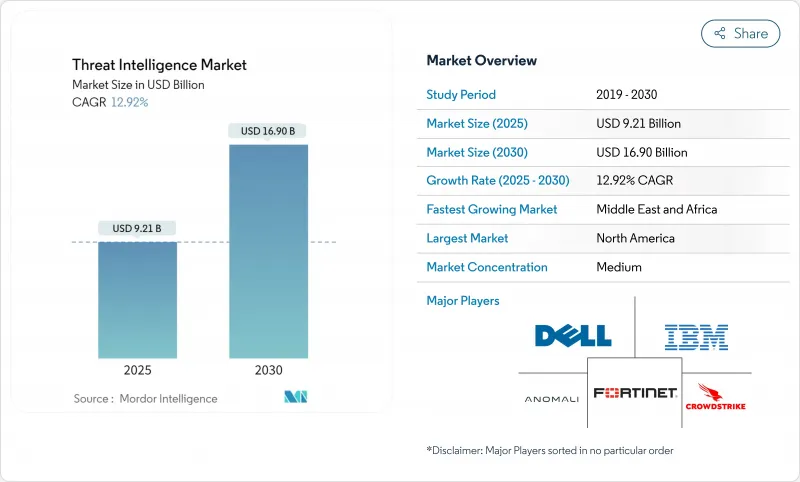

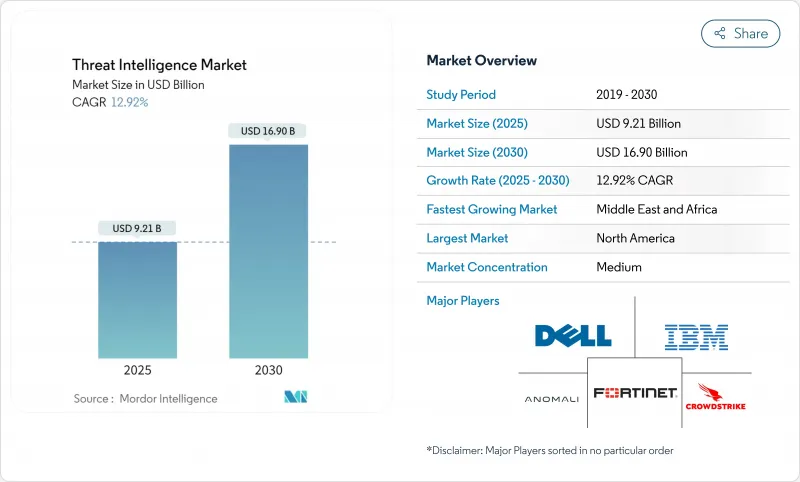

위협 인텔리전스 시장의 2025년 시장 규모는 92억 1,000만 달러로 평가되었고 CAGR은 12.92%를 나타낼 것으로 예측되며 2030년에는 169억 달러에 달할 전망입니다.

클라우드 도입 확대, 공격자의 AI 활용 가속화, EU-NIS2 지침과 같은 강화된 규제 프레임워크로 인해 사전 대응형 인텔리전스 플랫폼에 대한 지출이 증가하고 있습니다. 보안 리더들은 대응 시간을 단축하고 침해 비용을 낮추는 풍부한 컨텍스트 기반 분석을 우선시하는 한편, 보험사와 투자자들은 사이버 위험 인수 전에 실시간 인텔리전스 피드를 검토합니다. 대형 벤더 간 통합으로 플랫폼 범위가 확대되고 있지만, 특정 산업별 인텔리전스가 필요한 분야에서는 전문 공급업체의 역할이 여전히 중요합니다. 국가 차원의 활동 증가와 암호화폐를 통한 랜섬웨어 카르텔 자금 조달로 위협 환경은 변동성을 유지할 것으로 예상되며, 이는 모든 주요 산업 분야의 투자 모멘텀을 지속시킬 전망입니다.

AI 생성 다형성 악성코드는 실시간으로 코드를 재작성하여 기존 시그니처 기반 도구를 무력화시키고 방어자가 행동 기반 분석에 의존하도록 강요합니다. IBM 연구에 따르면, 이러한 악성코드는 이제 인간과의 접촉 없이 몸값 협상을 진행하며 클라우드 구성에 따라 전술을 전환하여 사고 대응을 복잡하게 만듭니다. 미국 법무부는 최근 AI 기반 공격을 통해 2억 6300만 달러 상당의 암호화폐를 탈취한 조직을 해체하며 재정적 위험을 강조했습니다. 북미 기업들은 머신러닝 탐지 예산을 증액하고 있어, 위협 인텔리전스 시장이 클라우드 워크로드 보호에 필수적입니다.

2024년 10월부터 시행되는 NIS2 지침은 약 30만 개의 유럽 기업에 의무적 위험 평가, 사고 보고, 공급망 감시를 적용합니다. 벌금은 1천만 유로 또는 글로벌 매출의 2%에 달할 수 있어 이사회가 실시간 정보 수집을 최우선 과제로 삼도록 압박합니다. EU 고객을 대상으로 하는 블록 외부 다국적 기업도 준수해야 하므로, 감사 준비 완료 정보 피드를 패키징하는 벤더에게 기회가 확대됩니다.

STIX와 TAXII가 2021년 OASIS 표준으로 채택되었음에도, 많은 기존 플랫폼은 여전히 독점 형식을 처리하여 원활한 데이터 공유를 방해합니다. 탐색적 연구에 따르면 통합 복잡성과 불일치하는 표기법이 주요 장애물로 확인되었습니다. 그 결과 조직들은 플랫폼 업그레이드를 지연시키며 단기 지출을 억제하고 있습니다.

2024년 솔루션 부문이 글로벌 매출의 56%를 차지하며 플랫폼이 위협 인텔리전스 시장에서 압도적 우위를 점하고 있습니다. 마이크로소프트 디펜더 위협 인텔리전스만 하루 78조 개의 신호를 처리하는 등 규모적 이점이 두드러집니다. 이러한 지배력은 플랫폼 연계 위협 인텔리전스 시장 규모가 2030년까지 지속적으로 성장할 것으로 예상되는 근거입니다. 주요 벤더들은 행동 분석을 위한 AI를 도입해 분석가의 업무 부담을 줄이고 탐지 정확도를 높이고 있습니다.

관리형 및 전문 서비스는 14.5%의 연평균 성장률(CAGR)로 제품 성장률을 앞지르며, 이는 인재 부족과 복잡성 증가를 반영합니다. SANS 설문조사에 따르면 많은 기업이 기술 격차를 해소하기 위해 위협 사냥 업무를 아웃소싱합니다. 전개를 중심으로 한 교육 파트너십은 구매자가 더 빠르게 가치를 창출할 수 있게 하여 서비스 채택을 촉진하며, 특히 위협 인텔리전스 산업의 중견 시장 부문에서 두드러집니다.

2024년 온프레미스 전개는 지출의 55%를 차지했으며, 규제 강도가 높은 부문은 현지 데이터 거주를 선호합니다. 그럼에도 클라우드 호스팅 플랫폼은 16.8% CAGR로 가장 빠르게 성장하며, 공급업체의 보안 강화와 Microsoft Defender Threat Intelligence의 High 인증 획득 등 FedRAMP 확장에 대한 신뢰를 시사합니다. 시장 관측통들은 클라우드 기반 위협 인텔리전스 시장 규모가 예측 기간 후반에 온프레미스 총량을 추월할 것으로 전망합니다.

하이브리드 접근법은 기존 센서와 SaaS 분석을 결합하여 자체 속도로 현대화를 추진하는 조직에 매력적입니다. 금융 규제 기관들은 이제 안전한 클라우드 도입을 위한 청사진을 발표하며, 특히 지속적인 인텔리전스 통합을 명시함으로써 시장 모멘텀을 가속화하고 있습니다.

북미는 성숙한 클라우드 도입, 공공-민간 정보 공유 협력, 그리고 공급업체의 깊은 시장 침투로 인해 2024년 매출의 38%를 차지했습니다. 입법자들은 계속해서 공개 법률을 개선하고 있으며, 연방 기관들은 위협 인텔리전스 시장을 강화하는 실시간 데이터 교환 플랫폼을 후원하고 있습니다. 클라우드 워크로드를 겨냥한 AI 기반 악성코드는 여전히 주요 지역적 우려사항으로, 플랫폼 지출을 촉진하고 있습니다.

유럽은 NIS2(네트워크 및 정보 보안 규정 2) 시행으로 전망이 밝아지고 있습니다. 이 규정은 의무 적용 대상을 20,000개에서 300,000개 기관으로 확대하여 잠재적 위협 인텔리전스 시장을 크게 확장합니다. 사이버 복원력 법(Cyber Resilience Act)과 같은 보완 법안은 공급망 전반에 걸친 지속적인 취약점 컨텍스트 수요를 촉진합니다. 감사 준비 완료 보고서를 다국어 위협 데이터와 패키지화하는 벤더들이 유리한 입지를 점하고 있습니다.

중동은 2030년까지 15.8%의 가장 빠른 연평균 복합 성장률(CAGR)을 보일 전망입니다. UAE와 사우디아라비아의 국가 기관들은 분야별 융합 센터에 투자하는 한편, 주요 에너지 기업들은 실시간 피드 연계 사이버 보험 할인 혜택을 받고 있습니다. 지역 내 지정학적 긴장 고조로 공공 및 민간 부문 모두에게 위협 인텔리전스 시장의 전략적 가치가 상승하고 있습니다.

아시아태평양 지역은 두 자릿수 공격 증가세를 보이며, 특히 인도네시아에서 주간 사건 수가 3,300건을 넘어섰다. 급속한 디지털화와 다양한 주권 규정이 결합되어 수요가 분산되는 현상이 발생합니다. 일본, 한국, 호주는 실시간 인텔리전스를 접근 결정에 통합하는 제로 트러스트 시범 사업을 주도하는 반면, 중국과 인도의 데이터 현지화 법규는 국내 클라우드 노드 선호를 유발합니다.

남미의 채택은 기술 부족을 극복하기 위해 중견 BFSI(은행·금융·보험) 기업들이 위협 탐색을 아웃소싱하면서 촉진되었으며, 규모는 작지만 글로벌 수익에 기여하고 있습니다.

The threat intelligence market is valued at USD 9.21 billion in 2025 and is forecast to reach USD 16.90 billion by 2030, reflecting a CAGR of 12.92%.

Expanding cloud adoption, rapid attacker use of AI, and tighter regulatory frameworks such as the EU-NIS2 directive are lifting spending on proactive intelligence platforms. Security leaders are prioritizing context-rich analytics that shorten response times and lower breach costs, while insurers and investors now examine live intelligence feeds before underwriting cyber risk. Consolidation among large vendors is accelerating platform breadth, yet specialist providers remain relevant where sector-specific intelligence is required. Heightened nation-state activity and ransomware cartel funding through cryptocurrencies are expected to keep the threat environment volatile, sustaining investment momentum across every major vertical.

AI-generated polymorphic malware can rewrite its code on the fly, defeating traditional signature tools and forcing defenders to rely on behavioural analytics. IBM research shows such malware now negotiates ransoms without human contact and pivots tactics based on cloud configuration, complicating incident response. The U.S. Department of Justice recently dismantled a ring that stole USD 263 million in cryptocurrency through AI-enabled exploits, underscoring the financial risk. North American enterprises are boosting budget for machine-learning detection, making the threat intelligence market essential for cloud workload protection.

Effective October 2024, the NIS2 directive subjects roughly 300,000 European entities to mandatory risk assessments, incident reporting, and supply-chain scrutiny. Penalties can reach EUR 10 million or 2% of global turnover, pushing boards to prioritise real-time intelligence. Multinationals outside the bloc must also comply when serving EU customers, widening opportunity for vendors that package ready-to-audit intelligence feeds.

Although STIX and TAXII became OASIS standards in 2021, many legacy platforms still process proprietary formats, preventing seamless data sharing. An exploratory study identified integration complexity and inconsistent notation as primary hurdles. As a result, organisations delay platform upgrades, restraining short-term spending.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions generated 56% of global revenue in 2024, giving platforms an outsized hold on the threat intelligence market. Microsoft Defender Threat Intelligence alone processes 78 trillion signals per day, highlighting scale advantages. This dominance underlines why the threat intelligence market size attached to platforms is expected to keep rising through 2030. Leading vendors incorporate AI for behaviour analytics, easing analyst workload and improving detection fidelity.

Managed and professional services are outpacing product growth with a 14.5% CAGR, reflecting talent shortages and rising complexity. SANS surveys show many enterprises outsource hunting duties to close skill gaps. Partnerships that wrap training around deployments allow buyers to derive quicker value, propelling service uptake, especially across the threat intelligence industry's mid-market segment.

On-premise deployments held 55% of spending in 2024 as heavily regulated sectors prefer local data residency. Even so, cloud-hosted platforms are the fastest riser at 16.8% CAGR, signalling confidence in provider hardening and FedRAMP expansions such as Microsoft Defender Threat Intelligence gaining High attestation. Segment observers see the threat intelligence market size for cloud deliveries eclipsing on-premise totals late in the forecast window.

Hybrid approaches blend legacy sensors with SaaS analytics, appealing to organisations modernising at their own pace. Financial regulators now publish blueprints for secure cloud adoption that specifically mention continuous intelligence integration, accelerating momentum.

The Threat Intelligence Market Report is Segmented by Component (Solutions, and Services), Deployment (On-Premise, Cloud, and Hybrid), Threat-Intelligence Type (Strategic, Tactical, Operational, and Technical), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, IT and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 38% of 2024 revenue owing to mature cloud uptake, joint public-private information sharing, and deep vendor presence. Legislators continue to refine disclosure laws, while federal bodies sponsor real-time data-exchange platforms that reinforce the threat intelligence market. AI-enabled malware against cloud workloads remains the top regional concern, keeping platform spending buoyant.

Europe's outlook brightens under NIS2, which scales mandatory coverage from 20 000 to 300 000 entities, greatly enlarging the addressable threat intelligence market. Complementary legislation such as the Cyber Resilience Act furthers demand for continuous vulnerability context across supply chains. Vendors that package audit-ready reporting with multi-lingual threat data are well positioned.

The Middle East shows the fastest CAGR at 15.8% through 2030. National agencies in the UAE and Saudi Arabia invest in sector-focused fusion centres while energy majors receive cyber-insurance discounts tied to live feeds. Rising geopolitical tension in the region elevates the strategic value of the threat intelligence market for both public and private sectors.

Asia-Pacific sees a double-digit attack uptick, notably in Indonesia where weekly incidents top 3,300. Rapid digitalisation, paired with diverse sovereignty rules, produces fragmented demand. Japan, South Korea, and Australia lead Zero Trust pilots that embed live intelligence into access decisions, while China and India's data-localisation laws create preferences for in-country cloud nodes.

South America's adoption is spurred by mid-tier BFSI outsourcing threat-hunting to overcome skills shortages, adding to global revenue even if from a smaller base.