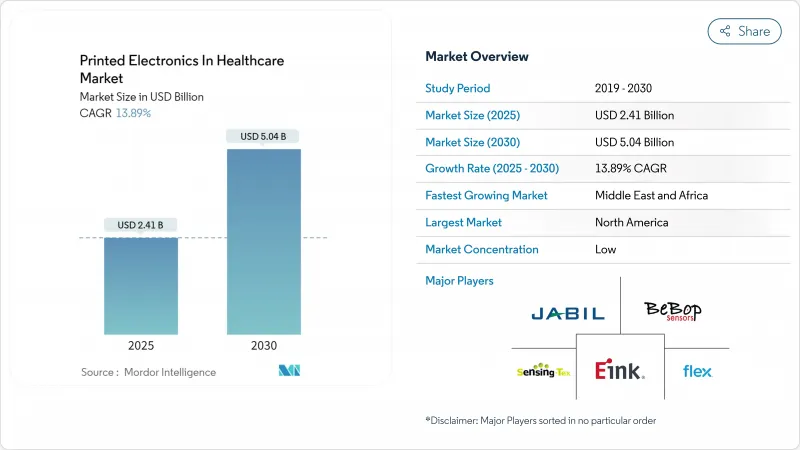

헬스케어 분야 프린티드 일렉트로닉스 시장 규모는 현재 24억 1,000만 달러에 달하고, CAGR 13.89%를 나타내 2030년까지 50억 4,000만 달러에 이를 것으로 예상되고 있습니다.

이 활발한 확장은 유연하고 가벼운 일회용 의료기기를 기존 실리콘 제조에서 지원할 수 없는 단가로 제공하는 기술의 능력으로 인해 발생합니다. 환자를 원격으로 모니터링하는 웨어러블 터미널의 왕성한 수요, 스마트 의약품 패키징의 성장, 생체 적합성 전도성 잉크의 급속한 기술 혁신이 가까운 미래의 성장을 지원합니다. 북미에서는 규제가 조기에 명확화되고, NIH의 보조금도 까다롭기 때문에 상업화 파이프라인이 가속되고, 아시아태평양에서는 POC(Point of Care) 진단의 추진에 의해 고객 기반이 확대됩니다. 한편, 자가 복구 전도체 및 신축성 기판의 돌파구는 임상 채용 장애물이 클리어됨에 따라 새로운 수익원을 약속합니다.

메디케어의 원격 의료에 대한 상환의 확대와 피부 친화적인 포도당 및 심장 패치의 FDA 허가는 가정 의료 채널에서 프린트 센서의 광범위한 전개를 뒷받침하고 있습니다. 하이브리드 마이크로플루이딕 제어 패치는 현재 여러 매개변수의 생체를 캡처하고 클리닉을 방문하지 않고 케어 팀에 자세한 장기 데이터를 제공합니다. 미국 시스템에서는 재입원 감소와 환자 만족도 향상이 보고되어 눈에 보이는 비용 절감이 확인되었습니다. 이러한 환경에서 규모를 확대하고 있는 기기 제조업체는 상환의 틀을 평가하는 EU나 APAC의 의료 제도에 있어서 설득력 있는 선례를 나타내고 있습니다.

EU의 위조 의약품 지침에 따라 완전한 직렬화를 통해 의약품 제조업체는 모든 소매용 팩에 인증 기능을 통합해야 합니다. 고속 Flexo 인쇄 라인에서 생산되는 인쇄 RFID 및 NFC 태그는 현재 제네릭 및 브랜드 제조업체가 허용할 수 있는 단가 수준에서 추적성과 변조 증거를 모두 충족합니다. EU 호환 패키징을 채택한 세계 의약품 기업은 동일한 솔루션을 APAC의 물류 허브로 확장하여 종이 및 포일 기재에 최적화된 전도성 잉크 수요에 승수 효과를 제공합니다.

실제 510(k) 심사는 심사관이 새로운 기재에 대한 추가 벤치 데이터와 임상 데이터를 요구하기 때문에 공칭 스케줄을 크게 넘어 6-7개월에 이르는 경우가 많습니다. 또한 유럽의 새로운 MDR에서는 임상 성능 시험이 추가되어 이중 신청 트럭을 강요하고 있습니다. 사이버 보안 및 AI 문서화 요구사항이 증가하고 테스트 비용이 부족하기 때문에 일부 중견기업은 미국에서 상시를 연기하고 중동과 남미에서의 시험적 배치를 선호하고 있습니다.

프린티드 바이오센서는 2024년에 프린티드 일렉트로닉스 시장의 41.8%를 차지했습니다. 포도당 스트립과 지속 포도당 모니터가 설치 기반의 대부분을 차지하고 일상적인 모니터링 오명을 반환하는 미국의 시판 승인이 뒷받침되고 있습니다. 전염병 분석은 APAC의 공중 보건 입찰에서 성장 엔진이지만, 신흥 pH 패치와 상처 모니터 패치는 임상 폭을 넓히고 있습니다.

신축성이 뛰어난 유연한 하이브리드 전자 제품은 CAGR이 16.3%로 가장 빠를 것으로 예측됩니다. 자기 회복성 전도성 메쉬는 박리 없이 반복되는 스트레인 사이클을 견딜 수 있어 1주일에 걸쳐 심장과 신경을 모니터링할 수 있습니다. 의약품 팩용 인쇄 RFID 라벨은 특히 세계적인 직렬화 의무가 성숙함에 따라 두 번째 수요의 기둥이 됩니다.

스크린 인쇄는 입증된 처리량과 일회용 전극의 단가가 낮아 2024년 프린티드 일렉트로닉스 시장의 52.9%를 획득했습니다. 성숙한 공정 관리는 FDA 신청을 용이하게 하며 대량 생산 바이오센서의 기본값입니다.

에어로졸 제트법과 3D법은 CAGR 14.7%를 나타낼 전망입니다. 3D 마이크로플루이딕스 채널 내에 전도성 트랙을 증착하는 능력은 프로토타이핑 시간을 며칠에서 몇 분으로 단축시켰습니다. 스위스와 싱가포르의 조기 채용 기업은 파일럿 스케일에서 100μm 이하의 유로 충실도를 입증하여 실험실 온칩 진단을 위한 신속한 설계 반복을 가능하게 합니다.

북미는 2024년 세계 매출의 40.8%를 차지하며, FDA의 조기 디지털 헬스의 틀과 재료의 연구개발 위험을 경감하는 NIH의 자금 제공 흐름의 혜택을 받았습니다. 메이요 클리닉과 클리블랜드 클리닉의 다시설 테스트는 원격 모니터링의 엔드포인트를 검증하고 지역 병원 네트워크의 조달 승인을 원활하게 합니다. 온타리오 주에 있는 캐나다의 연구 클러스터는 특수 기판에 대한 전문 지식을 추가하고 대륙의 리더십을 더욱 강화하고 있습니다.

유럽은 여전히 전략적 기지입니다. 이 지역의 제약 대기업은 위조 의약품 지침을 준수해야하며 직렬화 된 스마트 태그에 대한 지속적인 수요가 예상됩니다. 독일 정밀 기계의 전통은 대량 인쇄기를 지원하고 영국은 벤처 자금을 유연한 IC의 신흥 기업으로 옮깁니다. 프랑스와 북유럽 국가의 공중 보건 당국은 원격 센서의 예방 의료 보험 상환을 통해 보급을 촉진합니다.

중동 및 아프리카의 CAGR은 15.4%로 예측되며, 이는 세계에서 가장 빠릅니다. 사우디아라비아와 아랍에미리트(UAE)의 국가 위생 확장은 커넥티드 다이아그노스틱스에 예산 프레임을 할당하고 있으며, 프린티드 일렉트로닉스가 무거운 인프라를 필요로 하지 않고 농촌를 커버하는 신속한 경로가 될 것으로 보고 있습니다. 남아프리카의 규제 기관은 장치 코드를 FDA 분류에 맞추어 수입 승인을 가속화하고 있습니다. 이 기세는 이 지역의 의료기술 자급률에 한층 변화를 가져오는 것입니다.

The printed electronics market size in healthcare is currently valued at USD 2.41 billion and is forecast to achieve USD 5.04 billion by 2030, reflecting a 13.89% CAGR.

This vigorous expansion stems from the technology's ability to deliver flexible, lightweight, and disposable medical devices at unit costs traditional silicon manufacturing cannot match. Strong demand for remote patient-monitoring wearables, growth in smart pharmaceutical packaging, and rapid innovation in biocompatible conductive inks anchor near-term growth. North America's early regulatory clarity and generous NIH grants accelerate commercialization pipelines, while Asia-Pacific's push for point-of-care diagnostics widens the customer base. Meanwhile, breakthroughs in self-healing conductors and stretchable substrates promise fresh revenue streams as clinical adoption hurdles are cleared.

Medicare's broader reimbursement for telehealth, coupled with FDA clearance of skin-friendly glucose and cardiac patches, fuels wide deployment of printed sensors in the home-care channel. Hybrid microfluidic-regulated patches now capture multi-parameter vitals, handing care teams granular longitudinal data without clinic visits. U.S. systems report fewer readmissions and higher patient satisfaction, confirming tangible cost savings. Device makers scaling in this environment set a compelling precedent for EU and APAC health systems as they evaluate reimbursement frameworks.

Full serialization under the EU Falsified Medicines Directive forces pharmaceutical producers to embed authentication features on every retail pack. Printed RFID and NFC tags, fabricated on high-speed flexographic lines, now satisfy both traceability and tamper evidence at unit cost levels acceptable to generic and branded manufacturers. Global drug firms adopting EU-compliant packaging extend the same solutions to APAC logistics hubs, creating a multiplier effect on demand for conductive inks optimized for paper and foil substrates.

Actual 510(k) reviews often stretch to 6-7 months, well beyond nominal timelines, as examiners request extra bench and clinical data on novel substrates. De novo classifications lengthen approvals further, and the new European MDR imposes additional clinical performance studies, forcing dual submission tracks. Rising cybersecurity and AI documentation requirements add layers of testing cost, prompting some mid-cap firms to defer U.S. launches in favor of pilot deployments in MEA or South America.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Printed biosensors held 41.8% of the printed electronics market in 2024. Glucose strips and continuous glucose monitors dominate the installed base, buoyed by over-the-counter U.S. approvals that destigmatize routine monitoring. Infectious disease assays remain a growth engine in APAC public-health tenders, while emerging pH and wound-monitor patches broaden clinical reach.

Stretchable and flexible hybrid electronics is projected to post a 16.3% CAGR, the fastest among types. Self-healing conductive meshes now survive repeated strain cycles without delamination, allowing week-long cardiac or neuro monitoring. Printed RFID labels for pharma packs add a second demand pillar, especially as global serialization mandates mature

Screen printing captured 52.9% of the printed electronics market in 2024 thanks to proven throughput and low per-unit costs for disposable electrodes. Mature process controls ease FDA filing, making it the default for high-volume biosensors.

Aerosol jet and 3D methods are growing at a 14.7% CAGR. Their ability to deposit conductive tracks inside 3D microfluidic channels has cut prototyping times from days to minutes. Early adopters in Switzerland and Singapore have demonstrated sub-100 µm channel fidelity at pilot scale, enabling rapid design iteration for lab-on-chip diagnostics.

The Printed Electronics in Healthcare Market Report is Segmented by Type (Printed Biosensors, Printed Physiological Sensors, Printed RFID/NFC Labels, and More), Printing Technology (Screen Printing, Inkjet Printing, and More), Application (Patient Monitoring, Diagnostic Testing, Drug Delivery, and More), End-User (Hospitals, Home Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America posted 40.8% of global revenue in 2024, benefiting from FDA's early digital-health frameworks and NIH funding streams that de-risk material R&D. Multicenter trials at Mayo Clinic and Cleveland Clinic validate remote monitoring endpoints, smoothing procurement approvals for regional hospital networks. Canadian research clusters in Ontario add specialized substrate expertise, further bolstering continental leadership.

Europe remains a strategic stronghold. The region's pharmaceutical giants must comply with the Falsified Medicines Directive, locking in sustained demand for serialized smart tags. Germany's precision-machinery heritage supports high-volume printing presses, while the United Kingdom channels venture funding into flexible IC startups. Public health authorities in France and Nordic nations augment uptake through preventive-care reimbursement for remote sensors.

The Middle East and Africa is forecast to deliver a 15.4% CAGR, the fastest worldwide. National health expansions in Saudi Arabia and the United Arab Emirates allocate budget lines for connected diagnostics, seeing printed electronics as a quick path to rural coverage without heavy infrastructure. South Africa's regulatory agency aligns its device code to FDA classification, accelerating import approvals. This momentum signals a step-change in the region's medical technology self-sufficiency.