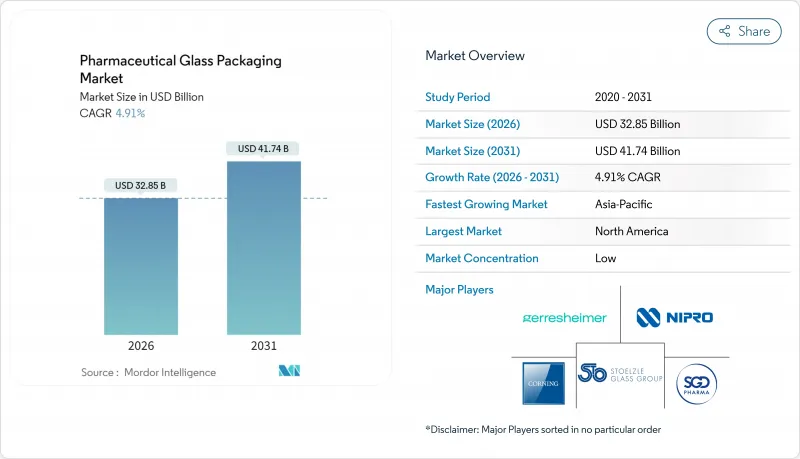

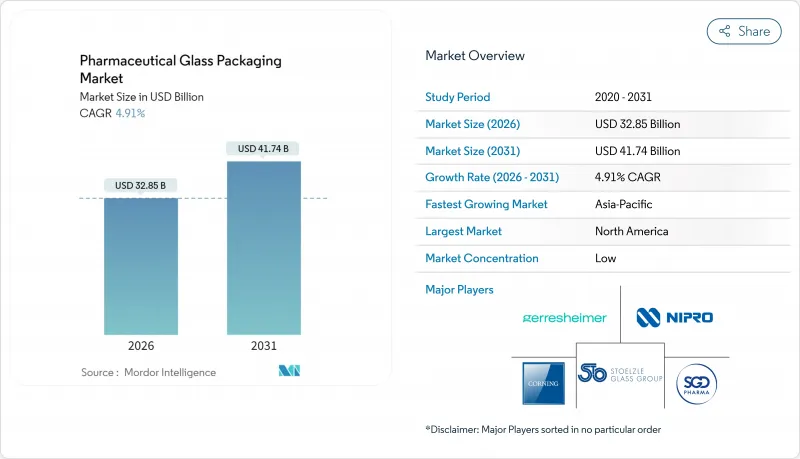

세계의 의약품용 유리 포장 시장은 2025년 313억 1,000만 달러에서 2026년에는 328억 5,000만 달러로 성장하고, 2026년부터 2031년까지 CAGR 4.91%로 성장을 지속해 417억 4,000만 달러에 이를 것으로 전망됩니다.

이 전망은 엄격한 무균성 및 용출물 제한을 충족시키면서 바이오 의약품의 신속한 스케일 업, 분산 백신 생산 및 자가주사 수요 증가에 대응할 수 있는 고부가가치 용기 시스템으로의 꾸준한 전환을 반영합니다. FDA 및 유럽 의약품청에 의한 규제 강화에 의해 제1종 붕규산 유리 포장에 대한 수요가 계속 증가하고 있습니다. 한편, AI를 활용한 검사 기술은 결함 리스크를 저감하면서 생산성을 향상시키고 있습니다. 동시에, 노의 현대화와 재생재 비율의 향상에 의해 제조업자는 규제 준수를 손상시키지 않고 지속가능성 요건에 대응이 가능하게 되고 있습니다. 그 결과, 의약품용 유리 포장 시장은 원재료 가격의 변동이나 첨단 폴리머와의 경쟁 격화라는 과제는 있지만, 안정된 성장 기회를 계속 제공합니다.

규제 데이터에 따르면 2024년 FDA가 승인한 신규 의약품 55개 품목 중 17개 품목이 바이오 의약품이며 바이오 의약품의 지속적인 기세를 뒷받침하고 있습니다. 이에 따라 제조업체는 단백질의 안정성을 확보하고 박리 위험을 줄이는 I 유형의 생산 능력 향상을 가속화하고 있습니다. Stevanato Group의 매출액이 11억 400만 유로로 급증하고 그 중 38%가 고부가가치 솔루션으로 인한 것은 프리미엄 용기가 이 조류를 어떻게 포착하고 있는지를 나타냅니다. 종양학 및 자가면역요법은 피하 투여를 가능하게 하는 대용량 카트리지의 채용을 확대하고 있으며, 환자 중심 투여를 지원하는 의약품 유리 포장 시장의 중요성이 더욱 높아지고 있습니다. 유전자 치료의 지속적인 발전은 냉동 공급망 전체에서 무균성을 유지하는 용기에 대한 의존성을 증가시킬 것입니다. 이러한 추세가 결합되어 생물학적 제형은 구조적 추풍이 불고, 2030년을 훨씬 넘어서는 기준선 수요가 밀려 올라갑니다.

각국 정부가 전략적 백신 비축을 유지하는 가운데 세계 바이알 소비량은 높은 수준을 유지하고 있습니다. SCHOTT가 10억 회분 이상의 COVID-19 백신용 바이알을 생산한 실적은 지속적인 기반 수요를 여실히 보여주고 있습니다. GLP-1 길항제 부족 해소를 위한 유럽의약청(EMA)의 조정은 강인한 공급망 구축에 대한 대처를 더욱 부각시키고 있습니다. 북미에서는 Bormioli Pharma가 FDA 승인 저장 능력을 추가함으로써 지역 매출이 47% 증가하여 수요가 강화되었습니다. 인도 및 동남아시아 전역의 시설 확장도 현지 컨버터에 대한 증분 공급량을 끌어올려 신흥 거점에서 의약 유리 포장 시장을 강화하고 있습니다. 이러한 투자는 광범위한 예방 접종 목표를 지원하는 동시에 팬데믹 초기 급증시에 발견된 주문량의 변동을 완화합니다.

Gerresheimer의 ClearJect 폴리머 주사기는 내충격성과 접착제 불필요한 특징을 갖추고 있어 자가주사요법에 적합합니다. SCHOTT Pharma의 TOPPAC Freeze는 극저온 내구성을 필요로 하는 mRNA 의약품을 타겟으로 하고, 폴리머의 범용성을 뒷받침하고 있습니다. 가정 환경에서 취약한 유리 포장의 환자 안전에 대한 우려가 고부가가치 틈새 시장에서 폴리머 채택을 가속화하고 있습니다. 기존 주사제에서는 유리가 여전히 주류인 한편, 점성 바이오의약품이나 대용량 자동 주사기 분야에서는 폴리머의 점유율 확대가 진행되고 있습니다. 이 경쟁은 중기적으로 의약품 유리 포장 시장에 약간의 억제요인이 생길 것으로 예측됩니다.

바이알은 2025년에 34.78%의 수익을 유지했습니다. 그것의 유연성이 백신, 동결건조 생물 제제, 임상 배치에 이르기 때문입니다. 안정적인 수요로 SGD 파마는 5개 공장에서 하루 800만개 이상의 바이알을 생산하여 세계 공급 지속성을 확보하고 있습니다. 재고 조정이 수렴하고 종양학 파이프라인이 상업 재고를 보충함에 따라 바이알용 의약품 유리 포장 시장 규모가 확대될 것으로 예측됩니다. 프리필 가능한 주사기 및 카트리지는 피하 투여용 생물학적 제제 및 GLP-1 수용체 길항제와 같은 즉시 주사 가능한 형태를 선호하는 제품으로 견인되어 7.15%의 연평균 복합 성장률(CAGR)로 가장 빠르게 확대되고 있습니다. BD의 최신 8mm 바늘은 고점도 제제에 대응하여 채용 장벽 중 하나를 제거했습니다. 경구 현탁액 및 소아용 전해질 분야에서 병은 안정적인 수요를 유지하는 반면, 앰풀은 내열성 마취제의 틈새 수요를 지원합니다. 복합 요법 증가에 따라 듀얼 챔버 시스템 등의 특수 형태도 확대. 전제품에 있어서 AI 검사에 의한 폐기율 저감이 계속되어, 의약품 유리 포장 시장의 이익률을 보호하고 있습니다.

환자 중심의 의료로의 이행에 따라, 제약 기업은 편리성, 복약 준수율 및 통원 횟수 삭감을 우선 과제로 하고 있습니다. 카트리지 펜은 다회 복용을 지원하며 자동 주사기는 전문가의 모니터링 없이 정확한 복용량을 보장합니다. 바이알 제조업체는 경쟁력을 유지하기 위해 모듈식 충전 라인을 도입하여 투명한 용기와 호박색 용기를 최소한의 다운 타임으로 전환 할 수있는 하이브리드 배치를 제공합니다. 입자 발생을 줄이고 실리콘화를 용이하게 하는 코팅 기술은 유리의 성능 한계를 확대합니다. 그 결과, 모든 제품 카테고리가 규제 대응력, 가공성, 총소유비용의 조합으로 경쟁하게 되어 의약품 유리 포장 시장에서의 차별화가 더욱 진행되고 있습니다.

뛰어난 내약품성과 세계 각국 약전에서의 채용에 의해 2025년에는 보로실리케이트 유리(I 유형)가 매출의 54.71%를 차지했습니다. 고농도 바이오의약품과 항체 약물 복합체(ADC)가 불활성 표면을 요구하는 한, 그 이점은 지속될 것입니다. 붕소가 없는 'Valor'와 같은 박리 위험을 실질적으로 제거하는 새로운 조성으로 I 유형 용기의 의약품 유리 포장 시장 규모는 더욱 확대될 것으로 전망됩니다. 한편, 표면 코팅 기술로 약산성 주사제에 대한 적용 범위가 확대되고 저비용으로 성능과 예산의 매력적인 균형을 제공하는 처리된 II 유형 소다 석회 유리는 6.59%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. Gerresheimer의 최신 II 유형 제품 라인은 고가의 붕규산 유리의 채용이 정당화되지 않는 중급 치료제용 옵션을 확충하고 있습니다.

III 유형 유리는 가수분해 스트레스보다 pH 중성이 선호되는 경구 용액, 기침 시럽 및 스포이드 병에 여전히 널리 사용됩니다. 한편, 착색된 호박색 유리는 광분해성 의약품 및 안과용 항바이러스제의 라인 확장을 보호합니다. 주요 제약회사가 스코프 3 배출량 목표를 설정하는 동안 재생재 사용률이 상승하고 있습니다. SGD Pharma는 현재 규제 준수를 손상시키지 않고 특정 제품군에 20% 소비 후 칼렛(유리 분말)을 배합하고 있습니다. 예측 기간에 지속가능성 평가는 조달 결정을 강화하고 라이프사이클 분석이 제약 유리 포장 시장의 모든 유리 유형에 통합된 가치 제안이 될 것입니다.

북미는 2025년 수익의 38.42%를 차지했으며, 활발한 R&D 파이프라인, 강력한 벤처 자금 조달, 엄격한 컴플라이언스 문화가 성장을 이끌었습니다. SCHOTT Pharma는 노스캐롤라이나주에 3억 7,100만 달러를 투자하고, 2030년까지 RTU 주사기의 국내 생산량을 3배로 확대할 계획이며, 지역의 주도적 지위를 더욱 강화합니다. 첨단 제조에 대한 연방정부의 우대조치도 노의 전기 하이브리드화를 가속시켜 탄소삭감 목표에 따른 움직임이 되고 있습니다. GLP-1 치료제와 종양 생물 제제에 대한 견조한 수요는 주요 컨버터에서 다중 이동 시스템의 운영을 지원하고 전통적인 제네릭 의약품의 생산량 변동에 대한 위험을 완화합니다.

유럽은 엄격한 규제 환경과 조기 지속가능성 의무에 힘입어 균형 잡힌 성장을 유지하고 있습니다. 새로운 EU 포장 및 포장 폐기물 규제 2025/40에서는 중요 의약품용 유리가 일부 재활용 할당에서 면제되지만, 브랜드 소유자는 기업의 넷 제로 목표 달성을 향해 칼렛의 통합을 자발적으로 맹세하고 있습니다. 팬데믹 후 전략적 의약품 비축에 대한 정치적 지원은 현지 바이알 카트리지 생산 능력을 촉진하고 있습니다. 그러나, 에너지 비용은 여전히 경쟁적 과제이며, 녹색 전력 요금이 안정되지 않는 한, 일부 제조업체들은 저비용 지역으로의 생산 기지 이전을 강요받고 있습니다.

아시아태평양은 7.72%라는 가장 빠른 CAGR을 기록하고 있으며 중국과 인도의 제조 규모 확대가 견인 역할을 하고 있습니다. 양국의 2023년 바이오 의약품 시장 규모는 6,506억 위안에 이르며 2029년까지 두배로 될 것으로 예측됩니다. 정부의 경기자극책에 의해 국내 제조업체가 용해로의 재건을 가속시키는 가운데 고급 유리 제품의 수입이 촉진되고 있습니다. 다국적 CDMO 기업이 싱가포르와 한국에 충전 및 마무리 공장을 설립하고, 지역의 규격을 미국 및 EU 수준으로 끌어올려, 의약품용 유리 포장의 잠재 시장을 확대하고 있습니다. 동남아시아 백신연구소는 우대자금을 활용하여 충전 및 마무리 라인을 건설하여 바이알 수요를 더욱 밀어 올리고 있습니다.

남미 및 중동, 아프리카는 절대 수로 지연되고 있지만, 현지 제네릭 의약품 제조업체가 수입 의존도 삭감을 위해 시설 규모를 확대하는 움직임이 기세를 늘리고 있습니다. 브라질의 ANVISA(국가위생 감독청)의 엄격한 규제에 의해 포장의 업그레이드가 강요되고 있으며, 걸프 국가는 경제 다각화 계획의 일환으로 의료 분야에 대한 투자를 추진하고 있습니다. 중요한 점으로는 소다재와 LPG 에너지의 지역 공급망이 노용 연료의 우려를 완화하고 있으며, 특정 성장 시장이 의약 유리 포장 시장에서 수출 지향형 생산의 2차적 거점으로 자리잡고 있습니다.

The pharmaceutical glass packaging market is expected to grow from USD 31.31 billion in 2025 to USD 32.85 billion in 2026 and is forecast to reach USD 41.74 billion by 2031 at 4.91% CAGR over 2026-2031.

This outlook reflects a steady pivot toward high-value container systems that can meet rigorous sterility and leachables limits while supporting rapid biologics scale-up, decentralized vaccine production and growing self-injection preferences. Tightened guidelines from the FDA and the European Medicines Agency continue to elevate demand for Type I borosilicate formats, while AI-enabled inspection unlocks higher throughput with lower defect risk. At the same time, furnace modernization and greater recycled content help producers manage sustainability mandates without compromising regulatory compliance. As a result, the pharmaceutical glass packaging market continues to offer reliable growth opportunities, tempered only by raw-material cost swings and rising competition from advanced polymers.

Regulatory data show 17 biologics approvals among 55 new FDA drugs in 2024, underscoring sustained biologics momentum. Manufacturers therefore accelerate Type I capacity upgrades that ensure protein stability and mitigate delamination risk. A revenue jump to EUR 1,104 million at Stevanato Group, with 38% from high-value solutions, highlights how premium containers capture this wave. Oncology and autoimmune therapies increasingly favor large-volume cartridges that enable subcutaneous dosing, reinforcing the critical role of the pharmaceutical glass packaging market in supporting patient-centric delivery. Continued gene-therapy breakthroughs will deepen reliance on containers that maintain sterility across frozen supply chains. Together these trends give biologics a structural tailwind that raises baseline demand well beyond 2030.

Global vial consumption remains elevated as governments keep strategic vaccine reserves. SCHOTT produced enough vials for more than 1 billion COVID-19 doses, illustrating the sustained baseline. EMA coordination to ease GLP-1 agonist shortages further spotlights the drive for resilient supply chains. North American demand strengthened when Bormioli Pharma lifted regional sales 47% after adding FDA-approved storage capacity. Facility expansions across India and Southeast Asia also push incremental volume to local converters, reinforcing the pharmaceutical glass packaging market across emerging hubs. These investments support broad immunization goals while smoothing order volatility seen during the initial pandemic surge.

ClearJect polymer syringes from Gerresheimer deliver break-resistant, glue-free formats that appeal to self-injection therapies. SCHOTT Pharma's TOPPAC Freeze targets mRNA drugs that need deep-cold durability, underscoring polymer versatility. Patient safety concerns for fragile glass in at-home settings accelerate polymer acceptance in high-value niches. While glass maintains dominance for conventional injectables, polymers now capture incremental share in viscous biologics and high-volume autoinjectors. This competitive encroachment creates a modest drag on the pharmaceutical glass packaging market over the medium term.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Vials retained 34.78% revenue in 2025 as their flexibility spans vaccines, lyophilized biologics and clinical batches. Steady demand lets SGD Pharma run more than 8 million vials daily across five plants, safeguarding global supply continuity. The pharmaceutical glass packaging market size for vials is projected to grow as destocking subsides and oncology pipelines refill commercial inventories. Prefillable syringes and cartridges expand fastest at a 7.15% CAGR, propelled by subcutaneous biologics and GLP-1 antagonists that favor ready-to-inject formats. BD's latest eight-millimeter needles address higher viscosity formulations, removing one adoption hurdle. Bottles hold steady in oral suspensions and pediatric electrolytes, whereas ampoules preserve niche demand for heat-stable anesthetics. Specialty formats, including dual-chamber systems, rise alongside complex combination therapies. Across products, AI inspection continues to trim scrap rates, protecting margins within the pharmaceutical glass packaging market.

The shift toward patient-centric care pushes drug developers to prioritize convenience, adherence and reduced clinic visits. Cartridge-based pens accommodate multi-dose regimes, while autoinjectors ensure accurate dose delivery without professional oversight. Vial makers lean on modular filling lines to remain competitive, offering hybrid batches that switch between clear and amber containers with minimal downtime. Coating technologies that reduce particle generation and ease siliconization broaden the performance envelope for glass. Consequently, every product category now competes on a mix of regulatory robustness, machinability and total cost of ownership, heightening differentiation within the pharmaceutical glass packaging market.

Type I borosilicate captured 54.71% revenue in 2025 thanks to sterling chemical resistance and global pharmacopeia acceptance. Its dominance will persist as high-concentration biologics and antibody-drug conjugates demand inert surfaces. The pharmaceutical glass packaging market size for Type I containers benefits further from new compositions like boron-free Valor that virtually eliminate delamination risk. Treated Type II soda-lime glass, however, posts a 6.59% CAGR as surface coatings extend suitability to mildly acidic injectables at lower cost, offering an attractive balance between performance and budget. Gerresheimer's latest Type II lines broaden options for mid-tier therapies that cannot justify premium borosilicate pricing.

Type III glass remains common for oral liquids, cough syrups and dropper bottles where pH neutrality dominates over hydrolytic stress. Meanwhile, colored amber variants shield photolabile drugs and line extensions of ophthalmic antivirals. Recycled content climbs as large pharma institutes Scope 3 emission targets; SGD Pharma now offers 20% post-consumer cullet in selected ranges without compromising regulatory compliance. Over the forecast horizon, sustainability scoring will intensify procurement decisions, making life-cycle analysis an embedded value proposition across all glass types of the pharmaceutical glass packaging market.

The Pharmaceutical Glass Packaging Market Report is Segmented by Product (Bottles, Vials, Ampoules, and More), Glass Type (Type I Borosilicate, Type II Treated Soda-Lime, and More), Drug Formulation (Injectables, Oral Liquids, Ophthalmic/Nasal, Topical), End-User (Pharma Innovator Companies, Generic and CMOs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 38.42% of 2025 revenue, fueled by intense R&D pipelines, strong venture funding and strict compliance culture. SCHOTT Pharma's USD 371 million investment in North Carolina is slated to triple domestic output of RTU syringes by 2030, further cementing regional leadership. Federal incentives for advanced manufacturing also speed furnace rebuilds into electric hybrids, aligning with carbon-reduction targets. Robust demand for GLP-1 therapeutics and oncology biologics sustains multi-shift operations at major converters, guarding against volume swings in legacy generics.

Europe maintains balanced growth, underpinned by its stringent regulatory environment and early sustainability mandates. The new EU Packaging and Packaging Waste Regulation 2025/40 exempts critical pharma glass from some recycling quotas, yet brand owners voluntarily pledge to integrate cullet to meet corporate net-zero goals. Political support for strategic drug reserves post-COVID fosters local vial and cartridge capacity. However, energy costs remain a competitive thorn, pushing some producers to relocate capacity to lower-cost regions unless green power tariffs stabilize.

Asia-Pacific records the fastest 7.72% CAGR, powered by manufacturing scale-ups in China and India where the 2023 biopharma market stood at 650.6 billion yuan and is forecast to double by 2029. Government stimulus packages encourage high-end glass imports even as domestic players ramp furnace rebuilds. Multinational CDMOs establish fill-finish sites in Singapore and South Korea, raising regional specifications to US and EU levels and enlarging the addressable pharmaceutical glass packaging market. Southeast Asian vaccine institutes leverage concessional funding to build fill-finish lines, further lifting vial demand.

South America and the Middle East & Africa trail in absolute numbers but gain momentum as local generics houses expand facility footprints to cut import reliance. Brazil's stringent ANVISA rules compel packaging upgrades, and Gulf states pursue health-care investment drives as part of economic diversification plans. Importantly, regional arteries for soda ash and LPG energy ease furnace-fuel concerns, positioning select emerging markets as secondary hubs for export-oriented production within the pharmaceutical glass packaging market.