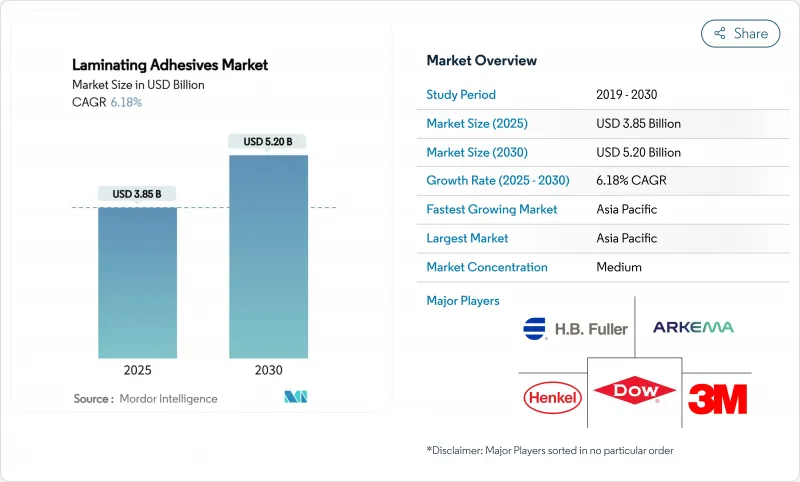

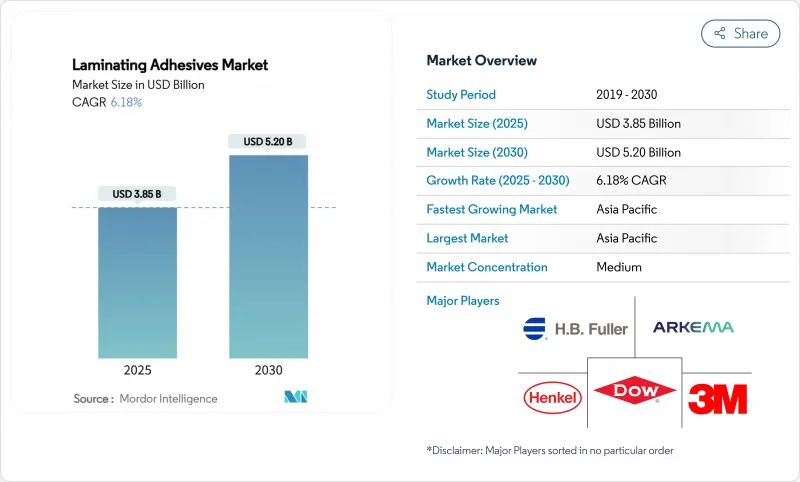

라미네이트 접착제 시장 규모는 2025년에 38억 5,000만 달러, 2030년에는 52억 달러에 이를 것으로 예측되며, 기간 중 CAGR은 6.18%를 나타낼 전망입니다.

화학물질 규제를 강화하는 것 외에도 식품, 의약품 및 전자상거래 소포에서 연포장에 대한 수요가 지속되고 있는 것이 이 꾸준한 확대를 지원하고 있습니다. 브랜드 소유자는 현재 휘발성 유기 화합물(VOC) 배출량을 줄이기 위해 무용제 또는 수성 솔루션을 지정하고 있으며 고급 폴리우레탄(PUR) 및 아크릴 화학물질 채택을 가속화하고 있습니다. 가속화하는 아시아태평양의 산업화, 북미의 왕성한 의료기기 생산, 유럽의 엄격한 서큘러 이코노미 규칙이 총체로서 제품 개발의 우선 순위를 형성하고 있습니다. 경쟁 우위는 수직 통합, 규제 대응력, 비용 및 성능 목표를 충족하는 바이오 원료의 스케일 업 능력에 달려 있습니다.

FDA 21 CFR Part 175 및 중국의 GB 4806.15-2024 식품접촉 접착제 국가규격에 준거한 내이행성 라미네이트 접착제 수요가 계속 늘어나고 있습니다. 정확한 열 활성화 프로파일에 대한 컨버터의 요구는 다층 구조에 걸친 맛의 전이를 방지하면서 높은 레토르트 공정 동안 씰의 무결성을 보장합니다. 선도적인 공급업체는 EU의 디이소시아네이트 임계값 아래의 낮은 단량체 PUR 등급을 통해 차별화를 도모하고 적응 리드 타임을 단축하고 있습니다. 세계적인 식품 브랜드는 정량적인 전환 시험을 점차 의무화하고 있으며, 사내에 애널리틱스가 있으며 세계 규제 서류가 있는 벤더를 선호하고 있습니다. 라미네이트 접착제 시장은 에너지 사용량을 줄이고 직장 안전성을 높이는 무용제 라인을 확대함으로써 이 변화를 활용하고 있습니다.

주조 압출 필름은 물방울 가방의 외관 검사에 필수적인 투명성을 제공하며, 블로우 필름 라미네이트는 의약품 파우치의 내천자성을 향상시킵니다. ISO 10993의 생체적합성 시험에는 높은 장벽이 있어 신규 진입이 제한되어 유효한 등급의 프리미엄 가격이 강화되고 있습니다. 웨어러블 의료기기는 끈적거림과 통증이 없는 박리의 균형을 맞춘 피부 친화적인 접착제 기술 혁신을 촉진합니다. 규제기관은 감마선, 전자빔, 에틸렌옥사이드 공정에 걸친 멸균 안정성을 요구하고 있으며, 멸균 후에도 기계적 강도를 유지하는 화학물질의 연구개발을 뒷받침하고 있습니다. 북미 제조업체는 GMP 시설과 실적 문서를 활용하여 병원과의 장기 계약을 확보하고 있습니다.

미국 환경보호청(EPA)의 40 CFR Part 59는 산업용 접착제에 엄격한 VOC 상한을 설정하여 오랫동안 사용해온 솔벤트 제품의 재제조를 강요하고 있습니다. 캘리포니아에서는 2025년 12월에 비닐 아세테이트가 프로포지션 65로 지정되어 라벨 표시 및 재생산 비용이 지역 전체에서 증가합니다. 동시에 EU 규정은 2026년 8월까지 식품 포장재의 PFAS 총량을 250ppb로 제한하여 PFAS가 없는 화학물질로의 급속한 전환을 촉진합니다. 컴플라이언스 비용과 재인증 시험은 R&D 예산을 늘리고 중소 컨버터에 불균형한 영향을 미치며 라미네이트 접착제 시장 내 통합을 가속화하고 있습니다.

2024년의 라미네이트 접착제 시장에서는 용제계 제품이 45.65%의 점유율을 차지해, 범용성의 높은 접착성과 컨버터가 익숙해지고 있는 것을 반영했습니다. 이 부문은 부드럽게 확장되었지만 VOC에 대한 규제 강화는 에너지 집약적 인 건조 터널 재평가에 박차를 가하고 있습니다. 따라서 무용제 등급은 컨버터가 오븐을 폐지하고 에너지 비용을 최대 40% 삭감하는 고속 탠덤 라인을 채용함에 따라 2030년을 향해 7.64%의 연평균 복합 성장률(CAGR)를 나타낼 전망입니다. 수성 분배는 중간 틈새를 차지하고 솔벤트에서 마이그레이션하는 기업의 학습 곡선을 완화하고 환경 혜택을 제공합니다. 새로운 UV 및 전자빔 경화형 시스템은 즉각적인 녹색 강도와 낮은 전환이 필요한 틈새 응용 분야를 대상으로 합니다.

이 전환을 지원하는 것은 가공 경제성입니다. 반응성 PUR 핫멜트는 핫멜트의 취급성과 열경화성 수지의 최종 강도를 겸비하여 이중 라미네이터와 삼중 라미네이터의 유력한 후보가 됩니다. 히브리 대학의 연구원이 입증한 마이크로파 트리거 광활성 접착제는 온디맨드 재활용을 가능하게 하는 차세대 경화 메커니즘을 시사합니다. 광범위한 기술 포트폴리오를 갖춘 공급업체는 단계적인 장비 업그레이드를 통해 컨버터를 지원하고 포장, 산업 및 운송의 최종 용도에서 일관된 성능을 보장함으로써 전략적 영향력을 얻을 수 있습니다.

2024년 라미네이트 접착제 시장 점유율은 아시아태평양이 49.02%를 차지했고, 2030년까지의 CAGR은 7.09%를 나타낼 전망입니다. 프로판 원료를 활용한 중국의 16억 달러의 아크릴산 투자는 비용 혁신의 시너지 효과를 보여줍니다. 인도의 중간층 증가와 인프라 프로젝트는 마하라슈트라 주에서 헨켈의 록타이트 시설 확장과 함께 이 지역의 생산 능력을 지원합니다. 일본과 한국은 긴밀한 공급망과 견고한 지적 재산 보호의 혜택을 받아 전자 및 EV 배터리 모듈을 위한 고정밀 배합에 기여하고 있습니다.

북미는 첨단 R&D 생태계와 엄격한 규제 감독을 활용하여 지속 가능한 제제의 획기적인 가속화를 추진하고 있습니다. 이 지역은 의료기기 및 의약품 제조에 주도적인 역할을 하고 있으며, FDA 요건에 따라 특수 접착제에 대한 수요를 견인하고 있습니다. 캐나다의 다환 방향족 탄화수소(PAH) 실란트 규제는 이 대륙의 규제가 세계 공급업체에 미치는 영향력을 돋보이게 합니다. 멕시코의 비용 경쟁력있는 공장은 자동차 인테리어 및 소비자 포장의 NAFTA 공급망을 지원합니다.

유럽은 계속 세계 표준을 형성하고 있습니다. EU의 재활용 함량 규제 증가는 컨버터에 대한 투자를 재활용 가능한 PUR 및 아크릴 시스템으로 유도하고 있습니다. 독일의 기술 기반은 지속적인 공정 개선을 촉진하고 프랑스와 이탈리아는 무용제 업그레이드에 의존하는 대규모 컨버팅 클러스터를 유지하고 있습니다. 남미와 중동, 아프리카는 현재 규모가 작은 것, 인프라와 소비자 시장의 확대에 따라 평균 이상의 성장을 보이고 있습니다. 산고반의 10억 2,500만 달러의 FOSROC 거래는 이 지역의 건설 및 산업 분야에 대한 관심 증가를 강조하고 있습니다.

The laminating adhesives market size is valued at USD 3.85 billion in 2025 and is forecast to reach USD 5.20 billion by 2030, advancing at a 6.18% CAGR during the period.

Sustained demand for flexible packaging in food, pharmaceuticals and e-commerce parcels, alongside tightening chemical regulations, underpins this steady expansion. Brand owners now specify solvent-free or water-borne solutions to lower volatile organic compound (VOC) emissions, driving accelerated adoption of advanced polyurethane (PUR) and acrylic chemistries. Accelerating Asia-Pacific industrialization, robust medical device output in North America and stringent circular-economy rules in Europe collectively shape product development priorities. Competitive advantage hinges on vertical integration, regulatory fluency and the ability to scale bio-based raw materials that meet cost and performance targets.

Flexible packaging's 3.2% annual expansion toward a projected USD 341.6 billion by 2028 continues to lift demand for migration-resistant laminating adhesives that comply with FDA 21 CFR Part 175 and China's GB 4806.15-2024 national food-contact adhesive standard. Converter requirements for precise thermal activation profiles ensure seal integrity during high-retort processes while preventing flavor transfer across multilayer structures. Leading suppliers differentiate through low-monomer PUR grades that fall beneath EU diisocyanate thresholds, shortening compliance lead times. Global food brands increasingly mandate quantitative migration testing, favoring vendors with in-house analytics and global regulatory dossiers. The laminating adhesives market capitalizes on this shift by scaling solvent-less lines that cut energy use and elevate workplace safety.

Cast-extruded films deliver crystal clarity vital for IV-bag visual inspection, whereas blown-film laminates boost puncture resistance for pharmaceutical pouches. ISO 10993 biocompatibility testing poses high barriers, restricting new entrants and reinforcing premium pricing for validated grades. Wearable medical devices drive innovation in skin-friendly adhesives that balance adhesion and painless removal. Regulatory bodies demand sterilization stability across gamma, e-beam and ethylene oxide processes, pushing R&D toward chemistries that retain mechanical strength post-sterilization. North American producers leverage GMP facilities and track-record documentation to secure long-term hospital contracts.

The US EPA's 40 CFR Part 59 sets stringent VOC ceilings for industrial adhesives, forcing reformulation of long-standing solvent products. California's listing of vinyl acetate under Proposition 65 effective December 2025 increases labeling and reformulation costs across the region. Concurrently, EU rules cap total PFAS to 250 ppb in food packaging by August 2026, catalyzing rapid migration toward PFAS-free chemistries. Compliance expenditures and re-qualification testing stretch R&D budgets, disproportionately affecting smaller converters and accelerating consolidation within the laminating adhesives market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solvent-borne products retained a 45.65% share of the laminating adhesives market in 2024, reflecting versatile adhesion and entrenched converter familiarity. The segment expands modestly, yet regulatory clampdowns on VOCs spur processors to reassess energy-intensive drying tunnels. Solvent-less grades are therefore registering a vigorous 7.64% CAGR toward 2030 as converters adopt high-speed tandem lines that eliminate ovens and curb energy bills by up to 40%. Water-borne dispersions occupy an intermediary niche, easing the learning curve for firms transitioning away from solvents while offering environmental benefits. Emerging UV- and electron-beam-curable systems target niche applications requiring instant green-strength and low migration.

Processing economics underpin this migration. Reactive PUR hot-melts supply the handling simplicity of hot-melts and the final strength of thermosets, making them prime candidates on duplex and triplex laminators. Microwave-triggered light-activated adhesives demonstrated by Hebrew University researchers hint at next-generation cure mechanisms that could enable on-demand recycling. Suppliers with broad technology portfolios gain strategic leverage by supporting converters through phased equipment upgrades while guaranteeing consistent performance across packaging, industrial and transportation end uses.

The Laminating Adhesives Market Report is Segmented by Type (Solvent-Borne, Water-Borne, and More), Resin Chemistry (Polyurethane, Acrylic, and More), Application (Packaging, Industrial Laminations, and More), and Geography (Asia-Pacific, North America, South America, Europe, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 49.02% of laminating adhesives market share in 2024 and is forecast to grow at a 7.09% CAGR through 2030. China's USD 1.6 billion acrylic acid investment leveraging propane feedstock underlines cost-innovation synergies. India's growing middle class and infrastructure projects, coupled with Henkel's Loctite facility expansion in Maharashtra, anchor regional capacity. Japan and South Korea contribute high-precision formulations for electronics and EV battery modules, benefiting from tight supply chains and robust IP protections.

North America leverages advanced R&D ecosystems and stringent regulatory oversight that accelerate sustainable-formulation breakthroughs. The region's leading role in medical device and pharmaceutical manufacturing drives specialized adhesive demand aligned with FDA requirements. Canada's restriction on polycyclic aromatic hydrocarbon (PAH) sealants highlights the continent's regulatory influence on global suppliers. Mexico's cost-competitive plants support NAFTA supply chains in automotive interiors and consumer packaging.

Europe continues to shape global standards. The EU's escalating recycled-content mandates steer converter investments toward recyclable PUR and acrylic systems. Germany's engineering base fosters continuous process improvements, while France and Italy retain sizable converting clusters that rely on solvent-less upgrades. South America and Middle East & Africa, though smaller today, display above-average growth as infrastructure and consumer markets expand. Saint-Gobain's USD 1.025 billion FOSROC deal underscores rising interest in these regions' construction and industrial segments.