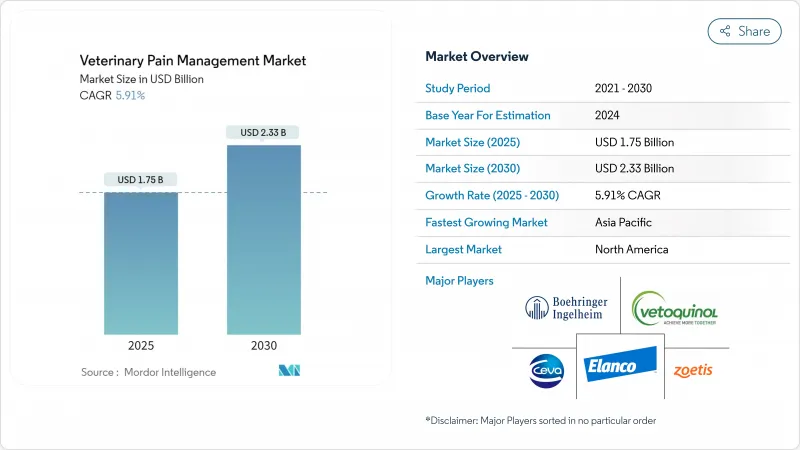

동물 통증 관리 시장 규모는 2025년에 17억 5,000만 달러로 평가되었고 2030년에는 23억 3,000만 달러에 이를 것으로 예측되며, CAGR은 5.91%를 나타낼 전망입니다.

반려동물 인간화 추세 확대, 가축 복지 규정 강화, 지속적인 신제품 출시가 이러한 성장세를 뒷받침하고 있습니다. 약물 기반 치료법이 여전히 가치 창출에서 우위를 점하고 있으나, 부작용에 대한 감시가 수의사들을 비약물적 치료법으로 이끌면서 기기 치료법이 보조적 역할에서 주류로 빠르게 자리 잡고 있습니다. 단일클론 항체, 인공지능 기반 통증 평가 플랫폼, 카나비노이드 후보물질 등은 기존 비스테로이드성 항염증제(NSAIDs)와 오피오이드를 넘어 확장되는 파이프라인을 보여줍니다. 동시에 미국과 유럽연합(EU)의 의무적 다중 모드 진통 프로토콜은 오피오이드 노출을 줄이면서도 효과를 유지하는 복합 요법에 대한 수요를 촉진하고 있습니다.

반려동물 소유자들은 점차 인간 수준의 임상 기준을 기대하며, 조에티스의 베딘베타맙 주사제와 같은 혁신적 제품의 프리미엄 채택을 촉진하고 있습니다. 미국동물병원협회(AAHA)의 2024년 지침은 다중 모드 요법을 공식화하여 항체 사용을 NSAIDs와 병용하는 것을 정당화합니다. 복지 인증 가축 제품 유통업체들도 가격 프리미엄을 정당화하기 위해 신뢰할 수 있는 진통 효과를 주장하며, 이는 전반적인 수요를 확대합니다.

골관절염은 1세 이상 개들의 20%, 12세 이상 고양이의 거의 90%에게 영향을 미칩니다. 베딘베트마브(bedinvetmab)의 FDA 승인으로 생물학적 제제가 장기적 해결책으로 자리 잡았으며, 임상시험 성공률은 위약군 16.9% 대비 43.5%를 기록했습니다. 엘란코(Elanco)의 노시타(Nocita)와 같은 장시간 작용 부피바카인 제제는 72시간 지속 효과를 제공하여 재입원률과 소유주 부담을 줄입니다. 치료받지 않은 가축의 생산성 손실은 효과적인 진통제의 경제적 필요성을 더욱 부각시킵니다.

수의사들은 NSAIDs 처방 시 신장, 간, 위장관 위험을 고려하며, 오피오이드 조제 시 불법 유통 우려가 복잡성을 더합니다. 베딘베트맙의 시판 후 감시 결과 1,800만 회 투여에서 1만 7,162건의 부작용 보고가 기록되어, 혁신적인 생물학적 제제조차 안전성 의무를 동반함을 임상의들에게 상기시켰습니다. 수제트리진의 인간용 FDA 승인은 수의학 분야로 확장될 수 있는 비오피오이드 계열 약물의 추진력을 강조합니다.

2024년 동물 통증 관리 시장 규모에서 제약 부문은 멜록시캄과 같은 비스테로이드성 항염증제(NSAIDs)를 중심으로 81.42%를 차지했으나, 기기 매출은 연평균 6.14% 성장률을 보이고 있습니다. 비용 효율성으로 인해 NSAIDs는 1차 치료제로 지속되는 반면, 오피오이드 사용은 전용 목적 외 사용 감시 강화로 감소 추세입니다. 노시타(Nocita)와 같은 장기 작용 국소 마취제는 진통 효과를 72시간까지 연장하고 재입원을 줄입니다. 알파-2 작용제는 대형 동물 진정 분야에서 틈새 역할을 유지합니다. 초기 진입한 카나비노이드는 규제적 역풍에도 불구하고 기존 치료군이 효과적이지 않은 만성 통증에 대응합니다.

휴대용 다이오드 레이저 장치, PEMF 매트, 충격파 시스템은 단독 또는 보조 솔루션으로 입지를 다지고 있습니다. 동물병원은 NSAIDs 내성이 있는 노령 반려동물에게 이러한 기술을 권장하며, 말 전문 수의사는 근골격계 회복을 위해 PEMF를 활용합니다. 제조사들은 이제 세션 매개변수를 기록하는 소프트웨어 분석 기능을 번들로 제공하여 수의사들이 다중 모드 치료 지침 준수를 문서화할 수 있게 합니다. 이러한 기기 발전 추세는 동물 통증 관리 시장이 약물 치료와 비약물적 치료법 간의 균형을 점차적으로 맞추어 갈 것임을 시사합니다.

북미는 2024년 글로벌 매출의 42.23%를 차지했으며, 이는 높은 반려동물 보험 보급률과 신속한 시장 출시 승인을 가능케 하는 규제 환경에 힘입은 결과입니다. 단일클론 항체 선구 기업들은 FDA 심사 효율성을 활용하여 초기 브랜드 인지도를 확보했습니다. 그러나 캐나다의 규제 약물에 대한 신중한 입장은 비오피오이드 약물 및 카나비노이드 연구 파이프라인에 대한 투자를 촉진했습니다.

유럽은 세계에서 가장 엄격한 복지 법규의 영향을 받아 근소한 차이로 뒤를 이었습니다. 의무화된 복합 진통법은 다양한 제품 키트 수요를 증가시켜 공급업체들이 더 광범위한 처방 목록을 보유하도록 유도했습니다. 항생제 관리 프로그램은 비스테로이드성 항염증제(NSAID) 사용을 제한하여 간접적으로 레이저 및 전자기 치료 기기 채택을 촉진했습니다. 영국의 브렉시트 이후 규제 자율성은 틈새 제품에 대한 신속한 승인 경로를 허용하여 범유럽 승인 전에 중소기업의 진입 기회를 제공하고 있습니다.

아시아태평양 지역은 연평균 7.35% 성장률로 가장 빠르게 확장 중입니다. 중국에서는 팬데믹 이후 생활 방식 변화로 도시 반려동물 소유율이 급증했으며, 일본의 고령 반려동물 인구는 서구 시장과 유사한 양상을 보입니다. 한국의 동물보호법 개정은 미용 수술 및 질병 치료 시 통증 완화를 의무화하여 새로운 기본 수요를 창출하고 있습니다. 신흥 동남아시아 경제권은 수출 인증 기준에 부합하기 위해 복지 기준을 상향 조정하며, 이는 글로벌 브랜드에게 접근 가능한 시장 규모로 이어지고 있습니다.

The veterinary pain management market size stood at USD 1.75 billion in 2025 and is forecast to climb to USD 2.33 billion by 2030, advancing at a 5.91% CAGR.

Growing pet humanization, tightening livestock welfare rules, and sustained product launches underpin this trajectory. Drug-based modalities still dominate value contribution, but device therapies are moving rapidly from adjunct to mainstream status as adverse-event scrutiny pushes veterinarians toward non-pharmaceutical tools. Monoclonal antibodies, AI-enabled pain-scoring platforms, and cannabinoid candidates illustrate a pipeline that is broadening beyond legacy NSAIDs and opioids. Simultaneously, mandatory multimodal analgesia protocols in the United States and the European Union are fostering demand for combination regimens that lower opioid exposure while sustaining efficacy.

Pet owners increasingly expect human-level clinical standards, prompting premium adoption of innovations such as Zoetis' bedinvetmab injections. The American Animal Hospital Association's 2024 guidelines codify multimodal regimens, legitimizing antibody use alongside NSAIDs. Retailers of welfare-certified livestock products likewise seek credible analgesia claims to justify price premiums, widening overall demand.

Osteoarthritis affects 20% of dogs older than one year and nearly 90% of cats above 12 years. FDA approval of bedinvetmab established biologics as viable long-term solutions, with trial success rates of 43.5% versus 16.9% for placebo. Long-acting bupivacaine formulations such as Elanco's Nocita deliver 72-hour coverage, curbing readmission rates and owner burden. Productivity losses in untreated livestock further amplify the economic argument for effective analgesia.

Veterinarians weigh renal, hepatic, and gastrointestinal risks when prescribing NSAIDs, and diversion concerns complicate opioid dispensing. Post-marketing surveillance of bedinvetmab documented 17,162 adverse reports from 18 million doses, reminding clinicians that even innovative biologics carry safety obligations. FDA approval of suzetrigine for human use underscores momentum toward non-opioid classes that may cross into veterinary care.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The pharmaceutical segment captured 81.42% of the veterinary pain management market size in 2024, anchored by NSAIDs such as meloxicam, yet device revenues are growing at a 6.14% CAGR. NSAIDs persist as first-line therapy because of cost efficiency, whereas opioid use retreats under diversion scrutiny. Long-acting local anesthetics like Nocita extend analgesia to 72 hours and mitigate readmission. Alpha-2 agonists retain niche roles in large animal sedation. Early cannabinoid entrants address chronic pain that resists conventional classes, despite regulatory headwinds.

Portable diode-laser units, PEMF mats, and shockwave systems are carving out space as stand-alone or adjunct solutions. Clinics promote these technologies for geriatric pets intolerant of NSAIDs, while equine practitioners leverage PEMF for musculoskeletal recovery. Manufacturers now bundle software analytics that log session parameters, enabling veterinarians to document compliance with multimodal mandates. The device trajectory signals that the veterinary pain management market will increasingly balance pharmacology with non-pharmacologic modalities.

The Veterinary Pain Management Market Report is Segmented by Product (Drugs Including NSAIDs, Opioids, Local Anesthetics, and More; Devices Including Laser Therapy, Electromagnetic Therapy), Animal Type (Companion Animals, Livestock), End User (Veterinary Hospitals & Clinics, Homecare Settings, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 42.23% of global revenue in 2024, underpinned by high pet insurance penetration and a regulatory climate that enables rapid first-to-market approvals. Monoclonal antibody pioneers capitalized on FDA review efficiencies, securing early brand recognition. Canada's cautious stance on controlled substances has, however, catalyzed investment in non-opioid drugs and cannabinoid research pipelines.

Europe follows closely, shaped by some of the world's strictest welfare legislation. Mandatory multimodal analgesia elevates demand for diverse product kits, pushing suppliers to hold broader formularies. Antimicrobial stewardship programs restrain NSAID courses, indirectly prompting uptake of laser and electromagnetic therapy devices. The United Kingdom's post-Brexit regulatory autonomy is allowing accelerated pathways for niche products, giving smaller firms an entry door ahead of pan-EU approvals.

Asia-Pacific is the fastest-expanding region with a projected 7.35% CAGR. Urban pet ownership in China rose sharply after pandemic-era lifestyle shifts, while Japan's aging pet cohort parallels that of Western markets. South Korea's reform of its Animal Protection Act stipulates pain relief during cosmetic surgery and disease treatment, creating new baseline demand. Emerging Southeast Asian economies deploy welfare upgrades to align with export certification criteria, translating policy into accessible market volume for globally established brands.