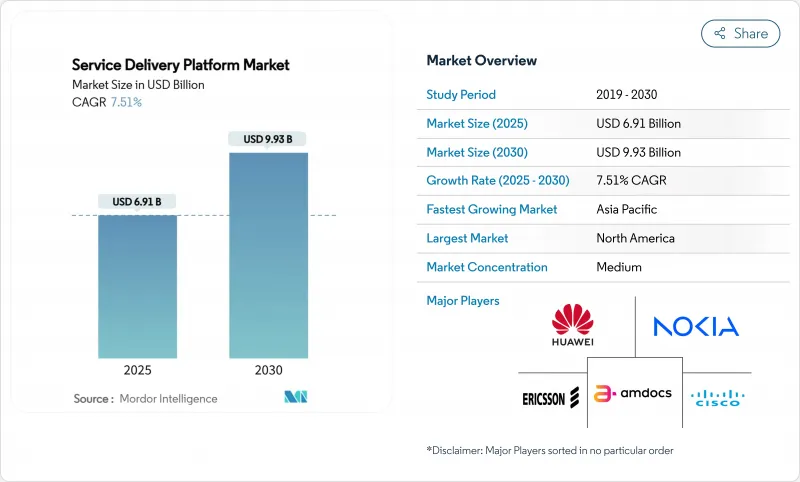

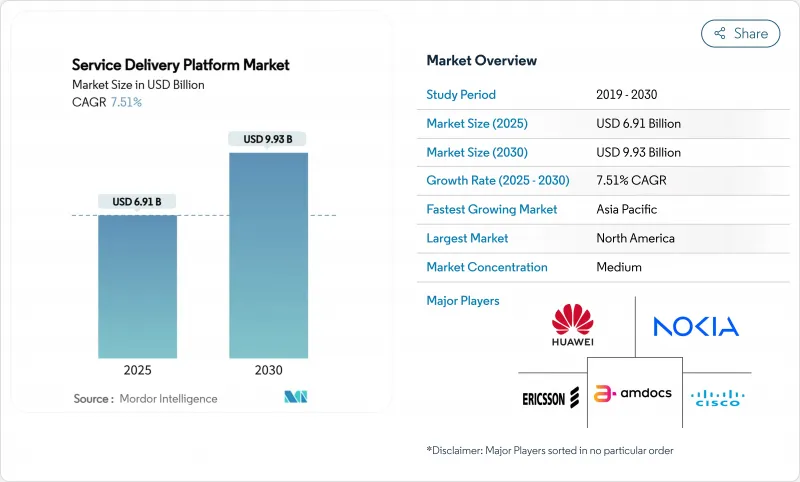

서비스 제공 플랫폼 시장 규모는 2025년에 69억 1,000만 달러, 2030년에는 93억 3,000만 달러로 확대될 것으로 예측되며, 이 기간의 CAGR은 7.51%를 나타낼 전망입니다.

5G의 독립형 배포, 클라우드 네이티브 변혁 전략, 레거시 OSS/BSS 스택의 긴급 리플레이스 등이 함께, 자본은 플랫폼의 현대화를 향하고 있습니다. 통신 사업자는 출시 주기를 단축하고 네트워크 슬라이싱을 가능하게 하며 저지연 기업 이용 사례를 수익화하는 마이크로서비스 아키텍처에 투자하고 있습니다. 소프트웨어 정의의 민첩성은 산업 캠퍼스에서 개인 5G를 채택하고 슈퍼 맞춤형 소비자 제안에 대한 수요가 증가함에 따라 더욱 증폭되고 있습니다. 하이퍼스케일 클라우드 제공업체, 전통적인 네트워크 공급업체, 틈새 소프트웨어 전문가들이 동일한 비즈니스 기회에 집중하고 통합, 파트너십 및 개방형 API 전략을 강요하기 때문에 경쟁이 치열해지고 있습니다.

5G 단위 구축의 경우, 운영자는 밀리초 단위로 네트워크 리소스를 할당하고 오픈 API를 통해 기능을 노출하는 오케스트레이션 계층을 채택해야 합니다. 에릭슨은 네트워크 슬라이싱만으로 2,000억 달러의 새로운 가치를 풀어낼 수 있다고 추정하고 있으며, 싱텔이 2024년에 프리미엄 5G층을 구축하기 위해 소비자용 슬라이싱을 상용화한 이유를 강조했습니다. 커리어가 워크로드를 클라우드 네이티브 코어로 전환했기 때문에 전 세계 모바일 코어에 대한 지출은 2025년 1분기에 전년 동기 대비 32% 급증했습니다. 서비스 기반 아키텍처는 본질적으로 마이크로 서비스에 적합하며 플랫폼 공급업체는 지연, 대역폭 및 보안 보증을 수익화하는 정책 엔진을 통합합니다. 따라서 서비스 제공 플랫폼 시장은 5G 무선 자원을 기업의 SLA에 연결하는 의도 기반 오케스트레이션에 대한 수요를 포착합니다. 건강 관리, 물류 및 미디어에서 더 많은 슬라이스가 가동됨에 따라 수익 기회가 증가하고 플랫폼의 확장성이 경쟁력을 좌우할 것으로 보입니다.

하이퍼스케일 얼라이언스는 통신 사업자의 IT 로드맵을 재구성합니다. Vodafone과 Microsoft의 10년에 걸친 15억 달러의 계약은 유럽과 아프리카 전반에 걸쳐 3억 명의 가입자를 대상으로 하며 워크로드를 Azure로 전환하고 출시 주기를 몇 달에서 몇 주로 단축하는 DevOps 관행을 통합하고 있습니다. Telefonica 독일은 4,500만 명의 사용자를 클라우드 네이티브 5G 코어로 전환하고 서비스 중단 없이 컨테이너화된 네트워크 기능의 성숙도를 입증했습니다. 현재 지속적인 통합과 자동화된 테스트는 신속한 기능 활성화를 지원하고 동적 리소스의 확장은 비용 규율을 향상시키고 있습니다. 공급업체는 SaaS 딜리버리 모델과 종량 라이선스 라이선스를 통해 대응할 수 있는 서비스 제공 플랫폼 시장을 확대하고 있습니다. 장기적으로 클라우드 퍼스트 전략을 통해 통신 사업자는 독점 하드웨어에 대한 의존도를 낮추고 업계를 가로질러 제안을 보다 민첩하게 시작할 수 있을 것으로 보입니다.

메인프레임 시대의 스택을 리플레이스하기 위한 선행 투자는 많은 중견·신흥 시장의 통신 사업자가 본격적인 디지털화를 망설이는 요인이 되고 있습니다. 에어텔 스리랑카(Airtel Sri Lanka)의 변혁은 영업 IT 비용을 80% 절감했지만, 단계적인 자본 주입과 전문가의 컨설팅 지원이 필요했습니다. 소규모 통신 사업자는 코어 사일로를 그대로 남기는 오버레이 접근법에 의존하는 경우가 많아 당분간의 플랫폼 수익을 억제하고 있습니다. 클라우드 구독 모델은 밸런스시트에 압박을 덜어주지만 통합의 복잡성은 여전히 전문 서비스 예산을 크게 좌우합니다. 그 결과, 단기적인 도입 곡선은 평탄해지고, 서비스 제공 플랫폼 시장 전체의 CAGR은 추정으로 마이너스 1.2% 둔화할 가능성이 있습니다.

서비스 제공 플랫폼 시장의 소프트웨어 매출은 CAGR 11.7%로 상승하고 있으며, 사업자가 자체 어플라이언스에서 API 중심 오케스트레이션 스위트로 전환함에 따라 헤드라인 성장률을 상회하고 있습니다. 통합, 마이그레이션 및 관리 운영에 대한 지속적인 수요를 반영하여 2024년 매출의 60.3%는 서비스가 차지했습니다. 벤더는 AI, 애널리틱스, 로우코드 툴 등 서비스 혁신의 타임라인을 단축하기 위해 대폭적인 R&D를 할당하고 있습니다(화웨이만으로도 2024년에 248억 달러를 소비했습니다).

플랫폼 소프트웨어는 네트워크 복잡성을 추상화하고 파트너의 온보딩을 촉진하는 컴포저블 마이크로서비스를 가능하게 합니다. Nexign의 프레임워크와 같은 프로젝트는 통합 기간을 3개월에서 4주로 단축하여 메가폰이 170개 이상의 서비스를 신속하게 배포할 수 있도록 했습니다. 레거시 컷오버 단계와 DevOps를 구현하려면 전문 서비스가 필수적입니다. 이를 종합하면 소프트웨어가 증가함에 따라 서비스 제공 플랫폼 시장 점유율은 모듈형 라이선스 기반 제품의 점유율을 꾸준히 끌어올릴 것입니다.

클라우드 구현은 2024년 세계 매출의 63.1%를 차지했고, 통신 사업자가 자본 확약의 위험을 피하고 탄력적인 스케일링을 추구함에 따라 CAGR 14.2%를 나타낼 전망입니다. 클라우드 퍼스트의 흐름은 T-Mobile이 선불 BSS를 AWS로 마이그레이션하여 하드웨어 오버헤드를 줄이고 가동 시간을 향상시키고 있다는 점에서 분명합니다.

하이브리드 설계도는 데이터 레지던시 규칙에 따라 On-Premise 제어 평면이 의무화된 금융 서비스 및 공공 부문에서 출현합니다. 공급업체의 툴킷은 현재 CI/CD 파이프라인을 자동화하고 제로 터치로 네트워크 기능을 업그레이드할 수 있게 되어 클라우드에 대한 선호를 더욱 향상시키고 있습니다. 그 결과 클라우드 배포로 인한 서비스 제공 플랫폼 시장 규모는 2030년까지 50억 달러 이상에 달할 것으로 예상됩니다.

북미는 2024년 매출의 31.6%를 차지하며 적극적인 5G 배포 스케줄, 주파수 정책, 클라우드에 대한 깊은 전문 지식에 의해 지원되었습니다. Verizon의 200억 달러 프론티어 인수와 전세 345억 달러 콕스 인수와 같은 대규모 합병은 광섬유 실적를 확대하고 엔드 투 엔드 플랫폼 통합을 자극합니다. T-모바일 KKR과의 합작을 통한 메트로넷 인수는 통합 고정 무선 제안을 가속화합니다. 공급망 보안 및 해저 케이블 모니터링에 대한 규제의 초점은 병렬로 컴플라이언스 컨설팅 수요를 창출하여 이 지역공급업체 서비스 포트폴리오를 형성합니다.

아시아태평양의 CAGR은 14.1%로 세계 최고 속도로 예측되는데, 이는 통신사업자가 이미 2024년 상반기 매출액의 19.9%를 차지한 비커넥티비 수익으로 축족을 옮기고 있기 때문입니다. 중국 모바일과 중국 유니콤은 클라우드, 비디오 및 산업용 디지털 서비스에 규모의 이점을 활용합니다. StarHub의 Cloud Infinity 프로그램은 AWS, Google Cloud, Nokia와의 멀티클라우드 오케스트레이션을 활용하여 엔터프라이즈 워크로드에 10밀리초 미만의 대기 시간을 제공하여 아키텍처의 혁신성을 보여줍니다. 각국의 디지털 이코노미 정책은 민간 5G와 스마트 제조업의 전개에 인센티브를 주고 지역의 기세를 강화하고 있습니다.

유럽은 성숙하고 규제가 많은 환경이며 EU의 AI 법과 데이터 주권 지침이 아키텍처 선택에 영향을 미칩니다. Vodafone의 Azure 파트너십은 여러 국가 시장에서 클라우드 네이티브 혁신에 대한 장기적인 자본 헌신을 보여줍니다. 영국의 텔레콤 보안법은 Tier1 사업자에게 258개의 사이버 보안 관리를 실시하도록 의무화하여 플랫폼 업그레이드를 가속화하고 있습니다. 남미와 중동 및 아프리카는 낮은 기준선에서 시작하지만, 모바일 보급률의 상승과 정부의 디지털화 계획은 민첩한 서비스, 전달 프레임 워크에 대한 미래 수요가 왕성하다는 것을 보여줍니다.

The service delivery platform market size stood at USD 6.91 billion in 2025 and is forecast to advance to USD 9.33 billion by 2030, reflecting a 7.51% CAGR over the period.

5G standalone deployments, cloud-native transformation strategies and the urgent replacement of legacy OSS/BSS stacks combine to pull capital toward platform modernization. Operators are investing in microservices architectures that shorten release cycles, enable network slicing, and monetize low-latency enterprise use cases. Software-defined agility is further amplified by private-5G adoption in industrial campuses and by rising demand for hyper-personalized consumer propositions. Competitive intensity is rising as hyperscale cloud providers, traditional network vendors and niche software specialists converge on the same opportunity set, forcing consolidation, partnerships and open-API strategies.

Standalone 5G build-outs obligate operators to adopt orchestration layers that allocate network resources in milliseconds and expose capabilities through open APIs. Ericsson estimates network slicing alone can unlock USD 200 billion in new value, underscoring why Singtel commercialised consumer slicing in 2024 to create premium 5G+ tiers . Global mobile core spending jumped 32% year-over-year in Q1 2025 as carriers moved workloads onto cloud-native cores. Service-based architecture inherently suits microservices, and platform vendors are embedding policy engines that monetise latency, bandwidth and security guarantees. The service delivery platform market therefore captures demand for intent-based orchestration that links 5G radio resources to enterprise SLAs. As more slices go live in healthcare, logistics and media, revenue opportunities will multiply and platform scalability will become a competitive determinant.

Hyperscale alliances are recasting telco IT roadmaps. Vodafone's decade-long USD 1.5 billion pact with Microsoft targets 300 million subscribers across Europe and Africa, shifting workloads to Azure and embedding DevOps practices that shrink release cycles from months to weeks. Telefonica Germany migrated 45 million users to a cloud-native 5G core without service disruption, evidencing maturity of containerised network functions. Continuous integration and automated testing now underpin rapid feature activation, while dynamic resource scaling improves cost discipline. Vendors are responding with SaaS delivery models and pay-as-you-grow licensing, expanding the addressable service delivery platform market. Over the long term, cloud-first strategies will make telcos less dependent on proprietary hardware and more agile in launching cross-vertical propositions.

The upfront investment to replace mainframe-era stacks deters many mid-tier and emerging-market operators from full-scale digitalisation. Airtel Sri Lanka's transformation trimmed operating IT spend by 80% but required phased capital injections and specialist consulting support . Smaller carriers often resort to overlay approaches that leave core silos intact, tempering immediate platform revenues. While cloud subscription models soften balance-sheet pressure, integration complexity still commands sizeable professional services budgets. As a result, near-term adoption curves can flatten, moderating the overall service delivery platform market CAGR by an estimated -1.2 percentage points.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software revenue in the service delivery platform market is climbing at an 11.7% CAGR, eclipsing the headline growth rate as operators migrate from proprietary appliances to API-centric orchestration suites. Services still generated 60.3% of 2024 turnover, reflecting ongoing demand for integration, migration, and managed operations. Vendors allocate substantial R&D-Huawei alone spent USD 24.8 billion in 2024-toward AI, analytics, and low-code tooling that compress service innovation timelines.

Platform software enables composable microservices that abstract network complexity and promote partner onboarding. Projects such as Nexign's framework cut integration windows from three months to barely four weeks, allowing MegaFon to roll out 170-plus offers swiftly . Professional services remain indispensable during legacy cut-over phases and DevOps enablement. Taken together, software gains will steadily lift the service delivery platform market share of modular, license-based products.

Cloud implementations contributed 63.1% of global revenue in 2024 and are increasing at a 14.2% CAGR as carriers de-risk capital commitments and pursue elastic scaling. The cloud-first trajectory is evidenced by T-Mobile migrating its prepaid BSS onto AWS to cut hardware overhead and improve uptime.

Hybrid blueprints are emerging in financial services and public-sector contexts where data residency rules mandate on-premise control planes. Vendor toolkits now automate CI/CD pipelines and provide zero-touch network function upgrades, further tilting preference toward cloud. Consequently, the service delivery platform market size attributed to cloud deployments is expected to eclipse USD 5 billion before 2030.

The Service Delivery Platform Market Report is Segmented by Type (Software, Services), Deployment Mode (On-Premise, Cloud), Application (Telecom Operators, BFSI, Media and Entertainment, Healthcare, Retail and E-Commerce, Government and Public Sector, Others), Network Type (Wireless, Wireline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 31.6% of revenue in 2024, buoyed by aggressive 5G roll-out timetables, supportive spectrum policy and deep cloud expertise. Large-scale mergers such as Verizon's USD 20 billion Frontier acquisition and Charter's USD 34.5 billion Cox purchase expand fibre footprints and stimulate end-to-end platform consolidation. T-Mobile's joint venture with KKR to gain Metronet accelerates integrated fixed-wireless propositions. Regulatory focus on supply-chain security and submarine cable oversight creates parallel compliance consulting demand, shaping vendor service portfolios in the region.

Asia-Pacific is forecast to generate a 14.1% CAGR, the fastest worldwide, as operators pivot toward beyond-connectivity revenue that already formed 19.9% of H1-2024 takings. China Mobile and China Unicom channel scale advantages into cloud, video and industrial digital services. StarHub's Cloud Infinity programme leverages multi-cloud orchestration with AWS, Google Cloud and Nokia to deliver sub-10 millisecond latency for enterprise workloads, illustrating architectural innovation. National digital-economy policies funnel incentives toward private 5G and smart-manufacturing roll-outs, reinforcing regional momentum.

Europe represents a mature, regulation-heavy environment where the EU's AI Act and data-sovereignty mandates influence architectural choices. Vodafone's Azure partnership exemplifies long-term capital commitment to cloud-native transformation across several national markets. The UK Telecoms Security Act compels tier-1 operators to implement 258 cybersecurity controls, prompting accelerated platform upgrades. Although South America and the Middle East and Africa start from lower baselines, rising mobile penetration and government digitalisation agendas signal vibrant future demand for agile service delivery frameworks.