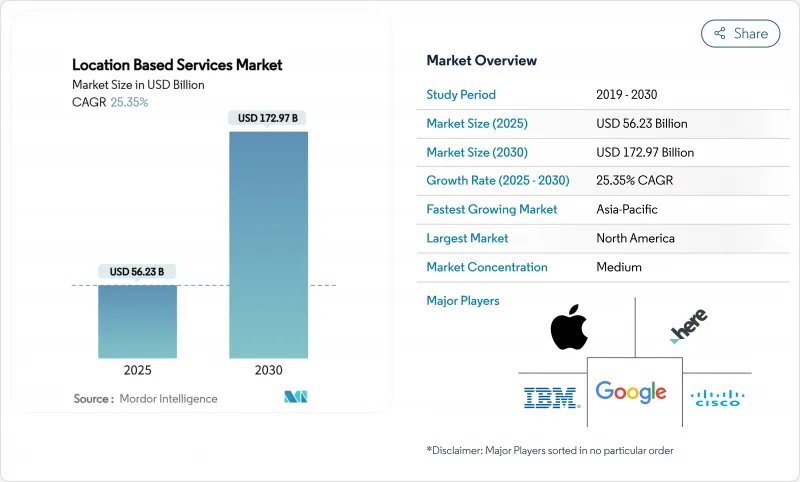

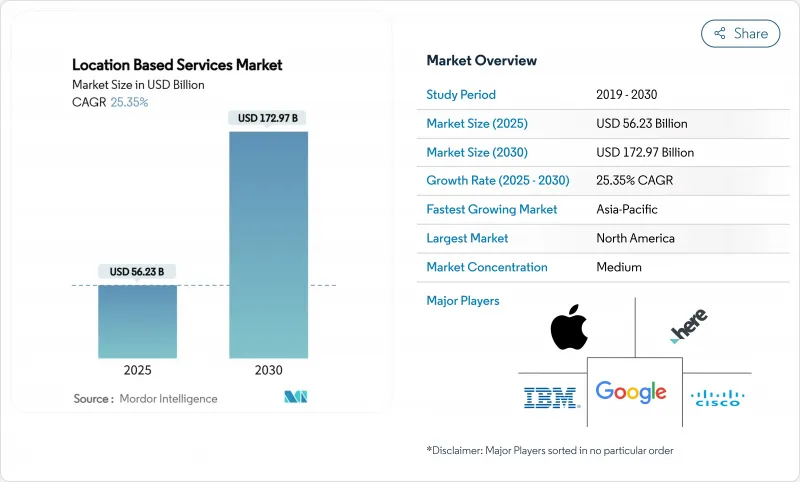

위치기반서비스 시장 규모는 2025년 562억 3,000만 달러로 추정되고, CAGR 25.35%로 성장할 전망이며, 2030년에는 1,729억 7,000만 달러에 이를 것으로 예측됩니다.

이 호조 궤도는 서브미터의 정밀도를 보장하는 5G 네트워크 슬라이싱의 전개, 고도의 모바일 위치 정보를 강제하는 긴급 통보 규제의 의무화, 실시간 위치 기반 시스템에 의존하는 디지털 트윈 물류 허브의 대두 등에 기인합니다. 초로컬 광고 예산 확장, 센티미터급 위성 증강, AI 주도 실내 위치 추적 등 대응 가능한 이용 사례가 모두 확대되어 기업은 마케팅, 안전, 산업 자동화 워크플로우 전체에 위치 정보 인텔리전스를 통합하도록 촉구하고 있습니다. 따라서 시장 진출 기업은 GPS, UWB, BLE, Wi-Fi FTM, 센서 퓨전을 융합하여 실내외를 원활하게 커버하는 멀티 모달 포지셔닝 엔진에 주목하고 있습니다. 합병, 고가치 파트너십, 컴플라이언스 지출은 통합을 촉진하는 반면, 프라이버시 규정은 명시적 동의의 참여를 위한 상업 모델을 형성하고 있습니다.

마케팅 담당자는 2024년 46%에서 2025년에는 20% 이상의 예산을 지역 캠페인에 할당할 계획입니다. Google 지도는 이미 광고 출고를 통해 연간 111억 달러를 수익화하고 있습니다. 위치 정보를 트리거로 푸시 알림을 채택한 소매업체는 매장 내 전환이 급증한 것으로 보고되었으며 수익 확대 가설이 입증되었습니다. 위치 정보의 입도가 높아지면 동적 광고 소재를 최적화할 수 있으며 브랜드는 미시적 시장에 맞는 메시지를 전달할 가능성이 있습니다. 결과적으로 위치 서비스 시장은 광고 기술 플랫폼, 게시자 및 온라인상의 의사를 오프라인 구매 경로에 연결하려는 브랜드에서 지속적인 수요를 얻고 있습니다.

유럽의 전자통신규약은 모든 스마트폰에 AML을 탑재하고 긴급사태의 87%에 대해 50m 이내의 발신자 좌표를 제공할 것을 의무화하고 있습니다. 영국의 경험은 Cell-ID에 비해 정확도가 4,000배 향상되고 응답 시간이 단축되고 10년 동안 7,500명의 생명이 구출될 수 있습니다. 30개국 이상이 AML을 채택하고 미국은 E-911의 수직 정밀도 규칙을 강화하고 있습니다. 따라서 통신사는 포지셔닝 코어를 업그레이드하고 API를 핸드오프해야 하며 하이브리드 GNSS, Wi-Fi, 센서 지원 솔루션에 대한 지출을 촉진하고 있습니다. 통신 사업자가 고급 위치 미들웨어를 네트워크 코어 및 최종 사용자 앱에 통합하기 때문에 규정 준수 예산은 위치 서비스 시장을 직접 확장합니다.

조사에 따르면 사용자의 71%는 명확한 동의를 얻은 경우에만 위치 정보를 공유합니다. GDPR(EU 개인정보보호규정)은 데이터 최소화를 의무화하고 CCPA는 옵트아웃 메커니즘을 부과하고 항상 추적 범위를 최대 30%까지 줄입니다. 인도의 DPDP 법에서는 추가 동의 계층이 도입되어 공급자는 엔지니어링 비용을 추가하는 차동 프라이버시 및 페더레이티드 러닝 모델에 대한 투자를 강요합니다. 이러한 이동은 데이터 수집 속도를 낮추고 위치 서비스 시장에서 특정 광고 수익원을 억제합니다.

기업이 설계, 전개, 지원을 매니지드 서비스 전문가에게 위탁하고 있기 때문에 2024년 매출의 47.5%를 서비스가 차지했습니다. 그러나 소프트웨어는 CAGR 26.8%로 성장할 것으로 예측되며, AI 분석이 원시 핑을 비즈니스 액션으로 변환하는 방법을 강조합니다. 디지털 트윈 커맨드 센터를 통합하는 대규모 3PL은 턴키 스위트가 프리미엄 계약을 이끌어내는 이유를 보여줍니다. 반면 하드웨어는 UWB 앵커와 BLE 게이트웨이가 헬스케어 캠퍼스에서 널리 보급되어 긍정적인 성장을 유지하고 있습니다.

Mapbox의 MapGPT와 TomTom의 Azure 통합을 통해 자동차 제조업체는 차량 탑재 장치를 새로 고치지 않고 무선 업그레이드를 추진할 수 있기 때문에 소프트웨어 구독의 위치기반서비스 시장 규모가 꾸준히 확대되고 있습니다. 서비스 통합자는 하드웨어, 클라우드 대시보드 및 애널리틱스를 번들하여 고객의 총 소유 비용을 낮추고 경상 수익 가시성을 강화합니다.

성숙한 GNSS 생태계로 인해 옥외 포지셔닝은 여전히 우세하지만 실내 배치는 빠르게 확대되고 있습니다. 옥외 위치기반서비스 시장 점유율은 2024년에 68.6%에 달했는데, 실내에서는 2030년까지 CAGR 28.6%로 성장할 전망이며, 향후 수습해 나갈 것으로 예측됩니다. 병원, 쇼핑몰, 공항에서는 BLE 태그와 UWB 태그를 도입하여 자산 검색 사이클을 단축하고 방문자를 유도하고 있습니다.

하이브리드 솔루션은 GPS, 5G, Wi-Fi, 블루투스 간을 완벽하게 핸드오프하고 사용자 경험을 유지합니다. 표준화 컨소시엄은 정확도의 벤치마크를 지속적으로 연마하고, 교정 비용을 절감하며, 잠재 수요를 발굴하고, 위치기반서비스 시장 전체를 확대합니다.

북미는 AML 대응 스마트폰의 보급과 견고한 클라우드 인프라를 배경으로 2024년에 36.8%로 최대의 슬라이스를 창출했습니다. HERE Technologies의 10억 달러 AWS 제휴와 같은 고액 계약은 이 지역의 규모를 이야기하고 있습니다. 연방 정부 E-911의 기한은 운영자의 지속적인 투자를 보장하고 자동차 OEM은 레벨 3 자율성을 실현하기 위해 차선 수준의 HD 맵을 시도합니다.

아시아태평양은 CAGR 25.8%에서 가장 급성장하고 있으며, 독특한 모바일 가입자는 2030년까지 21억명에 달할 전망이며, GDP에 8,800억 달러 공헌할 전망입니다. 중국, 한국, 일본의 5G 단독 전개는 네트워크 기반 포지셔닝 API를 촉진하고, GAGAN과 같은 SBAS 성상도는 정밀 농업을 위한 GNSS를 보완합니다. 각국 정부는 혁신과 프라이버시의 균형을 맞추는 데이터 거버넌스의 틀을 지지하고, 국내 생태계 형성을 촉진하며, 지역 전체의 위치 기반 서비스 시장 규모를 확대하고 있습니다.

유럽은 소비자의 신뢰를 키우는 엄격한 프라이버시 지도를 통해 꾸준한 기세를 유지하고 있습니다. AML은 2022년 이후 모든 스마트폰에 의무가 있으며, 통신 사업자 및 PSAP의 백엔드 업그레이드를 촉진하고 있습니다. 프라이버시에 중점을 둔 신흥 기업의 부상은 GDPR(EU 개인정보보호규정)을 충족시키기 위해 차동 프라이버시를 채택하여 서비스의 다양성을 풍부하게 하고 있습니다. 남미와 중동, 아프리카는 아직 발전 도상이지만 유망합니다. 브라질은 항공용 SBAS를 채택하고 걸프의 스마트 시티 프로그램은 메가몰에 BLE m-commerce 비콘을 전개합니다. 아프리카 항공기관은 SatNav-Africa SBAS와 협력하여 미래 정밀 농업 및 운송 서비스를 위한 기초 인프라를 구축하고 있습니다. 이러한 노력이 일체가 되어, 위치기반서비스 시장의 지리적 풋 프린트를 넓히고 있습니다.

The location-based services market size equals USD 56.23 billion in 2025 and is forecast to advance at a 25.35% CAGR, reaching USD 172.97 billion by 2030.

This brisk trajectory stems from 5G network-slicing deployments that guarantee sub-meter accuracy, mandatory emergency-call regulations that enforce Advanced Mobile Location, and the rise of digital-twin logistics hubs that depend on real-time location systems. Intensifying hyper-local advertising budgets, centimeter-grade satellite augmentation, and AI-driven indoor positioning all expand addressable use cases, prompting enterprises to embed location intelligence across marketing, safety, and industrial automation workflows. Market participants therefore focus on multi-modal positioning engines that blend GPS, UWB, BLE, Wi-Fi FTM, and sensor fusion to deliver seamless indoor-outdoor coverage. Mergers, high-value partnerships, and compliance spending drive consolidation, while privacy regulation shapes commercial models toward explicit-consent engagement.

Marketers plan to allocate 20%-plus of budgets to local campaigns in 2025, up from 46% in 2024, as geofencing proves effective for foot-traffic uplift. Google Maps already monetizes USD 11.1 billion annually through ad placements. Retailers adopting location-triggered push notifications report sharp increases in in-store conversions, validating the revenue-expansion thesis. Greater location granularity also supports dynamic creative optimization, letting brands tailor messages to micro-markets. As a result, the location-based services market gains sustained demand from advertising technology platforms, publishers, and brands eager to link online intent with offline purchase paths.

The European Electronic Communications Code requires AML on all smartphones, delivering caller coordinates within 50 m for 87% of emergencies . The UK experience shows a 4,000-fold accuracy boost versus Cell-ID, cutting response times and potentially saving 7,500 lives over 10 years. More than 30 nations have adopted AML, while the US is tightening E-911 vertical-accuracy rules. Telcos must therefore upgrade positioning cores and hand-off APIs, fueling spending on hybrid GNSS, Wi-Fi, and sensor-assisted solutions. Compliance budgets directly expand the location-based services market as operators embed advanced location middleware within network cores and end-user apps.

Surveys show 71% of users will only share location after explicit consent. GDPR mandates data-minimization, while CCPA imposes opt-out mechanics, reducing always-on tracking coverage by up to 30%. India's DPDP Act introduces extra consent layers, compelling providers to invest in differential-privacy and federated-learning models that add engineering cost. These shifts slow data-collection velocity, tempering certain advertising revenue streams inside the location-based services market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Services represented 47.5% of 2024 revenue as enterprises outsourced design, deployment, and support to managed-service experts. Software, however, is forecast to log a 26.8% CAGR, underscoring how AI analytics convert raw pings into business actions. Large 3PLs integrating digital-twin command centers illustrate why turnkey suites attract premium subscriptions. Meanwhile, hardware growth stays positive as UWB anchors and BLE gateways proliferate in healthcare campuses.

The location-based services market size for software subscriptions climbs steadily as Mapbox's MapGPT and TomTom's Azure integrations let automakers push over-the-air upgrades without refreshing on-board units. Service integrators bundle hardware, cloud dashboards, and analytics, ensuring lower total cost of ownership for clients and reinforcing recurring-revenue visibility.

Outdoor positioning still dominates owing to mature GNSS ecosystems, yet indoor deployments are scaling fast. The location-based services market share for outdoor stood at 68.6% in 2024; indoor positioning is tracking a 28.6% CAGR through 2030, suggesting convergence down the line. Hospitals, malls, and airports deploy BLE and UWB tags to cut asset-search cycles and guide visitors, inching the indoor slice toward parity with outdoor during the forecast horizon.

Hybrid solutions hand-off seamlessly between GPS, 5G, Wi-Fi, and Bluetooth, preserving user experience. Standardisation consortia continue refining accuracy benchmarks, which should trim calibration costs and unlock pent-up demand, expanding the overall location-based services market.

The Location Based Services Market Report is Segmented by Component (Hardware, Software, Services), Location Type (Indoor, Outdoor), Core Technology (GPS/A-GPS, Wi-Fi and WLAN Triangulation, and More), Application (Navigation and Mapping, and More), End-User Industry (Retail and FMCG, Transportation and Logistics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated the largest slice at 36.8% in 2024 on the back of AML-ready smartphone penetration and robust cloud infrastructure. High-value contracts such as HERE Technologies' USD 1 billion AWS alliance illustrate the region's scale. Federal E-911 deadlines ensure continuous operator investment, while automotive OEMs trial lane-level HD maps for Level-3 autonomy.

Asia-Pacific is the fastest-growing at 25.8% CAGR, with unique mobile subscribers on track to hit 2.1 billion by 2030 and contribute USD 880 billion to GDP . Standalone 5G rollouts in China, Korea, and Japan foster network-based positioning APIs; SBAS constellations such as GAGAN complement GNSS for precision farming. Governments champion data-governance frameworks that balance innovation with privacy, encouraging domestic ecosystem formation and enlarging the location-based services market size across the region.

Europe maintains steady momentum through stringent privacy leadership that nurtures consumer trust. AML has been mandatory on all smartphones since 2022, catalyzing backend upgrades among carriers and PSAPs. An emerging crop of privacy-focused startups employs differential-privacy to meet GDPR, enriching service diversity. Southern and Eastern European cities trial U-Space corridors requiring reliable drone positioning, adding a new adjacency.South America and Middle East and Africa remain nascent but promising. Brazil adopts SBAS for aviation, while Gulf smart-city programs deploy BLE m-commerce beacons in mega-malls. African regional aviation bodies collaborate on SatNav-Africa SBAS, sowing foundational infrastructure for future precision-agriculture and transport services. Collectively these initiatives broaden the geographic footprint of the location-based services market.