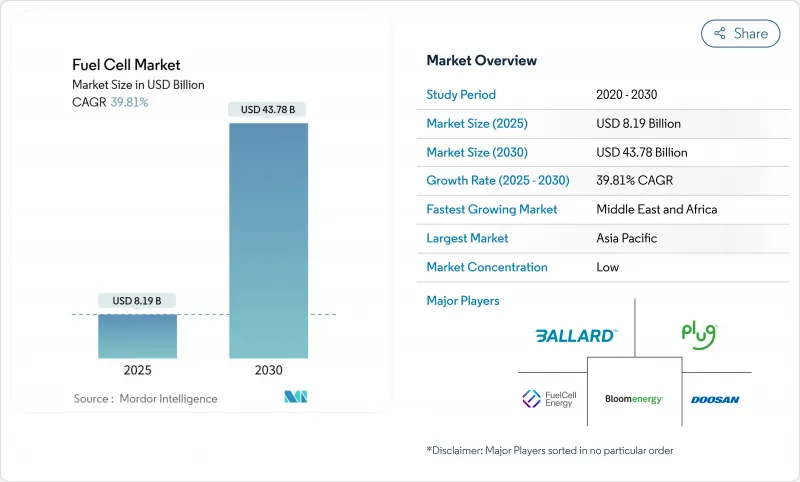

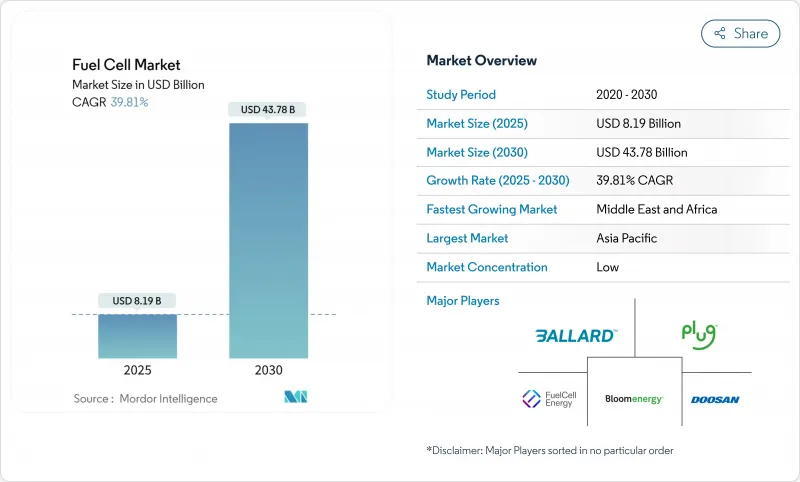

연료전지 시장 규모는 2025년에 81억 9,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 39.81%로, 2030년에는 437억 8,000만 달러에 달할 것으로 예상됩니다.

확장의 배경은 운송, 데이터센터 및 유틸리티 규모 용도에서 수요가 급증하고 있으며, 각각은 보다 깨끗한 에너지 정책의 의무화의 혜택을 받고 있습니다. 그린 수소와 블루 수소의 비용 절감, 아시아태평양의 수소 보급 코리도의 급속한 전개, 대형 트럭 제조업체에 의한 투자의 가속이, 상업적인 길을 넓혀가고 있습니다. 기술 혁신의 기세는 거치형 부하에 대응하는 고체 산화물 연료전지로 변화하고 있지만, 한편 고체 고분자형 연료전지는 자동차, 버스, 지게차의 주류로 계속되고 있습니다. 백금족 금속과 수소 인프라의 갭을 둘러싼 공급망 위험이 당면 성장을 억제하는 한편, 해운사업자와 유틸리티자의 관심의 고조가 연료전지 시장의 대응가능한 밑단을 더욱 넓히고 있습니다.

미국의 클린수소제조세액공제(최대 3달러/kg)와 EU재생가능에너지지령의 산업용 재생가능수소할당량 42%라는 정책 인센티브가 투자 파이프라인을 지원하고 있습니다. 2020년부터 2024년 사이에 최종 투자 결정에 이르는 프로젝트가 7배로 급증한 것은 자본 흐름의 심화를 반영했습니다. 수소 연료는 일반적으로 연료전지의 총 소유 비용의 절반 가까이를 차지하기 때문에 저렴한 분자는 직접 확산을 확장합니다. 연료전지 시장의 개척자는 2USD/kg 이하의 수소가 장거리 운송 차량에 있어서 디젤과 동등하게 되는 계기가 될 것으로 예측했습니다.

도요타, 현대차, 혼다는 향후 2년간 4만 5,000대의 FCEV 공급 계약을 포함한 수소 모빌리티을 위한 수십억 달러 규모의 로드맵을 약속했습니다. 중국은 2035년까지 100만대의 연료전지차와 2,000기의 스테이션을 목표로 내걸고 있으며, 한국은 수소트럭을 국가 스마트 그리드 계획에 연결하고 있습니다. 자동차 제조업체 각사는 생산 스케줄의 조정, 에너지 기업과의 합작 사업, 스테이션의 공동 투자에 의해 스케일 업의 스케줄을 단축하고 있습니다. 이러한 수요 신호는 스택 공급업체, 압축기 제조업체 및 연료 보급 통합 업체를 통해 연료전지 시장에 연결됩니다.

일본과 한국의 성숙한 회랑을 제외하고 네트워크의 밀도는 여전히 부족합니다. 독일은 유럽을 선도하는 약 170개의 공공 수소 스테이션을 가지고 있지만, 그 커버율은 지역 트럭 운송 경로의 요구에 아직 미치지 못합니다. 미국에서는 캘리포니아 주에서만 일관된 건설 계획을 제공하며 1kg당 12-15달러의 펌프 가격이 함대 전체의 전개를 방해하고 있습니다. 인프라 정비 지연은 함대 전환을 늦추고 조기 도입 기업의 투자 회수 기간을 늘리고 연료전지 시장의 전체량을 줄이고 있습니다.

차량 부문은 2024년 세계 매출의 80.9%를 차지하고 연료전지 시장에서 중심적인 역할을 한 것으로 확인되었습니다. 상용 트럭, 시 버스, 소형차는 고속 연료 보급과 장거리 주행을 실현하는 PEMFC 아키텍처에 의존합니다. 최근 235대의 수소트럭이 도매되어 유럽 연료전지 버스의 대량 주문과 함께 수요곡선이 성숙하고 있음을 보여주고 있습니다. 수소 가격이 낮아지고 유지 보수가 절약됨에 따라 디젤 차량의 총 비용 차이가 줄어들고 있습니다.

데이터센터, 통신타워, 병원용 거치형이 나머지 19.1%의 점유율을 차지해 급성장을 이루고 있습니다. 하이퍼스케일 사업자는 디젤 발전기를 대체하는 몇 메가와트의 설비를 시험적으로 도입하고 있습니다. 이러한 초기 단계에서의 승리는 2030년 이후 가동 시간과 배기가스 규제가 입증됨에 따라 연료전지 시장이 모바일용과 거치형 사이에서 보다 균등하게 균형을 이룬다는 것을 시사합니다.

PEMFC는 승용차와 자재관리 플릿에 의해 지원되며 2024년에는 70.4%의 점유율을 유지했습니다. 작동 온도가 낮기 때문에 빈번한 시동·정지에 적합하고, 도시에서의 가동률이 높아집니다. 스택 수명 개선 및 막 재활용 프로그램은 PEMFC의 경제성을 더욱 향상시킵니다.

그러나 SOFC는 2030년까지 연평균 복합 성장률(CAGR)이 51.1%로 예측되어 가장 빠르게 성장하고 있습니다. 60% 가까이 전기효율과 유연한 연료 투입으로 유틸리티과 데이터센터 고객은 오늘은 파이프라인 가스로, 내일은 수소로 가동할 수 있게 됩니다. 블룸 에너지의 몇 메가와트 규모의 주문은 이러한 변화를 뒷받침합니다. 결과적으로 SOFC 시스템의 연료전지 시장 규모는 베이스로드 대체와 마이크로그리드 용도의 혼합을 반영하여 2035년까지 200억 달러 이상에 달할 것으로 예상됩니다. 알칼리, 인산, 용융 탄산염 연료전지는 특정 산업 틈새에 대응하여 기술 스펙트럼을 완성합니다.

연료전지 시장 보고서는 용도별(차량용, 비차량용), 기술별(고분자 전해질막 연료전지, 고체 산화물 연료전지, 알칼리성 연료전지 등), 연료 유형별(수소, 천연가스, 암모니아 등), 최종사용자 산업별(운수, 유틸리티, 상업 및 산업, 기타), 지역별(북미, 유럽, 아시아, 태평양, 남미)

아시아태평양은 2024년 연료전지 시장에서 57.8%의 점유율을 차지했습니다. 일본의 전략적 로드맵은 연료전지 자동차와 주택용 마이크로CHP 유닛에 보조금을 내고 한국은 수소와 스마트 시티 구상을 세트로 하고 있습니다. 중국은 2035년까지 100만대의 FCEV와 2,000기의 스테이션을 목표로 내걸고 있으며, 이는 기타 국가에서는 예를 들지 않는 규모입니다. 지방정부는 전해조에 자금을 공급하고 통행료를 면제하여 차량의 운영 비용을 절감하고 있습니다. 유명한 자동차 그룹은 트럭, SUV 및 지게차에 연료전지를 통합하고 지역 공급업체에 부품 수요를 고정화합니다.

북미는 미국의 정책적 추풍을 받아 2위를 차지했습니다. 클린 수소 생산세 공제와 7개 지역 수소 허브는 전해, 저장, 다운스트림 프로젝트를 위해 수십억 달러를 동원합니다. 캘리포니아의 첨단 클린 트럭 규정은 중형 및 대형 함대의 초기 수요를 지원하고 캐나다의 각 주는 수소 버스를 지원합니다. 텍사스, 일리노이 및 버지니아의 데이터센터 사업자는 송전망의 신뢰성을 높이기 위해 몇 메가 와트의 SOFC 플랜트를 계약하고이 지역의 연료전지 시장에 두께를 더했습니다.

유럽은 Fit-for-55 기후 변화 대책 패키지를 활용하여 트럭, 철도, 해운에서 연료전지의 채용을 촉진합니다. 최신 CO2 기준에서는 2040년까지 대형차의 배출가스를 90% 삭감하는 것이 요구되고 있으며, 수소추진은 신뢰할 수 있는 길입니다. 독일의 170개가 넘는 공공 스테이션은 대륙을 이끌고 있습니다. 유럽 수소 은행(European Hydrogen Bank)과 혁신 기금(Innovation Fund)은 입찰 참가자들에게 보조금을 제공하여 전해조 및 스택 플랜트의 규모 증가 위험을 줄입니다. 스페인에서 프랑스까지의 국경을 넘는 파이프라인 업그레이드는 미래의 그린 수소 흐름을 위한 인프라를 정비합니다.

중동 및 아프리카는 CAGR 예측 41.2%로 가장 빠른 성장 전망을 보여줍니다. 풍부한 태양광 자원과 풍력 자원은 경쟁력 있는 그린 수소의 수출 거점을 형성합니다. 이집트, 아랍에미리트(UAE), 사우디아라비아는 각각 운송 고객을 위한 암모니아 생산과 관련된 몇 기가와트의 전해조 공원을 계획하고 있습니다. 기존 천연가스 파이프라인과 항만 인프라는 수소혼합 연료로의 전환을 가능하게 하는 플랫폼을 제공합니다. 아프리카 경제는 약전망을 안정시키고 디젤 발전기를 대체하는 현지 연료전지 마이크로그리드에 주목하고 있으며 새로운 수요의 파도를 조율하고 있습니다.

The Fuel Cell Market size is estimated at USD 8.19 billion in 2025, and is expected to reach USD 43.78 billion by 2030, at a CAGR of 39.81% during the forecast period (2025-2030).

Expansion is rooted in surging demand from transportation, data centers, and utility-scale applications, each benefiting from cleaner-energy policy mandates. Falling costs of green and blue hydrogen, rapid roll-outs of hydrogen refueling corridors in Asia-Pacific, and accelerating investment from heavy-duty truck makers together widen commercial pathways. Innovation momentum is shifting toward solid oxide fuel cells that serve stationary loads, while polymer electrolyte membrane fuel cells continue to dominate cars, buses, and forklifts. Growing interest from maritime operators and utilities further broadens the addressable base of the fuel cell market, even as supply-chain risks around platinum group metals and hydrogen infrastructure gaps temper near-term growth.

Green hydrogen production costs are set to decline by up to 60% by 2030 as electrolyzer manufacturing scales and renewable power prices fall.Policy incentives such as the U.S. Clean Hydrogen Production Tax Credit of up to USD 3.00/kg and the EU Renewable Energy Directive's 42% renewable-hydrogen quota for industry underpin investment pipelines. A seven-fold jump in projects reaching final investment decision between 2020 and 2024 reflects deepening capital flows. As hydrogen fuel typically represents nearly half of a fuel cell's total cost of ownership, cheaper molecules directly widen adoption. Developers in the fuel cell market anticipate that sub-USD 2/kg hydrogen will trigger parity with diesel in long-haul fleets.

Toyota, Hyundai, and Honda have collectively pledged multi-billion-dollar roadmaps for hydrogen mobility, including supply contracts for 45,000 FCEVs over the next two years. China targets 1 million fuel-cell vehicles and 2,000 stations by 2035, while South Korea links hydrogen trucks to its national smart-grid plan. Automakers' aligned production schedules, joint ventures with energy firms, and station co-investment compress scale-up timelines. Their demand signals cascade along the fuel cell market through stack suppliers, compressor makers, and refueling integrators.

Network density remains insufficient outside the mature corridors of Japan and South Korea. Germany leads Europe with about 170 public hydrogen stations, yet coverage still trails the needs of regional trucking routes. In the U.S., only California offers a cohesive buildout plan, and pump prices of USD 12-15/kg deter fleet wide roll-outs. Infrastructure delays slow fleet conversion, stretching payback periods for early adopters and reducing overall volumes in the fuel cell market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The vehicular segment generated 80.9% of global revenue in 2024, confirming its central role within the fuel cell market. Commercial trucks, city buses, and light-duty cars rely on PEMFC architecture that delivers fast refueling and long range. Recent wholesale of 235 hydrogen trucks, coupled with bulk orders for European fuel-cell buses, signals maturing demand curves. The total cost gap versus diesel narrows as hydrogen prices fall and maintenance savings accrue.

Stationary deployments for data centers, telecom towers, and hospitals capture the remaining 19.1% share, yet post sharp growth. Hyperscale operators trial multi-megawatt installations that displace diesel gensets. These early wins suggest that the fuel cell market will balance more evenly between mobile and stationary uses after 2030 as uptime and emission credentials prove out.

PEMFC retained a 70.4% share in 2024, underpinned by passenger cars and material-handling fleets. Its low operating temperature suits frequent starts and stops, which lifts utilization rates in urban duty cycles. Stack lifetime improvements and membrane recycling programs further cement PEMFC economics.

SOFC, however, is the fastest climber with a forecast 51.1% CAGR to 2030. Electrical efficiencies near 60% and flexible fuel inputs empower utilities and data-center customers to run on pipeline gas today and hydrogen tomorrow. Bloom Energy's multi-megawatt orders underscore this inflection. As a result, the fuel cell market size for SOFC systems is expected to pass USD 20 billion by 2035, reflecting a mix of base-load replacements and microgrid applications. Alkaline, phosphoric acid, and molten carbonate fuel cells address specific industrial niches, completing the technology spectrum.

The Fuel Cell Market Report is Segmented by Application (Vehicular and Non-Vehicular), Technology (Polymer Electrolyte Membrane Fuel Cell, Solid Oxide Fuel Cell, Alkaline Fuel Cell, and Others), Fuel Type (Hydrogen, Natural Gas, Ammonia, and Others), End-User Industry (Transportation, Utilities, Commercial and Industrial, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Asia-Pacific held a 57.8% share of the fuel cell market in 2024. Japan's strategic roadmap subsidizes fuel-cell cars and residential micro-CHP units, while South Korea bundles hydrogen with smart-city initiatives. China's target of 1 million FCEVs and 2,000 stations by 2035 signals a scale unmatched elsewhere. Local governments fund electrolyzers and provide toll exemptions that cut fleet operating costs. Established automotive groups embed fuel cells across trucks, SUVs, and forklifts, locking in component demand for regional suppliers.

North America ranked second, propelled by policy tailwinds in the United States. The Clean Hydrogen Production Tax Credit and seven Regional Hydrogen Hubs mobilize billions toward electrolysis, storage, and downstream projects. California's Advanced Clean Trucks rule anchors early demand in medium- and heavy-duty fleets, while Canadian provinces support hydrogen buses. Data-center operators in Texas, Illinois, and Virginia are contracting multi-megawatt SOFC plants to bolster grid reliability, adding depth to the regional fuel cell market.

Europe leverages its Fit-for-55 climate package to stimulate fuel-cell adoption in trucks, rail, and maritime. Updated CO2 standards require a 90% cut in heavy-duty vehicle emissions by 2040, making hydrogen propulsion a credible path. Germany's 170-plus public stations lead continental coverage. The European Hydrogen Bank and Innovation Fund align bidders with grant finance, derisking scale-up for electrolyzer and stack plants. Cross-border pipeline upgrades from Spain to France pave the infrastructure for future green-hydrogen flows.

The Middle East & Africa offers the fastest growth outlook at a forecast 41.2% CAGR. Ample solar and wind resources enable competitive green-hydrogen export hubs. Egypt, the United Arab Emirates, and Saudi Arabia each map multi-gigawatt electrolyzer parks tied to ammonia production for shipping customers. Existing natural-gas pipelines and port infrastructure provide a ready platform for conversion to hydrogen blends. African economies eye local fuel-cell microgrids that stabilize weak grids and displace diesel gensets, signalling a fresh demand wave.