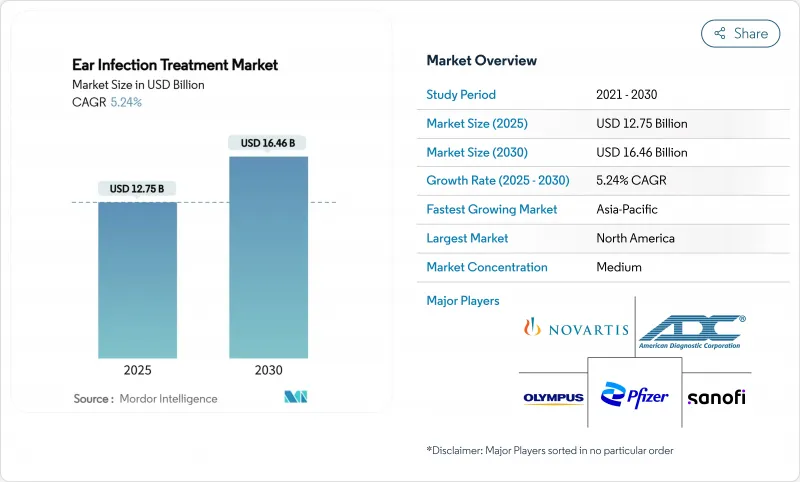

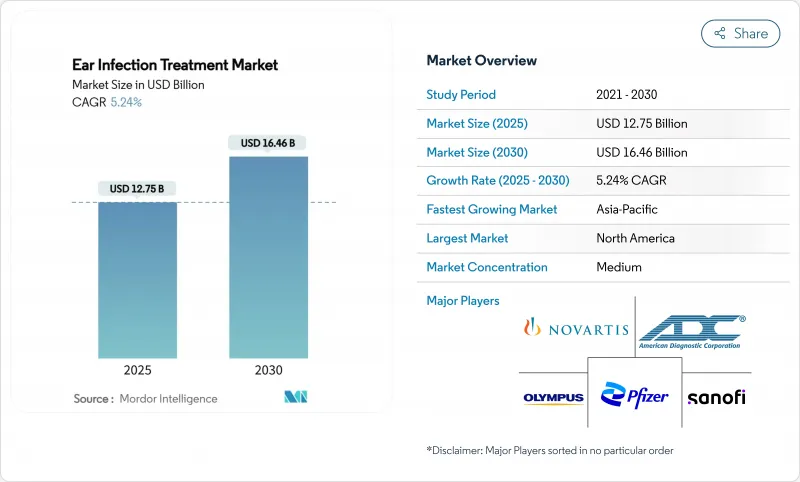

세계의 귀 감염증 치료 시장 규모는 2025년 127억 5,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 5.24%로 확대되어, 2030년에는 164억 6,000만 달러에 달할 것으로 예측됩니다.

성장을 지원하는 것은 항균제 내성 증가, 소아과 질환에 대한 광범위한 부담, 의약품, 진단제, 저침습 장치에 걸친 지속적인 제품 혁신입니다. 최근의 유전체 감시에서는 폐렴구균 분리주의 30%가 페니실린 내성이고, 인플루엔자균 분리주의 30%가 β-락타마제 유전자를 포함하고 있는 것으로 확인되어 임상의사는 항생제의 효능을 유지하는 표적 치료의 도입을 촉진하고 있습니다. 폐렴구균 백신접종 스케줄의 갱신, 프로바이오틱스에 의한 예방법의 등장, FDA에 의한 진찰실에서의 고막절개술의 지지 등, 치료의 선택은 총체적으로 확대되고 있습니다. 한편 인공지능을 활용한 이경검사와 초음파 영상 진단은 진단 불확실성을 줄여 불필요한 항생제 사용을 줄여줍니다. 아시아태평양의 CAGR은 7.94%로 가장 빠르며, 이는 국민 모두 보험 제도에 따라 이비인후과 의료가 지금까지 충분한 서비스를 받지 못한 사람들까지 확대한 것이 요인입니다.

임상적 증거에 따르면 소아의 93%가 3세까지 적어도 한 번의 급성 중이염을 경험하고 있다고 합니다. 감염의 재발에 따른 발육 지연과 학급 폐쇄는 경제적 및 사회적 압력이 되어 치료적 및 예방적 해결책에 대한 수요를 높입니다. 학부모는 유아에 대한 안전성이 입증된 치료를 선호하고 나이에 따라 약물 제형이나 바늘을 사용하지 않는 전달 시스템에 대한 투자를 촉진합니다. 제약 회사는 독성을 증가시키지 않고 부분적 내성을 상쇄하는 고용량 아목시실린 요법으로 대응합니다. 북미와 서유럽 납부자들은 장기적인 비용을 억제하기 위해 폐렴구균 백신접종 부스터 및 프로바이오틱스 보충제를 포함한 예방조치에 대한 환불을 늘리고 있습니다.

Hummingbird TTS와 Tula Systems은 6개월의 어린이에게 사무실에서 귀관을 놓아 전신 마취와 수술실에서 일정 지연을 제거합니다. HCPCS 코드 G0561에 의한 FDA의 승인으로 제3자로의 상환이 확대되고 소아 이비인후과 의사들 사이에서 급속히 보급이 진행되고 있습니다. 곡선 루멘 튜브의 디자인은 체액 배출을 개선하고, 바이오 필름의 형성에 저항하며, 고장률을 감소시킵니다. 초기 임상 데이터는 기존의 스트레이트 튜브에 비해 재수술이 40% 감소하고 비용에 제약이 있는 병원 시스템에서의 채용을 뒷받침하고 있습니다. 아시아태평양 클리닉은 신속한 규제 경로 하에서 이 기술을 수입하기 시작했으며, 이 지역의 성장 예측을 뒷받침하고 있습니다.

증가하는 항균제 내성은 기존의 귀 감염증 치료의 패러다임을 근본적으로 덮는 것으로, 유전체 감시에 의해 1차 중이염의 병원균의 내성 패턴이 우려해야 하는 것으로 밝혀졌습니다. 황색포도상구균의 암피실린 내성은 100%, 세폭시틴 내성은 90.9%인 반면, 녹농균의 플루오로퀴놀론 감수성은 65.2-67.4%에 불과하다고 보고되었습니다. 임상의는 세프트리악손과 같은 제2선택제로 에스컬레이션해야 하며, 직접 약제비가 증가하고, 부작용의 위험이 높아집니다. 엠필릭 광역 스펙트럼 제형은 선택 압력을 증폭시켜 장기적인 시장 지속성을 손상시키는 내성 나선형을 영속시킵니다. 바이오필름 형성 내성 균주의 출현은 특히 만성 및 재발성 감염을 복잡하게 하고, 또 다른 치료 접근법이 필요합니다.

중이 질환은 2024년 매출의 61.86%를 차지했으며, 귀 감염증 치료 시장의 근간이 되고 있습니다. 초음파 귀경 검사와 같은 기술 혁신을 통해 중이 삼출물은 몇 초 안에 감지되고 진단의 확실성이 높아져 부적절한 항생제를 최대 50%까지 줄일 수 있습니다. 중이에 대한 개입에 관한 귀 감염증 치료 시장 규모는 정확하고 부위에 특화된 치료에 대한 지속적인 수요를 반영하여 향후 수년간 확대될 것으로 예측됩니다. 내이 감염은 영상 진단에 의한 전정 후유증의 발견이 향상됨에 따라 시장 규모는 축소되지만, 6.72%의 성장률을 나타냅니다. 외이도 감염은 국소 항균제의 진보에 힘입어 견조하게 추이하고 있습니다.

2세대 약물전달 시스템은 중이강을 대상으로 하는 서방형 겔과 리포솜 운반체로, 전임상에서는 24시간 만에 병원체의 완전 치료를 달성하고 있습니다. 제조업체 각 회사는 표준 치료 요법을 재구성하고 항생제의 총 복용량을 줄일 수 있는 임상 연구를 계획하고 있습니다. 한편, 일회 투여 고막내 주사는 간병인의 부담을 경감해, 어드히어런스를 개선하는 것을 목적으로 한 중요한 임상시험이 진행중입니다.

2024년 귀 감염증 치료 시장 점유율은 세균성 병원체가 72.12%를 차지했습니다. 고활성 폐렴구균 백신의 도입은 박테리아 혈청형의 유행을 재조정하고 항생제 제조자의 민첩한 제형 갱신을 필요로 합니다. 바이러스 감염은 2030년까지 연평균 복합 성장률(CAGR)이 7.28%로 가장 빠르게 성장하는 병인 부문입니다. 항바이러스 연구개발 파이프라인은 이비인후과용으로 조절된 뉴라미니다제 억제제와 엔도뉴클레아제 억제제로 대응하고 있습니다.

곰팡이 감염은 여전히 틈새 시장이지만 면역 결핍 집단에서 임상 적으로 중요합니다. 감시 조사에 의하면, 난치성의 이개 주위 염증례의 41.7%에 진균이 관여하고 있어, 병원체 특이적인 치료제의 필요성이 강조되고 있습니다. 장비 제조업체는 수술 후 콜로니 형성을 억제하기 위해 환기 튜브의 항진균 코팅을 연구합니다.

북미는 2024년 세계 매출의 38.32%를 차지하고 보험 적용과 급속한 기술 도입이 주도했습니다. Medicare는 현재 사무실 기반 고막 절개술에 보험을 적용하고 있으며 외래 수술실에서 치료 건수를 증가시키고 있습니다. 캐나다의 단일 국민 부담 제도는 거의 세계의 백신 접종을 보장하고 중증 감염의 발생률을 감소시키지만 예방적 수요는 유지됩니다. 멕시코 사립 병원의 성장으로 고급 의료기기의 도입이 진행됩니다.

유럽은 프로바이오틱스와 백신 접종 전략을 지원하는 강력한 공중 보건 시스템으로 이어집니다. 항균제 스튜어드십에 관한 이 지역의 지침은 광역 스펙트럼의 처방을 제한하고 합제의 발매를 촉진합니다. 중동 및 아프리카에서는 단편적인 보험 상환이 방해되어 완만한 도입이 기록되고 있지만 자선 사업에 의한 백신 접종의 추진이 혜택을 가져오고 있습니다. 남미에서는 민간보험사가 원격 내시경 검사를 시험적으로 도입하여 아마존의 원격지 커뮤니티에 보급을 도모하고 있습니다.

아시아태평양은 CAGR 7.94%에서 가장 빠르게 성장하는 지역입니다. 중국의 Healthy China 2030 계획은 이비인후과의 능력을 확대하고 인도의 의료기기 마케팅 행동 강령은 투명한 상업화를 촉진합니다. 일본은 청각과 전정을 통합한 클리닉으로 고령화 인구에 대응합니다. 호주 원격 의료 인센티브는 지리적 고립을 극복합니다.

The Ear Infection Treatment Market size is estimated at USD 12.75 billion in 2025, and is expected to reach USD 16.46 billion by 2030, at a CAGR of 5.24% during the forecast period (2025-2030).

Growth is underpinned by rising antimicrobial resistance, the broad pediatric disease burden, and sustained product innovation across drugs, diagnostics, and minimally invasive devices. Recent genomic surveillance confirms that 30% of Streptococcus pneumoniae isolates are penicillin-resistant and that 30% of Haemophilus influenzae strains contain beta-lactamase genes, prompting clinicians to adopt targeted therapies that preserve antibiotic efficacy. Updated pneumococcal vaccination schedules, the emergence of probiotic prophylaxis, and the FDA's support for office-based tympanostomy collectively expand therapeutic options. Meanwhile, artificial-intelligence-enabled otoscopy and ultrasound imaging reduce diagnostic uncertainty and cut unnecessary antibiotic use. Asia-Pacific now registers the fastest regional CAGR at 7.94%, fueled by universal health coverage programs that extend ENT care to previously underserved populations.

Clinical evidence indicates that 93% of children experience at least one acute otitis media episode by age 3, while daycare attendance accelerates cross-contamination and resistant pathogen spread. Developmental delays and classroom absences associated with recurrent infections create economic and social pressure that fuels demand for both therapeutic and prophylactic solutions. Parents prioritize treatments with proven safety in infants, driving investment into age-appropriate drug formulations and needle-free delivery systems. Pharmaceutical companies respond with high-dose amoxicillin regimens that offset partial resistance without escalating toxicity. Payers in North America and Western Europe increasingly reimburse prophylactic measures, including pneumococcal vaccination boosters and probiotic supplements, to curb long-term costs.

The Hummingbird TTS and Tula Systems enable office-based ear tube placement in children as young as 6 months, eliminating general anesthesia and operating-room scheduling delays. FDA recognition through HCPCS code G0561 broadens third-party reimbursement and drives rapid uptake among pediatric otolaryngologists. Curved-lumen tube designs improve fluid drainage and resist biofilm formation, lowering failure rates. Early clinical data show a 40% reduction in repeat procedures compared with conventional straight tubes, encouraging adoption in cost-constrained hospital systems. Asia-Pacific clinics are beginning to import the technology under expedited regulatory pathways, supporting regional growth projections.

Escalating antimicrobial resistance fundamentally challenges traditional ear infection treatment paradigms, with genomic surveillance revealing alarming resistance patterns among primary otitis media pathogens. Studies report 100% ampicillin resistance and 90.9% cefoxitin resistance in Staphylococcus aureus isolates, while Pseudomonas aeruginosa shows only 65.2-67.4% fluoroquinolone susceptibility. Clinicians must escalate to second-line agents such as ceftriaxone, increasing direct drug spend and raising adverse-event risk. Empiric broad-spectrum prescribing amplifies selective pressure, perpetuating a resistance spiral that undercuts long-term market sustainability. The emergence of biofilm-forming resistant strains particularly complicates chronic and recurrent infections, necessitating alternative therapeutic approaches.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Middle ear conditions accounted for 61.86% of 2024 revenue, making them the backbone of the ear infection treatment market. Innovations such as ultrasound otoscopy now detect middle ear effusion within seconds, increasing diagnostic certainty and cutting inappropriate antibiotics by up to 50%. The ear infection treatment market size for middle ear interventions is projected to expand in the coming years, reflecting continual demand for precise, site-specific therapies. Inner ear infections, though smaller in volume, post a 6.72% growth trajectory as imaging improves detection of vestibular sequelae. Outer ear infections remain steady, supported by topical antimicrobial advances.

Second-generation drug-delivery systems target the middle ear space with sustained-release gels and liposome carriers that achieve complete pathogen eradication in 24 hours in preclinical trials. Manufacturers plan clinical studies that could reshape standard-of-care regimens and reduce total antibiotic exposure. Meanwhile, single-dose intratympanic injections are undergoing pivotal trials aimed at lowering caregiver burden and improving adherence.

Bacterial pathogens retained 72.12% ear infection treatment market share in 2024. The introduction of higher-valency pneumococcal vaccines realigns bacterial serotype prevalence, necessitating agile formulation updates among antibiotic producers. Viral infections are the fastest-growing etiologic segment with a 7.28% CAGR to 2030 as molecular diagnostics reveal a larger viral contribution than previously recognized. Antiviral R&D pipelines respond with neuraminidase and endonuclease inhibitors tailored for otologic delivery.

Fungal infections remain niche yet clinically important in immunocompromised cohorts. Surveillance studies show fungi involved in 41.7% of refractory auricular perichondritis cases, underscoring the need for pathogen-specific therapeutics. Device makers investigate antifungal coatings for ventilation tubes to reduce postoperative colonization.

The Ear Infection Treatment Market Report is Segmented by Infection Site (Inner Ear, Middle Ear, Outer Ear), Cause Pathogen (Viral, Bacterial, Fungal), Treatment Type (Medication, Surgical Procedures), Patient Age Group (Pediatrics, Adolescents, and More), End User (Hospitals, ENT Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 38.32% of 2024 global sales, leveraging robust insurance coverage and rapid technology uptake. Medicare now reimburses office-based tympanostomy, driving procedure volumes in outpatient suites. Canada's single-payer system ensures near-universal vaccine coverage, lowering severe infection incidence but sustaining prophylactic demand. Mexico's private hospital growth introduces premium device adoption.

Europe follows with strong public health systems that back probiotic and vaccination strategies. The region's directive on antimicrobial stewardship limits broad-spectrum prescribing, stimulating fixed-dose combination launches. Middle East and Africa record gradual uptake hindered by fragmented reimbursement but benefit from philanthropic vaccination drives. South America sees private insurers piloting tele-otoscopy to reach remote Amazonian communities.

Asia-Pacific represents the fastest-growing region at 7.94% CAGR. China's Healthy China 2030 plan expands ENT capacity, while India's code of conduct for medical-device marketing fosters transparent commercialization. Japan addresses an aging demographic with integrated hearing and vestibular clinics. Australia's telehealth incentives overcome geographic isolation.