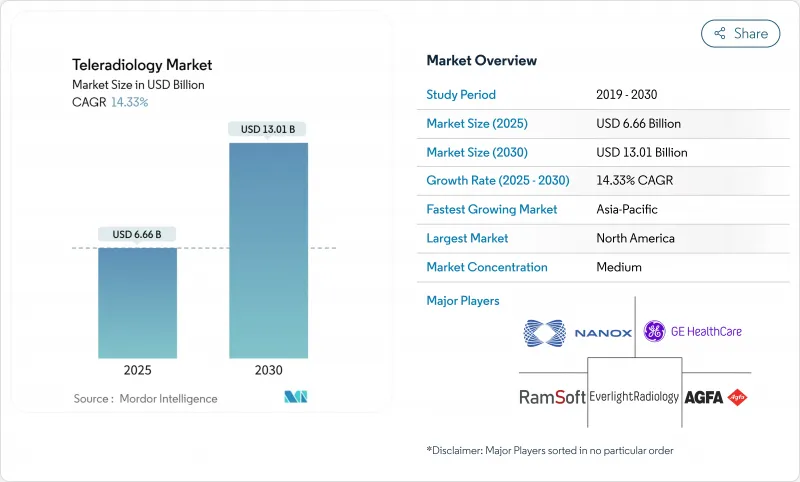

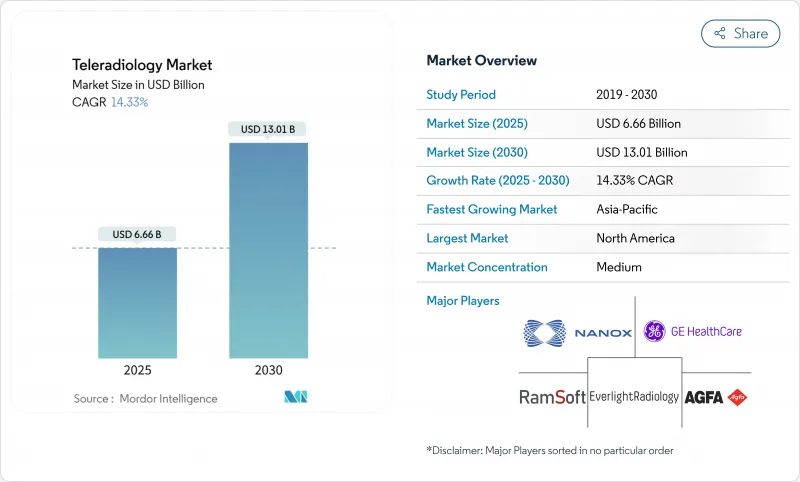

원격 방사선 진단 시장 규모는 2025년에 66억 6,000만 달러로 추정되고 예측 기간(2025-2030년)의 CAGR은 14.33%로, 2030년에는 130억 1,000만 달러에 이를 것으로 예상됩니다.

이 급증은 방사선 기사 부족의 심각화, 광대역의 급속한 확대, 과거에는 옵션이었던 원격 판독을 핵심 임상 유틸리티로 전환하는 클라우드 퍼스트의 이미지 처리 플랫폼과 일치합니다. 노동력 격차는 2028년까지 영국에서 방사선과 의사가 40% 부족할 것으로 예상되지만, 이는 OECD 회원국 전체의 유사한 적자를 반영한 것으로, 원격 진단이 지속적으로 필요합니다. 동시에 노화로 인해 횡단 영상 진단이 필요하기 때문에 방사선 기사의 수가 증가의 길을 따라가고 있습니다. AI를 활용한 트리아지와 제로 실적의 뷰어는 소요 시간과 자본 지출을 줄이고 유연한 성장을 요구하는 프로바이더를 끌어들이고 있습니다. 통합은 가속화되고 있습니다. 2025년 1월에 ONRAD가 Direct Radiology를 인수함에 따라 550개 시설에 서비스를 제공하는 확장 가능한 플랫폼이 탄생하여 원격 방사선 진단가 단편적인 서비스에서 전략적 인프라로 전환되었음을 투자자들에게 보여주었습니다.

영상 진단 수요는 30년간 27% 증가하고 있지만, 방사선과 의사의 수는 가로로, 특히 신경과, 근골격계, 심장흉부 등의 서브 스페셜리티에 있어서, 병원은 24시간 체제로 커버할 수 없었습니다. 원격 판독은 지리적, 시간적 격차를 메우고, 응급실을 지원하며, 유연한 일정을 선호하는 젊은 의사에게 호소합니다. 특히 농촌나 충분한 서비스를 받지 않은 지역에서는 원내에 방사선과를 설치하는 것은 비용이 높아지므로 원격 독영에 의존하고 있습니다. 인적 부족은 구조적이며, 원격 방사선 진단 서비스에 대한 장기적인 수요는 확실합니다.

CT 25.1%, 핵의학 26.9%, X선 17.8%, 초음파 17.3%, MRI 16.9%라는 2055년의 모달리티 증가가 예측되어 이미 인력 부족에 시달리고 있는 의료 시스템에 대한 압박이 되고 있습니다. 만성 질환, 인구 역학의 고령화, 검진 이니셔티브의 확대가 검사 건수 증가를 뒷받침하고 있습니다. 원격 방사선 진단를 이용함으로써 시설은 급여를 늘리지 않고 업무량의 급증을 흡수할 수 있어 환자가 3차 센터까지 이동하지 않고 서브스페셜리스트가 복잡한 사례를 확실히 해석할 수 있습니다.

2024년에는 헬스케어 사업체의 88%가 정보 유출을 보고하고 1억 600만 명의 미국인에게 영향을 미쳤습니다. 레거시 PACS는 최신 세이프 가드가 부족하고 랜섬웨어는 한 달 이상 가동 중지 시간을 유발하여 6,300만 달러를 넘는 손실을 보입니다. GDPR(EU 개인정보보호규정)과 같은 엄격한 프레임워크는 국경을 넘어서는 읽기를 위한 컴플라이언스 비용을 증가시키고, 구매자는 공급업체의 보안 자세를 엄격히 음미하고 사이버 보험과 주권 클라우드 배포 옵션을 제공하는 파트너를 지원하도록 촉구하고 있습니다.

소프트웨어 솔루션은 2024년 매출의 40.54%를 차지했으며 자본 지출을 줄이고 자동 업그레이드를 제공하는 구독 모델에 뒷받침된 지위를 확립했습니다. 이러한 클라우드 플랫폼은 AI 모듈, 제로 실적 뷰어, 벤더 중립 아카이브를 통합하여 임상의가 모든 기기에서 액세스할 수 있습니다. GE Healthcare의 제네시스 포트폴리오는 멀티사이트 워크플로우를 동기화하는 탄력적인 인프라로의 전환을 보여줍니다. On-Premise 서버, 고해상도 워크스테이션 및 네트워크 장비를 대표하는 하드웨어는 5G 게이트웨이와 에지 장치가 널리 보급되고 지역 병원이 위성 수신기를 추가하여 대도시 지역의 독서 허브와 연결됨에 따라 CAGR이 가장 빠른 15.23%를 나타낼 전망입니다. 아웃소싱이 주류가 됨에 따라 서비스 계약은 계속 확대되고 있지만, 서비스의 원격 방사선 진단 시장 규모는 폭발적이기보다는 오히려 꾸준히 확대되고 있습니다.

소프트웨어 웨이브는 데이터센터 유지보수를 필요로 하지 않고 종량 과금의 확장성을 개방함으로써 30%에 가까운 비용 절감을 제공합니다. 공급업체는 우선순위와 하위 전문성을 기반으로 검사를 라우팅하는 AI 오케스트레이션을 통합하여 차별화를 도모하고 유휴 시간과 핸드오프 실패를 줄이고 있습니다. 하이브리드 클라우드 에지 디자인은 로컬로 이미지 전처리를 수행한 다음 AI 추론을 위해 퍼블릭 클라우드로 안전하게 전송할 수 있도록 합니다. 그 결과, 중소득국 전체의 시설이 수백만 달러의 인프라 없이 완전한 기능의 이미지 솔루션을 출시할 수 있어 대응 가능한 원격 방사선 진단 시장이 확대됩니다.

북미는 메디케어의 적용 범위, 견고한 파이버 네트워크, 구매자를 안심시키는 확립된 말프랙티스의 틀을 배경으로 2024년 매출에서 38.83%를 차지해 선두가 되었습니다. 그러나 2025년에 육박한 3-4%의 메디케어 요금 인하가 병원의 이익률을 압박하기 때문에 관리자는 비용 절감을 위한 원격 진료를 가속시킬 필요가 있습니다. 프라이빗 에퀴티는 계속 합니다. RadNet에 의한 1억 300만 달러의 iCAD 인수는 AI 유방 이미지 툴킷을 강화하고 규모의 이점을 강화했습니다. 캐나다와 멕시코는 국경을 넘은 원격 방사선 진단를 야간 진료에 채용해, 바이링갈의 방사선과의를 활용해 지역의 워크플로우를 원활화했습니다.

아시아태평양의 CAGR은 16.16%를 나타낼 것으로 예측되며 세계에서 가장 높습니다. 중국과 인도의 정부 프로그램은 PACS의 도입과 1차 건강 센터로의 광대역을 조성하고 중산 계급의 성장은 고해상도 MRI와 CT 수요를 촉진합니다. 의료기술용 AI에 대한 투자는 2028년까지 2억 5,000만 달러에 달할 것으로 예상되며, RamSoft와 같은 기업은 다국어 고객을 수용하기 위해 지역 허브를 설립했습니다. 호주의 i-Med Radiology Network의 평가 금액은 20억 달러에 달하며 지역 통합에 대한 투자자의 의욕을 보여줍니다.

유럽에서는 EU 회원국의 84%가 이미 어떤 형태로 원격 방사선 진단를 채택하고 있으며 꾸준한 기세를 유지하고 있습니다. 그러나 데이터 주권에 관한 규칙과 노동 조합의 저항은 그 속도를 약화시키고 있습니다. 영국의 헥사라드는 1,300만 유로의 성장 자금을 지원하여 200명 이상의 방사선과 의사를 등록하여 규제된 환경에서도 플랫폼 사업이 성공적임을 입증합니다. 독일 외래 클리닉에서는 79.2%의 추천 의사가 원격 독서를 호의적으로 평가했으며, 지역에서 충족되지 않은 수요를 보여주고 있습니다.

The Teleradiology Market size is estimated at USD 6.66 billion in 2025, and is expected to reach USD 13.01 billion by 2030, at a CAGR of 14.33% during the forecast period (2025-2030).

The surge aligns with widening radiologist shortages, rapid broadband expansion, and cloud-first imaging platforms that convert once-optional remote reading into a core clinical utility. Workforce gaps-expected to leave the United Kingdom 40% short of radiologists by 2028-mirror similar deficits across OECD members and keep remote diagnostics in permanent demand. At the same time, radiology volumes continue to climb as aging populations require more cross-sectional imaging, driving health systems toward outsourced overnight coverage and subspecialty reads. AI-enabled triage and zero-footprint viewers reduce turnaround time and capital outlays, attracting providers seeking flexible growth. Consolidation is accelerating: ONRAD's January 2025 purchase of Direct Radiology created a scaled platform serving 550 sites and signalled to investors that teleradiology has moved from a fragmented service to a strategic infrastructure layer.

Demand for imaging is climbing 27% over three decades, yet radiologist headcount growth is flat, leaving hospitals without round-the-clock coverage, especially in neurology, musculoskeletal, and cardiothoracic subspecialties. Remote reading fills both geographic and temporal gaps, supports emergency departments, and appeals to younger physicians who prioritize flexible schedules. Rural and underserved regions, in particular, rely on remote diagnostics because running an in-house radiology department is cost-prohibitive. The structural nature of the shortage ensures long-term demand for teleradiology services.

Projected 2055 modality growth-CT 25.1%, nuclear medicine 26.9%, X-ray 17.8%, ultrasound 17.3%, MRI 16.9%-adds pressure on health systems already grappling with staffing constraints. Chronic diseases, aging demographics, and expanded screening initiatives drive the volume uptick. Teleradiology allows facilities to absorb workload spikes without proportional payroll growth and ensures subspecialists interpret complex cases without patients travelling to tertiary centers.

In 2024, 88% of healthcare entities reported a breach, affecting 106 million Americans. Legacy PACS lack modern safeguards, and ransomware has caused downtimes exceeding a month and losses above USD 63 million. Strict frameworks such as GDPR elevate compliance costs for cross-border reads, prompting buyers to vet vendor security posture rigorously and favor partners offering cyber-insurance and sovereign-cloud deployment options.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software solutions generated 40.54% of 2024 revenue, a position underpinned by subscription models that cut capital outlays and provide automatic upgrades. These cloud platforms integrate AI modules, zero-footprint viewers, and vendor-neutral archives that clinicians can reach on any device. GE HealthCare's Genesis portfolio exemplifies this move toward elastic infrastructure that synchronizes multisite workflows. Hardware, representing on-premise servers, high-resolution workstations, and network equipment, is set to post the briskest 15.23% CAGR as 5G gateways and edge devices proliferate and as rural hospitals add satellite receivers to link with metropolitan reading hubs. Service contracts keep expanding as outsourcing becomes mainstream, but the teleradiology market size for services scales steadily rather than explosively because buyers blend vendor assistance with in-house IT teams.

The software wave creates cost savings near 30% by eliminating data-center maintenance and unlocking pay-as-you-go scalability. Vendors differentiate by embedding AI orchestration that routes studies based on priority and subspecialty, reducing idle time and failed handoffs. Hybrid cloud-edge designs ensure image pre-processing happens locally, then the study transfers securely to public clouds for AI inference, an architecture that satisfies privacy obligations while preserving bandwidth. As a result, facilities across mid-income countries can spin up full-featured imaging solutions without multimillion-dollar infrastructure, widening the addressable teleradiology market.

The Teleradiology Market Report is Segmented by Component (Hardware, Software, Services), Imaging Technique (X-Ray, Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound, Nuclear Imaging, and More), End User (Hospitals, Diagnostic Imaging Centers, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America led with 38.83% revenue in 2024 on the back of Medicare coverage, robust fiber networks, and established malpractice frameworks that reassure buyers. However, looming 3-4% Medicare fee cuts in 2025 pressure hospital margins, prompting administrators to accelerate cost-saving remote reads. Private equity remains active: RadNet's USD 103 million iCAD acquisition augmented its AI breast-imaging toolkit, reinforcing scale advantages. Canada and Mexico adopt cross-border teleradiology for night coverage, leveraging bilingual radiologists to smooth regional workflow.

Asia-Pacific is forecast for a 16.16% CAGR, the highest worldwide. Government programs in China and India subsidize PACS rollouts and broadband to primary health centers, while middle-class growth fuels demand for high-resolution MRI and CT. Investments in AI for MedTech are projected to hit USD 250 million by 2028, and companies such as RamSoft have planted regional hubs to serve multilingual clients. Australia's I-Med Radiology Network, valued near USD 2 billion, showcases investor appetite for regional consolidation.

Europe maintains steady momentum as 84% of EU members already employ teleradiology in some form. Yet data-sovereignty rules and union resistance temper velocity. The United Kingdom's Hexarad-backed by EUR 13 million in growth funding-adds over 200 radiologists to its roster, illustrating how platform plays can thrive even in regulated environments. Germany's outpatient clinics show positive attitudes, with 79.2% of referring physicians rating remote reading favorably, pointing to unmet demand in rural districts.