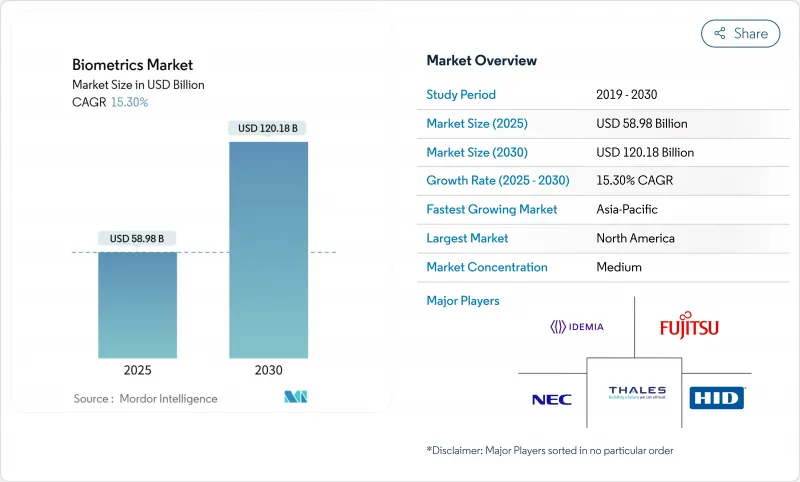

바이오메트릭스 시장 규모는 2025년에 589억 8,000만 달러, 2030년에는 1,201억 8,000만 달러에 이르고, CAGR 15.30%로 성장할 것으로 예측되고 있습니다.

이 확대는 정부의 디지털 ID 프로그램, 결제 토큰화 증가, 공항의 현대화의 급증이 마찰 없는 ID 증명의 필요성을 높이고 있다는 점에서 뒷받침됩니다. 현재의 도입은 여전히 하드웨어가 주류이지만, 기업이 포인트 솔루션에서 플랫폼 모델로 이행함에 따라 클라우드 지원 소프트웨어 엔진이 가장 급속히 확대되고 있습니다. 중국과 유럽 연합(EU)의 새로운 프라이버시 규정은 컴플라이언스 요구 사항을 강화하는 동시에 정확성과 동의 관리의 균형을 이루는 멀티모달 아키텍처를 장려합니다. 북미에서는 2025년 5월부터 REAL ID의 시행에 의해 공항이나 육운국에서의 전개를 향한 연방 정부나 주 정부에 의한 긴급 조달의 파도가 밀려오고 있습니다. 아시아태평양에서는 바이오메트릭스가 슈퍼앱, 지갑, 은행의 e-KYC 프레임워크에 통합되어 장기적인 수요 촉진요인이 되고 있습니다.

아시아 당국은 대규모 디지털 신원의 변화를 지휘하고 있습니다. 한국 스마트폰 기반의 주민등록카드와 2025년 7월까지 외국인들에게도 바이오메트릭스 ID를 확대한다는 베트남의 결정은 종합적인 에코시스템의 벤치마크가 되고 있습니다. 인도네시아의 2억 달러를 투자한 INA 디지털 플랫폼과 필리핀의 8,950만 명의 시민 등록은 지금까지 은행 계좌가 없었던 성인 금융 서비스를 개방합니다. 스리랑카 지문, 얼굴, 망막 스캔을 결합한 멀티 모달 프로그램은 2026년 완료를 목표로 하고 있으며, 신흥 경제권이 레거시 인프라를 뛰어넘는 방법을 보여줍니다.

EMVCo와 ISO 규칙이 조화를 이루면서 생체 인식 카드는 파일럿에서 상업 발행으로 전환했습니다. 인피니언의 SECORA Pay Bio 실리콘과 탈레스의 세계 테스트는 오인식률을 줄이고 높은 거래 상한을 가능하게 했습니다. Mastercard의 Identity Check과 passkey의 지원은 마찰없는 인증을 약속하고 발행자가 부정 행위와 지불 거절을 줄일 수 있도록 도와줍니다. 벤더는 은행이 PIN 프리 비접촉 경험을 선호하기 때문에 2028년까지 1억 1,330만 장의 바이오메트릭 카드가 출하될 것으로 예측했습니다.

2024년부터 2025년까지 BIPA에 의한 2억 달러 이상의 화해는 명시적인 동의 없이 얼굴 인증을 도입하는 기업에 대한 중대한 책임을 시사합니다. GDPR(EU 개인정보보호규정)의 엄격한 데이터 최소화 및 로컬 처리 규칙은 유럽 설치당 EUR 50,000-200,000(56,500-226,000달러)의 컴플라이언스 비용을 추가하여 소규모 프로젝트의 대응 가능한 기반을 줄입니다. FTC의 Rite Aid에 대한 강제 집행은 알고리즘 바이어스 감사의 미국에서 선례가 되고, 벤더는 프라이버시 바이 디자인을 위해 아키텍처를 재설계해야 합니다.

소프트웨어 엔진은 하드웨어가 42.5%의 판매 점유율을 유지하는 동안 CAGR 16.6%로 조연에서 가장 높은 성장률을 기록했습니다. 조직은 클라우드 오케스트레이션, AI 기반 생존 감지, 진화하는 사기 행위에 지속적으로 적응하는 분산형 ID 지갑을 평가합니다. Entrust의 Onfido 인수는 위조 ID 방지를 5배 향상시키는 딥페이크 대응책을 추가하는 등 이러한 궤적에 부합합니다.

하드웨어 영역은 특수 센서가 암호화 템플릿을 안전한 요소에 제공하는 데 필수적입니다. 인피니언의 자동차 핑거프린트 IC는 생산 등급 구성요소가 생체인식 시장을 이동성과 액세스 영역으로 확장한다는 것을 보여줍니다. 서비스는 가장 작지만 통합업체는 규제 산업을 위한 멀티모달 배포를 사용자 정의하여 일관된 보급을 기록하고 있습니다.

홍채 인증은 CAGR은 18.2%를 기록하여 재료비를 절감하고 폼 팩터를 축소하는 액체 렌즈 광학계에 지지되고 있습니다. 지문인증은 스마트폰, 결제카드, 타임클럭 시스템을 통해 2024년 바이오메트릭 시장 점유율의 37.0%를 차지하며 계속 정착하고 있습니다. 얼굴 인증은 공항과 경기장에 꾸준히 침투하고, 음성 해석은 콜센터 인증으로 발판을 굳힙니다.

특히 보행이나 키 스트로크의 동태와 같은 행동적인 생체 지표는 사용자와의 마찰 없이 보안을 향상시키는 수동적인 레이어를 추가합니다. 성숙한 지문과 얼굴 솔루션은 홍채, 손바닥 정맥 및 음성 모듈과 결합하여 멀티모달 키트에 탑재되고 있으며 수익을 다양화하고 단일 양식의 위험을 줄일 수 있습니다.

비접촉식 모달리티는 위생성과 편리성이 기존의 사고방식을 대체하기 때문에 CAGR17.1%로 확대하고 있습니다. 접촉형 시스템의 바이오메트릭스 시장 규모는 2024년에는 37.0%의 점유율을 차지하는 것, 헬스케어나 소매로 전개되는 터치리스 지문 인증, 얼굴 인증, 홍채 인증 키오스크에 밀려, 기세를 잃고 있습니다. ZKTeco는 비접촉 선호도가 장기적인 세속적 변화로 식별합니다.

콘티넨탈의 자동차 카메라와 레이저 콤보로 대표되는 눈에 보이지 않는 센싱은 액세스뿐만 아니라 웰니스 모니터링으로 바이오메트릭스를 변화시킵니다. AI의 개선으로 터치리스 정밀도는 접촉형 벤치마크에 접근하여 고보증 분야를 만족시킵니다.

북미는 2024년 세계 매출의 30.7%를 차지하며 연방 정부의 예산과 민간의 광범위한 도입에 지지되고 있습니다. TSA의 가속 레인 확장과 DHS ID 관리를 위한 2억 5,080만 달러의 라인 아이템은 공급업체에게 수년간 수요 플로어를 제공합니다. 캐나다와 멕시코는 무역을 간소화하기 위해 육상 국경의 전자 게이트를 현대화하고 대륙 규모를 강화합니다.

아시아태평양은 2030년까지의 예측 CAGR이 18.5%로 가장 급경사를 기록하고 있습니다. 한국의 전국적인 모바일 ID 완성, 중국의 성문화된 얼굴 인식 규칙, 인도의 Aadhaar와 연동한 유료 서비스는 어느 나라의 프로그램보다 큰 통일 생체 인식 시장을 육성합니다. 이 지역의 48억 명의 디지털 월렛 이용자는 은행과 통신 사업자 전체에서 바이오메트릭스 KYC를 임의에서 의무로 밀어 올리고 있습니다.

유럽은 GDPR(EU 개인정보보호규정)의 엄격한 감시하에 안정적인 성장을 유지하고 있습니다. EU 출입국 시스템은 솅겐 협정 회원국간에 국경의 바이오메트릭스를 전개하고, 미국의 새로운 신뢰 프레임워크는 민간 부문의 자격 증명 혁신을 촉진합니다. 북유럽에서는 온디바이스 처리가 속도를 저하시키지 않으면서도 개인정보 감독 기관의 요구를 충족할 수 있음이 입증되어, 유럽 전역의 조달 기준 수립에 영향을 미치고 있습니다.

The biometrics market size is valued at USD 58.98 billion in 2025 and is forecast to expand to USD 120.18 billion by 2030, advancing at a 15.30% CAGR.

The expansion is underpinned by government digital-ID programs, rising payments tokenization, and surging airport modernization that collectively elevate the need for frictionless identity proofing. Hardware still dominates current deployments, yet cloud-ready software engines are scaling fastest as enterprises shift from point solutions to platform models. New privacy regulations in China and the European Union are tightening compliance requirements, simultaneously encouraging multi-modal architectures that balance accuracy with consent management. In North America, REAL ID enforcement from May 2025 is driving an urgent wave of federal and state procurements for airport and DMV roll-outs. Asia Pacific's integration of biometrics into super-apps, wallets, and bank e-KYC frameworks positions the region as the long-run demand accelerator.

Asian authorities are orchestrating large-scale digital identity transformations. South Korea's smartphone-based resident registration card and Vietnam's decision to extend biometric IDs to foreign nationals by July 2025 have set benchmarks for inclusive ecosystems. Indonesia's USD 200 million INA Digital platform and the Philippines' registration of 89.5 million citizens unlock financial services for previously unbanked adults. Sri Lanka's multi-modal program combining fingerprints, face, and retina scans targets completion in 2026, illustrating how emerging economies leapfrog legacy infrastructures.

Harmonized EMVCo and ISO rules have moved biometric cards from pilots to commercial issuance. Infineon's SECORA Pay Bio silicon and Thales' global trials cut false-accept rates and allow higher transaction ceilings . Mastercard's Identity Check and passkey support promise frictionless authentication, helping issuers reduce fraud and chargebacks. Vendors forecast shipments of 113.3 million biometric cards by 2028 as banks prioritize PIN-free contactless experiences.

More than USD 200 million in BIPA settlements during 2024-2025, including Clearview AI's USD 51.75 million payment, signals material liability for enterprises deploying facial recognition without explicit consent. GDPR's strict data-minimization and local-processing rules add EUR 50,000-200,000 (USD 56,500-226,000) compliance cost per European installation, shrinking the addressable base for small projects. The FTC's enforcement against Rite Aid sets a U.S. precedent for algorithmic-bias audits, compelling vendors to redesign architectures for privacy by design.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software engines grew from a supporting role to the highest-growth component at a 16.6% CAGR, even while hardware kept the 42.5 revenue share. Organizations value cloud orchestration, AI-based liveness detection, and decentralized identity wallets that continuously adapt to evolving fraud. Entrust's acquisition of Onfido aligns with this trajectory, adding deep-fake countermeasures that improved forged-ID prevention five-fold.

The hardware segment remains indispensable where specialized sensors deliver cryptographic templates to secure elements. Infineon's automotive-qualified fingerprint ICs illustrate how production-grade components expand the biometrics market into mobility and access domains. Services, while smallest, record consistent uptake as integrators customize multi-modal deployments for regulated industries.

Iris recognition posts an 18.2% CAGR, supported by liquid-lens optics that lower bill-of-material cost and shrink form factors. Fingerprint remains entrenched with 37.0% of biometrics market share in 2024, thanks to smartphones, payment cards, and time-clock systems. Facial recognition steadily penetrates airports and stadiums, while voice analytics gains footing in call-center authentication.

Behavioral biometrics, particularly gait and keystroke dynamics, add passive layers that elevate security without user friction. Mature fingerprint and facial solutions increasingly pair with iris, palm-vein, or voice modules in multi-modal kits, diversifying revenue and diluting single-modality risk.

Contactless modalities are scaling at 17.1% CAGR as hygiene and convenience trump legacy mindset. The biometrics market size for contact-based systems, despite a 37.0% share in 2024, is losing momentum to touchless fingerprint, face, and iris kiosks rolled out in healthcare and retail. ZKTeco identifies contactless preference as a long-term secular shift.

Invisible sensing, showcased by Continental's in-vehicle camera-laser combo, morphs biometrics beyond access into wellness monitoring. AI improvements cut false rejects, moving touchless accuracy closer to contact-based benchmarks and satisfying high-assurance sectors.

The Biometrics Market Report is Segmented by Component (Hardware, Software, Services), Biometric Modality (Physiological, Behavioral), Contact Type (Contact-Based, Contactless, Hybrid), Authentication Type (Single-Factor, Multi-Factor), Application (Access Control, Payment Authentication, and More), End-Use Industry (Government, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America produced 30.7% of global revenue in 2024, anchored by federal budgets and widespread private-sector adoption. TSA's accelerating lane expansions and DHS's USD 250.8 million line-item for identity management provide a multi-year demand floor for vendors . Canada and Mexico modernize land-border e-gates to streamline trade, reinforcing continental scale.

Asia Pacific records the steepest trajectory with an 18.5% CAGR forecast to 2030. South Korea's nationwide mobile-ID completion, China's codified face-recognition rules, and India's Aadhaar-linked pay services cultivate a unified biometrics market bigger than any single-country program. The region's 4.8 billion digital-wallet users push biometric KYC from optional to mandatory across banks and telecoms.

Europe's growth remains steady under strict GDPR oversight. The EU Entry/Exit System rolls out border biometrics across Schengen states, while the United Kingdom's new trust framework fosters private-sector credential innovation. Nordic pilots prove that on-device processing can satisfy privacy watchdogs without sacrificing speed, shaping procurement criteria across the continent.