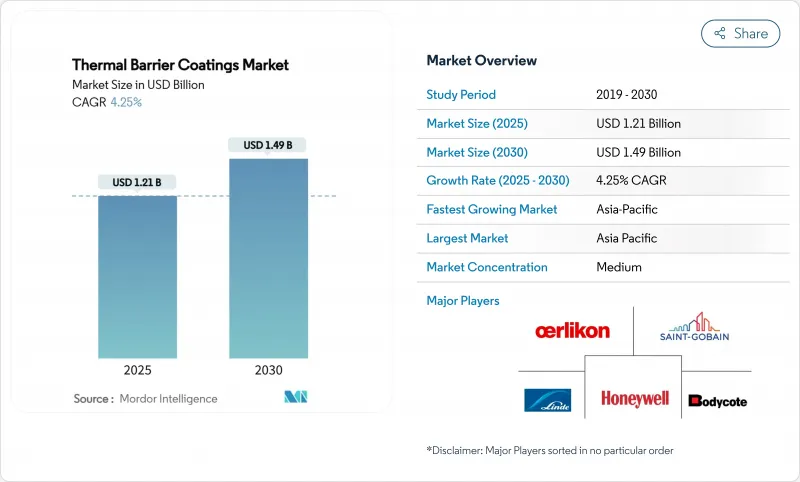

열차폐 코팅 시장 규모는 2025년에 12억 1,000만 달러로 추정 및 예측되고, 2030년에 14억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 4.25%를 나타낼 전망입니다.

지속적인 수요는 고온 가동 가스 터빈, 중량에 민감한 항공우주 엔진, 그리고 신뢰성 있는 단열을 위해 모두 첨단 세라믹-금속 스택에 의존하는 새로운 초음속 플랫폼에서 비롯됩니다. 상업 항공 분야의 향상된 연비 목표, 산업용 발전에서 발생하는 CO2 배출 억제 필요성, 그리고 초고온 연구 프로그램에 대한 지속적인 투자가 열 차단 코팅 시장의 상승 곡선을 뒷받침하고 있습니다. 기존 공급업체들이 스마트 스프레이 공장을 도입하는 한편 신규 진입업체들이 틈새 시장 및 소량 응용 분야를 공략하면서 중견 기업 중심의 분산 구조가 경쟁 강도를 형성하고 있습니다. 한편, 다년간의 가격 변동성 이후 이트리아 안정화 지르코니아(yttria-stabilized zirconia) 및 희토류 안정제(rare-earth stabilizers)의 공급망 회복탄력성은 여전히 전략적 우선순위로 남아 있습니다.

차세대 터보팬 엔진 코어는 현재 약 1,650°C에서 연소되어 터빈 고온 부위에 극한의 열 사이클링을 견딜 수 있는 다층 세라믹 채택을 요구합니다. 희토류 지르코네이트는 기존 8YSZ보다 낮은 격자 열전도율을 제공하여 금속 온도를 임계값 이하로 유지하는 이중층 구조에 대한 신규 특허를 촉진하고 있습니다. GE 에어로스페이스는 2025년 세라믹 매트릭스 복합재 및 관련 코팅에 10억 달러를 배정하며, 연료 중립 추진 시스템이 강력한 열 관리에 달려 있음을 시사했습니다. 지속 가능한 항공 연료는 새로운 연소 화학 반응이 연소기 내 열 유동을 변화시켜 현장에서 작동하는 상태 모니터링 센서를 갖춘 스마트 코팅의 가치를 높임으로써 복잡성을 가중시킵니다.

중국, 인도, 걸프 지역의 복합발전소는 50% 중반대의 열효율을 달성하기 위해 1,500°C 이상으로 가동 중이며, 이로 인해 흡입 공기 냉각 및 수소 연소기 적용이 변형 내성 코팅에 대한 관심을 높이고 있습니다. 터빈 연소 온도가 1% 상승할 때마다 연료 비용이 절감되며, 이는 재생에너지 중심의 전력망 안정화를 위해 발전사들이 설비를 현대화함에 따라 내열성 코팅 시장을 견인하고 있습니다. 공급업체들은 이제 10분 이내에 공회전 상태에서 최대 부하로 전환할 때 발생하는 열충격을 완화하는 기능적 그레이딩 스택을 선보이고 있습니다.

2020년 글로벌 지르콘 모래 생산량은 28% 감소했으며 아직 완전히 회복되지 않아 코팅제 생산사들이 마진을 잠식하는 가격 급등에 노출되고 있습니다. 이트륨은 여전히 중국 광산에 집중되어 있으며, 2022년 생산량은 명목 생산 능력 1,500톤 대비 45톤에 그쳐 열차단 코팅 시장에 지정학적 위험을 지속시키고 있습니다. 주요 공급업체들은 전략적 재고 확보와 가돌리늄 같은 대체 도핑제 사용으로 위험 노출을 제한하고 있습니다.

2024년 세라믹 탑코트는 열장벽 코팅 시장의 56.02%를 차지하며, 이트리아 안정화 지르코니아 시스템이 제공하는 탁월한 단열 성능을 입증했습니다. 항공우주 주요 업체들이 가돌리늄 지르코네이트와 8YSZ를 결합한 이중층 스택을 CMAS 저항성 향상을 위해 인증함에 따라 세라믹 제품의 열장벽 코팅 시장 규모는 지속적으로 확대될 전망입니다.

금속 본드 코트는 하위 층에 불과하지만, 균일한 알루미나 스케일을 형성하고 스패레이션을 지연시키는 새로운 MCrAlY 화학 성분 덕분에 5.91%의 연평균 성장률(CAGR)로 가장 빠른 성장을 기록하고 있습니다. 금속간 화합물 및 그레이디드 코트는 부품 수명이 25,000시간을 초과하는 발전소 개조 프로그램에서 확산되고 있습니다. 고엔트로피 합금 코팅은 여전히 연구 대상이지만, 더 넓은 온도 범위에서 상 안정성을 약속합니다.

에어 플라즈마 스프레이는 2024년 41.64% 점유율을 유지했으며, 터빈 베인, 슈라우드, 연소기 패널 전반에 걸쳐 넓은 재료 적용 범위와 경제적인 처리량으로 선호됩니다. 디지털 트윈 모델은 이제 실시간으로 토치 전류를 조정하여 기공률을 ±1% 이내로 유지함으로써 품질 중심의 항공우주 공급망을 지원합니다.

플라즈마 스프레이-PVD는 열 사이클에 유연하게 대응하는 기둥형 미세구조를 저압 증기 플룸으로 증착하기 때문에 5.48%의 연평균 성장률(CAGR)로 상승 중입니다. 전자빔 PVD는 광폭체 엔진의 단결정 블레이드에 대한 프리미엄 선택으로 남아 있는 반면, HVOF는 석유 및 가스 밸브의 내마모성 코팅 시장을 주도합니다. 용액 전구체 플라즈마 스프레이와 CVD는 고밀도, 균열 없는 필름이 필수적인 틈새 시장을 차지합니다.

아시아태평양 지역은 2024년 열 차단 코팅 시장의 35.14% 점유율을 차지했으며, 2030년까지 연평균 5.05%의 성장률을 보일 것으로 예상됩니다. 이 지역은 중국의 50GW 가스 터빈 건설 프로그램과 일본이 국내 및 수출 부품 모두에 코팅을 적용하는 수직 통합 항공기 엔진 공급망의 혜택을 받고 있습니다. 한국 조선소는 이중 연료 LNG 엔진에 세라믹 스택을 채택하고 있으며, 인도의 민간 항공우주 생태계는 단일 통로 제트기에 특화된 독립 스프레이 공장을 추가하고 있습니다.

북미는 강력한 항공우주 2차 공급망을 바탕으로 초음속 연구개발(R&D) 분야 최대 투자국으로 자리매김했습니다. 미국 에너지부는 1,700°C 터빈 입구 온도에 적합한 이트륨-알루미늄-가넷 변형체 연구를 지원하는 초고온 연구를 추진 중입니다. 캐나다는 몬트리올의 지역 제트기 프로그램용 코팅을 지원하며, 멕시코 바히오 클러스터는 글로벌 자동차 OEM 업체를 위한 터보 부품 코팅을 수행하며 통합 공급망에 기여합니다.

유럽은 설비 증가율은 낮지만 기술력은 여전히 풍부합니다. 독일 자동차 제조사들은 지적재산권 보호를 위해 터보차저 생산라인에 자체 스프레이 부스를 개조 설치합니다. 영국과 프랑스는 ‘호라이즌 유럽’ 연구비를 상변화 세라믹 연구에 투입합니다. 동유럽의 낮은 인건비는 계약 코팅 업체를 유인하지만, REACH 규정 준수를 위해 저감 시스템에 대한 신속한 투자가 필수적입니다. 중동 같은 신흥 지역은 대규모 가스 터빈 애프터마켓 계약을 활용하는 반면, 남미는 중유 발전 장치에 코팅을 적용해 황화 현상을 완화합니다.

The Thermal Barrier Coatings Market size is estimated at USD 1.21 billion in 2025, and is expected to reach USD 1.49 billion by 2030, at a CAGR of 4.25% during the forecast period (2025-2030).

Sustained demand stems from hotter-running gas turbines, weight-sensitive aerospace engines, and new hypersonic platforms that all rely on advanced ceramic-metal stacks for reliable insulation. Greater fuel-efficiency targets in commercial aviation, the need to curb CO2 from industrial power generation, and persistent investments in ultra-high temperature research programs underpin the upward curve of the thermal barrier coatings market. Competitive intensity is shaped by mid-sized fragmentation as legacy suppliers introduce smart-spray factories while newer entrants chase niche, low-volume applications. Meanwhile, supply chain resilience for yttria-stabilized zirconia and rare-earth stabilizers remains a strategic priority after a multi-year run of price volatility.

Next-generation turbofan cores now burn near 1,650 °C, forcing turbine hot sections to adopt multi-layer ceramics that can survive intense thermal cycling. Rare-earth zirconates deliver lower lattice thermal conductivity than conventional 8YSZ, prompting new patents in double-layer architectures that keep metal temperatures below critical thresholds. GE Aerospace earmarked USD 1 billion in 2025 for ceramic matrix composites and allied coatings, signaling that fuel-neutral propulsion hinges on robust thermal management. Sustainable aviation fuels add complexity because new flame chemistries alter heat flux in combustors, raising the value of smart coatings with in-situ health sensors.

Combined-cycle plants in China, India, and the Gulf are running at >1,500 °C to chase mid-fifties thermal efficiency, so inlet air cooling and hydrogen-capable combustors are sharpening the focus on strain-tolerant coatings. Every percentage point of turbine firing-temperature gain trims fuel cost, which propels the thermal barrier coatings market as utilities modernize fleets to stabilize grids dominated by renewables. Vendors now field functionally graded stacks that dampen thermal shock when ramping from idle to full load in under ten minutes.

Global zircon sand output slipped by 28% during 2020 and has not fully recovered, exposing coat producers to price spikes that erode margin. Yttrium remains heavily concentrated in Chinese mines, where output reached only 45 t in 2022 against nameplate capacity of 1,500 t, maintaining geopolitical risk for the thermal barrier coatings market. Leading suppliers have turned to strategic stock builds and alternate dopants such as gadolinium to cap exposure.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Ceramic top coats contributed 56.02% to the thermal barrier coatings market in 2024, underscoring the unmatched thermal insulation offered by yttria-stabilized zirconia systems. The thermal barrier coatings market size for ceramic products is expected to keep expanding as aerospace primes qualify double-layer stacks that pair gadolinium zirconate with 8YSZ for better CMAS resistance.

Metal bond coats, while only a sub-layer, register the quickest growth at 5.91% CAGR, thanks to new MCrAlY chemistries that form uniform alumina scales and delay spallation. Intermetallic and graded coats are spreading in power-plant retrofit programs where component lives stretch beyond 25,000 h. High-entropy alloy coats remain a research subject but they promise phase stability across wider temperature bands.

Air plasma spray held 41.64% share in 2024, favoured for its wide material window and economical throughput across turbine vanes, shrouds, and combustor panels. Digital twin models now adjust torch current in real time to keep porosity within +-1%, supporting the quality-centric aerospace supply chain.

Plasma spray-PVD is climbing at a 5.48% CAGR because its low-pressure vapour plume deposits columnar microstructures that flex with thermal cycles. Electron-beam PVD stays the premium choice for single-crystal blades in wide-body engines, whereas HVOF dominates wear-resistant coatings in oil and gas valves. Solution precursor plasma spray and CVD occupy niches where dense, crack-free films are mandatory.

The Thermal Barrier Coating Market Report Segments the Industry by Product (Metal, Ceramic, and More), Coating Technology (Air Plasma Spray (APS), High-Velocity Oxygen Fuel (HVOF), and More), Coating Material (Yttria-Stabilized Zirconia (8YSZ), Rare-Earth Zirconates (GdZrO, Lazro), and More), End-User Industry (Aerospace, Power Plants, and More) and Geography (Asia-Pacific, North America, Europe, and More).

Asia-Pacific held a 35.14% share of the thermal barrier coatings market in 2024 and is set to grow at 5.05% CAGR to 2030. The region gains from China's 50-GW gas-turbine build-out program and Japan's vertically integrated aero-engine supply chain that coats both domestic and export components. South Korea's shipyards adopt ceramic stacks on dual-fuel LNG engines, and India's private aerospace ecosystem adds independent spray shops dedicated to single-aisle jets.

North America benefits from its strong aerospace tier base, standing as the largest spender on hypersonic R&D. The U.S. Department of Energy funds ultra-high temperature research that explores yttrium-aluminium-garnet variants suited for 1,700 °C turbine inlet temperatures. Canada supports coatings for regional-jet programs in Montreal, while Mexico's Bajio cluster coats turbo parts for global auto OEMs, feeding integrated supply chains.

Europe remains technology-rich despite lower installed capacity growth. Germany's carmakers retrofit turbocharger lines with in-house spray booths to protect intellectual property. The UK and France channel Horizon Europe grants to phase-shifting ceramic research. Eastern Europe's lower labour cost lures contract coaters, but compliance with REACH regulation obliges rapid investment in abatement systems. Emerging regions such as the Middle East leverage large gas-turbine aftermarket deals, whereas South America applies coatings on heavy-fuel power units to mitigate sulphidation.