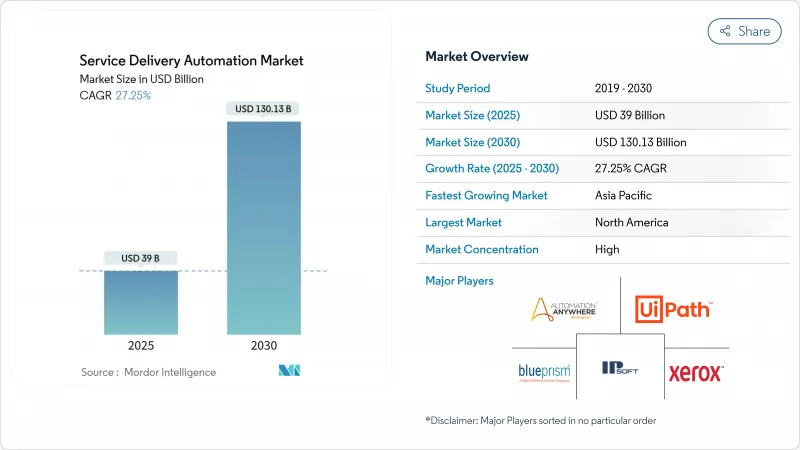

서비스 딜리버리 자동화 시장의 2025년 시장 규모는 390억 달러로 추정되고, CAGR 27.25%로 성장할 전망이며, 2030년에는 1,301억 3,000만 달러에 이를 것으로 예측됩니다.

수요는 고객 대응 프로세스와 백오피스 프로세스에 걸쳐 운영 비용 절감, 사이클 타임 단축, 정밀도 향상을 요구하는 기업으로부터 발생하고 있습니다. 하이퍼오토메이션(RPA, AI, 로우코드 툴의 조합)은 단순한 태스크 실행에서 인지적인 의사결정으로 이용 사례를 확대하여 초기 파일럿에서 기업 전체 롤아웃으로 채용을 뒷받침하고 있습니다. 주요 플랫폼이 일반 인공지능을 통합하고 총 소유 비용을 줄이고 사용 기반 클라우드 전개로 전환함에 따라 공급업체 간 경쟁이 치열해지고 있습니다. 북미는 지역별로 가장 큰 투자액을 차지하지만 아시아태평양은 현지 서비스 센터와 디지털 퍼스트 중소기업이 클라우드 자동화를 대규모로 도입하고 있기 때문에 가장 가파른 성장 곡선을 보여줍니다.

기업은 노동 집약적이고 대량의 워크플로우를 자동화하고 있으며, 프로세스당 평균 30-40%의 비용 절감을 기록하고 있습니다. RPA를 도입한 은행에서는 초년도의 ROI가 3-10배가 되는 경우가 많아 예외 처리의 실수가 대폭 삭감됩니다. 플랫폼 벤더의 사내 조사는 반복 작업이 자동화된 후 직원의 88%가 작업에 대한 만족감을 높이고 있음을 보여주고 있으며 비용 절감과 직원 경험 향상이 일치하는 것으로 나타났습니다. 이 경향은 임금 격차가 큰 BFSI, 통신, 공유 서비스 센터에서 가장 강합니다.

서비스 수준 목표의 엄격화로 인해 조직은 귀환을 줄이면서 프로세스의 주기 시간을 가속화해야 합니다. 서비스 딜리버리 자동화를 도입한 재무관리팀은 보고 실수가 90% 감소했으며, 장부 마감이 기존 수작업에 비해 85배 빨라졌다고 보고되었습니다. 자동화된 트리어지 봇이 서비스 티켓을 몇 분 이내에 해결하므로 업데이트가 신속한 문제 해결에 의존하는 구독 기반 비즈니스의 경우 고객 지원 측정 항목에도 이점이 있습니다.

인지 자동화 프로젝트에는 프로세스 엔지니어링, 데이터 사이언스, 리스크 컨트롤 등 다양한 분야에 걸쳐 인력이 필요합니다. 그러나 수석 아키텍트는 수요가 트레이닝 파이프라인을 능가하기 때문에 공급 부족이 계속되고 있으며, 가치가 높은 전개가 늦어지면서 기업은 비싼 컨설턴트를 계약할 수밖에 없습니다. 로우 코드 시티즌 개발자 도구는 유용하지만 복잡한 교차 시스템 오케스트레이션은 여전히 숙련된 설계자에 의존합니다.

IT 프로세스 자동화는 명확하게 정의된 런북 스크립트와 명확한 ROI 벤치마크를 통해 2024년 서비스 딜리버리 자동화 시장 점유율의 56%를 차지했습니다. 비밀번호 재설정, 백업 검사 및 인시던트 라우팅을 자동화하는 서비스 데스크 팀은 평균 해결 시간을 최대 40% 단축합니다. 이와 병행하여 인지 및 AI 기반 자동화 분야는 봇이 비구조화 입력을 해석할 수 있도록 하는 대규모 언어 모델과 이미지 분석의 진보에 힘입어 CAGR 40.20%로 확대되고 있습니다. 언더라이터는 현재 인지 봇을 도입하고, 클레임 문서를 평가하며, 실시간으로 비정상적인 플래그를 지정함으로써 효율성 향상과 동시에 새로운 수익 흐름을 이끌어 가고 있습니다. 기업이 기초가 되는 RPA 자산에 AI를 거듭함에 따라, 서비스 딜리버리 자동화 시장은 지능형 오케스트레이션을 중심으로 플랫폼의 리프레시 사이클을 예측했습니다.

이 진화는 구매 기준을 변경합니다. 구매자는 작업 자동화, 의사 결정 지원 및 지속적인 학습을 하나의 라이선스로 통합하는 솔루션을 추구합니다. 벤더는 네이티브 AI를 통합하거나 하이퍼스케일 AI 서비스와 제휴함으로써 대응하고, 틈새 스크립트 전용 툴에서 통합 스위트로 지출을 이동시키는 수렴을 창출하고 있습니다. 따라서 서비스 딜리버리 자동화 시장은 단일 거버넌스 프레임워크 하에서 IT와 비즈니스 운영 모두에 대응하는 수가 적지만 보다 광범위한 전개를 기울이고 있습니다.

소프트웨어 플랫폼은 2024년 매출의 61.56%를 차지했습니다. 이러한 플랫폼에는 현재 가치 증명 구축을 가속화하는 컴퓨터 비전, 프로세스 마이닝 및 거버넌스 콘솔이 내장되어 있습니다. 그러나 서비스는 CAGR 15.00%로 소프트웨어를 초과할 것으로 예측됩니다. 자동화가 수백 가지 프로세스로 확대됨에 따라 기업은 로드맵 설계, 변경 관리, 봇의 건전성 모니터링, 지속적인 개선 프로그램이 필요하지만, 내부 팀은 이를 흡수하는 데 어려움을 겪고 있습니다. 따라서 컨설팅 회사 및 시스템 통합사업자는 가치 평가, 시티즌 개발자의 인에이블먼트, 센터 오브 엑셀런스 운영을 위한 프레임워크를 번들로 제공합니다. 결과적으로, 서비스 딜리버리 자동화 시장의 예산 구성은 순수한 라이선스에서 지속적인 관리 서비스로 꾸준히 이동하고 있습니다.

매니지드 서비스의 서비스 딜리버리 자동화 시장 규모는 지속적인 컴플라이언스 테스트 및 감사 로그가 필수적인 규제 산업에서 특히 빠르게 확대되고 있습니다. 공급업체는 현재 SLA 준수, 버전 업그레이드 및 보안 패치 적용을 다루는 책임 공유 매트릭스를 갖춘 '자동화-as-a-서비스' 모델을 제공합니다. 이러한 구독 지향 제공은 엔터프라이즈급 신뢰성을 추구하는 중소기업에 매력적입니다.

서비스 딜리버리 자동화 시장 보고서는 업계를 유형별(IT 프로세스 자동화, 비즈니스 프로세스 자동화 등), 컴포넌트별(소프트웨어 플랫폼, 서비스), 전개 모드별(온프레미스, 클라우드), 조직 규모별(대기업, 중소기업), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), IT 서비스, 통신 및 미디어 등), 지역별로 분류합니다.

북미는 여전히 서비스 딜리버리 자동화 시장에서 가장 큰 허브이며 높은 인건비, 성숙한 클라우드 인프라 및 주요 플랫폼 공급업체의 본사에 의해 지원됩니다. 금융기관 및 헬스케어 시스템이 도입의 선을 긋고 있으며, 많은 경우 인지 봇과 애널리틱스를 통합하여 예외를 예측하고 SLA 위반을 미연에 방지하고 있습니다. 일반 인공지능의 시도는 광범위하게 진행되고 있으며, 법률 요약 및 규정 준수 내러티브를 초안하기 위해 대규모 언어 모델을 시험적으로 도입하는 기업도 있습니다.

아시아태평양이 가장 급성장하고 있습니다. 인도와 필리핀에서는 디지털 근로자를 활용하여 인건비 절감에 열성적인 세계 서비스 센터를 설립하고 중국의 보험 회사는 급증하는 보험 계약을 관리하기 위해 보험금 청구의 자동화를 진행하고 있습니다. 스마트 제조 및 물류의 디지털화를 위한 정부의 자극 방법은 AGV를 스케줄하기 위한 오케스트레이션 봇에 의존하는 창고의 자동화를 촉진합니다. 현지 벤더는 가격 중심의 번들 제품을 제공하고 ASEAN 시장의 중견 기업에 대한 침투를 가속화하고 있습니다.

유럽에서는 북부 및 서부 경제 지역에서 꾸준한 보급을 볼 수 있습니다. EU의 일반 데이터 보호 규칙(General Data Protection Regulation)은 기업이 봇의 모든 작업을 기록하고 자동화 및 감사 추적을 일치시키는 제어를 통합하도록 요구합니다. 독일과 베네룩스 제조업 콩그로 매리트는 현장 보고서를 자동화하고 있으며, 북유럽 공공기관은 시민들의 문의를 다국어로 처리하기 위해 채팅봇을 도입하고 있습니다. 의사 결정은 신중합니다. IT 지출은 투명성이 높은 투자 회수가 가능한 프로젝트를 선호하며 서비스 딜리버리 자동화 시장 전체에 여전히 크게 기여하고 있는 단계적인 롤아웃을 추진하고 있습니다.

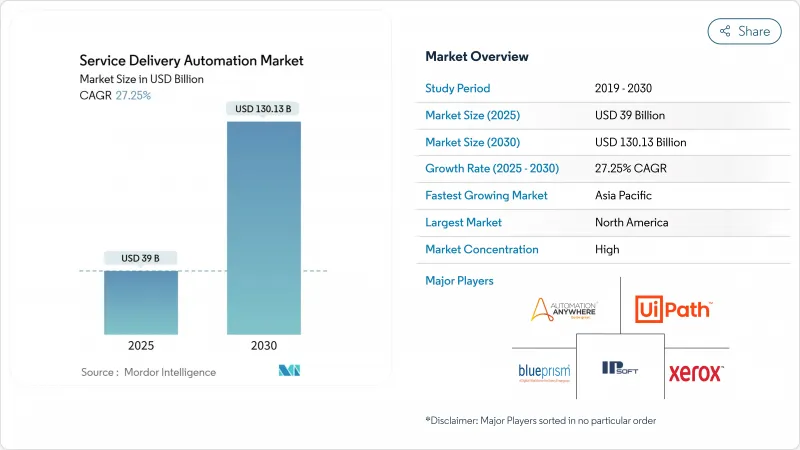

The service delivery automation market is valued at USD 39 billion in 2025 and is projected to grow at a 27.25% CAGR, reaching USD 130.13 billion by 2030.

Demand stems from enterprises seeking lower operating costs, faster cycle times, and higher accuracy across customer-facing and back-office processes. Hyperautomation- the combination of RPA, AI, and low-code tools- is expanding use cases from simple task execution to cognitive decision making, pushing adoption beyond early pilots into enterprise-wide rollouts. Vendor competition is intensifying as leading platforms embed generative AI, reducing total cost of ownership,, and shifting to usage-based cloud delivery. North America accounts for the largest regional spend, yet Asia-Pacific shows the steepest growth curve as local service centers and digital-first SMEs embrace cloud automation at scale.

Enterprises continue to automate labor-intensive, high-volume workflows and record average savings of 30-40% per process. Banks that deploy RPA often earn 3-10 times ROI in year one and cut exception-handling errors markedly. Internal surveys by platform vendors reveal that 88% of employees experience higher job satisfaction after repetitive tasks are automated, signaling that cost savings align with workforce experience gains. This sentiment is strongest in BFSI, telecommunications and shared service centers where wage differentials are high.

Tighter service-level targets have forced organizations to accelerate process cycle times while reducing rework. Financial control teams that add service delivery automation report 90% fewer reporting errors and close books up to 85 times faster than previously manual workflows. Customer response metrics also benefit: automated triage bots resolve service tickets within minutes, boosting retention in subscription-based businesses where renewal hinges on rapid issue resolution.

Cognitive automation projects require multi-disciplinary talent covering process engineering, data science and risk controls. Yet senior architects remain in short supply as demand outpaces training pipelines, delaying high-value deployments and forcing companies to contract premium-priced consultants. Low-code citizen-developer tooling helps, but complex cross-system orchestration still relies on experienced designers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

IT Process Automation held 56% of service delivery automation market share in 2024 owing to well-defined run-book scripts and clear ROI benchmarks. Service desk teams that automate password resets, backup checks and incident routing cut mean-time-to-resolve by up to 40%. In parallel, the Cognitive/AI-based Automation segment is expanding at a 40.20% CAGR, fueled by advances in large language models and image analytics that let bots interpret unstructured inputs. Underwriters now deploy cognitive bots to assess claim documents and flag anomalies in real time, unlocking new revenue streams alongside efficiency wins. As firms layer AI onto foundational RPA estates, the service delivery automation market anticipates a platform refresh cycle centred on intelligent orchestration.

This evolution changes purchasing criteria. Buyers increasingly seek solutions that combine task automation, decision support and continuous learning inside one license. Vendors respond by embedding native AI or partnering with hyperscale AI services, creating a convergence that shifts spend away from niche script-only tools toward unified suites. The service delivery automation market is therefore tilting toward fewer but broader deployments that serve both IT and business operations under a single governance framework.

Software Platforms represented 61.56% of 2024 revenue because every automation journey begins with a licence. These platforms now ship with built-in computer vision, process mining and governance consoles that accelerate proof-of-value builds. However, Services are projected to outpace software at a 15.00% CAGR. As automation scales to hundreds of processes, enterprises need roadmap design, change management, bot health monitoring, and continuous improvement programs that internal teams struggle to absorb. Consulting firms and system integrators thus bundle frameworks for value assessment, citizen-developer enablement and center-of-excellence operation. The result is a steady shift in budget mix from pure licences toward ongoing managed services inside the service delivery automation market.

The service delivery automation market size for managed services is expanding particularly fast in regulated industries where continuous compliance testing and audit logs are mandatory. Vendors now offer "automation-as-a-service" models with shared responsibility matrices covering SLA adherence, version upgrades and security patching. This subscription-oriented delivery appeals to SMEs that lack an internal IT operations bench yet want enterprise-grade reliability.

The Service Delivery Automation Market Report Segments the Industry Into by Type (IT Process Automation, Business Process Automation, and More), Component (Software Platforms, and Services), Deployment Mode (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, Information Technology Services, Telecommunications and Media, and More), and Geography.

North America remains the largest hub for the service delivery automation market, supported by high labor costs, mature cloud infrastructure and headquarters of leading platform vendors. Financial institutions and healthcare systems spearhead adoption, often integrating cognitive bots with analytics to predict exceptions and pre-empt SLA breaches. Generative AI experimentation is widespread, with firms piloting large language models to draft legal summaries and compliance narratives.

Asia-Pacific records the steepest growth trajectory. India and the Philippines host global service centers keen to reduce attrition costs through digital workers, while Chinese insurers automate claims to manage surging policy volumes. Government stimulus for smart manufacturing and logistics digitization fuels warehouse automation that relies on orchestration bots to schedule AGVs. Local vendors offer price-sensitive bundles, accelerating penetration into medium-sized enterprises across ASEAN markets.

Europe exhibits steady uptake across Northern and Western economies. The EU's General Data Protection Regulation prompts businesses to embed controls that log every bot action, aligning automation with audit trails. Manufacturing conglomerates in Germany and Benelux automate shop-floor reporting, while public agencies in the Nordics deploy chatbots to handle citizen queries in multiple languages. Decision making is cautious: IT spending favors projects with transparent payback, driving phased roll-outs that still contribute significant volume to the overall service delivery automation market.