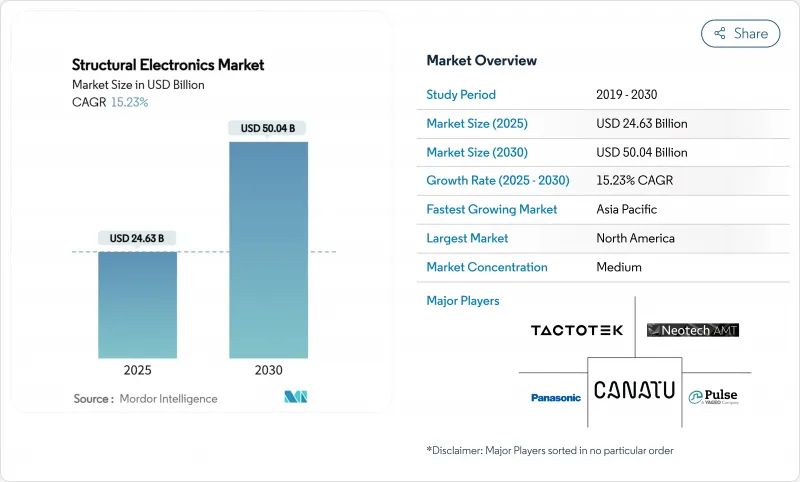

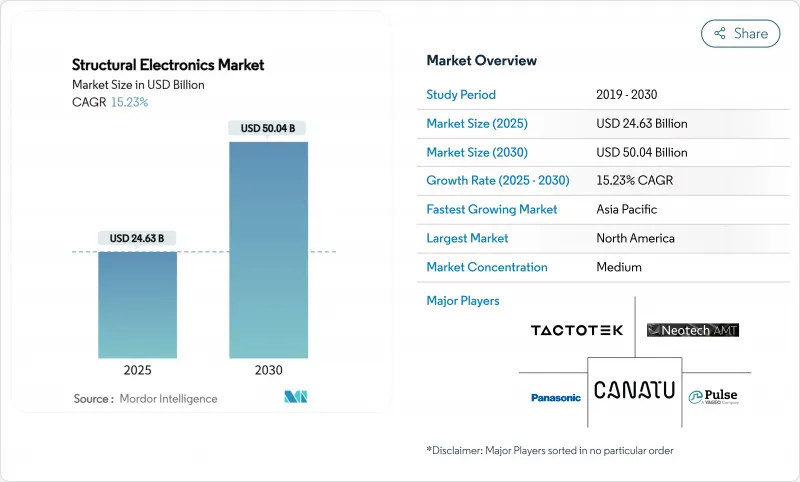

구조 전자공학 시장은 2025년에 246억 3,000만 달러에 이르고, 2030년에는 500억 4,000만 달러에 달할 것으로 예상되며, CAGR은 15.23%를 나타낼 전망입니다.

이 가속은 급속히 진행되는 자동차의 경량화 의무화, 반도체 정책에 의한 우대 조치, 내하중 부품에 회로를 직접 내장하는 3D 인몰드 전자공학에 있어서 새로운 브레이크 스루를 반영하고 있습니다. 자동차 제조업체는 현재 경량화와 전기자동차의 항속 거리 연장을 위해 센서 스킨과 구조용 배터리를 캐빈 패널에 접고 있으며, 아시아태평양의 소비자용 전자기기 공장은 곡선형 터치식 하우징의 양산을 확대하고 있습니다. 유럽의 Chips Act와 미국의 CHIPS and Science Act와 같은 규정은 구조 통합을 단순화하는 고급 패키징 기지에 자본을 주입합니다. 지리적 성장은 아시아태평양 제조의 깊이에 의해 뒷받침되지만, 중동 방어와 스마트 인프라 프로젝트가 미래 수요를 끌어올릴 것입니다.

유럽 자동차 제조업체는 통합 전력 전자 장치가 장착된 보다 가벼운 차량을 선호하는 엄격한 함대 방출 규제에 직면하고 있습니다. 시노나스 AB의 탄소섬유 구조 배터리는 50%의 경량화와 함께 70%의 항속 거리 향상을 보여주며 단일 복합 부품이 에너지 저장과 기계적 부하 운반을 모두 수행할 수 있는 방법을 보여줍니다. 이 디자인은 또한 가연성 액체 전해질을 반고체 화학물질로 대체함으로써 열 폭주의 우려를 줄여줍니다. 폭스바겐과 같은 자동차 제조업체들은 이러한 배터리를 온세미 탄화규소 인버터와 연동시켜 부품 수를 줄이고 드라이브 트레인의 효율을 높입니다. 철강과 알루미늄의 기가 캐스팅을 둘러싼 논쟁은 모든 구조 재료에 회로를 통합하는 가치를 더욱 돋보이게합니다. 그 결과 섀시, 도어, 기기 패널 등의 구조 전자공학 시장의 채용이 급속히 증가하고 있습니다.

중국, 한국, 베트남의 소비자 기기 수탁 제조업자는 전도성 잉크, 필름, 수지를 1회의 성형 공정으로 조합하는 3D 인몰드 전자공학를 표준화하고 있습니다. TactoTek의 사출 성형 구조 전자공학(IMSE) 공정은 기존 조립에 비해 온실가스 배출량을 60% 줄이고 플라스틱 사용량을 70% 줄일 수 있음을 확인했습니다. 코베스트로의 Makrofol 폴리카보네이트 필름은 초박형 쉘 내에서 터치 조명과 촉각 피드백을 가능하게 합니다. 홍콩 대학의 유기 전기 화학 트랜지스터와 같은 지역 연구는 웨어러블, 온 센서 컴퓨팅의 다음 파도를 추진합니다. 동남아시아의 PCB 부문은 이미 20억 달러를 넘는 생산량을 자랑하며 이러한 구조 하우징과 짝을 이루는 다층 백플레인을 공급하고 있습니다. 가속화하는 투어링 사이클은 스마트폰, 히어러블, 스마트 홈 허브 등의 제품 출시를 지원하고, 개인 전자 제품 전체의 구조 전자공학 시장을 밀어 올립니다.

탄소나노튜브 잉크와 페이스트는 세계 생산량의 40% 이상을 차지하는 한 줌의 중국 공장에 집중하고 있습니다. 노스캐롤라이나의 고순도 석영을 파괴한 허리케인은 반도체 기판에 필수적인 원료 체인의 취약성을 드러냈습니다. 미국과 유럽의 생산자가 최근 발표한 CNT의 스케일 업은 여전히 수요 성장 예측에 미치지 못하고 있습니다. 그 결과, 자동차와 항공우주의 바이어는 리드 타임의 장기화와 가격 상승에 직면하여 다양한 조달이 가능할 때까지 구조 전자공학 시장의 확대를 억제하게 됩니다.

센서와 안테나의 카테고리는 ADAS(첨단 운전자 보조 시스템)와 항공기의 안전 모니터링의 의무화에 힘입어 2024년에 34.7%의 매출에 공헌했습니다. 비행 복합 패널에는 광섬유 어레이가 내장되어 승용차 대시보드에 레이더와 커패시턴스 터치가 통합되어 있습니다. 태양광 발전은 2030년까지의 CAGR이 17.5%로 가장 높아 건물의 인테리어나 웨어러블 태그를 따르도록 만곡하는 플렉서블 페롭스카이트 모듈이 견인합니다. 구조적 통합은 별도의 하우징 없이 발전을 가능하게 하고, 조립 비용을 줄이고, 자산 추적 및 실내 농업에 새로운 용도를 엽니다.

구조 배터리와 마이크로 슈퍼커패시터는 611 F cm-3의 부피 커패시턴스를 실현하는 MXene 잉크 장치에서 볼 수 있듯이 프로토타입 영역을 넘어서고 있습니다. 디스플레이는 자동차의 스타일링 동향에 추종하고 OLED나 마이크로 LED 필름에 의한 연속 곡면으로 향하고 있습니다. 상호접속재료는 구리의 휘발성에 직면하면서도 은 나노와이어나 MXene을 사용함으로써 구부러진 포맷에서도 전도성을 유지할 수 있게 됩니다. 이러한 변화는 감지, 에너지 및 디스플레이 기능을 하나의 라미네이트로 실현하는 구조 전자공학 시장을 확장합니다.

인몰드 전자공학는 필름, 잉크, 수지를 융합하여 즉시 장착할 수 있는 경량 부품으로 출하함으로써 2024년에 51.3%의 매출을 획득했습니다. 자동차 도어 트림에는 별도의 PCB를 사용하지 않고 백라이트 컨트롤이 장착되어 와이어 하네스의 무게가 줄어 듭니다. 소비자용 웨어러블 제품은 IP68 표준 케이싱에 동일한 프로세스를 채택합니다. Additive Manufacturing은 DARPA의 AMME 프로그램에 지원되어 복잡한 마이크로 회로를 3차원 기판에 직접 프린트하는 CAGR 최고 18.2%를 기록. MXene 잉크의 에어로졸 제트 인쇄는 에너지 밀도가 높은 커패시터를 실현하고 다광자 리소그래피는 인쇄 가능한 유기 바이오 전자공학를 개척합니다.

스크린 인쇄기와 플렉소 인쇄기는 대면적 히터와 가전 패널의 안테나에 비용 효율적으로 대응할 수 있습니다. 잉크젯 플랫폼은 금형이 대량 성형으로 전환되기 전에 미세한 프로토타입을 제공합니다. 이 기술이 보급됨에 따라 진입의 선택이 넓어지고, 대량 생산과 특주 생산의 양쪽 모두로 구조 전자공학 시장의 채용이 가속합니다.

아시아태평양은 반도체, PCB, 몰딩의 대량생산 에코시스템으로 2024년 매출의 37.9%를 차지했습니다. 중국은 수직 통합을 추진하고 태국과 말레이시아는 세계 공급에 공급 능력을 추가하고 있습니다. 일본은 세계 적층 세라믹 커패시터의 절반 이상을 공급하고 있으며, 무라타 제작소와 QuantumScape와 같은 파트너십은 고체 전지 세라믹으로 다각화하고 있습니다.

유럽의 구조 전자공학 시장은 자동차 전기의 이정표와 800억 유로(940억 6,000만 달러)의 Chips Act 기금으로부터 혜택을 받으며 2030년까지 세계 반도체 점유율 20%를 목표로 하고 있습니다. 독일의 OEM은 회로를 통합한 기가 주조에 연마를 하고, 프랑스의 건설회사는 태양광 발전을 이용한 센서 스킨을 개수용 외관에서 시험적으로 사용하고 있습니다.

중동 및 아프리카는 국방 근대화와 스마트 시티 전개에 밀려 CAGR 최고 속도 15.7%를 나탄래 전망입니다. 아랍에미리트(UAE)의 EDGE 그룹은 컨포멀 안테나와 경량 전원을 필요로 하는 AI 대응 위성 링크를 모색. 지방자치단체는 국내 조립라인에 종을 뿌리는 오프셋 프로그램으로 공급업체를 유치하고 있지만, 이 지역은 여전히 나노재료의 대부분을 수입하고 있으며, 이 갭이 10년대 후반의 성장을 억제할 가능성이 있습니다.

북미는 항공우주 프로젝트와 첨단 패키징 파운드리에 대한 새로운 CHIPS 법 보조금을 통해 기세를 유지하고 있습니다. 보잉사에 의한 스피릿사의 인수는 센서 대응 기체 부분의 통합 강화를 목표로 하고 있습니다. 연방규칙이 국산공급을 우대하게 되면서 구조 전자공학 시장 진입기업은 재료, 인쇄, 성형능력의 공동 배치를 진행시킵니다.

The structural electronics market reached USD 24.63 billion in 2025 and is forecast to rise to USD 50.04 billion by 2030, translating to a 15.23% CAGR.

This acceleration reflects fast-moving vehicle lightweighting mandates, semiconductor policy incentives, and fresh breakthroughs in 3-D in-mold electronics that embed circuitry directly into load-bearing parts. Automotive manufacturers now fold sensor skins and structural batteries into cabin panels to trim weight and extend electric-vehicle range, while Asia-Pacific consumer-electronics plants scale volume production of curved, touch-activated housings. Regulations such as the European Chips Act and the U.S. CHIPS and Science Act pump capital into advanced packaging hubs that simplify structural integration. Geographic growth remains anchored in Asia-Pacific manufacturing depth, but defense and smart-infrastructure projects in the Middle East lift future demand.

European automakers face firm fleet-emission rules that prioritize lighter vehicles equipped with integrated power electronics. Sinonus AB's carbon-fiber structural battery shows a 70% range boost coupled with 50% weight reduction, illustrating how a single composite part can both store energy and carry mechanical loads. The design also mitigates thermal-runaway concerns by replacing flammable liquid electrolytes with semi-solid chemistries. Automakers such as Volkswagen link these batteries with silicon-carbide inverters from onsemi to shrink component count and raise drivetrain efficiency. The debate around steel versus aluminum gigacasting further underscores the value of embedding circuitry into any structural material. The result is a rapid uptick in structural electronics market adoption across chassis, doors, and instrument panels.

Consumer-device contract manufacturers in China, South Korea, and Vietnam are standardizing 3-D in-mold electronics that combine conductive inks, films, and resins in a single molding step. TactoTek's injection-molded structural electronics (IMSE) process has verified a 60% drop in greenhouse-gas emissions and 70% less plastic usage versus traditional assembly. Covestro's Makrofol polycarbonate films enable touch lighting and haptic feedback inside ultrathin shells. Regional research, such as organic electrochemical transistors from the University of Hong Kong, drives the next wave of wearable, on-sensor computing. Southeast Asia's PCB sector, already above USD 2 billion in output, supplies multilayer backplanes that mate with these structural housings. Accelerated tooling cycles support product launches in smartphones, hearables, and smart-home hubs, lifting the structural electronics market across personal electronics.

Carbon-nanotube inks and pastes are concentrated in a handful of Chinese plants that together command over 40% of global output. Hurricanes that disrupted high-purity quartz in North Carolina exposed parallel weaknesses in raw-material chains essential for semiconductor substrates. Recent CNT scale-up announcements from U.S. and European producers remain short of demand growth projections. Automotive and aerospace buyers consequently face longer lead times and price spikes, constraining structural electronics market expansion until diversified sourcing becomes available.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The sensor and antenna category contributed 34.7% revenue in 2024, buoyed by mandates for advanced driver-assistance systems and aircraft safety monitoring. Flight composite panels now embed fiber-optic arrays, whereas passenger-vehicle dashboards integrate radar and capacitive touch in one molded insert. Photovoltaics post the strongest 17.5% CAGR through 2030, driven by flexible perovskite modules that curve around building interiors and wearable tags. Structural integration allows power generation without separate housing, shrinking assembly cost, and opening new applications in asset tracking and indoor agriculture.

Structural batteries and micro-super-capacitors move beyond prototypes, illustrated by MXene ink devices delivering 611 F cm-3 volumetric capacitance. Displays follow automotive styling trends toward continuous curved surfaces enabled by OLED and micro-LED films. Interconnect materials confront copper volatility yet gain from silver-nanowire and MXene alternatives that sustain conductivity in bendable formats. Together, these shifts expand the structural electronics market as designers combine sensing, energy, and display functions within a single laminate.

In-mold electronics captured 51.3% revenue in 2024 by fusing films, inks, and resin into lightweight parts that ship ready-to-install. Automotive door trims now host back-lit controls without separate PCBs, cutting wire harness weight. Consumer wearables adopt the same process for IP68-rated casings. Additive manufacturing records the highest 18.2% CAGR, supported by DARPA's AMME program that 3-prints complex micro-circuits directly onto three-dimensional substrates. Aerosol-jet printing of MXene inks scales energy-dense capacitors, while multiphoton lithography pioneers printable organic bioelectronics.

Screen and flexographic presses remain cost-effective for large-area heaters and antennas on appliance panels. Inkjet platforms supply fine-feature prototypes before tooling commits to mass molding. This technology spreads, widening entry options, accelerating structural electronics market adoption in both high-volume and bespoke production runs.

Structural Electronics Market Report is Segmented by Integrant (Photovoltaics, Batteries/Super-capacitors, and More), Manufacturing Technology (In-Mold Electronics, Additive Manufacturing/3-D Printing, and More), Material (Conductive Inks, Substrates, Encapsulation and Adhesives), Application (Automotive, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific delivered 37.9% of 2024 revenue by virtue of high-volume semiconductor, PCB, and molding ecosystems. China drives vertical integration, while Thailand and Malaysia add capacity that feeds global supply. Japan supplies over half the world's multilayer ceramic capacitors, and partnerships such as Murata with QuantumScape diversify into solid-state battery ceramics.

Europe's structural electronics market gains from automotive electrification milestones and EUR 80 billion (USD 94.06 billion) in Chips Act funds, targeting a 20% global semiconductor share by 2030. German OEMs refine giga casting with embedded circuits, whereas French construction firms pilot PV-powered sensor skins on retrofit facades.

The Middle East and Africa record the fastest 15.7% CAGR, propelled by defense modernization and smart-city rollouts. UAE's EDGE Group explores AI-enabled satellite links that demand conformal antennas and lightweight power sources. Local governments entice suppliers with offset programs that seed domestic assembly lines, yet the region still imports most nanomaterials, a gap that could temper late-decade growth.

North America keeps momentum through aerospace projects and fresh CHIPS Act subsidies for advanced packaging foundries. Boeing's acquisition of Spirit targets tighter integration of sensor-ready fuselage sections. Federal rules now favor home-grown supply, nudging structural electronics market participants to co-locate material, printing, and molding capabilities.