential where labor is scarce and expensive. Daifuku's new manufacturing plant in India was commissioned to satisfy this surge in urban automation demand. Real-estate constraints and wage inflation thus act in tandem to move VLM investments higher on management priority lists.

Many European plants built before 1990 lack the 25-foot clear height that unlocks peak VLM efficiency. Retrofitting involves floor reinforcement and structural checks that inflate project costs; in some locations, heritage rules bar vertical alterations. AutoStore estimates that 65% of its European installs occur in such retrofit scenarios, highlighting both opportunity and constraint

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Single-level systems captured 57% of 2024 revenue, a reflection of their compatibility with existing building heights and straightforward operations. Typical throughput averages 250 items per hour, adequate for medium-velocity environments. Dual-level variants, however, post an 11.9% CAGR through 2030. They hit 350 items per hour by allowing simultaneous extraction and presentation trays, making them a preferred choice when brownfield sites possess sufficient vertical clearance. Kardex has upgraded controller firmware to harmonize either configuration within the same WMS, giving operators flexibility to mix system types as order profiles evolve. The vertical lift module market continues to tilt toward dual-level investments as facilities chase higher picks-per-square-foot.

A modular design framework lowers engineering costs and accelerates installation. OEMs now offer plug-and-play conveyor docks and robotic interfaces, allowing single-level modules to serve as buffers for adjacent high-throughput zones while dual-level units handle fast movers. This hybrid strategy ensures continuity during seasonal spikes without oversizing equipment for average demand, reinforcing the vertical lift module market's value proposition for balanced capex planning.

Units rated for 20-50 tons held 43% market share in 2024, reflecting their suitability for boxed automotive parts, tote-handled e-commerce inventory, and pharmaceutical payloads that rarely exceed 1,000 pounds per tray. These systems form the backbone of multi-industry deployments because they require no special flooring or crane assistance. Above-50-ton modules record a 12.6% CAGR, fueled by aerospace and heavy-machinery suppliers consolidating oversized components into single storage points. Conversely, sub-20-ton machines occupy niche roles in electronics and medical device assembly lines where cleanliness and precision outweigh weight metrics.

Schaefer's LOGIMAT illustrates the trend, offering capacities up to 1 ton per tray with ERP connectors that reduce integration times by 30%. As Industry 4.0 spreads, facilities select load classes based on digital-twin simulations rather than generic rules of thumb. Consequently, procurement cycles extend to include data modeling, yet adoption momentum sustains because the vertical lift module market size aligns closely with quantifiable productivity gains.

Vertical Lift Module (VLM) Market is Segmented by Type (Single-Level Delivery, Dual-Level Delivery), Load Capacity (Up To 20 Tons, 20 - 50 Tons, Above 50 Tons ), Application (Storage and Buffering and More), End-User Industry (Automotive, Electrical and Electronics and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe leads with 36% revenue share in 2024, anchored by automotive manufacturing corridors in Germany, Spain, and France. Brownfield retrofits dominate because many facilities predate modern ceiling-height norms. OEM mandates for traceability and energy-footprint reduction, combined with strict worker-safety codes, keep the regional vertical lift module market growing even when new-build projects slow. Germany's Tier-1 suppliers integrate AI-based motor diagnostics to prevent unscheduled line stops, a feature now embedded in most European purchase specifications.

Asia-Pacific posts the fastest 12.3% CAGR through 2030. China deploys VLMs in greenfield smart factories where cell-based manufacturing needs compact point-of-use stores. India's logistics automation spending is climbing as new industrial corridors receive public funding for integrated supply-chain parks, reinforcing regional appetite for high-density vertical storage. Japan and South Korea apply modules to alleviate labor shortages caused by aging demographics. The region's scale and greenfield nature mean suppliers sell complete ecosystems-VLM hardware, WMS, and AMR fleets-in one turnkey package, bolstering the vertical lift module market size across the decade.

North America maintains a steady expansion track. Retailers retrofit suburban outlets with micro-fulfillment nodes, and life-sciences clusters in the U.S. Northeast adopt GMP-compliant modules for biologics. Cold-storage operators in the U.S. Midwest and Canada appreciate dual-drive hoist efficiencies that curb utility bills during peak tariffs. Latin America and the Middle East & Africa are emerging but uneven. Brazil's contract-logistics firms explore leasing models to bypass capex barriers, while South African distributors face power-quality issues that necessitate voltage-regulation add-ons, a factor that suppresses near-term vertical lift module market penetration.