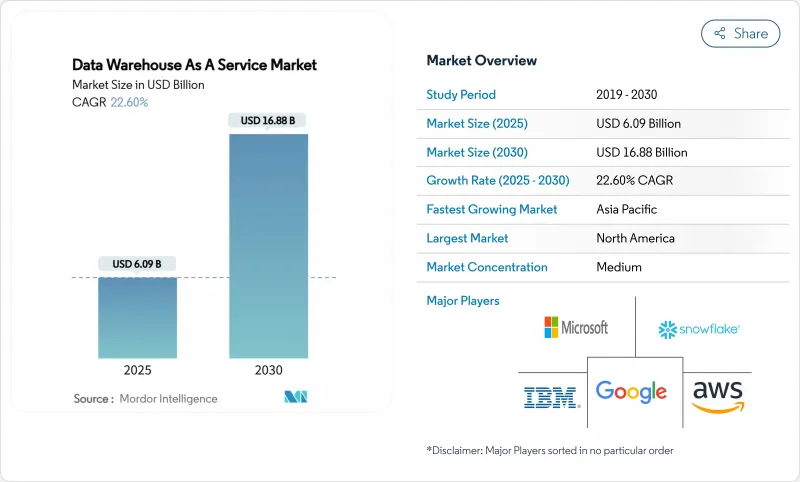

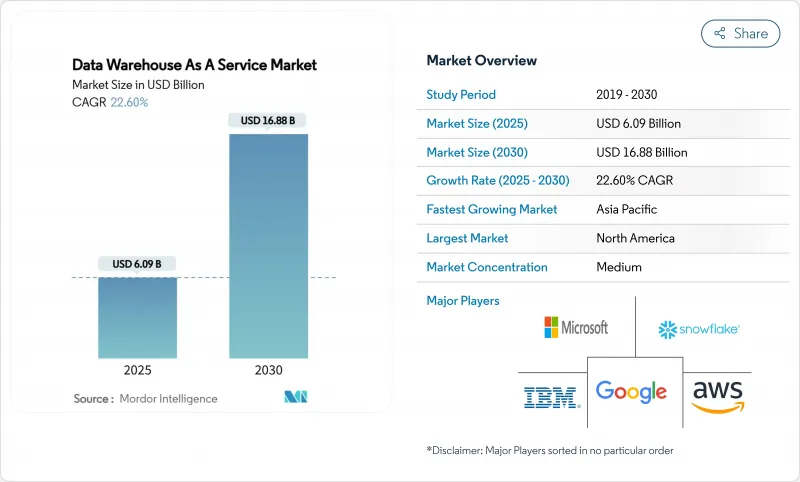

DWaaS(Data Warehouse As A Service) 시장 규모는 2025년에 60억 9,000만 달러에 달하고, 2030년에는 168억 8,000만 달러에 도달할 것으로 예상되며, 예측 기간의 CAGR은 22.6%를 나타낼 전망입니다.

최신 클라우드 네이티브 애널리틱스에 대한 왕성한 수요, 기업 인공지능 워크로드 증가, 종량 과금에 의한 비용 효율성이 주요 성장 요인이 되고 있습니다. 현재의 도입에서는 퍼블릭 클라우드 플랫폼이 대부분을 차지하고 있지만, 기업이 워크로드의 배치를 최적화하면서 락인을 회피하기 때문에 멀티클라우드와 하이브리드 아키텍처가 전체 확대를 웃돌고 있습니다. 지출의 대부분은 여전히 대기업이 차지하고 있지만, 셀프 서비스 툴에 의해 진입 장벽이 낮아지고, 서버리스 스케일링에 의해 용량 계획이 불필요하게 되었기 때문에 중소기업(SME)의 도입이 급속히 증가하고 있습니다. 업계별로는 금융서비스가 도입 페이스를 올리고 있지만, 헬스케어 및 생명과학는 임상 데이터와 연구 데이터의 통합에 의해 정밀의료 프로그램이 가속되기 때문에 가장 급속히 도입이 진행되고 있습니다. 하이퍼스케일 제공업체는 통합 에코시스템을 활용하는 반면, 전문가들은 멀티클라우드 이식성과 머신러닝 기능을 통합하여 차별화를 도모하고 있습니다.

엔터프라이즈는 정기적인 배치 보고서에서 서브초 단위의 대시보드 및 예측 모델에 피드하는 스트리밍 아키텍처로 전환하고 있습니다. ABB는 40개의 다른 ERP 시스템에서 단일 Snowflake 인스턴스로 데이터를 통합하여 실시간 생산 시각화를 통해 수백만 달러의 비용 절감을 실현했습니다. 에지 게이트웨이는 생산 라인 근처에서 시간 감응형 원격 측정을 필터링하고 클라우드 데이터 웨어하우스는 용량 병목 현상 없이 복잡한 조인 및 과거 동향 분석을 수행합니다. 이러한 저지연 파이프라인은 자율적인 설비 최적화, 동적 가격 설정, 즉각적인 무단 관리를 지원합니다. 더 많은 연결 장치가 보급됨에 따라 실시간 분석은 계속해서 최우선 지출 항목이 되어 고정 노드가 아닌 인제스트 비율에 따라 확장되는 탄력적인 DWaaS 용량에 대한 수요가 증가합니다.

최신 데이터 웨어하우스 레이어는 구조화된 테이블과 구조화되지 않은 파일을 혼합하여 스토리지 계층에서 모델 학습을 가능하게 합니다. Snowflake와 NVIDIA의 협업을 통해 특수 GPU를 컴퓨팅 클러스터에 통합하면 추론 가속 중에 데이터가 보안 경계를 벗어나지 않습니다. Databricks는 데이터 사이언스자가 대시보드를 실행하는 것과 동일한 SQL 엔드포인트를 사용하여 페타바이트 스케일 로그에서 기능을 구축할 수 있도록 하는 레이크하우스 스토리지 형식을 통합합니다. 대규모 언어 모델에 의해 구동되는 자연 언어 쿼리 어시스턴트는 비즈니스 사용자의 애널리틱스 액세스를 민주화하고, 보다 광범위한 조직에서의 채용을 촉진하며, DWaaS(Data Warehouse As A Service) 시장 전체의 컴퓨팅 소비를 증가시킵니다.

유럽에서는 일반 데이터 보호 규정(General Data Protection Regulation)의 요구 사항이 아시아에서는 새로운 현지화 법령이 국경을 넘은 데이터의 이동을 제한하고 다국적 기업의 클라우드 전략을 복잡하게 하고 있습니다. 민감한 자산을 타사 클라우드에 집계하는 것은 위협 행위자에게 매력적이며 기업은 광범위한 암호화, 제로 트러스트 액세스 및 지속적인 자세 모니터링의 도입을 강요합니다. 보안 책임 분담 모델 자체가 특히 클라우드 보안에 특화된 인력이 부족한 팀에게는 책임의 위치를 모호하게 하고, 조달 사이클을 장기화하고 도입을 지연시킬 수 있습니다.

퍼블릭 클라우드 플랫폼은 2024년 DWaaS(Data Warehouse As A Service) 시장 규모의 65.5%를 차지했는데, 이는 기업이 턴키 확장성과 세계 가용성을 우선했기 때문입니다. AWS는 깊은 서비스 통합으로 세계 매출의 약 34%를 획득했으며, Microsoft Azure는 Office 365의 발판이 확립됨에 따라 조달이 용이해졌습니다. 프라이빗 클라우드 인스턴스는 소블린 만다드가 외부 호스팅을 할 수 없을 때 뿌리 깊게 존재하지만, 높은 운영 오버헤드는 성장을 억제합니다.

하이브리드 클라우드와 멀티클라우드 배포는 2030년까지 연평균 복합 성장률(CAGR) 24.6%를 나타낼 것으로 예측됩니다. 이는 기업이 공급업체 간에 애널리틱스를 분산하여 잠금을 피하고, 지역별 비용 차이를 활용하고, 기밀성이 높은 데이터 세트를 우선적인 소블린 플랫폼에 배치하기 때문입니다. Google Cloud의 BigQuery Omni는 물리적 데이터 마이그레이션이 없는 크로스클라우드 쿼리를 가능하게 하고 상호 운용성 기능을 통해 igless 요금 및 대기 시간 패널티를 줄일 수 있음을 보여줍니다. Snowflake의 개방형 Polaris Catalog는 AWS, Azure, Google Cloud 간에 메타데이터를 표준화하여 마이그레이션을 더욱 용이하게 합니다.

대기업은 복잡한 거버넌스 요구와 여러 부문에 걸친 애널리틱스 시설을 통해 2024년 DWaaS(Data Warehouse As A Service) 시장 점유율의 62.2%를 차지했습니다. 이러한 기업은 고급 보안 계층을 도입하고 수천 명의 동시 사용자를 지원하며 웨어하우스를 기존 ERP, CRM 및 리스크 엔진과 통합합니다.

한편, 중소기업은 서버리스 엔진이 용량 계획의 장애물을 없애기 때문에 2030년까지 연평균 복합 성장률(CAGR) 26.4%를 나타내 수익 증가를 가장 촉진합니다. 로우 코드 캡처 커넥터와 자연 언어 쿼리 인터페이스를 통해 비즈니스 분석가는 데이터 사이언스 전문 팀 없이도 예측 모델을 시작할 수 있어 대규모 기업과의 능력 격차가 줄어듭니다. 학술 연구는 중소기업 애널리틱스 프로그램의 주요 성공 요인으로 하드웨어 예산이 아니라 기업 문화의 변화를 강조합니다.

북미는 2024년 세계 매출의 39.6%를 차지하며, 풍부한 데이터센터용량, 유리한 클라우드 조달 정책, 기술, 금융, 헬스케어 등 각 분야의 풍부한 기술 기반에 힘입었습니다. 하이퍼스케일러 각 회사는 지역 특화된 AI 가속기와 소블린 클라우드 존을 지속적으로 시작하고 프리미엄 애널리틱스 계층 수요를 지원하고 있습니다. 메인 주 클라우드 마이그레이션으로 대표되는 연방 및 주 정부 기관은 공공 부문 워크로드를 위한 클라우드 웨어하우스를 더욱 검증하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 24.8%로 가장 빠르게 성장하고 있는 지역으로 대규모 하이퍼스케일 구축과 정부의 디지털 경제 로드맵에 지원되고 있습니다. 싱가포르의 GovTech와 같은 공공 부문의 모범 사례는 규제의 명확화와 국가가 지원하는 클라우드 교육이 기업의 도입주기를 단축하는 방법을 돋보이게합니다.

유럽에서는 높은 애널리틱스 수요와 엄격한 주권법제의 균형을 맞추고 있습니다. 벤더는 EU 한정 리전, 기밀 컴퓨팅 엔클레이브, 소블린 메타데이터 서비스를 시작함으로써 대응하고 있습니다. 다국적 금융 기관은 분산 데이터 메쉬 아키텍처를 도입하고 국경을 넘어서는 위험 분석을 유지하면서 현지 거주 규칙을 준수하고 있습니다. 남미와 중동, 아프리카는 전자상거래 확대 및 스마트시티 구상과 관련하여 소규모이면서 비즈니스 기회가 확대되고 있습니다.

The data warehouse as a service market size reached USD 6.09 billion in 2025 and is projected to climb to USD 16.88 billion by 2030, translating into a 22.6% CAGR over the forecast period.

Strong demand for modern, cloud-native analytics, rising enterprise artificial-intelligence workloads, and the cost efficiencies of pay-as-you-go pricing are the principal growth engines. Public-cloud platforms dominate current deployments, yet multi-cloud and hybrid architectures are outpacing overall expansion as firms hedge against lock-in while optimizing workload placement. Large enterprises still account for a majority of spending, but small and medium enterprises (SMEs) are increasing adoption rapidly as self-service tooling lowers entry barriers and serverless scaling eliminates capacity planning. Vertically, financial services set the adoption pace, whereas healthcare and life sciences log the fastest gains because unified clinical and research data accelerates precision-medicine programs. Competitive intensity remains moderate; hyperscale providers leverage integrated ecosystems while specialists differentiate through multi-cloud portability and built-in machine-learning features.

Enterprises are shifting from periodic batch reporting to streaming architectures that feed sub-second dashboards and predictive models. ABB consolidated data from 40 disparate ERP systems into a single Snowflake instance and unlocked multimillion-dollar savings through real-time production visibility . Edge gateways now filter time-sensitive telemetry close to manufacturing lines, while cloud data warehouses execute complex joins and historical trend analyses without capacity bottlenecks. These low-latency pipelines support autonomous-equipment optimization, dynamic pricing, and instantaneous fraud controls. As more connected devices proliferate, real-time analytics will remain a top spending priority, reinforcing demand for elastic DWaaS capacity that scales on ingestion rates rather than fixed nodes.

Modern data-warehouse layers blend structured tables with unstructured files, enabling model training inside the storage tier. Snowflake's collaboration with NVIDIA embeds specialized GPUs alongside compute clusters so data never leaves the security perimeter during inference acceleration . Databricks integrates lakehouse storage formats that let data scientists build features over petabyte-scale logs using the same SQL endpoints powering dashboards. Natural-language query assistants driven by large language models democratize analytics access for business users, fueling broader organizational adoption and increasing overall compute consumption across the data warehouse as a service market.

General Data Protection Regulation requirements in Europe and new localization statutes in Asia restrict cross-border data movement, complicating multinational cloud strategies. Consolidating sensitive assets inside third-party clouds heightens the appeal for threat actors, forcing enterprises to deploy pervasive encryption, zero-trust access and continuous posture monitoring. The shared-responsibility security model itself can blur accountability lines, especially for teams lacking dedicated cloud-security talent, thereby extending procurement cycles and slowing adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Public-cloud platforms held 65.5% of the data warehouse as a service market size in 2024 as enterprises prioritized turnkey scalability and global availability. AWS captured roughly 34% of worldwide revenue thanks to deep service integration, while Microsoft Azure benefited from established Office 365 footprints that eased procurement. Private-cloud instances persist where sovereignty mandates preclude external hosting, but higher operational overhead tempers growth.

Hybrid and multi-cloud deployments are projected to record a 24.6% CAGR through 2030 as firms distribute analytics across providers to avoid lock-in, exploit regional cost differentials and place sensitive datasets on preferred sovereign platforms. Google Cloud's BigQuery Omni allows cross-cloud querying without physical data moves, showing how interoperability features reduce egress fees and latency penalties . Snowflake's open Polaris Catalog further eases migration by standardizing metadata across AWS, Azure and Google Cloud.

Large organizations controlled 62.2% of the 2024 data warehouse as a service market share due to complex governance needs and multi-department analytics estates. They deploy advanced security layers, support thousands of concurrent users and integrate warehouses with legacy ERP, CRM and risk engines.

In contrast, SMEs will drive the highest incremental revenue, expanding at a 26.4% CAGR through 2030 as serverless engines remove capacity-planning hurdles. Low-code ingestion connectors and natural-language query interfaces allow business analysts to launch predictive models without dedicated data-science teams, narrowing capability gaps versus larger peers. Academic studies highlight cultural change as the primary success factor for SME analytics programs, not hardware budgets.

The Data Warehouse As A Service Market Report is Segmented by Deployment Model (Public Cloud, Private Cloud, Hybrid/Multi-cloud), End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (BFSI, Government and Public Sector, and More), Service Type (Enterprise DWaaS, Operational Data-Store As A Service, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 39.6% of global revenue in 2024, buoyed by abundant data-center capacity, favorable cloud procurement policies and a deep skills base across technology, finance and healthcare verticals. Hyperscalers continuously launch region-specific AI accelerators and sovereign-cloud zones, sustaining demand for premium analytics tiers. Federal and state agencies, exemplified by the State of Maine's cloud migration, further validate cloud warehouses for public-sector workloads .

Asia-Pacific is the fastest-growing region with a 24.8% CAGR through 2030, supported by massive hyperscale build-outs and government digital-economy roadmaps. Public-sector exemplars such as Singapore's GovTech highlight how regulatory clarity and state-sponsored cloud training shorten enterprise adoption cycles.

Europe balances high analytics demand with stringent sovereignty legislation. Vendors respond by launching EU-only regions, confidential computing enclaves and sovereign-metadata services. Multinational financial institutions implement distributed data-mesh architectures to comply with local residency rules while preserving cross-border risk analytics. South America plus the Middle East & Africa exhibit growing, albeit smaller, opportunity pools linked to e-commerce expansion and smart-city initiatives; however, infrastructure gaps and macro-economic volatility moderate near-term uptake.