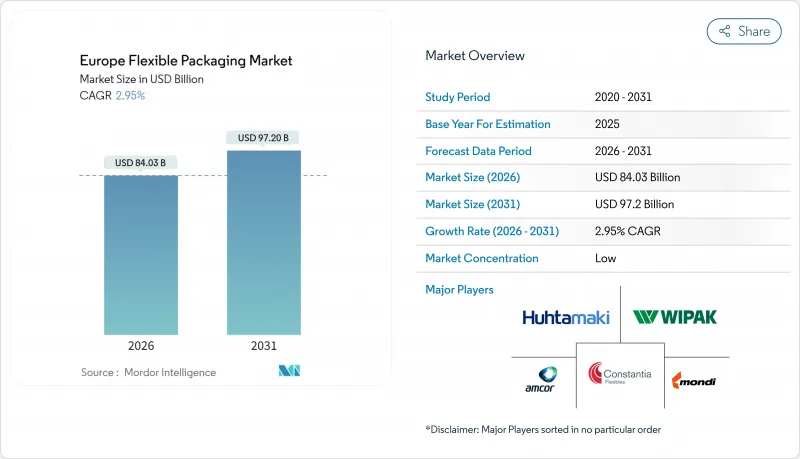

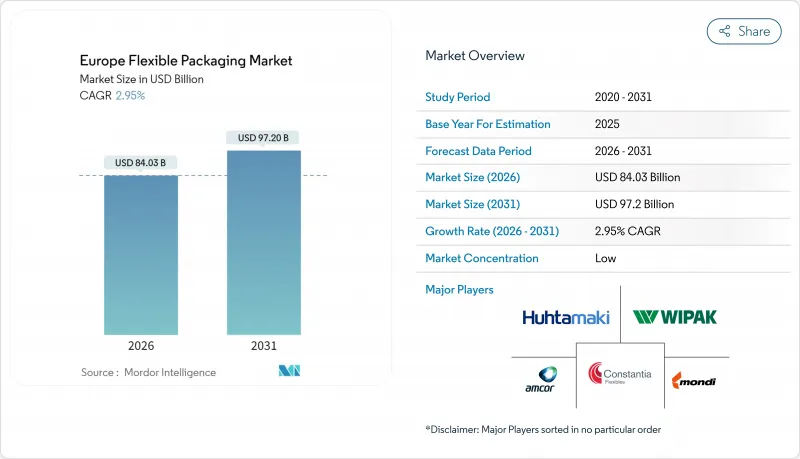

유럽의 연포장 시장 규모는 2026년 840억 3,000만 달러로 추정되며, 2025년 816억 2,000만 달러에서 성장한 수치입니다. 2031년에는 972억 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 2.95%로 성장할 전망입니다.

이 성장 궤적은 EU의 보다 엄격한 재활용 의무화, 전자상거래의 수하물 확대, 장기 보존이 필요한 편리한 식품에 대한 수요 가속에 기인합니다. 포장 및 포장폐기물 규제(PPWR)가 2030년까지 재생플라스틱 30% 함유를 추진하는 가운데, 단일소재 필름의 혁신이 가속되고 있으며, 생분해성 옵션도 소규모이면서 확대되고 있습니다. 브랜드 소유자는 물류 비용 절감을 위해 경량 파우치로의 이행을 계속하고 있습니다만, 필름이나 랩은 식품 및 공업 제품 라인에 있어서의 범용성으로부터, 여전히 수량 베이스로 주류를 차지하고 있습니다. 상위 7개 공급업체가 매출의 약 4분의 1만을 차지하고 있다는 중간 수준의 경쟁 환경은 장벽 기술과 디지털 인쇄의 틈새 기회를 지역 전문 기업이 획득할 여지를 창출하고 있습니다.

PPWR(포장 폐기물 지령)에 의해 2030년까지 유럽에서 판매되는 모든 포장은 리사이클 가능한 것이 의무화되고, 컨버터 각사는 기계적 리사이클 공정을 통과하는 단일 소재 형식에 다층 구조의 재설계를 강요되고 있습니다. 네슬레사는 반려동물 먹이용 폴리프로필렌 레토르트 파우치에 의해 탄소발자국를 60% 삭감했다고 보고, 사이카플렉스사는 2025년까지 소비 후 재생재를 포함한 완전 리사이클 가능한 제품군의 실현을 계획하고 있습니다. 종이는 재생재 함유율의 의무 대상외이기 때문에 켈러 페이퍼사의 NexPlus 배리어 라인 등 종이 베이스의 대체품이 주목을 받고 있습니다. 다층 구조의 성능 저하를 보완하기 위해, 공급자 각 사는 폴리프로필렌 기재상에서 산소 투과율을 95% 저감하는 오르모서(ORMOCER) 등의 무기 코팅을 시험 중입니다. 확대 생산자 책임 제도의 비용 부담이 비재생 가능 소재에 부과됨으로써, 채택 스케줄이 앞당겨지고 있습니다.

많은 EU 시장에서 온라인 소매는 두 자릿수 성장을 계속하고 있으며 소포 당 운송 비용을 줄이는 경량 메일 가방과 보호 필름의 채택을 촉진하고 있습니다. HP Indigo 200K와 같은 디지털 인쇄기는 계절 및 지역별 프로모션에 맞게 외장 그래픽을 개인화할 수 있어 플렉소 인쇄와 비교하여 설치 시 폐기물을 줄입니다. 우테코의 하이브리드 플랫폼 '사파이어 아쿠아'는 식품 접촉 규제를 충족하는 저이행성 수성 잉크를 사용하여 150 mpm의 속도로 1,200×1,200 DPI 인쇄를 실현합니다. 중소규모의 전자상거래 브랜드는 풀필먼트 업무를 외부 위탁하는 경향이 강해지고 있으며, 자동 포장 라인에 대응한 유연한 포맷을 선호하는 간접 유통업체를 통한 출하량이 증가하고 있습니다.

중소 컨버터 기업은 재활용 가능성의 인증 취득, 재생 수지의 통합, 조화된 표시 기준을 충족하기 위한 그래픽 재설계에 많은 투자를 하고 있습니다. 비준수 포장에 대한 확장 생산자 책임(EPR) 비용은 납품 비용을 50% 이상 증가시킬 수 있으며, 새로운 라인이 가동될 때까지 이익률을 압박합니다. 2026년에 시행되는 PFAS 금지에 의해 식품 포장용 내유성 코팅의 재배합이 강요되는 한편, 2028년 시행의 표시 규칙은 수천의 SKU에 걸친 아트워크 변경을 촉구합니다.

2025년 시점에서 유럽 연포장 시장에서의 플라스틱 점유율은 61.88%를 차지했고 식품 및 전자상거래 라인에서 폴리에틸렌의 코스트 퍼포먼스 우위성이 견인하고 있습니다. 석유 유래 기재는 현재도 주도권을 쥐고 있지만, 브랜드 오너가 PPWR에의 적합을 추구하는 가운데, 유럽 연포장 시장에서는 바이오 기반 및 퇴비화 가능 필름에 대한 관심이 높아지고 있어, CAGR5.66%로 확대중입니다. 종이 및 판지는 재생재 함유율의 의무화 대상외가 되고 있어, 켈러 페이퍼사 등공급자는 배리어 코팅을 실시한 그레이드로 81.5%의 재생 이용률을 달성해, 진전을 보이고 있습니다. 금속화 구조는 절대적인 배리어성이 요구되는 의약품이나 고급 식품 분야에서 여전히 사용되고 있지만, 틈새 수요에 따라 수량 변동의 영향을 크게 받지 않고 있습니다. PET의 화학적 재활용 기술(탈중합에 의한 버진 원료 상당의 원료화 포함)은 2027년까지 식품 등급 수지의 안정 공급을 목표로 하는 노력으로, 재활용률 목표의 상승 속에서 PET의 지위를 안정시키는 중요한 이정표가 될 수 있습니다.

유럽의 연포장 시장에서는 기존 폴리올레핀 층과 생분해성 코팅을 결합한 하이브리드 라미네이트 시험이 진행되고 있습니다. 이를 통해 보존 기간 동안 밀봉 성능을 유지하면서 토양 분해를 가속화할 수 있습니다. 투명 스낵 필름의 주력 소재는 여전히 BOPP입니다만, 레토르트 대응 뚜껑재에는 씰성이 뛰어난 CPP가 선호되고 있습니다. 바이오플라스틱은 현재 총 생산량의 극히 일부에 불과하지만, 퇴비화 가능한 쇼핑백에서 PLA, PBAT, 전분을 혼합한 고배리어 구조로 진화하고 있습니다. 컨버터 각 사는 원료의 스케일 업과 수요를 환기하는 규제가 갖추어진 2028년 이후가 아니면 화석 유래 등급과의 비용 경쟁력 달성은 어렵다고 예측했습니다.

필름 및 랩은 베이커리 제품, 치즈, 산업용 부품 등 대량 소비 카테고리에 대응하기 위해 2025년 시점에서 유럽 연포장 시장의 43.92%를 차지했습니다. 그러나 레토르트 대응 반려동물 먹이 포장이나 전자 레인지 대응 레토르트 식품 등 외출처에서의 소비 라이프 스타일에 적합한 제품에 지지되어 파우치는 2031년까지 연평균 복합 성장률(CAGR)6.55%로 확대를 계속하고 있습니다. 스탠드업 형식은 선반 스페이스의 유효 활용과 브랜드 인지도 향상에 기여해, 소매업체로부터 우대된 진열 위치를 획득하고 있습니다. 네슬레의 재활용 가능한 레토르트 파우치는 기존 구조에 비해 성능을 유지하면서 카본 실적을 60% 삭감할 수 있는 사례를 보여줍니다(Packaging Digest).

백 형식은 중량 제한으로 얇은 대체품의 채택이 어려운 농업용 종자, 비료 및 DIY 시장에서 계속 주류입니다. 디지털 인쇄 기술의 보급으로 컨버터는 5,000 단위 미만의 작은 로트에서도 SKU 단위의 커스터마이즈를 제공 가능하게 되어, 단위 경제성을 손상시키지 않고 틈새 시장 음식 브랜드가 라이프 사이클 조기부터 파우치 포장을 채택하는 움직임을 촉진하고 있습니다. 중첩 포장 및 수축 슬리브는 음료 및 의약품 분야에서 변조 방지 솔루션으로 여전히 중요하지만, 재활용 가능성에 대한 엄격한 시선이 향하고 있습니다. 유럽에서 반려동물 사육률의 두 자릿수 성장은 제품의 신선도와 향기 보호를 보장하는 레토르트 파우치와 스탠드 업 파우치에 대한 수요를 더욱 강화하고 있습니다.

Europe flexible packaging market size in 2026 is estimated at USD 84.03 billion, growing from 2025 value of USD 81.62 billion with 2031 projections showing USD 97.2 billion, growing at 2.95% CAGR over 2026-2031.

This trajectory follows tougher EU recycling mandates, expanding e-commerce parcel volumes, and accelerating demand for convenience foods that need extended shelf life. Mono-material film innovation is gathering pace as the Packaging and Packaging Waste Regulation (PPWR) pushes for 30% recycled plastic content by 2030, while biodegradable options are scaling from a small base. Brand owners continue to migrate toward lightweight pouches that cut logistics costs, yet films and wraps still dominate on volume thanks to their versatility in food and industrial lines. Moderate competitive intensity-as the seven largest suppliers together control only about one quarter of sales-creates room for regional specialists to capture niche opportunities in barrier technology and digital printing.

The PPWR obliges every package sold in Europe to be recyclable by 2030, prompting converters to redesign multilayer structures into mono-material formats that pass mechanical recycling streams. Nestle reports 60% carbon-footprint savings from polypropylene retort pouches for pet food, while Saica Flex plans a fully recyclable portfolio by 2025 that integrates post-consumer recyclate. Paper's exemption from recycled-content quotas gives a lift to paper-based alternatives such as Koehler Paper's NexPlus barrier line. To compensate for lost multilayer performance, suppliers are testing ORMOCER and other inorganic coatings that cut oxygen transmission rates by 95% on PP substrates. Extended Producer Responsibility fees now penalize non-recyclable materials, compressing timetables for adoption.

Online retail continues to expand double-digit in many EU markets, spurring uptake of lightweight mailers and protective films that reduce freight cost per parcel. Digital presses such as HP Indigo 200K allow brands to personalize outer graphics for seasonal or regional promotions, while cutting set-up waste versus flexography. Uteco's SapphireAQUA hybrid platform prints 1,200 X 1,200 DPI at 150 mpm using low-migration, water-based inks that fulfil food-contact rules. Smaller e-commerce brands increasingly outsource fulfillment, channeling more volume through indirect distributors who favor flexible formats compatible with automated packing lines.

Smaller converters face steep investments to certify recyclability, integrate recycled resin, and redesign graphics to meet harmonized labeling. Extended Producer Responsibility fees for non-compliant packs can add 50% or more to delivered cost, squeezing margins until new lines come on-stream. PFAS bans hitting in 2026 will force reformulation of grease-resistant coatings for food wraps, while labeling rules effective 2028 drive artwork changeovers across thousands of SKUs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastics contributed 61.88% of Europe flexible packaging market share in 2025, powered by polyethylene's cost-to-performance edge in food and e-commerce lines. Petro-based substrates maintain leadership today, yet the Europe flexible packaging market is witnessing brisk interest in bio-based and compostable films expanding at a 5.66% CAGR as brand owners chase PPWR alignment. Paper and paperboard enjoy an exemption from recycled-content quotas, and suppliers such as Koehler Paper are making headway with barrier-coated grades that hit 81.5% recycling rates. Metalized structures still serve pharma and premium food where absolute barrier rules, but stand largely insulated from volume swings thanks to niche demand. Chemical recycling initiatives for PET, including depolymerization to virgin-like feedstock, aim to secure food-grade resin streams by 2027, a milestone that could stabilise PET's position amid rising recycled-content targets.

Europe flexible packaging market players are trialing hybrid laminates that pair traditional polyolefin layers with biodegradable coatings to accelerate soil decomposition while preserving seal integrity during shelf life. BOPP remains the workhorse for transparent snack films, whereas CPP is favoured for retortable lidding thanks to its sealability. Bioplastics, currently a sliver of overall tonnage, are moving beyond compostable shopping bags into high-barrier structures with blending of PLA, PBAT, and starch. Converters anticipate cost parity with fossil-based grades only after 2028, pending feedstock scale-up and mandates that spur demand.

Films and wraps carried 43.92% of Europe flexible packaging market share in 2025 because they serve high-volume categories such as bakery, cheese, and industrial components. Nonetheless, pouches are clocking a 6.55% CAGR through 2031, buoyed by retortable pet-food packs and microwaveable ready meals that fit on-the-go consumer lifestyles. Stand-up formats improve shelf utilisation and brand visibility, which retailers reward with premium placement. Nestle's recyclable retort pouch illustrates how brands can cut carbon footprints by 60% versus legacy structures while maintaining performance Packaging Digest.

Bag formats continue to dominate agricultural seeds, fertilizers, and DIY markets, where bulk weight limits the appeal of thin-wall alternatives. Digital printing's rise allows converters to offer SKU-level customisation in lot sizes below 5,000 units without compromising unit economics, encouraging niche gourmet brands to adopt pouch packaging earlier in their lifecycle. Overwraps and shrink sleeves remain relevant as tamper-evidence solutions in beverages and pharmaceuticals but face scrutiny over recyclability. Double-digit growth in European pet ownership further underpins demand for retort and stand-up pouches that guarantee product freshness and aroma protection.

The Europe Flexible Packaging Market Report is Segmented by Material Type (Plastics, Paper and Paperboard, and More), Product Type (Pouches, Bags, and More), End-User Industry (Food, Beverage, Healthcare and Pharmaceuticals, and More), Distribution (Direct Sales, Indirect Sales), and Country (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).