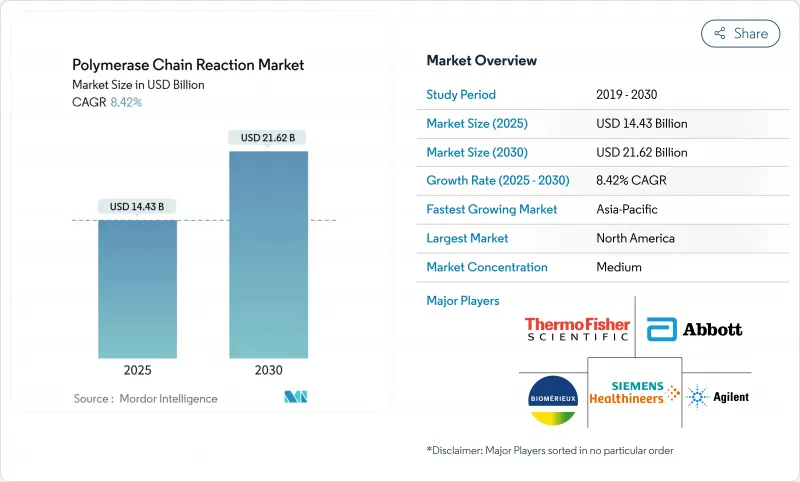

중합효소 연쇄반응(PCR) 시장 규모는 2025년에 144억 3,000만 달러로 평가되었고 예측 기간 중(2025-2030년) CAGR은 8.42%를 나타낼 것으로 예측되며 2030년에는 216억 2,000만 달러에 달할 전망입니다.

정밀진단으로의 전환이 성장을 주도하고 있습니다. 디지털 시스템과 AI 강화 플랫폼은 기존 증폭 장비 대비 단위 판매량은 적으나 프리미엄 가격을 형성합니다. 순환종양DNA 검사는 디지털 PCR만이 구현 가능한 절대적 정량화에 의존하기 때문에 액체생검 도입이 가속화되고 있습니다. 경쟁 강도는 대량·저마진 검사와 프리미엄 종양학 응용 분야 간의 분화로 형성되며, 일회용 플라스틱에 대한 지속가능성 우려로 공급업체들은 소모품 재설계를 추진하고 있습니다. PCR 시장은 아시아태평양 지역의 규제 조화와 북미의 병원 통합으로 혜택을 보는데, 이 두 요인 모두 간소화된 실험실 워크플로우에 부합하는 자동화 멀티플렉스 시스템을 장려합니다.

병원들은 이제 암 바이오마커 감지 및 신생아 유전자 검사를 위해 PCR을 일상적인 병리 서비스에 통합하고 있습니다. 로슈는 2024년 검사당 비용을 절감하면서 실험실 효율성을 높이는 고처리량 패널 지원을 위해 100대의 cobas 5800 시스템을 배치했습니다. SARS-CoV-2, 인플루엔자 A/B, RSV를 동시에 감지하는 cobas Liat 검사에 대한 FDA 긴급사용승인은 현장진료(POCT) 환경에서 증후군 기반 검사가 확산되고 있음을 보여줍니다. 디지털 PCR은 qPCR로는 감지 불가능한 초저농도 종양 부하 수준을 탐지함으로써 혈액암의 최소 잔류병 모니터링을 한층 발전시킵니다. 통합된 실험실 네트워크는 최소한의 조작자 개입으로 다양한 검사를 처리할 수 있는 플랫폼을 요구하며, 이는 PCR 시장의 꾸준한 성장에 기여합니다.

동반진단(CDx)은 연구 환경에서 일상적인 종양학 진료로 이동하며, 약물 개발자들이 바이오마커로 정의된 환자 하위 그룹에 치료법을 매칭하는 검사를 추구함에 따라 PCR 시장을 확장하고 있습니다. 유럽 액체 생검 학회(ELBS)는 2024년 93개 기관에 걸쳐 순환 종양 DNA 워크플로우를 표준화하여 디지털 PCR의 광범위한 채택을 위한 길을 열었습니다. QIAGEN은 QIAcuity 플랫폼용 검증된 100개 이상의 분석법을 출시하며 일반 시약에서 질환 특이적 패널로의 전환을 입증했습니다. Bio-Rad는 Oncocyte와 협력하여 액적 디지털 PCR 기반 이식 모니터링 검사를 제공함으로써 해당 기술을 종양학 분야를 넘어 확장했습니다.

신흥 경제국의 자본 예산은 고급 분자 플랫폼을 거의 포함하지 않습니다. 비용 효율성 모델에 따르면, 종양학 바이오마커에 대한 환자당 PCR 검사 비용은 18,246달러로, 차세대 시퀀싱(8,866달러)보다 훨씬 높게 나타나 경제적 어려움을 부각시켰습니다. QIAGEN의 NeuMoDx 시스템 철수는 팬데믹 수요 감소 후 고비용 하드웨어 유지의 어려움을 보여줍니다. 임대 프로그램이 비용 분산을 돕지만, 유지보수 계약은 여전히 소규모 실험실의 진입 장벽입니다. 효모 유래 중합효소를 연구 중인 개발사들은 시약 비용을 절감할 수 있으나, 장비 상각 비용이 여전히 더 큰 장벽으로 남아 있습니다.

2024년 PCR 시장 점유율에서 시약 및 소모품 부문은 48.94%를 차지했으며, 이는 실험실이 매주 재주문하는 효소 및 마스터 믹스에 대한 장비 독립적 수요를 반영합니다. 디지털 PCR 시스템은 13.78%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상되며, 동반진단에 필수적인 절대 정량화를 제공하는 제품으로서 PCR 시장 규모 내 점유율을 높일 전망입니다. 기존 열순환기는 상품화 압박에 직면하여, 업체들은 마진 보호를 위해 번들 소프트웨어, 자동화 모듈, 포괄적 서비스 계약으로 차별화를 꾀하고 있습니다. 고처리량 통합 플랫폼은 인건비 절감과 표준화된 품질 관리를 추구하는 통합 실험실에 매력적입니다.

휴대용 및 현장진단(POCT) 기기는 소형화와 저전력 소비가 구급차 및 농촌 진료소 같은 새로운 환경을 가능케 하는 최전선을 대표합니다. 한국의 Lab On An Array 장치는 MEMS 칩이 분석 감도를 유지하면서 에너지 소모를 줄이는 방식을 보여줍니다. AI가 오프타겟 증폭을 제한하는 프라이머 설계를 제안함에 따라 소프트웨어 및 클라우드 분석의 중요성이 커지고 있습니다. QIAGEN은 자사의 생물정보학 부문이 2027년까지 매출 1억 달러를 돌파할 것으로 예상하며, 데이터 관리가 이제 하드웨어와 맞먹는 가치 창출이 가능함을 강조합니다.

북미는 2024년 PCR 시장 점유율 36.85%를 유지했으며, 이는 자금력이 풍부한 의료 시스템과 밀집된 제약 산업에 힘입은 결과입니다. 병원 체인들은 통합된 검사 부하를 처리하기 위해 고처리량 자동화를 선호하며, 연방 연구소들은 PCR 시장을 역동적으로 유지하는 생물안전 패널에 투자하고 있습니다. 이 지역의 명확한 규제 환경은 더 빠른 실행 시간과 다중 감지 기능을 제공하는 차세대 플랫폼 출시를 촉진합니다.

아시아태평양 지역은 2030년까지 연평균 13.23%의 성장률을 기록하며 PCR 시장 확장의 핵심 동력이 될 전망입니다. 각국 정부는 보편적 건강보험 제도를 시행하며 유전체학 분야에 사상 최대 규모의 예산을 배정하고 있습니다. 중국의 ‘건강중국 2030’ 계획은 수입 의존도를 낮추는 국내 제조업에 자본을 집중시켜 글로벌 브랜드와 어깨를 나란히 하는 현지 경쟁사를 창출하고 있습니다. 인도의 생산 연계 인센티브 제도는 진단 기기 생산에 세액 공제를 부여하여 지역 PCR 역량을 직접 강화합니다.

유럽은 강력한 학술 네트워크와 범지역 데이터 이니셔티브의 혜택을 누리고 있습니다. 곧 시행될 유럽 건강 데이터 공간 규정은 전자 건강 기록을 통합하여 PCR 기반 종결점을 활용하는 다국적 임상 연구를 용이하게 할 것입니다. 일부 회원국의 긴축 예산으로 자본 지출이 제한되지만, 주요 종양학 센터의 액체 생검 검사 수요가 수익을 유지하고 있습니다. 중동 및 아프리카 및 남미는 아직 초기 단계이지만, 특히 의료 관광 및 농업 검사를 위한 민간 실험실을 중심으로 인프라 투자가 증가하며 글로벌 PCR 시장에서의 역할을 점차 확대하고 있습니다.

The Polymerase Chain Reaction Market size is estimated at USD 14.43 billion in 2025, and is expected to reach USD 21.62 billion by 2030, at a CAGR of 8.42% during the forecast period (2025-2030).

Growth arises from the shift toward precision diagnostics, where digital systems and AI-enhanced platforms command premium prices despite lower unit volumes compared with traditional amplification instruments. Liquid biopsy adoption accelerates because circulating tumor DNA testing relies on absolute quantification that only digital PCR can deliver. Competitive intensity is shaped by the bifurcation between high-volume, low-margin testing and premium oncology applications, while sustainability concerns over single-use plastics push vendors to redesign consumables. The PCR market benefits from regulatory harmonization in Asia-Pacific and hospital consolidation in North America, both of which incentivize automated, multiplex systems that fit into streamlined laboratory workflows.

Hospitals now integrate PCR into routine pathology services for cancer biomarker detection and newborn genetic screening. Roche deployed 100 cobas 5800 systems in 2024 to support high-throughput panels that cut per-test costs while boosting laboratory efficiency. FDA Emergency Use Authorization for the cobas Liat assay that simultaneously detects SARS-CoV-2, Influenza A/B, and RSV shows syndromic testing gaining traction in point-of-care settings. Digital PCR further advances minimal residual disease monitoring in hematologic cancers by detecting ultra-low tumor burden levels not reachable by qPCR. Consolidated laboratory networks demand platforms that handle diverse menus with minimal operator intervention, contributing to steady PCR market growth.

Companion diagnostics have moved from research settings into routine oncology practice, expanding the PCR market as drug developers seek assays that match therapies to biomarker-defined patient subgroups. The European Liquid Biopsy Society standardized circulating tumor DNA workflows across 93 institutions in 2024, paving the way for broader digital PCR adoption. QIAGEN released more than 100 validated assays for its QIAcuity platform, demonstrating the shift from generic reagents toward disease-specific panels. Bio-Rad partnered with Oncocyte to deliver transplant monitoring tests based on droplet digital PCR, pushing the technology beyond oncology.

Capital budgets in emerging economies seldom cover high-end molecular platforms. A cost-effectiveness model put per-patient PCR testing for oncology biomarkers at USD 18,246 versus USD 8,866 for next-generation sequencing, underscoring economic challenges. QIAGEN's withdrawal of its NeuMoDx system shows the difficulty of sustaining costly hardware once pandemic volumes recede. Leasing programs help spread expenses, yet maintenance contracts still deter smaller labs. Developers exploring yeast-derived polymerases may cut reagent costs, though instrument amortization remains the bigger hurdle.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Reagents & Consumables held 48.94% of PCR market share in 2024, reflecting the instrument-agnostic demand for enzymes and master mixes that laboratories reorder each week. Digital PCR Systems are forecast to grow at a 13.78% CAGR, lifting their portion of the PCR market size for products that deliver absolute quantification essential for companion diagnostics. Traditional thermal cyclers face commoditization; vendors therefore differentiate through bundled software, automation modules, and inclusive service contracts to protect margins. High-throughput integrated platforms appeal to consolidated laboratories that seek lower labor costs and standardized quality control.

Portable and point-of-care devices represent the frontier where miniaturization and low power consumption unlock new settings such as ambulances and rural clinics. The South Korean Lab On An Array unit shows how MEMS chips trim energy draw while keeping analytical sensitivity. Software and cloud analytics grow in importance as AI suggests primer designs that limit off-target amplification. QIAGEN expects its bioinformatics arm to cross USD 100 million in revenue by 2027, underscoring that data management can now rival hardware in value creation.

The Polymerase Chain Reaction Market Report Segments the Industry Into by Product (Instruments, Reagents and Consumables, Software and Services), Application (Clinical Diagnostics, Drug Discovery and Development, and More), End User (Hospitals and Diagnostic Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 36.85% of PCR market share in 2024, supported by well-funded healthcare systems and a dense pharmaceutical industry. Hospital chains favor high-throughput automation to meet consolidated testing loads, and federal laboratories invest in biosecurity panels that keep the PCR market dynamic. The region's regulatory clarity encourages next-generation platform launches that offer faster run times and multiplex abilities.

Asia-Pacific is set to grow at a 13.23% CAGR through 2030, becoming the engine of PCR market expansion. Governments allocate record budgets for genomics as they roll out universal health coverage. China's Healthy China 2030 initiative channels capital toward domestic manufacturing that reduces import reliance, creating local competitors alongside global brands. India's Production Linked Incentive scheme grants tax credits for diagnostic device production, directly bolstering regional PCR capability.

Europe benefits from strong academic networks and pan-regional data initiatives. The forthcoming European Health Data Space regulation will unify electronic health records, easing multi-country clinical research that relies on PCR-based endpoints. Although austerity budgets in some member states restrict capital spending, demand for liquid biopsy assays in major oncology centers sustains revenue. Middle East & Africa and South America remain nascent but show rising infrastructure investment, particularly in private labs that cater to medical tourism and agriculture testing, gradually enlarging their role in the global PCR market.